|

市場調査レポート

商品コード

1693676

北米のレディーミクストコンクリート:市場シェア分析、産業動向、成長予測(2025~2030年)North America Ready-Mix Concrete - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 北米のレディーミクストコンクリート:市場シェア分析、産業動向、成長予測(2025~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 100 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

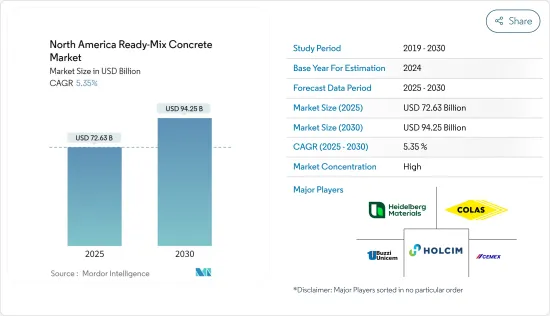

北米のレディーミクストコンクリート市場規模は2025年に726億3,000万米ドルと推定され、予測期間(2025~2030年)のCAGRは5.35%で、2030年には942億5,000万米ドルに達すると予測されます。

COVID-19の大流行は、建築・建設産業のような労働集約型産業に大打撃を与えました。しかし、社会的距離を置くための規範や監禁に関するすべての制限が解除されたことで、この地域は現在、回復への道を進んでいます。

主要ハイライト

- RMCの潜在的な利点や通常のコンクリートよりも優れた特性に対する認識の高まりとともに、この地域全体の建築需要の高まりが、この地域の市場成長を促進すると予想されます。

- その反面、RMCの輸送に関連する課題とともに、潜在的な代替品の入手が容易であることが市場成長の妨げになる可能性があります。

- しかし、インフラ開発への投資が増加しているため、地域全体で建設活動が増加しており、それによって将来的にレディーミクストコンクリート市場に潜在的な機会を提供しています。

- 予測期間中、米国は北米のレディーミクストコンクリート市場のリーダーになると予想されます。

北米のレディーミクストコンクリート市場動向

成長の大きな可能性を示す住宅セグメント

- 北米地域では、住宅開発が有望視されており、米国やカナダなどの主要経済諸国ではすでに様々なプロジェクトが発表・開始されています。

- 住宅建設で見られるレディーミクストコンクリートクリートの用途は、縁石敷きと裏打ち、補強と非補強基礎、平屋と二階建て増築、補強と非補強住宅床、いかだ、ガレージ、浄化槽敷き、溝盛り土、庭の物置と壁、排水工事、外部庭エリア、大型貨物車(HGV)駐車場と車道、小道、階段、外部舗装、温室、パティオ、温室のハードスタンドと土台です。

- 住宅建設のための不動産市場における政府支出の増加は、高級住宅への需要の高まりとともに、調査した市場の成長に利益をもたらすと考えられます。官民双方による手ごろな価格の住宅への注目の高まりが、この地域における住宅建設セクタの成長を牽引しています。

- 米国とカナダの一部の地域では、中流住宅層が低迷しているもの(手頃な価格で購入できる住宅が減り続けているため)、住宅ローンの低金利が住宅建設を増加させています。

- カナダでは、アフォーダブル・ハウジング・イニシアチブ(AHI)、ニュー・ビルディング・カナダ・プラン(NBCP)、メイドインカナダなど、さまざまな政府プロジェクトが住宅セクタの拡大を大きく後押しし、住宅セクタにおける建築用塗料・コーティングの使用を促進しています。

- さらに、ハーバード大学住宅研究共同センター(Harvard Joint Center for Housing Studies)によると、米国人は住宅の改築や修繕に年間4,000億米ドル以上を費やしていると推定されており、これには建築用塗料やコーティングが使用される可能性があり、需要にプラスの影響を与えています。

- 米国国勢調査局によると、米国における民間部門の新築住宅生産額は2022年に約9,000億米ドルに達し、3年連続で堅調な伸びを示しました。この動向は建築許可件数にも反映されており、テキサス州ダラス・フォートワース・アーリントン都市圏の住宅建設件数は国内最大級です。

- さらに、2023年3月には、季節調整済み年間ベースで141万3,000戸の個人所有住宅が建築許可を受けました。これは2023年2月改定値の155万件より8.8%低く、2022年3月の187.9万件より24.8%低いです。3月の一戸建て認可件数は81.8万件で、2月の改定値78.6万件より4.1%増加しました。2023年3月には、5戸以上の建物の認可件数は54万3,000件でした。

- したがって、前述の要因により、住宅産業向けのレディーミクストコンクリート需要が予測期間中の市場成長に影響を与える可能性が高いです。

市場を独占する米国

- 米国の建設部門は、住宅建設とインフラ建設が大きな注目と投資を集めており、大きな将来性を示しています。

- 米国は、760万人以上を雇用する巨大な建設部門を誇っています。商業、工業、施設、住宅、インフラ、エネルギー、公共事業の建設で重要な役割を果たしており、同国の建設部門は同国経済に大きく貢献しています。経済分析局によると、2022年、米国のGDPに占める建設部門の割合は、前年の4.1%から4%に低迷しました。

- 米国国勢調査局によると、2023年2月中の同国の建設支出は、季節調整済み年率1兆8,441億米ドルと推定され、2023年1月改定値の1兆8,451億米ドルを0.1%下回りました。

- さらに、米国国勢調査局によると、2022年の米国の民間建設支出は公共建設支出の約4倍の伸び率でした。50州全体の建築支出を見ると、テキサス州とカリフォルニア州がトップです。予測によれば、米国の新築建物の価値は今後も上昇し続ける。

- 同様に、2023年2月の米国内の民間建設は、季節調整済年率1兆4,500億米ドルと推定され、住宅建設は季節調整済年率8,521億米ドルと評価され、1月に修正された推定値8,570億米ドルを0.6%下回りました。2023年2月の非住宅建設は、季節調整済年率6,010億米ドルで、1月改定値の5,967億米ドルを0.7%上回りました。

- 米国では住宅の新築に加え、大規模な改築も行われています。同国では移民人口が増加しており、リフォームの必要性がますます高まっています。また、持続可能性や高効率構造に対する意識の高まりも、修復動向に拍車をかけています。政府による複数の融資が利用できることも、同国の住宅リフォームを支えています。

- AIA(米国建築家協会)の建設コンセンサス予測パネルによると、2022年の非住宅建築支出は5.4%に拡大しました。さらに、米国の新規民間非住宅建築物への支出は、2022年に5,390億米ドル超でピークに達しました。2023年までには、主要な商業・工業・施設カテゴリーはすべて、少なくともそれなりに健全な伸びを示すと予測されています。

- 2022年5月、米国ホルシムはグレーターバトンルージュ地域の著名なレディーミクストコンクリート会社ケイジャン・レディミックスコンクリートを買収しました。この買収により、ホルシムはバトンルージュとその周辺都市にサービスを提供する51台のミキサー車と8つの州認定バッチプラントを利用できるようになりました。

- さらに2022年5月、マーティン・マリエッタ・マテリアルズ社は、西海岸のセメント・レディーミクストコンクリートクリート事業の一部を売却し、現金2億5,000万米ドルでカルポートランド社に売却する最終契約を締結しました。取引完了後、カルポートランド社はレディングのセメント工場、関連するセメント配送ターミナル、カリフォルニア州にある14のレディーミクストコンクリートクリート工場を利用できるようになります。

- これらの要因は、住宅とインフラ開拓が今後数年で強力に推進される可能性があり、それによってこの地域のレディーミクストコンクリート市場が強化されることを示しています。

北米のレディーミクストコンクリート産業概要

北米のレディーミクストコンクリート市場は、その性質上、統合されています。同市場の主要企業には、CEMEX SAB de CV、HOLCIM、Buzzi Unicem SpA、HeidelbergCementAG、Colasなどがあります。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 促進要因

- 地域全体での建築需要の高まり

- 通常のコンクリートよりも優れた特性と利点

- 抑制要因

- 潜在的な代替品の入手の容易さ

- バリューチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の程度

第5章 市場セグメンテーション

- エンドユーザー部門別

- 住宅用

- 商業

- 産業/施設

- インフラ

- 地域別

- 米国

- カナダ

- メキシコ

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 市場シェア(%)**/ランキング分析

- 主要企業の戦略

- 企業プロファイル

- BuzziUnicem SpA

- CEMEX SAB de CV

- Colas Group

- CRH

- GCC諸国

- HeidelbergCement

- HOLCIM

- R.W. Sidley, Inc.

- Sika AG

- Thomas Concrete Group

- Titan Cement

- Vicat SA

- Vulcan Materials

第7章 市場機会と今後の動向

- 地域における商業インフラ開発投資の増加

The North America Ready-Mix Concrete Market size is estimated at USD 72.63 billion in 2025, and is expected to reach USD 94.25 billion by 2030, at a CAGR of 5.35% during the forecast period (2025-2030).

The COVID-19 pandemic wreaked havoc on labor-intensive industries like the building and construction industry. However, with all restrictions on social distancing norms and lockdowns lifted, the region is now progressing on the path to recovery.

Key Highlights

- The growing demand for building construction across the region, along with the rising awareness about the potential advantages and superior properties of RMC over normal concrete, is expected to drive regional market growth.

- On the flip side, the easy availability of potential substitutes, along with the challenges associated with the transportation of RMC, may hamper the market growth.

- However, the rising investments in infrastructure development are resulting in increasing construction activities across the region, thereby providing potential opportunities to the ready-mix concrete market in the future.

- The United States is expected to the leader in the North American ready-mix concrete market during the forecast period.

North America Ready-Mix Concrete Market Trends

Residential Segment Showing Great Potential for Growth

- In the North American region, residential development looks promising, with various projects already announced and initiated across major economies like the United States and Canada.

- The applications of ready-mix concrete found in residential construction are curb bedding and backing, reinforced and unreinforced foundations, single and double-story extensions, reinforced and unreinforced house floors, raft, garage, and septic tank bedding, trench fill, garden shed and wall, drainage works, external yard areas, heavy goods vehicle (HGV) parking and driveways, paths, steps, and external paving, and hard standings and bases for greenhouses, patios, and conservatories.

- The increased government spending in the real estate market for residential construction, along with the growing demand for high-class residential homes, are likely to benefit the growth of the market studied. The increased focus on affordable housing by both the public and private sectors is driving the residential construction sector's growth in the region.

- Though the middle-class housing segment is suffering a slump in a few regions of the United States and Canada (as they keep losing ground on affordability), low interest rates for home mortgages have increased residential construction.

- In Canada, various government projects, including the Affordable Housing Initiative (AHI), the New Building Canada Plan (NBCP), and Made in Canada, are set to support the expansion of the sector hugely, thereby driving the use of architectural paints and coatings in the residential sector.

- Furthermore, as per the Harvard Joint Center for Housing Studies, it is estimated that Americans spend more than USD 400 billion a year on residential renovations and repairs, which might as well involve the use of architectural paints and coatings, which positively affects their demand.

- According to the US Census Bureau, the private sector's production of new house building in the United States reached approximately USD 900 billion in 2022, marking the third year of robust growth in a row. This trend is mirrored in the number of dwelling units authorized by building permits, with the Dallas-Fort Worth-Arlington metropolitan area in Texas having some of the largest residential construction production in the country.

- Additionally, in March 2023, 1,413,000 privately owned homes had building permits authorized on a seasonally adjusted annual basis. It was 8.8% lower than the revised February 2023 rate of 1,550,000 and 24.8% lower than the March 2022 rate of 1,879,000. Single-family authorizations were 818,000 in March, up by 4.1% from the revised February figure of 786,000. In March 2023, there were 543,000 authorizations for units in buildings with five or more units.

- Therefore, owing to the aforementioned factors, the demand for ready-mix concrete for the residential industry is likely to impact market growth during the forecast period.

United States to Dominate the Market

- The United States construction sector shows great promise, with residential and infrastructure construction drawing substantial attention and investment.

- The United States boasts a colossal construction sector that employs over 7.6 million people. It plays a prominent role in commercial, industrial, institutional, residential, infrastructure, energy, and utility construction; the construction sector in the country exhibits a significant contribution to the country's economy. As per the Bureau of Economic Analysis, in 2022, the share of the US construction sector in the country's GDP slumped to 4% from 4.1% in the past year.

- According to the US Census Bureau, during February 2023, construction spending in the country was estimated at a seasonally adjusted annual rate of USD 1,844.1 billion, 0.1% lower than the revised January 2023 estimate of USD 1,845.1 billion.

- Moreover, according to the US Census Bureau, in 2022, private construction spending in the United States grew at a rate roughly four times that of public construction spending. When looking at building spending throughout the 50 states, Texas and California came out on top. According to projections, the value of new buildings in the United States will continue to rise in the coming years.

- Similarly, in February 2023, private construction in the country was estimated at a seasonally adjusted annual rate of USD 1.45 trillion, with residential construction assessed at a seasonally adjusted annual rate of USD 852.1 billion, 0.6% lower than the revised January estimate of USD 857.0 billion. Nonresidential construction remained at a seasonally adjusted annual rate of USD 601.0 billion in February 2023, 0.7% higher than the revised January 2023 estimate of USD 596.7 billion.

- In addition to new home construction, the United States is doing massive home renovations. With the growing population of migrants in the country, the need for renovation has become increasingly important. Also, the growing awareness toward sustainability and high-efficiency structures has created a spur in the restoration trend. The availability of several loans by the government also supports home remodeling in the country.

- According to the AIA (American Institute of Architects) Construction Consensus Forecast Panel, non-residential building construction spending expanded to 5.4% in 2022. Further, US expenditure on new private non-residential buildings peaked at over USD 539 billion in 2022. By 2023, all the major commercial, industrial, and institutional categories are projected to witness at least reasonably healthy gains.

- In May 2022, Holcim US acquired a prominent ready-mix concrete company in the Greater Baton Rouge Area, Cajun Ready-Mix Concrete, to further expand its reach in Louisiana through enhanced capacity to serve its customers. The acquisition allowed Holcim to have access to 51 mixer trucks and eight state-certified batch plants that serve Baton Rouge and surrounding cities.

- Further, in May 2022, Martin Marietta Materials Inc. entered into a definitive agreement to divest certain West Coast cement and ready-mixed concrete operations and sell them to CalPortland Company for a transaction of USD 250 million in cash. On completion of the transaction, CalPortland Company will have access to the Redding cement plant, related cement distribution terminals, and 14 ready-mixed concrete plants located in California.

- These factors indicate that residential and infrastructure development may potentially gain strong traction in the coming years, thereby strengthening the market for ready-mix concrete in the region.

North America Ready-Mix Concrete Industry Overview

The North American ready-mix concrete market is consolidated in nature. Some of the key players in the market include CEMEX SAB de CV, HOLCIM, Buzzi Unicem SpA, HeidelbergCementAG, Colas, and others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Growing Demand for Building Construction across The Region

- 4.1.2 Superior Properties and Advantages Over Normal Concrete

- 4.2 Restraints

- 4.2.1 Easy Availability of Potential Subsitutes

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value)

- 5.1 By End-user Sector

- 5.1.1 Residential

- 5.1.2 Commercial

- 5.1.3 Industrial/Institutional

- 5.1.4 Infrastructure

- 5.2 By Geography

- 5.2.1 United States

- 5.2.2 Canada

- 5.2.3 Mexico

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%) **/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 BuzziUnicem SpA

- 6.4.2 CEMEX SAB de CV

- 6.4.3 Colas Group

- 6.4.4 CRH

- 6.4.5 GCC

- 6.4.6 HeidelbergCement

- 6.4.7 HOLCIM

- 6.4.8 R.W. Sidley, Inc.

- 6.4.9 Sika AG

- 6.4.10 Thomas Concrete Group

- 6.4.11 Titan Cement

- 6.4.12 Vicat SA

- 6.4.13 Vulcan Materials

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Rising Investment in Commercial and Infrastructure Development in the Region