乳化ショートニングの市場機会と成長促進要因、業界動向分析、2025年~2034年予測

Emulsified Shortenings Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 220 Pages

- 納期

- 2~3営業日

- 商品コード

- 1773469

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

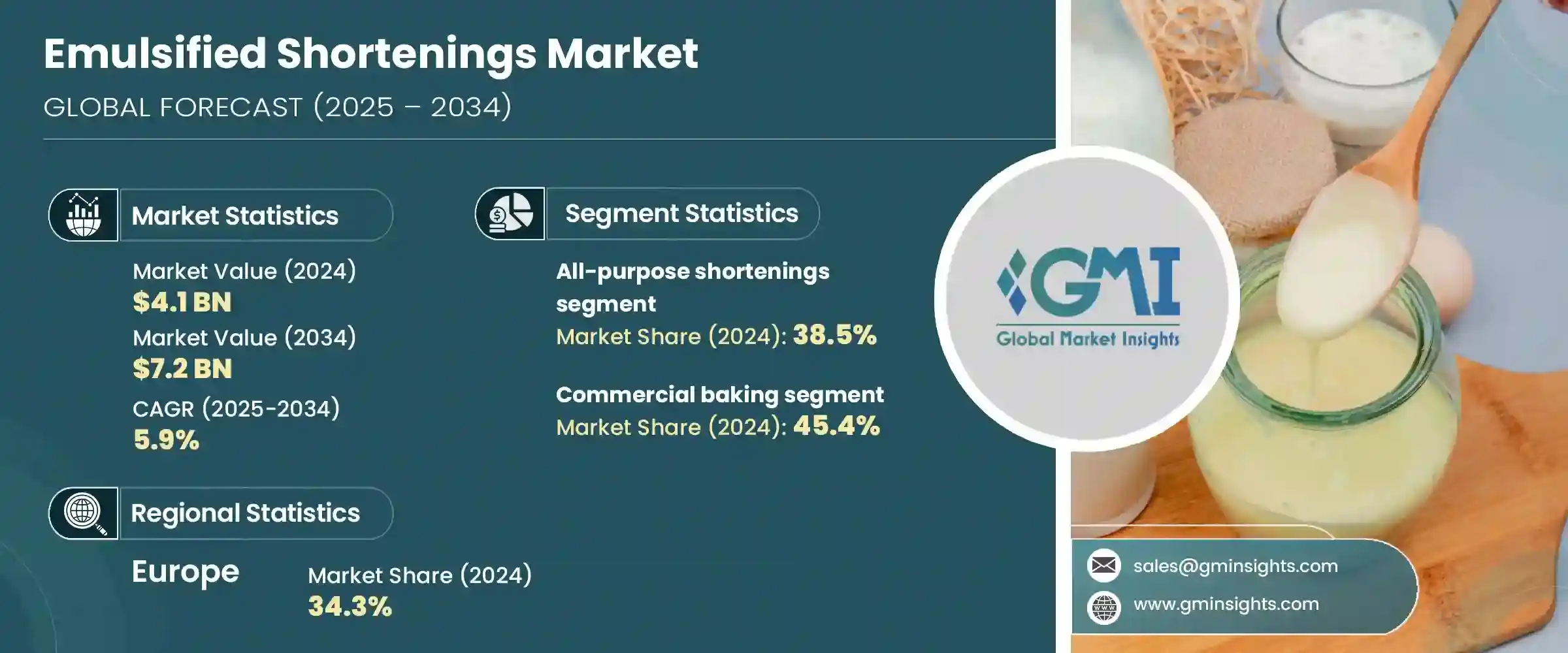

世界の乳化ショートニング市場は、2024年には41億米ドルと評価され、CAGR 5.9%で成長し、2034年には72億米ドルに達すると推定されています。

これらのショートニングは、乳化剤を組み込んだ特別に調合された脂肪混合物で、油中水型混合物の安定性を高める。その使用は、通気性、一貫性、食感、全体的な保存性を向上させる能力により、加工食品やベーカリー分野で重要です。便利ですぐに食べられる食品、クリーンラベルの代替食品、植物性脂肪の代替食品に対する需要の高まりを背景に、市場は着実に進展しています。

非水素添加やトランス脂肪酸フリーのショートニングなど、健康志向の配合へのシフトが、製品革新を引き続き促進しています。技術の進歩と食品規制の強化は、メーカーに持続可能で消費者の嗜好の変化に対応できる原材料の革新を促しています。ホームベーカリーの人気の高まりと、発展途上地域における外食チェーンの急速な拡大が、さらなる需要の原動力となっています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 41億米ドル |

| 予測金額 | 72億米ドル |

| CAGR | 5.9% |

各社は、多様な地域の味の嗜好、進化する食事要件、透明でクリーンラベルの原料に対する需要の高まりに対応するため、製品ポートフォリオを積極的に改良しています。文化的嗜好や健康志向の消費者動向に合わせて製品を提供することで、メーカー各社は成熟市場と成長著しい新興国市場の両方において、事業拡大の機会を活用できる体制を整えています。このような地域密着型のアプローチは、顧客ロイヤルティを高めるだけでなく、世界的に食品規制が強化され消費パターンが変化する中で、各ブランドが競争力を維持することを可能にします。

万能ショートニング・セグメントは2024年に最大のセグメントを占め、貢献額は16億米ドル、シェアは38.5%でした。様々な加工食品やベーカリー用途で幅広く使用されているのは、信頼できる性能、手頃な価格、多機能性によるものです。これらの特性により、汎用性が高く安定した原料を求める大規模食品メーカーから非常に望まれています。

直販セグメントは2024年に48.8%のシェアを占め、CAGR 5%で成長すると予想され、依然として最も好まれる市場ルートです。この販売アプローチは、オーダーメイドの製品仕様、大量供給能力、迅速な納品を求める大規模な産業バイヤーに魅力的です。また、メーカーが価格管理、技術サポート、合理化された供給ロジスティクスを維持できるため、戦略的な利点もあり、この分野で最も急成長している販売方法となっています。

2024年の欧州乳化ショートニング市場のシェアは34.3%。このリーダーシップは、同地域の先進的な食品生産エコシステム、加工食品や特殊焼き菓子の消費の増加、より健康的な脂肪代替食品への消費者志向の高まりに起因しています。欧州の規制はクリーンラベル製品と倫理的に調達された原料を支持しており、これは市場の需要と一致しています。持続可能な方法で収穫された油の使用など、信頼できる調達方法が乳化ショートニング分野の地域成長をさらに加速させています。

AAK AB、Wilmar International、Archer Daniels Midland Company、Bunge、Cargill Incorporatedといった主要企業は、世界の乳化ショートニング市場において極めて重要な役割を果たしています。これらの企業は、強固な世界・ネットワークと多様なポートフォリオを通じて、イノベーションと流通の最前線に自らを据えています。乳化ショートニング市場の主要企業は、市場での地位を確保・拡大するため、いくつかの戦略的アプローチに注力しています。

カスタム製剤開発は依然として最優先課題であり、これによってサプライヤーは、商業用・工業用を問わず特定の顧客ニーズに応えることができます。規制や消費者の健康への期待に応えるため、クリーンラベル技術やより健康的な代替脂肪に投資する企業も多いです。持続可能性も重視されており、環境意識の高いバイヤーにアピールするため、認証パーム油や植物由来の原料を採用しています。さらに企業は、製品の一貫性とコスト効率を確保するため、顧客直販チャネルを強化しています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 利益率

- 各段階での付加価値

- バリューチェーンに影響を与える要因

- ディスラプション

- 業界への影響要因

- 促進要因

- 業界の潜在的リスク&課題

- 市場機会

- 成長可能性分析

- 規制情勢

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ

- ポーター分析

- PESTEL分析

- 価格動向

- 地域別

- 製品別

- 将来の市場動向

- テクノロジーとイノベーションの情勢

- 現在の技術動向

- 新興技術

- 特許情勢

- 貿易統計(HSコード)(注:貿易統計は主要国のみ提供されます)

- 主要輸入国

- 主要輸出国

- 持続可能性と環境側面

- 持続可能な慣行

- 廃棄物削減戦略

- 生産におけるエネルギー効率

- 環境に優しい取り組み

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 地域別

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ航空

- 中東・アフリカ

- 地域別

- 企業マトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 主な発展

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

- 拡張計画

第5章 市場推計・予測:製品タイプ別、2021-2034

- 主要動向

- 万能ショートニング

- ケーキとアイシングのショートニング

- ショートニングを揚げる

- 特製ショートニング

第6章 市場推計・予測:用途別、2021-2034

- 主要動向

- 商業用ベーキング

- フードサービス

- 食品製造

- 小売・消費者

第7章 市場推計・予測:流通チャネル別、2021-2034

- 主要動向

- 直接販売

- 販売業者および卸売業者

- 小売チャネル

- 食品サービス販売業者

第8章 市場推計・予測:地域別、2021-2034

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- その他欧州地域

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- その他アジア太平洋地域

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- その他ラテンアメリカ地域

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

- その他中東・アフリカ地域

第9章 企業プロファイル

- Cargill Incorporated

- Bunge

- Archer Daniels Midland Company

- AAK AB

- Wilmar International

- Fuji Oil Holdings

- IOI Group

- Musim Mas

- Olenex

- Intercontinental Specialty Fats

- Ventura Foods

- Apical Group

- Sime Darby Plantation

- Mewah International

- Carotino

- Liberty Oil Mills

- Felda IFFCO

- Oleo-Fats

- PT SMART

- Golden Agri-Resources

目次

The Global Emulsified Shortenings Market was valued at USD 4.1 billion in 2024 and is estimated to grow at a CAGR of 5.9% to reach USD 7.2 billion by 2034. These shortenings are specially formulated fat blends that incorporate emulsifiers, enhancing the stability of water-in-oil mixtures. Their use is critical in processed food and bakery sectors due to their ability to improve aeration, consistency, texture, and overall shelf life. The market is advancing steadily on the back of rising demand for convenient, ready-to-eat food products, clean-label alternatives, and plant-based fat replacements.

The shift towards health-conscious formulations, such as non-hydrogenated and trans-fat-free shortenings, continues to fuel product innovation. Technological progress and tighter food regulations are pushing manufacturers to innovate with ingredients that are both sustainable and adaptable to evolving consumer preferences. The growing popularity of home baking, along with the rapid expansion of food service chains in developing regions, is driving further demand.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $4.1 Billion |

| Forecast Value | $7.2 Billion |

| CAGR | 5.9% |

Companies are actively refining their product portfolios to cater to diverse regional flavor preferences, evolving dietary requirements, and the rising demand for transparent, clean-label ingredients. By aligning their offerings with cultural tastes and health-conscious consumer trends, manufacturers are positioning themselves to capitalize on expansion opportunities in both mature and high-growth developing markets. This localized approach not only enhances customer loyalty but also allows brands to stay competitive amid tightening food regulations and shifting consumption patterns worldwide.

The all-purpose shortenings segment represented the largest segment in 2024, contributing USD 1.6 billion and a 38.5% share. Their wide usage across various processed foods and bakery applications stems from their dependable performance, affordability, and multi-functionality. These attributes make them highly desirable among large-scale food manufacturers seeking versatile and consistent ingredients.

The direct sales segment accounted for a 48.8% share in 2024 and is anticipated to grow at a CAGR of 5%, remaining the most preferred route to the market. This sales approach appeals to large industrial buyers who seek tailored product specifications, bulk supply capabilities, and prompt delivery. It also offers a strategic advantage by enabling manufacturers to maintain pricing control, technical support, and streamlined supply logistics, making it the fastest-growing distribution method in the sector.

Europe Emulsified Shortenings Market held a 34.3% share in 2024. This leadership stems from the region's advanced food production ecosystem, increased consumption of processed and specialty baked goods, and rising consumer inclination toward healthier fat alternatives. European regulations favor clean-label products and ethically sourced ingredients, which align with market demands. Reliable sourcing practices, such as the use of sustainably harvested oils, have further accelerated regional growth in the emulsified shortenings space.

Key players such as AAK AB, Wilmar International, Archer Daniels Midland Company, Bunge, and Cargill Incorporated play a pivotal role in the global emulsified shortenings landscape. These companies have anchored themselves at the forefront of innovation and distribution through robust global networks and diversified portfolios. Leading companies in the emulsified shortenings market are focusing on several strategic approaches to secure and expand their market positions.

Custom formulation development remains a top priority, allowing suppliers to cater to specific client needs across commercial and industrial applications. Many are investing in clean-label technologies and healthier fat alternatives to align with regulatory and consumer health expectations. A strong emphasis is placed on sustainability, with firms adopting certified palm oils and plant-based inputs to appeal to environmentally conscious buyers. Additionally, firms are strengthening direct-to-customer distribution channels to ensure product consistency and cost efficiency.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product

- 2.2.3 Application

- 2.2.4 Distribution channel

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.6.1 Technology and innovation landscape

- 3.6.2 Current technological trends

- 3.6.3 Emerging technologies

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By product

- 3.8 Future market trends

- 3.9 Technology and innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code) (Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly Initiatives

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2021 - 2034 (USD Million) (Kilo Tons)

- 5.1 Key trends

- 5.2 All-purpose shortenings

- 5.3 Cake and icing shortenings

- 5.4 Frying shortenings

- 5.5 Specialty shortenings

Chapter 6 Market Estimates and Forecast, By Applications, 2021 - 2034 (USD Million) (Kilo Tons)

- 6.1 Key trends

- 6.2 Commercial baking

- 6.3 Food service

- 6.4 Food manufacturing

- 6.5 Retail and consumer

Chapter 7 Market Estimates and Forecast, By Distribution Channel, 2021 - 2034 (USD Million) (Kilo Tons)

- 7.1 Key trends

- 7.2 Direct sales

- 7.3 Distributors and wholesalers

- 7.4 Retail channels

- 7.5 Food service distributors

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2034 (USD Million) (Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.3.7 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.5.4 Rest of Latin America

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of Middle East and Africa

Chapter 9 Company Profiles

- 9.1 Cargill Incorporated

- 9.2 Bunge

- 9.3 Archer Daniels Midland Company

- 9.4 AAK AB

- 9.5 Wilmar International

- 9.6 Fuji Oil Holdings

- 9.7 IOI Group

- 9.8 Musim Mas

- 9.9 Olenex

- 9.10 Intercontinental Specialty Fats

- 9.11 Ventura Foods

- 9.12 Apical Group

- 9.13 Sime Darby Plantation

- 9.14 Mewah International

- 9.15 Carotino

- 9.16 Liberty Oil Mills

- 9.17 Felda IFFCO

- 9.18 Oleo- Fats

- 9.19 PT SMART

- 9.20 Golden Agri- Resources

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 220 Pages

- 納期

- 2~3営業日