eコマース用耐熱包装市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測

E-Commerce Heat-Resistant Packaging Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 185 Pages

- 納期

- 2~3営業日

- 商品コード

- 1797693

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

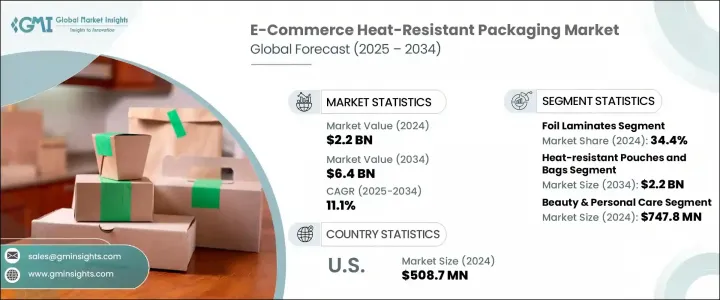

eコマース用耐熱包装の世界市場規模は2024年に22億米ドルとなり、CAGR 11.1%で成長し、2034年には64億米ドルに達すると予測されています。

市場拡大の主な要因は、eコマースの継続的な成長と製薬業界における熱保護のニーズの高まりです。オンライン購入や国際配送の急増に伴い、さまざまな温度条件下で製品の完全性を維持できる包装に対する需要が大幅に増加しています。消費者は、特に食品、パーソナルケア用品、温度に敏感な電子機器の安全な配送に関して、信頼性と持続可能性を求めています。包装ソリューションは現在、保温性を提供するだけでなく、環境にやさしく、現代の顧客の期待に沿うものでなければならないです。家庭へのヘルスケア配送が増加し、医薬品サプライヤーのデジタルプレゼンスが高まっていることも、断熱包装の需要に拍車をかけています。

生物製剤やインスリンのような重要な製品の規制遵守と温度管理も、輸送中の安全な配送のために先進的な断熱パッケージング技術の採用をメーカーに促しています。これらの繊細な医薬品は、有効性を維持し、劣化を避けるために、ロジスティクスチェーン全体を通して、多くの場合2℃~8℃の温度範囲を厳守する必要があります。世界の規制機関が医薬品のコールドチェーンの完全性に関するガイドラインを強化する中、メーカーは正確で有効な温度性能を提供する包装ソリューションの導入にますます迫られています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 22億米ドル |

| 予測金額 | 64億米ドル |

| CAGR | 11.1% |

フォイルラミネート分野は2024年に34.4%を占め、最大のシェアを占めました。これらの素材は、優れた断熱性能と最小限の重量により、包装業界の定番となりつつあります。温度に敏感な分野での用途は、特に国際輸送で拡大しています。多層フォイル技術の新たな開発により保温性と耐性が向上し、長期の輸送期間中や変動する気候条件下でより優れた保護を提供しています。

飲食品分野は2034年までCAGR 12.3%で成長すると予測されます。大都市圏におけるライフスタイルの変化、新鮮な食事に対する需要の高まり、料理の世界化はすべて、堅牢な耐熱性包装への要求を強めています。迅速かつ即日配達サービスの採用が増加しているため、サプライチェーン全体で一貫した温度管理がこの分野の企業にとって最優先事項となっています。

米国eコマース用耐熱包装市場は、2024年に5億870万米ドルを創出しました。その優位性は、持続可能なロジスティクス戦略と高度なコールドチェーンシステムの成功に起因します。製造業、飲食品、医薬品など様々な業界が、環境目標を達成するためにリサイクル可能な断熱フォームや環境に配慮した包装を採用しています。エネルギー効率の高いパッケージング・オプションに重点を置く同国の姿勢は、この分野における同国のリーダー的地位を形成し続けています。

eコマース用耐熱包装市場の主要企業には、LD Packaging、DS Smith、Insulated Products Corporation、Novolex、Amcor、Aspect Solutions、Nordic Cold Chain Solutions、DBS Packagingなどがあります。この分野の企業は、熱効率と環境持続性を兼ね備えた素材を開発するため、研究開発に積極的に投資しています。各ブランドは、環境に優しいソリューションを求める消費者の嗜好に合わせて、リサイクル可能で再利用可能な断熱製品を導入しています。また、多くの企業がeコマースやロジスティクス・プロバイダーと戦略的パートナーシップを結び、過酷な気象条件下でのラストワンマイル配送に対応した包装ソリューションを構築しています。生産能力と世界な流通網の拡大もまた、企業が地域の需要により効果的に対応できるようにするための主要な焦点です。さらに、企業は設計革新に重点を置いており、コスト効率を確保しながら温度管理規制を満たす、カスタマイズ可能な軽量多層包装を提供しています。

目次

第1章 調査手法

- 市場の範囲と定義

- 調査デザイン

- 調査アプローチ

- データ収集方法

- データマイニングソース

- 世界

- 地域/国

- 基本推定と計算

- 基準年計算

- 市場予測の主な動向

- 1次調査と検証

- 予測モデル

- 調査の前提と限界

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 利益率分析

- コスト構造

- 各段階での付加価値

- バリューチェーンに影響を与える要因

- ディスラプション

- 業界への影響要因

- 促進要因

- eコマース部門の成長

- 持続可能で生分解性の包装材料の需要の高まり

- ラストマイル配送におけるコールドチェーン遵守に関する厳格な規制

- 熱保護を必要とする医薬品分野の拡大

- オンライン食品配達および食事キットサービスの成長

- 業界の潜在的リスク&課題

- 高度な熱包装材料の高コスト

- リサイクル性が限られており、環境への懸念がある

- 市場機会

- Eコマースプラットフォームとパッケージイノベーターとのパートナーシップ

- リアルタイム温度監視のためのスマートセンサーの統合

- 高級菓子類やオーガニックスキンケアなどのニッチ分野での採用増加

- カスタマイズ可能でブランド差別化可能な断熱包装の開発

- 促進要因

- 成長可能性分析

- 規制情勢

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ

- ポーター分析

- PESTEL分析

- テクノロジーとイノベーションの情勢

- 現在の技術動向

- 新興技術

- 新たなビジネスモデル

- コンプライアンス要件

- 持続可能性対策

- 持続可能な材料評価

- カーボンフットプリント分析

- 循環型経済の実現

- 持続可能性の認証と基準

- 持続可能性ROI分析

- 世界の消費者感情分析

- 特許分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 地域別

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ

- 地域別

- 主要プレーヤーの競合ベンチマーキング

- 財務実績の比較

- 収益

- 利益率

- 研究開発

- 製品ポートフォリオの比較

- 製品ラインナップの広さ

- テクノロジー

- 革新

- 地理的プレゼンスの比較

- 世界フットプリント分析

- サービスネットワークの範囲

- 地域別の市場浸透率

- 競合ポジショニングマトリックス

- 戦略的展望マトリックス

- 財務実績の比較

- 主な発展, 2021-2024

- 合併と買収

- パートナーシップとコラボレーション

- 技術的進歩

- 拡大と投資戦略

- 持続可能性への取り組み

- デジタル変革の取り組み

- 新興企業/スタートアップ企業の競合情勢

第5章 市場推計・予測:材料タイプ別、2021年~2034年

- 主要動向

- 箔ラミネート

- 耐熱プラスチック

- 断熱紙ベースの材料

- 断熱フォーム

- その他

第6章 市場推計・予測:製品タイプ別、2021年~2034年

- 主要動向

- 耐熱パウチとバッグ

- 断熱箱と容器

- 保護ライナーとインサート

- サーマルメーラーと封筒

- その他

第7章 市場推計・予測:最終用途別、2021年~2034年

- 主要動向

- 美容とパーソナルケア

- 食品と飲料

- 電子・電気

- ヘルスケアと医薬品

- その他

第8章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- オランダ

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第9章 企業プロファイル

- Amcor plc

- Aspect Solutions Ltd.

- Cryopak

- DBS Packaging

- DS Smith

- Insulated Products Corporation.

- LD PACKAGING CO .,LTD

- Nordic Cold Chain Solutions

- Novolex

- Perstorp

- Puropak(Foshan)Co., Ltd.

- Sealed Air

- Sonoco ThermoSafe

- Taghleef Industries

- Thermal Packaging Solutions Ltd.

- ZTJ Packaging Co., Ltd.

目次

The Global E-Commerce Heat-Resistant Packaging Market was valued at USD 2.2 billion in 2024 and is estimated to grow at a CAGR of 11.1% to reach USD 6.4 billion by 2034. Market expansion is primarily driven by the ongoing growth of e-commerce and the increasing need for thermal protection in the pharmaceutical industry. With the surge in online purchases and international deliveries, the demand for packaging that can maintain product integrity under varied temperature conditions has significantly increased. Consumers are seeking reliability and sustainability, especially when it comes to the safe delivery of food, personal care items, and temperature-sensitive electronics. Packaging solutions must now not only provide thermal insulation but also be environmentally friendly, aligning with modern customer expectations. Rising healthcare delivery to homes and the growing digital presence of pharmaceutical suppliers have added momentum to the demand for insulated packaging.

Regulatory compliance and temperature control for critical products like biologics and insulin are also pushing manufacturers to adopt advanced thermal packaging technologies for secure delivery during transport. These sensitive pharmaceuticals require strict adherence to temperature ranges throughout the logistics chain, often between 2°C to 8°C, to preserve efficacy and avoid degradation. As global regulatory bodies tighten guidelines around pharmaceutical cold chain integrity, manufacturers are under increasing pressure to implement packaging solutions that offer precise, validated temperature performance.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $2.2 Billion |

| Forecast Value | $6.4 Billion |

| CAGR | 11.1% |

The foil laminates segment held the largest share in 2024, accounting for 34.4%. These materials are becoming a staple in the packaging industry due to their excellent insulation capabilities and minimal weight. Their application across temperature-sensitive sectors is growing, especially for international shipments. New developments in multi-layer foil technology are improving thermal retention and resistance, offering better protection during extended transit periods and under fluctuating climate conditions.

The food & beverage segment is projected to grow at a CAGR of 12.3% through 2034. Shifting lifestyles in metropolitan areas, rising demand for fresh meals, and the globalization of cuisine have all intensified the requirement for robust heat-resistant packaging. The rising adoption of fast and same-day delivery services has made consistent temperature control across the supply chain a top priority for businesses in this sector.

U.S. E-Commerce Heat-Resistant Packaging Market generated USD 508.7 million in 2024. Its dominance stems from the successful execution of sustainable logistics strategies and advanced cold chain systems. Various industries-including manufacturing, food and beverage, and pharmaceuticals-are embracing recyclable insulation foams and eco-conscious packaging to meet environmental goals. The country's strong focus on energy-efficient packaging options continues to shape its leadership position in this sector.

Leading companies in the E-Commerce Heat-Resistant Packaging Market include LD Packaging, DS Smith, Insulated Products Corporation, Novolex, Amcor, Aspect Solutions, Nordic Cold Chain Solutions, and DBS Packaging. Companies in this sector are actively investing in R&D to develop materials that combine thermal efficiency with environmental sustainability. Brands are introducing recyclable and reusable insulation products to align with consumer preferences for eco-friendly solutions. Many are also forming strategic partnerships with e-commerce and logistics providers to create tailored packaging solutions for last-mile delivery under extreme weather conditions. Expanding production capabilities and global distribution networks is another major focus, allowing firms to address regional demand more effectively. Additionally, businesses are emphasizing design innovation-offering customizable, lightweight, and multi-layer packaging that meets temperature control regulations while ensuring cost efficiency.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

- 2.2 Key market trends

- 2.2.1 Material type trends

- 2.2.2 Product type trends

- 2.2.3 End use trends

- 2.2.4 Regional

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growth in e-commerce sector

- 3.2.1.2 Rising demand for sustainable and biodegradable packaging materials

- 3.2.1.3 Stringent regulations for cold chain compliance in last-mile delivery

- 3.2.1.4 Expansion of pharmaceutical sector requiring thermal protection

- 3.2.1.5 Growth of online food delivery and meal kit services

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of advanced thermal packaging materials

- 3.2.2.2 Limited recyclability and environmental concerns

- 3.2.3 Market opportunities

- 3.2.3.1 Partnerships between E-commerce platforms and packaging innovators

- 3.2.3.2 Integration of smart sensors for real-time temperature monitoring

- 3.2.3.3 Increased adoption in niche segments like premium confectionery and organic skincare

- 3.2.3.4 Development of customizable, brand-differentiated insulated packaging

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Emerging business models

- 3.9 Compliance requirements

- 3.10 Sustainability Measures

- 3.10.1 Sustainable Materials Assessment

- 3.10.2 Carbon Footprint Analysis

- 3.10.3 Circular Economy Implementation

- 3.10.4 Sustainability Certifications and Standards

- 3.10.5 Sustainability ROI Analysis

- 3.11 Global consumer sentiment analysis

- 3.12 Patent analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments, 2021-2024

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Sustainability initiatives

- 4.4.6 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Material Type, 2021 - 2034 (USD Million & Kilo Tons)

- 5.1 Key trends

- 5.2 Foil laminates

- 5.3 High-temperature resistant plastics

- 5.4 Insulated paper-based materials

- 5.5 Thermal insulating foams

- 5.6 Others

Chapter 6 Market Estimates and Forecast, By Product Type, 2021 - 2034 (USD Million & Kilo Tons)

- 6.1 Key trends

- 6.2 Heat-resistant pouches and bags

- 6.3 Insulated boxes and containers

- 6.4 Protective liners and inserts

- 6.5 Thermal mailers and envelopes

- 6.6 Others

Chapter 7 Market Estimates and Forecast, By End Use, 2021 - 2034 (USD Million & Kilo Tons)

- 7.1 Key trends

- 7.2 Beauty & personal care

- 7.3 Food & beverages

- 7.4 Electronics & electrical

- 7.5 Healthcare & pharmaceuticals

- 7.6 Others

Chapter 8 Market Estimates & Forecast, By Region, 2021 - 2034 (USD Million & Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Spain

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 MEA

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Amcor plc

- 9.2 Aspect Solutions Ltd.

- 9.3 Cryopak

- 9.4 DBS Packaging

- 9.5 DS Smith

- 9.6 Insulated Products Corporation.

- 9.7 LD PACKAGING CO .,LTD

- 9.8 Nordic Cold Chain Solutions

- 9.9 Novolex

- 9.10 Perstorp

- 9.11 Puropak (Foshan) Co., Ltd.

- 9.12 Sealed Air

- 9.13 Sonoco ThermoSafe

- 9.14 Taghleef Industries

- 9.15 Thermal Packaging Solutions Ltd.

- 9.16 ZTJ Packaging Co., Ltd.

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 185 Pages

- 納期

- 2~3営業日