インドネシアの生コンクリート:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)

Indonesia Ready Mix Concrete - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 178 Pages

- 納期

- 2~3営業日

- 商品コード

- 1687957

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

インドネシアの生コンクリート市場規模は2024年に1億722万立方メートルと推定・予測され、2030年には1億6,240万立方メートルに達し、予測期間(2024~2030年)のCAGRは7.16%で成長すると予測されます。

トランジットミックスタイプが商業セクターにおけるインドネシア生コンクリート市場の成長を牽引

- すべてのセクターにおいて、2022年のインドネシアの生コンクリート需要は、現場打ちミックスコンクリートの使用が増えたため、2021年より大幅に減少しました。この結果、2022年の同国全体の生コンクリート消費量は2021年と比較して15.7%減少しました。しかし2023年には、住宅や商業などすべての最終用途部門で高い成長が見込まれたため、全体の消費量は2022年比で21.4%増加すると推定されました。

- インドネシアにおける生コンクリートモルタルの消費量は、住宅部門が最も多いです。例えば、2022年には、住宅部門はインドネシア全体の生コンクリート消費量の約40%のシェアを占めています。同部門で最も好まれる生コンクリートのタイプはトランジットミックスで、2022年の消費量の76%を占めました。

- 住宅に次いで建設面積が大きいため、インドネシアで最も生コンクリート消費量が多いのは産業・施設部門です。例えば、2022年には、工業・施設部門が国内の新設床面積の31%を占める。同部門におけるシュリンクミックスタイプの生コンクリート需要は、予測期間(2023~2030年)に最速のCAGR 8.3%を記録すると予想されます。

- インドネシアの生コンクリート需要全体は、予測期間中に商業セクターで最速のCAGR 8.94%を記録し、成長すると予測されます。これは主に、予測期間中にCAGR 9.20%の成長が見込まれるトランジットミックスの使用によるものです。トランジットミックスは2022年に同国の生コンクリート需要の73%を占めました。

インドネシアの生コンクリート市場動向

インドネシアの商業用不動産市場規模は2028年までに1兆3,900億米ドルに達すると予測され、商業セクターの需要が増大する可能性が高い

- 2022年、インドネシアの新規商業床面積は前年比9.7%減となりました。この落ち込みは、COVID-19パンデミック時の建築活動の落ち込みから平常に戻った結果です。パンデミック以前から、インドネシアの商業ビルの年間エネルギー原単位は低下傾向を示しており、その割合は年率2.64%でした。しかし、2023年には回復が見られ、新しいオフィス、倉庫、小売スペースを必要とする外国直接投資(FDI)の急増が原動力となって、新しい商業床面積が5.7%増加しました。

- COVID-19が大流行する中、2020年と2021年にインドネシアは、約960万平方フィートを占める新規商業床面積の大幅な急増を示しました。政府が経済活性化に注力した結果、民間・公共プロジェクトともに建設関連の検疫が緩和されるなどの措置がとられました。これにより、従業員は現場での仕事を再開し、企業は事業を継続できるようになりました。特筆すべきは、インドネシアの完成工事高が2020年には約1兆3,200億IDRに達し、2021年には1兆4,200億IDRに増加することです。

- インドネシアの新規商業床面積は、2023年比で2030年までに約58.72%の大幅な伸びが予測されています。この急増は、ショッピングモール、オフィス、その他の商業スペースに対する需要の高まりによるものです。小売不動産セグメントは、同国で特に魅惑的なセクターとして浮上しています。例えば、商業用不動産市場の規模は、2028年までに1兆3,900億米ドルに達すると予想されています。インドネシアの商業用新設床面積は、予測期間中にCAGR 6.82%を記録し、安定した成長を維持すると予想されます。

住宅需要の増加が住宅セクターの成長を促進する可能性が高い

- 2022年、インドネシアの住宅新設床面積は2021年比で7.10%の伸びを示しました。この急増は、人口増加、富裕化、都市化に起因しています。政府主導の住宅支援は2022年に29兆インドルピーに達し、住宅融資流動性ファシリティ・スキームの下、2023年には32兆インドルピーに増加すると予測されました。このイニシアチブは、少なくとも22万戸の住宅建設を目指しています。住宅建設セクターは著しい成長を遂げる見込みです。2023年には前年比で約5,600万平方フィートに増加すると推定されます。

- 2020年、インドネシアの住宅新築床面積は2019年比で7.06%増加しました。これは政府による戦略的な動きで、景気後退を緩和し、収入減に悩む家計を支援するために建設を優先させました。その結果、検疫を含む建設活動の制限が大幅に緩和されました。しかし、2021年には動向が逆転し、住宅着工床面積は約12.54%減少しました。これは主に、建設部門への外国直接投資(FDI)の落ち込みに起因します。2021年の建設へのFDIは前年比51%減となりました。

- インドネシアの住宅新設床面積は、予測期間中、数量ベースでCAGR 6.08%の成長が見込まれます。この成長は、政府のイニシアティブと国内外の投資によって後押しされた、同国の都市化の進展に起因します。これらの要因は、直接的・間接的に、同国における住宅ニーズの高まりを強調し、最終的に住宅建設を促進します。急増する需要を満たすには、2030年までに年間82万戸から100万戸の住宅が必要になると予測されています。

インドネシア生コンクリート業界の概要

インドネシアの生コンクリート市場は断片化されており、上位5社で7%を占めています。この市場の主要企業は以下の通りです。 Heidelberg Materials, PT Cemindo Gemilang Tbk, PT Waskita Beton Precast Tbk, SCG and SIG(sorted alphabetically).

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 エグゼクティブサマリーと主な調査結果

第2章 レポートのオファー

第3章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 調査手法

第4章 主要産業動向

- 最終用途分野の動向

- 商業

- 産業・施設

- インフラ

- 住宅

- 主要インフラプロジェクト(現在および発表済み)

- 規制の枠組み

- バリューチェーンと流通チャネル分析

第5章 市場セグメンテーション

- 最終用途分野

- 商業

- 産業・施設

- インフラ

- 住宅

- 製品

- セントラルミックス

- シュリンクミックス

- トランジットミックス

第6章 競合情勢

- 主要な戦略動向

- 市場シェア分析

- 企業情勢

- 企業プロファイル

- Heidelberg Materials

- Kalla Group.

- PT Cemindo Gemilang Tbk

- PT Waskita Beton Precast Tbk

- PT. Adhimix Precast Indonesia

- PT. Beton Indotama Surya

- PT. Fresh Beton Indonesia

- PT. Modernland Realty Tbk.

- SCG

- SIG

第7章 CEOへの主な戦略的質問

第8章 付録

- 世界概要

- 概要

- ファイブフォース分析フレームワーク(産業魅力度分析)

- 世界のバリューチェーン分析

- 市場力学(DROs)

- 情報源と参考文献

- 図表一覧

- 主要洞察

- データパック

- 用語集

目次

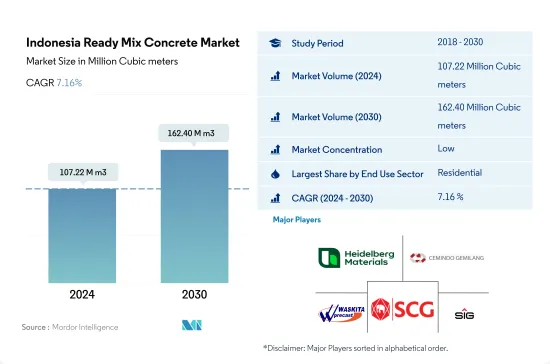

The Indonesia Ready Mix Concrete Market size is estimated at 107.22 million Cubic meters in 2024, and is expected to reach 162.40 million Cubic meters by 2030, growing at a CAGR of 7.16% during the forecast period (2024-2030).

Transit mixed type to drive the growth of the Indonesian ready mix concrete market in the commercial sector

- Across all sectors, the demand for ready mix concrete in Indonesia in 2022 was significantly lower than in 2021 due to more use of on-site mix concrete. This resulted in the country's overall consumption of ready mix concrete being 15.7% lower in 2022 compared to 2021. However, in 2023, as high growth was anticipated across all end-use sectors, such as residential and commercial, the overall consumption was estimated to grow by 21.4% compared to 2022.

- The residential sector accounts for the highest consumption volume of ready mix mortar in Indonesia. For instance, in 2022, the residential sector held a share of around 40% of the total ready mix concrete volume consumption across Indonesia. The most preferred type of ready mix concrete in the sector is transit mixed, which accounted for 76% of the consumption in 2022.

- After residential, the highest volume of ready mix concrete in Indonesia is consumed in the industrial & institutional sector as it has the largest construction area after residential. For instance, in 2022, the industrial & institutional sector accounted for 31% of the total new floor area of the country. The demand for shrink-mixed type ready mix concrete in the sector is expected to record the fastest CAGR of 8.3% during the forecast period (2023-2030).

- The overall demand for ready mix concrete in Indonesia is anticipated to grow, with the fastest CAGR of 8.94% in the commercial sector during the forecast period. This is mainly due to the usage of transit mix in the sector, which is expected to grow with a CAGR of 9.20% during the forecast period. Transit mix accounted for 73% of the country's ready mix concrete demand in 2022.

Indonesia Ready Mix Concrete Market Trends

Indonesian commercial real estate market volume is projected to reach USD 1.39 trillion by 2028 and is likely to augment the demand for commercial sector

- In 2022, Indonesia witnessed a 9.7% decline in the volume of new commercial floor area compared to the previous year. This drop was a result of a return to normalcy following a decline in building activities during the COVID-19 pandemic. Even before the pandemic, commercial buildings in Indonesia were already showing a downward trend in annual energy intensity, accounting for a rate of 2.64% per year. However, in 2023, the country saw a rebound, registering a 5.7% increase in the volume of new commercial floor area, driven by a surge in foreign direct investment (FDI) necessitating new offices, warehouses, and retail spaces.

- Amidst the COVID-19 pandemic, in 2020 and 2021, Indonesia witnessed a significant surge in the volume of new commercial floor area, accounting for approximately 9.6 million square feet. The government's focus on revitalizing the economy led to measures such as easing construction-related quarantines, both in private and public projects. This allowed employees to resume work on-site and companies to continue their operations. Notably, the value of completed constructions in Indonesia stood at around IDR 1.32 quadrillion in 2020 and rose to IDR 1.42 quadrillion in 2021.

- The volume of new commercial floor area in Indonesia is projected to witness a robust growth of around 58.72% by 2030 compared to 2023. This surge is driven by a rising demand for shopping malls, offices, and other commercial spaces. The retail real estate segment is emerging as a particularly captivating sector in the country. For instance, the volume of the commercial real estate market is anticipated to reach USD 1.39 trillion by 2028. The commercial new floor area in Indonesia is expected to maintain steady growth, registering a CAGR of 6.82% during the forecast period.

Increase in demand for housing units is likely to augment the residential sector's growth

- In 2022, Indonesia witnessed a 7.10% volume growth in residential new floor area compared to 2021. This surge can be attributed to increased population, wealth, and urbanization. The government-led housing aid reached IDR 29 trillion in 2022, which was projected to increase to IDR 32 trillion in 2023 under the Housing Financing Liquidity Facility scheme. This initiative aims to construct at least 220 thousand houses. The residential construction sector is poised to witness a significant growth rate. It was estimated to increase to approximately 56 million square feet in 2023 compared to the preceding year.

- In 2020, the volume of residential new floor areas in Indonesia grew by 7.06% compared to 2019. This was a strategic move by the government, prioritizing construction to mitigate the economic downturn and support households grappling with reduced incomes. Consequently, restrictions on construction activities, including quarantines, were significantly eased. However, in 2021, the trend reversed, with a decline of about 12.54% in residential new floor area, primarily attributed to a dip in foreign direct investment (FDI) in the construction sector. FDI for construction plummeted by 51% in 2021 compared to the previous year.

- The residential new floor area in Indonesia is projected to witness a CAGR of 6.08% in volume during the forecast period. This growth stems from the country's increasing urbanization, bolstered by government initiatives and foreign and domestic investments. These factors, directly and indirectly, underscore the mounting housing needs in the nation, ultimately driving residential building construction. Projections indicate that to meet the escalating demand, the country would require between 820,000 and 1 million housing units annually by 2030.

Indonesia Ready Mix Concrete Industry Overview

The Indonesia Ready Mix Concrete Market is fragmented, with the top five companies occupying 7%. The major players in this market are Heidelberg Materials, PT Cemindo Gemilang Tbk, PT Waskita Beton Precast Tbk, SCG and SIG (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 End Use Sector Trends

- 4.1.1 Commercial

- 4.1.2 Industrial and Institutional

- 4.1.3 Infrastructure

- 4.1.4 Residential

- 4.2 Major Infrastructure Projects (current And Announced)

- 4.3 Regulatory Framework

- 4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size, forecasts up to 2030 and analysis of growth prospects.)

- 5.1 End Use Sector

- 5.1.1 Commercial

- 5.1.2 Industrial and Institutional

- 5.1.3 Infrastructure

- 5.1.4 Residential

- 5.2 Product

- 5.2.1 Central Mixed

- 5.2.2 Shrink Mixed

- 5.2.3 Transit Mixed

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 Heidelberg Materials

- 6.4.2 Kalla Group.

- 6.4.3 PT Cemindo Gemilang Tbk

- 6.4.4 PT Waskita Beton Precast Tbk

- 6.4.5 PT. Adhimix Precast Indonesia

- 6.4.6 PT. Beton Indotama Surya

- 6.4.7 PT. Fresh Beton Indonesia

- 6.4.8 PT. Modernland Realty Tbk.

- 6.4.9 SCG

- 6.4.10 SIG

7 KEY STRATEGIC QUESTIONS FOR CONCRETE, MORTARS AND CONSTRUCTION CHEMICALS CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework (Industry Attractiveness Analysis)

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 178 Pages

- 納期

- 2~3営業日