植物性ショートニングの市場機会、成長要因、業界動向分析、および2026年~2035年の予測

Vegetable Shortening Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035- 発行日

- ページ情報

- 英文 190 Pages

- 納期

- 2~3営業日

- 商品コード

- 2027606

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

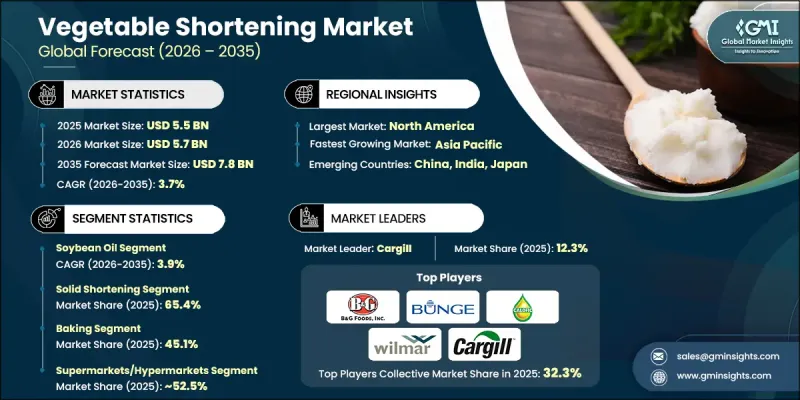

世界の植物性ショートニング市場は、2025年に55億米ドルと評価され、CAGR 3.7%で成長し、2035年までに78億米ドルに達すると推定されています。

この市場は、製パン・製菓業界および外食産業によって牽引されています。これらの業界では、植物性ショートニングが、ペストリー、クッキー、ケーキ、揚げ物などに柔らかくサクサクした食感をもたらし、かつ保存期間を延長する点で高く評価されています。健康やウェルネスに対する消費者の意識の高まりが市場力学に影響を与えており、トランス脂肪酸フリーや非水素化の配合製品への需要が増加しています。植物由来やヴィーガン食の人気の高まりは、持続可能でクリーンラベル、非遺伝子組み換えのショートニング製品への需要を加速させています。製品処方の革新と食品加工における用途の拡大が、持続的な成長を支えています。市場の拡大は、主に2つの要因によって牽引されています。それは、現代の食生活やライフスタイルの動向に合致する、より健康的で便利、かつ植物由来の代替品を求める消費者が増えるにつれ、即食可能な焼き菓子の消費が増加していることと、家庭でのベーキング活動が急増していることです。

| 市場の範囲 | |

|---|---|

| 開始年 | 2025年 |

| 予測期間 | 2026年~2035年 |

| 開始時の市場規模 | 55億米ドル |

| 予測額 | 78億米ドル |

| CAGR | 3.7% |

大豆油セグメントは40.5%のシェアを占めており、2035年までCAGR3.9%で成長すると予想されています。植物性ショートニングの原料は、大豆油、パーム油、綿実油、ひまわり油など、非常に多岐にわたります。パーム油は、そのコストパフォーマンスと優れた安定性から広く使用され続けていますが、大豆油は、栄養面での利点や様々な食品への幅広い用途から、依然として人気を保っています。

固形ショートニングセグメントは2025年に65.4%のシェアを占め、2026年から2035年にかけてCAGR 3.8%で成長すると予測されています。消費者の嗜好の変化により、利便性、汎用性、機能性が重視されるようになり、固形ショートニングは製パンや揚げ物用途において主導的な地位を維持しています。一貫した食感、長期的な鮮度保持、そして使いやすさを提供できる点が、製パン業者や食品加工業者におけるその優位性を強めています。

北米の植物性ショートニング市場は、2025年に34.7%のシェアを占めました。同地域は、消費者の意識の高さと、すぐに食べられる焼き菓子やスナックへの需要に支えられています。北米地域内では、米国が最大のシェアを占めており、これは製パン、揚げ物、スナック製造における植物性ショートニングの広範な利用に支えられています。企業は、健康志向の消費者の嗜好に応えるため、クリーンラベル、植物由来、非遺伝子組み換え(非GMO)製品の生産を拡大しています。ヴィーガンやベジタリアン食の普及が進んでいることも、植物性ショートニングの需要をさらに後押ししており、北米は主要な成長拠点となっています。

よくあるご質問

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 利益率

- 各段階における付加価値

- バリューチェーンに影響を与える要因

- ディスラプション

- 業界への影響要因

- 促進要因

- 業界の潜在的リスク&課題

- 市場機会

- 成長可能性分析

- 規制情勢

- ポーター分析

- PESTEL分析

- 価格動向

- 地域別

- タイプ別

- 将来の市場動向

- 技術およびイノベーションの動向

- 現在の技術動向

- 新興技術

- 特許動向

- 貿易統計(HSコード)

- 主要輸入国

- 主要輸出国

- 持続可能性と環境面

- 持続可能な取り組み

- 廃棄物削減戦略

- 生産におけるエネルギー効率

- 環境配慮型イニシアチブ

- カーボンフットプリントの考慮

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 地域別

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ

- 地域別

- 企業マトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 主な発展

- 合併・買収

- 提携・協業

- 新製品の発売

- 事業拡大計画

第5章 市場推計・予測:ソース別、2022-2035

- 大豆油

- パーム油

- 綿実油

- ひまわり油

- その他

第6章 市場推計・予測:形態別、2022-2035

- 固形ショートニング

- 液体ショートニング

- 粉末ショートニング

第7章 市場推計・予測:用途別、2022-2035

- ベーキング

- 揚げ物

- 菓子類

- スナック・塩味食品

- 食品加工

- その他

第8章 市場推計・予測:流通チャネル別、2022-2035

- スーパーマーケット/ハイパーマーケット

- コンビニエンスストア

- オンライン小売

- 専門店

- その他

第9章 市場推計・予測:地域別、2022-2035

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- その他欧州地域

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- その他アジア太平洋地域

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- その他ラテンアメリカ地域

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

- その他中東・アフリカ地域

第10章 企業プロファイル

- B&G Foods, Inc.

- Bunge

- CALOFIC

- Cargill

- GOLDEN HOPE-NHA BE EDIBLE OILS CO., LTD

- Manildra Group

- NIRMALA AVIJAYA GROUP

- Spectrum Naturals

- Stratas Foods

- Ventura Foods

- Wilmar International

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 190 Pages

- 納期

- 2~3営業日