|

市場調査レポート

商品コード

1797863

コンクリートプラント機器市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測Concrete Plant Equipment Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| コンクリートプラント機器市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測 |

|

出版日: 2025年07月25日

発行: Global Market Insights Inc.

ページ情報: 英文 125 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

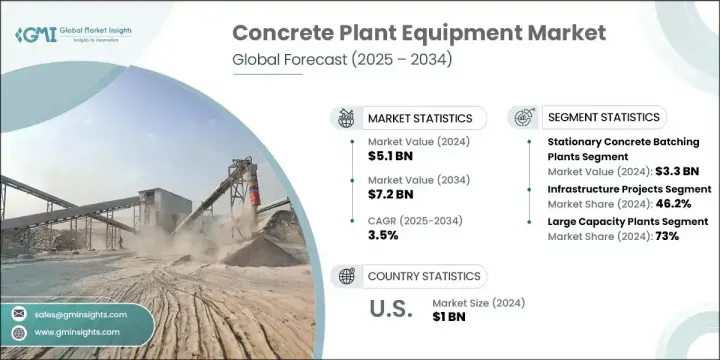

世界のコンクリートプラント機器市場は、2024年に51億米ドルと評価され、CAGR 3.5%で成長し、2034年には72億米ドルに達すると推定されています。

この成長は、急速な都市開発、インフラ投資の増加、高品質な生コンに対する需要の急増によって世界中で推進されています。政府は、交通、商業開発、公共事業などの公共事業に多額の予算を割り当てています。建設業界が効率化と革新にシフトするにつれ、コンクリートバッチプラントもスマートオートメーションやデジタル統合などの先進機能で進化しています。環境問題や規制の枠組みは、資源利用を最適化し廃棄物を最小限に抑える環境効率の高い機器の開発に影響を与えています。

企業は、より環境に優しく、よりスマートなソリューションを優先しており、排出量削減のための世界の取り組みと歩調を合わせています。新興経済圏からの需要の高まり、現場全体の自動化、モノのインターネット(IoT)対応システムの普及が、市場の再形成を後押ししています。デジタル化の推進は、作業精度の向上、エネルギーの節約、生産性の向上を促しています。業界では、持続可能でインテリジェントなバッチプラントへのシフトが見られ、環境コンプライアンスを維持しながら、大規模な建設事業のユニークなニーズを満たすように調整されています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 51億米ドル |

| 予測金額 | 72億米ドル |

| CAGR | 3.5% |

据置型バッチプラント分野は、その高効率と優れた出力能力により、2024年に64.5%のシェアを占めました。これらのプラントは、特に大規模インフラや商業開発プロジェクトに適しています。これらのプラントは、30から150立方メートル/時以上のバッチ処理能力に対応でき、コンパクトなユニットや移動式ユニットよりも性能面で優位性があります。安定した設計により、デジタル制御システムやオートメーション・ソフトウェアとのシームレスな統合が可能で、ヒューマンエラーを20%~30%削減し、生産効率を大幅に高めることができます。初期投資は高くなるが、省エネ、長期的なコスト削減、生産の安定性などの利点から、据置型プラントは継続的かつ大規模な使用に適した選択肢となっています。

2024年には、インフラプロジェクト分野が46.2%のシェアを占め、2034年までCAGR 3.7%で成長すると予測されています。インフラストラクチャーは、耐久性があり、精密に混合された大量のコンクリートに依存していることから、コンクリートバッチ装置にとって最も要求の厳しい分野であることに変わりはないです。こうしたプロジェクトでは、継続的なコンクリート消費に対応するため、最低でも毎時100立方メートルの能力を持つバッチプラントが必要とされることが多いです。このようなプロジェクトには、道路、鉄道、滑走路、橋梁、その他の公共工事が含まれます。据置型バッチプラントは、長期間にわたって安定した生産量を維持し、品質不良を最大30%削減し、プロジェクトの遅延を抑えることができるため、ここでは好まれています。

米国のコンクリートプラント機器市場は68.9%のシェアを占め、2024年には10億米ドルを生み出します。同国は、成熟したインフラストラクチャーの枠組みや、建設に対する公的・民間投資の高水準に支えられ、引き続き地域市場をリードしています。高速道路、空港、橋梁、複合商業施設などの継続的な改善により、先進的なバッチ処理機械に対する需要は旺盛です。米国の建設業者は、プラントの操業を最適化し、優れたコンクリート品質を確保するために、デジタル技術とスマートシステムへの依存度を高めています。また、規制状況が厳しいことから、メーカーや請負業者は、安全性と環境性能のベンチマークを満たす機器を採用する必要に迫られています。

世界のコンクリートプラント機器市場の競合環境を形成している主要企業は、Sany、Meka、Fangyuan、Janeoo、Zoomlion、RexCon、XCMG、Elkon、Ammann、Lintec、CON-E-CO、Liebherr、McCrory Engineering、Schwing Stetter、Putzmeisterなどです。コンクリートプラント機器分野の主要企業は、戦略的パートナーシップや現地生産を通じて、世界なプレゼンス拡大に積極的に注力しています。多くの企業は、デジタル制御、AIベースのモニタリング、IoT対応ソリューションをバッチプラントに統合することで、ポートフォリオを強化しています。これは、エンドユーザーが遠隔で生産を監視し、バッチの精度を確保するのに役立ちます。各社はまた、環境基準の強化に対応するため、水リサイクルシステム、ダスト抑制ユニット、低排出ミキサーを組み込んだ環境に優しいモデルの開発も進めています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 利益率

- 各段階での付加価値

- バリューチェーンに影響を与える要因

- 業界への影響要因

- 促進要因

- インフラ開発の増加

- 技術的進歩

- 都市化と住宅需要

- 業界の潜在的リスク&課題

- 原材料価格の変動

- 複雑なメンテナンス要件

- 機会

- 促進要因

- 成長可能性分析

- 将来の市場動向

- テクノロジーとイノベーションの情勢

- 現在の技術動向

- 新興技術

- 価格動向

- 地域別

- 植物の種類別

- 規制情勢

- 標準とコンプライアンス要件

- 地域規制枠組み

- 認証基準

- 貿易統計(HSコード-84743110)

- 主要輸入国

- 主要輸出国

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 地域別

- 企業マトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 主な発展

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

- 拡張計画

第5章 市場推計・予測:プラントタイプ別、2021年~2034年

- 主要動向

- 据置型コンクリートバッチプラント

- 移動式コンクリートバッチプラント

第6章 市場推計・予測:機器種別、2021年~2034年

- 主要動向

- コンクリートミキサー

- コンクリートポンプ

- コンクリートレーザースクリード

- その他

第7章 市場推計・予測:容量別、2021年~2034年

- 主要動向

- 小規模プラント

- 大規模プラント

第8章 市場推計・予測:自動化レベル別、2021年~2034年

- 主要動向

- マニュアル

- 半自動

- 全自動

第9章 市場推計・予測:用途別、2021年~2034年

- 主要動向

- 住宅建設

- 商業建設

- インフラプロジェクト

第10章 市場推計・予測:最終用途別2021-2034

- 主要動向

- 建設会社

- 生コンクリート製造業者

- プレキャストコンクリートメーカー

- 政府機関

第11章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- 中東・アフリカ

- アラブ首長国連邦

- 南アフリカ

- サウジアラビア

第12章 企業プロファイル

- Ammann

- CON-E-CO

- Elkon

- Fangyuan

- Liebherr

- Lintec

- McCrory Engineering

- Meka

- Putzmeister

- RexCon

- Sany

- Janeoo

- Schwing Stetter

- XCMG

- Zoomlion

The Global Concrete Plant Equipment Market was valued at USD 5.1 billion in 2024 and is estimated to grow at a CAGR of 3.5% to reach USD 7.2 billion by 2034. This growth is being propelled by rapid urban development, increasing infrastructure investment, and surging demand for high-quality ready-mix concrete across the globe. Governments are allocating large budgets toward public works, including transportation, commercial developments, and utility projects. As the construction industry shifts toward efficiency and innovation, concrete batching plants are evolving with advanced features, including smart automation and digital integration. Environmental concerns and regulatory frameworks are influencing the development of eco-efficient equipment that optimizes resource usage and minimizes waste.

Companies are prioritizing greener, smarter solutions, aligning with global initiatives to reduce emissions. Rising demand from emerging economies, automation across job sites, and the widespread adoption of Internet of Things (IoT)-enabled systems are helping reshape the market. A push for digitalization is driving higher operational accuracy, energy savings, and productivity. The industry is witnessing a shift toward sustainable and intelligent batching plants, which are being tailored to meet the unique needs of massive construction ventures while maintaining environmental compliance.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $5.1 Billion |

| Forecast Value | $7.2 Billion |

| CAGR | 3.5% |

The stationary batching plants segment held 64.5% share in 2024 due to their high efficiency and superior output capacities. These plants are particularly well-suited for large-scale infrastructure and commercial development projects. They can handle batching capacities from 30 up to over 150 cubic meters per hour, offering a performance advantage over compact and mobile units. Their stable design supports seamless integration with digital control systems and automation software, which helps reduce human errors by 20% to 30% and significantly boosts production efficiency. Although their initial investment is higher, the benefits in terms of energy savings, long-term cost reduction, and production consistency make stationary plants a preferred option for continuous, large-scale use.

In 2024, the infrastructure projects segment held 46.2% share and is forecasted to grow at a CAGR of 3.7% through 2034. Infrastructure remains the most demanding sector for concrete batching equipment, given its reliance on high volumes of durable, precision-mixed concrete. These projects often require batching plants with a minimum capacity of 100 cubic meters per hour to keep up with continuous concrete consumption. Such projects include roads, railways, runways, bridges, and other public works. Stationary batching plants are favored here due to their ability to maintain consistent output over extended periods, reduce quality defects by up to 30%, and limit project delays.

U.S. Concrete Plant Equipment Market held 68.9% share, generating USD 1 billion in 2024. The country continues to lead the regional market, supported by a mature infrastructure framework and high levels of public and private investment in construction. Ongoing improvements in highways, airports, bridges, and commercial complexes keep demand strong for advanced batching machinery. US builders increasingly rely on digital technologies and smart systems to optimize plant operations and ensure superior concrete quality. Additionally, the strict regulatory landscape pushes manufacturers and contractors to adopt equipment that meets safety and environmental performance benchmarks.

Major players shaping the competitive landscape of the Global Concrete Plant Equipment Market include Sany, Meka, Fangyuan, Janeoo, Zoomlion, RexCon, XCMG, Elkon, Ammann, Lintec, CON-E-CO, Liebherr, McCrory Engineering, Schwing Stetter, and Putzmeister. Leading companies in the concrete plant equipment space are aggressively focusing on expanding their global presence through strategic partnerships and localized manufacturing. Many firms are enhancing their portfolios by integrating digital controls, AI-based monitoring, and IoT-enabled solutions into their batching plants. This helps end-users monitor production remotely and ensure batch accuracy. Companies are also developing eco-friendly models that incorporate water recycling systems, dust suppression units, and low-emission mixers to comply with tightening environmental standards.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.3 Data collection methods

- 1.4 Data mining sources

- 1.4.1 Global

- 1.4.2 Regional/Country

- 1.5 Base estimates and calculations

- 1.5.1 Base year calculation

- 1.5.2 Key trends for market estimation

- 1.6 Primary research and validation

- 1.6.1 Primary sources

- 1.7 Forecast model

- 1.8 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Plant Type

- 2.2.3 Capacity

- 2.2.4 Automation Level

- 2.2.5 Application

- 2.2.6 End use

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.4 Critical success factors for market players

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising infrastructure development

- 3.2.1.2 Technological advancements

- 3.2.1.3 Urbanization and housing demand

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 Raw material price volatility

- 3.2.2.2 Complex maintenance requirements

- 3.2.3 Opportunities

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and Innovation Landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By region

- 3.6.2 By plant type

- 3.7 Regulatory landscape

- 3.7.1 Standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.7.3 Certification standards

- 3.8 Trade statistics (HS code -84743110)

- 3.8.1 Major importing countries

- 3.8.2 Major exporting countries

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East and Africa

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates & Forecast, By Plant Type, 2021 - 2034 ($ Bn, Units)

- 5.1 Key trends

- 5.2 Stationary concrete batching plants

- 5.3 Mobile concrete batching plants

Chapter 6 Market Estimates & Forecast, By Equipment Type, 2021 - 2034 ($ Bn, Units)

- 6.1 Key trends

- 6.2 Concrete mixers

- 6.3 Concrete pumps

- 6.4 Concrete laser screeds

- 6.5 Others

Chapter 7 Market Estimates & Forecast, By Capacity, 2021 - 2034 ($ Bn, Units)

- 7.1 Key trends

- 7.2 Small-capacity plants

- 7.3 Large-capacity plants

Chapter 8 Market Estimates & Forecast, By Automation Level, 2021 - 2034 ($ Bn, Units)

- 8.1 Key trends

- 8.2 Manual

- 8.3 Semi-automatic

- 8.4 Fully automatic

Chapter 9 Market Estimates & Forecast, By Application 2021 - 2034 ($ Bn, Units)

- 9.1 Key trends

- 9.2 Residential construction

- 9.3 Commercial construction

- 9.4 Infrastructure projects

Chapter 10 Market Estimates & Forecast, By End Use 2021 - 2034 ($ Bn, Units)

- 10.1 Key trends

- 10.2 Construction companies

- 10.3 Ready-mix concrete producers

- 10.4 Precast concrete manufacturers

- 10.5 Government organizations

Chapter 11 Market Estimates & Forecast, By Region, 2021 - 2034 ($ Bn, Units)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 UK

- 11.3.2 Germany

- 11.3.3 France

- 11.3.4 Italy

- 11.3.5 Spain

- 11.3.6 Russia

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 Australia

- 11.4.5 South Korea

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.6 MEA

- 11.6.1 UAE

- 11.6.2 South Africa

- 11.6.3 Saudi Arabia

Chapter 12 Company Profiles

- 12.1 Ammann

- 12.2 CON-E-CO

- 12.3 Elkon

- 12.4 Fangyuan

- 12.5 Liebherr

- 12.6 Lintec

- 12.7 McCrory Engineering

- 12.8 Meka

- 12.9 Putzmeister

- 12.10 RexCon

- 12.11 Sany

- 12.12 Janeoo

- 12.13 Schwing Stetter

- 12.14 XCMG

- 12.15 Zoomlion