営業支援プラットフォームの市場機会、成長促進要因、業界動向分析、2025年~2034年予測

Sales Enablement Platform Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 170 Pages

- 納期

- 2~3営業日

- 商品コード

- 1782087

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

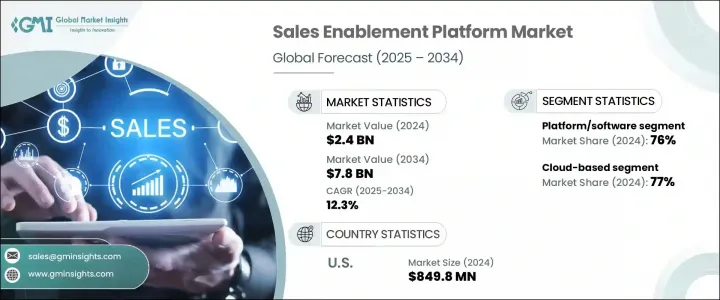

営業支援プラットフォームの世界市場規模は、2024年に24億米ドルとなり、CAGR 12.3%で成長し、2034年には78億米ドルに達すると予測されています。

企業がインテリジェントなツール、実用的なインサイト、パーソナライズされたコンテンツで営業チームを強化することをますます優先するようになるにつれ、この市場は牽引力を増し続けています。営業支援プラットフォームは、バイヤージャーニーの各ステージで文脈に沿ったメッセージングを提供することで、マーケティングとセールスの整合性を高めるために不可欠なものとなっています。これらのソリューションは、B2Bバイヤーがこれまで以上にデジタル情報に精通している状況において、コンサルティングセールスを推進し、取引転換率を向上させ、営業サイクルを加速させるために採用されています。企業は効率を高めるだけでなく、急速に進化する市場で俊敏性と競争力を維持するためにも、こうしたプラットフォームを活用しています。

営業支援プラットフォームがAIによって強化されたエコシステムへと進化することで、組織の営業実行管理方法が変化しています。これらのプラットフォームは現在、動的なコーチング機能、CRM統合、よりスマートな販売戦略をサポートする予測分析を提供しています。営業担当者は、自動化されたコンテンツ配信、オポチュニティスコアリング、インテリジェントなワークフローによって、迅速かつ十分な情報に基づいた行動を取ることができます。このようなインテリジェントな自動化は、世界企業全体の需要に拍車をかけ、営業チームがバイヤーを取り込み、パイプラインを短縮し、顧客との対話における一貫性を維持する方法を再構築しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 24億米ドル |

| 予測金額 | 78億米ドル |

| CAGR | 12.3% |

2024年、ソフトウェア/プラットフォームソリューション部門は76%のシェアを獲得し、2034年までCAGR 13%で成長すると予想されます。この成長の背景には、営業トレーニングの簡素化、営業資産の一元化、業績指標のリアルタイム配信を実現するデジタルソリューションへの依存度が高まっていることがあります。企業は、最小限のインフラしか必要としない一方で、拡張可能な支援戦略に柔軟にアクセスできるクラウドベースのツールを採用する傾向が強まっています。

クラウドベースの展開モデルは、2024年に77%のシェアを占める。クラウドソリューションは、シームレスな拡張性、迅速な導入、世界に分散した営業チームをサポートする能力により好まれています。クラウドソリューションは特にハイブリッド環境やリモートワーク環境に適しており、24時間365日いつでもツールにアクセスでき、ITサポートに負担をかけることなく地域間のコラボレーションを促進します。

米国の営業支援プラットフォーム市場は、2024年に8億4,980万米ドルを生み出し、85%のシェアを占めました。この優位性は、同国におけるエンタープライズテクノロジーの急速な導入、成熟したビジネスエコシステム、営業実績とデジタルファーストのエンゲージメント戦略の重視の高まりに起因します。製造業、金融業からハイテク、電気通信に至るまで、米国中の企業が、トレーニング、リアルタイム分析、パーソナライズされたコンテンツ、コーチングを1つの合理化されたシステムに統合した支援プラットフォームを導入しています。この市場は、世界なイノベーションと支援リーダーシップのベンチマークであり続けています。

世界の営業支援プラットフォーム業界を支配する主要企業には、Allego、MindTickle、Outreach、Seismic、Showpadなどがあります。各社が営業支援プラットフォーム市場での足場を固めるために用いている主な戦略には、AI搭載機能による製品エコシステムの拡大、CRMやサードパーティ製ソフトウェアとの統合強化、超パーソナライズされたユーザー体験の重視などがあります。また、大手企業は買収、戦略的提携、世界展開に投資し、プラットフォームの認知度と市場浸透度を高めています。トレーニングツール、コンテンツ自動化、パフォーマンス分析における絶え間ないイノベーションは、主要企業が競争力を維持し、さまざまな分野の企業顧客を引き付けるのに役立っています。カスタマイズされた導入オプション、多言語サポート、拡張可能なオンボーディングワークフローは、顧客維持と世界展開をさらに後押ししています。

目次

第1章 調査手法

- 市場の範囲と定義

- 調査デザイン

- 調査アプローチ

- データ収集方法

- データマイニングソース

- 世界

- 地域/国

- 基本推定と計算

- 基準年計算

- 市場予測の主な動向

- 1次調査と検証

- 一次情報

- 予測モデル

- 調査の前提と限界

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 利益率

- コスト構造

- 各段階での付加価値

- バリューチェーンに影響を与える要因

- ディスラプション

- 業界への影響要因

- 促進要因

- リモートワークとハイブリッドワークのモデル

- CRMおよびマーケティングオートメーションとの統合

- 分析とパフォーマンスの洞察

- パーソナライズされた購入者体験の需要

- 営業におけるデジタル変革

- 業界の潜在的リスク&課題

- 高い導入コスト

- データのプライバシーとセキュリティに関する懸念

- 市場機会

- AIと自動化の統合

- リモートおよびハイブリッドワークフォースのサポート

- 促進要因

- 成長可能性分析

- 規制情勢

- ポーターの分析

- PESTEL分析

- テクノロジーとイノベーションの情勢

- 現在の技術動向

- 新興技術

- 特許分析

- 持続可能性と環境側面

- 持続可能な慣行

- 廃棄物削減戦略

- 生産におけるエネルギー効率

- 環境に優しい取り組み

- カーボンフットプリントの考慮

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 戦略的展望マトリックス

- 主な発展

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

- 拡張計画と資金調達

第5章 市場推計・予測:コンポーネント別、2021年~2034年

- 主要動向

- プラットフォーム/ソフトウェア

- コンテンツ管理

- トレーニングとコーチング

- 売上分析とレポート

- CRM統合

- コミュニケーションツール

- AIを活用した推奨事項

- サービス

- 専門サービス

- マネージドサービス

- サポートとメンテナンス

- トレーニングと教育

第6章 市場推計・予測:展開モード別、2021年~2034年

- 主要動向

- クラウドベース

- オンプレミス

- ハイブリッド

第7章 市場推計・予測:組織規模別、2021年~2034年

- 主要動向

- 大企業

- 中小企業

第8章 市場推計・予測:最終用途別、2021年~2034年

- 主要動向

- BFSI

- ヘルスケアとライフサイエンス

- ITおよび通信

- 製造業

- メディア&エンターテイメント

- 消費財および小売

- 教育

- 旅行とホスピタリティ

- その他

第9章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- 北欧諸国

- アジア太平洋地域

- 中国

- インド

- 日本

- 韓国

- オーストラリア・ニュージーランド

- 東南アジア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- アラブ首長国連邦

- サウジアラビア

第10章 企業プロファイル

- Allego

- Bigtincan

- Brainshark

- ClearSlide

- Cloze

- DocSend

- Guru

- Highspot

- Mediafly

- Mindtickle

- Outreach

- Pitcher G

- Qstream

- Sales Gravy

- SalesHood

- Seismic

- Showpad

- Upland Software

目次

The Global Sales Enablement Platform Market was valued at USD 2.4 billion in 2024 and is estimated to grow at a CAGR of 12.3% to reach USD 7.8 billion by 2034. As enterprises increasingly prioritize empowering their sales teams with intelligent tools, actionable insights, and personalized content, this market continues to gain traction. Sales enablement platforms are now essential for creating alignment between marketing and sales by delivering contextual messaging across each stage of the buyer journey. These solutions are being embraced to drive consultative selling, improve deal conversion rates, and accelerate sales cycles in a landscape where B2B buyers are more digitally informed than ever. Companies are leveraging these platforms not only to increase efficiency but also to remain agile and competitive in rapidly evolving markets.

The evolution of sales enablement platforms into AI-enhanced ecosystems is changing the way organizations manage sales execution. These platforms now offer dynamic coaching capabilities, CRM integration, and predictive analytics that support smarter selling strategies. Sellers benefit from automated content delivery, opportunity scoring, and intelligent workflows that allow them to take fast, informed actions. This intelligent automation is fueling demand across global businesses, reshaping how sales teams engage buyers, shorten pipelines, and maintain consistency in customer interactions.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $2.4 Billion |

| Forecast Value | $7.8 Billion |

| CAGR | 12.3% |

In 2024, the software/platform solutions segment captured 76% share, expected to grow at 13% CAGR through 2034. This growth is rooted in rising dependence on digital solutions that simplify sales training, centralize sales assets, and deliver performance metrics in real time. Businesses are increasingly adopting cloud-based tools that require minimal infrastructure while allowing flexible access to scalable enablement strategies.

The cloud-based deployment models segment accounted for 77% share in 2024. Cloud solutions are preferred due to their seamless scalability, faster implementation, and ability to support globally distributed sales teams. They are particularly suited to hybrid and remote work environments, enabling 24/7 access to tools and fostering collaboration across regions without the burden of heavy IT support.

U.S. Sales Enablement Platform Market generated USD 849.8 million and held 85% share in 2024. This dominance stems from the country's rapid adoption of enterprise tech, mature business ecosystem, and the growing emphasis on sales performance and digital-first engagement strategies. From manufacturing and finance to tech and telecom, businesses across the U.S. are integrating enablement platforms that combine training, real-time analytics, personalized content, and coaching into one streamlined system. The market here remains a benchmark for global innovation and enablement leadership.

Key players dominating the Global Sales Enablement Platform Industry include Allego, MindTickle, Outreach, Seismic, and Showpad. Key strategies used by companies to strengthen their foothold in the sales enablement platform market include expanding their product ecosystems through AI-powered features, enhancing CRM and third-party software integrations, and focusing on hyper-personalized user experiences. Leading firms are also investing in acquisitions, strategic alliances, and global expansions to increase their platform visibility and market penetration. Continuous innovation in training tools, content automation, and performance analytics has helped top players stay competitive and attract enterprise clients across varied sectors. Tailored deployment options, multilingual support, and scalable onboarding workflows further support customer retention and global reach.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Component

- 2.2.3 Deployment Mode

- 2.2.4 Organization Size

- 2.2.5 End Use

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Key decision points for industry executives

- 2.4.2 Critical success factors for market players

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Remote and hybrid work models

- 3.2.1.2 Integration with CRM and marketing automation

- 3.2.1.3 Analytics and performance insights

- 3.2.1.4 Demand for personalized buyer experiences

- 3.2.1.5 Digital transformation in sales

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 High implementation costs

- 3.2.2.2 Data privacy and security concerns

- 3.2.3 Market opportunities

- 3.2.3.1 AI and automation integration

- 3.2.3.2 Remote and hybrid workforce support

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Patent analysis

- 3.9 Sustainability and environmental aspects

- 3.9.1 Sustainable practices

- 3.9.2 Waste reduction strategies

- 3.9.3 Energy efficiency in production

- 3.9.4 Eco-friendly initiatives

- 3.9.5 Carbon footprint considerations

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Latin America

- 4.2.5 Middle East & Africa

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans and funding

Chapter 5 Market Estimates & Forecast, By Component, 2021 - 2034 ($Mn)

- 5.1 Key trends

- 5.2 Platform/software

- 5.2.1 Content management

- 5.2.2 Training and coaching

- 5.2.3 Sales analytics and reporting

- 5.2.4 CRM integration

- 5.2.5 Communication tools

- 5.2.6 AI-powered recommendations

- 5.3 Services

- 5.3.1 Professional services

- 5.3.2 Managed services

- 5.3.3 Support & maintenance

- 5.3.4 Training & education

Chapter 6 Market Estimates & Forecast, By Deployment Mode, 2021 - 2034 ($Mn)

- 6.1 Key trends

- 6.2 Cloud-based

- 6.3 On-premises

- 6.4 Hybrid

Chapter 7 Market Estimates & Forecast, By Organization Size, 2021 - 2034 ($Mn)

- 7.1 Key trends

- 7.2 Large enterprise

- 7.3 SME

Chapter 8 Market Estimates & Forecast, By End Use, 2021 - 2034 ($Mn)

- 8.1 Key trends

- 8.2 BFSI

- 8.3 Healthcare & life sciences

- 8.4 IT & telecom

- 8.5 Manufacturing

- 8.6 Media & entertainment

- 8.7 Consumer goods and retail

- 8.8 Education

- 8.9 Travel & hospitality

- 8.10 Others

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 ($Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Russia

- 9.3.7 Nordics

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 ANZ

- 9.4.6 Southeast Asia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 UAE

- 9.6.2 Saudi Arabia

Chapter 10 Company Profiles

- 10.1 Allego

- 10.2 Bigtincan

- 10.3 Brainshark

- 10.4 ClearSlide

- 10.5 Cloze

- 10.6 DocSend

- 10.7 Guru

- 10.8 Highspot

- 10.9 Mediafly

- 10.10 Mindtickle

- 10.11 Outreach

- 10.12 Pitcher G

- 10.13 Qstream

- 10.14 Sales Gravy

- 10.15 SalesHood

- 10.16 Seismic

- 10.17 Showpad

- 10.18 Upland Software

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 170 Pages

- 納期

- 2~3営業日