機能性粉の市場機会、成長促進要因、産業動向分析、2025年~2034年予測

Functional Flours Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 225 Pages

- 納期

- 2~3営業日

- 商品コード

- 1773224

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

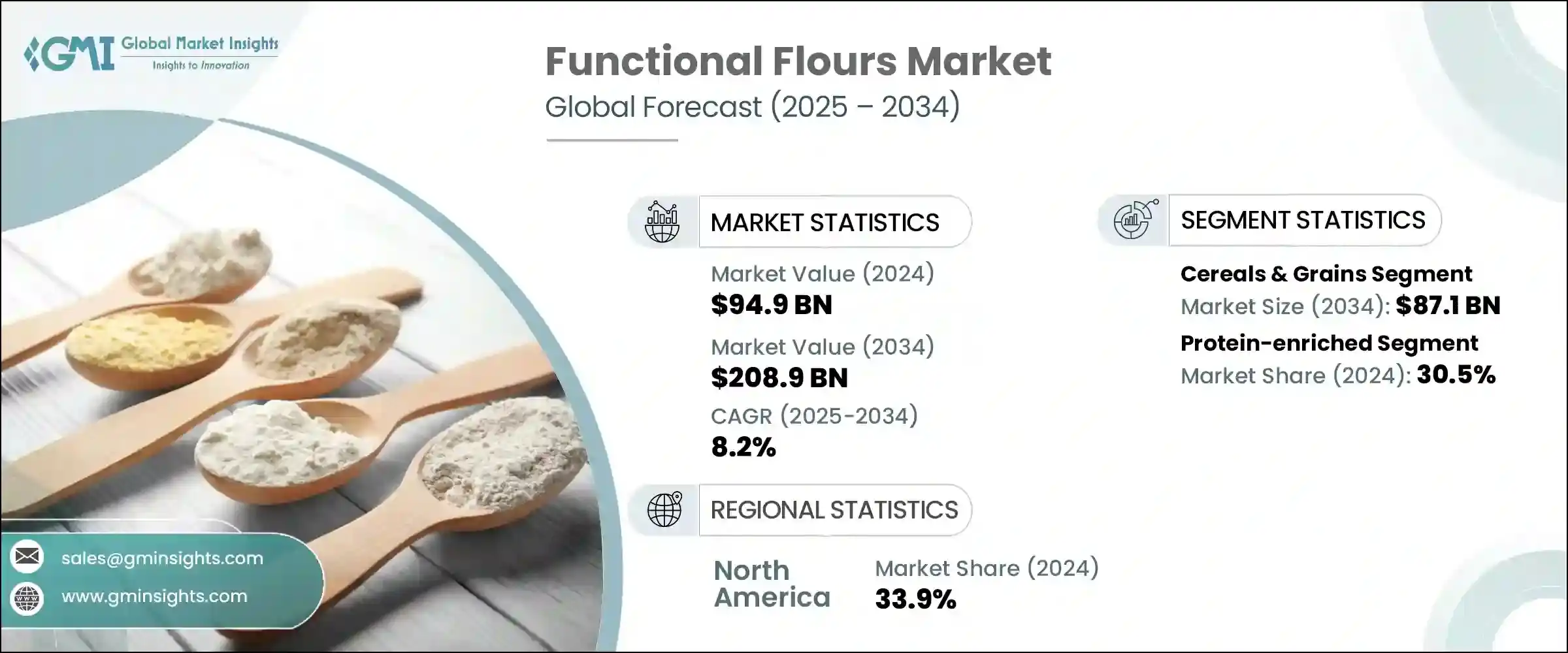

世界の機能性粉市場は2024年に949億米ドルと評価され、CAGR 8.2%で成長し、2034年には2,089億米ドルに達すると推定されています。

この急成長の背景には、強化穀粉がもたらす健康上の利点、特に肥満や糖尿病といった生活習慣に関連する症状の管理における役割に対する意識の高まりがあります。消費者はますます栄養価の高い代替品を求めるようになり、メーカーは穀粉に繊維、タンパク質、微量栄養素を強化するようになりました。さらに、ベーカリー、スナック、コンビニエンスフードなどの用途、特にクリーンラベルやグルテン・フリーの分野での需要の高まりが、市場の勢いを強めています。製粉と生産における技術強化もまた、食感、栄養価、機能的性能を向上させた穀粉の製造を可能にし、その水準を引き上げています。

こうした進歩により、生産者は消費者の多様な期待に応えることができるようになり、特定の食嗜好、健康ニーズ、文化動向に合わせた高度に専門化された穀粉製品の開発が可能になることで、市場の拡大がさらに加速しています。消費者が透明性、機能性、クリーンラベルの原料をますます求めるようになる中、メーカーはこれらの技術革新を活用して、栄養価の向上、消化率の改善、保存性の向上を実現した穀粉を製造しています。グルテンフリー、低炭水化物、プロテインリッチ、アレルゲン対応など、穀粉の配合をカスタマイズできるため、ブランドはニッチ市場に対応しつつ、消費者層の拡大を図ることができます。ひいては、進化する食品動向との戦略的な整合性が、プレミアム製品のポジショニングと大衆市場への拡張性の両方をサポートし、世界の機能性粉産業の勢いを強めています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 949億米ドル |

| 予測金額 | 2,089億米ドル |

| CAGR | 8.2% |

シリアル&穀物分野は、CAGR 5.4%で拡大し、2034年には871億米ドルに達すると予測されます。パン、朝食用シリアル、スナックバー、調理済み食品など、日常的な製品に広く取り入れられていることが、この市場の強い存在感を支えています。特にグルテンフリー、全粒粉、高繊維質の製剤など、より体に良い選択肢を求める消費者の嗜好が急増していることが、この分野の成長に拍車をかけています。健康とウェルネスの動向が世界の食習慣を形成し続けているため、この分野は先進国市場でも新興国市場でも定番商品であり続けています。このような勢いにもかかわらず、原材料価格の変動、輸送コスト、時折発生するサプライチェーンの中断が継続的なリスクとなっています。こうした課題に対処するため、生産者は食物繊維、ビタミン、ミネラルを添加して強化することで、シリアルベースの穀粉の栄養密度を高め、健康志向の購買層にアピールすることに注力しています。

2024年には、タンパク質強化粉セグメントが30.5%のシェアを占めました。このセグメントは2034年までCAGR 5.2%で成長すると予測されています。このセグメントは、身体能力の向上、筋肉の健康、満腹感、体重管理に広く関連する、タンパク質が豊富な食事に対する需要の急増が原動力となっています。特に高齢者や特定の人口集団におけるタンパク質不足の悪影響に対する消費者の意識の高まりが、タンパク質を添加した機能性粉への関心を強めています。これに対応するため、メーカーはベジタリアンやビーガンの人口増加に対応し、乳製品や大豆アレルギーのある消費者にも対応できるよう、レンズ豆、エンドウ豆、大豆などの植物性タンパク質を使用した革新的な製品を開発しています。

北米機能性粉市場は2024年に33.9%のシェアを占めました。同地域がトップシェアを占める主な要因は、食生活のカスタマイズに関する意識の高まりにあり、消費者はグルテン不耐症、セリアック病、その他のライフスタイルに基づく食事パターンに適した穀粉を積極的に求めています。この需要は、ひよこ豆、キヌア、玄米のような栄養密度の高い原料由来の穀粉の生産と消費を促進しています。技術革新と製品の多様化を通じて一貫して製品ポートフォリオを拡大している既存業界企業の存在感が強く、市場の成長をさらに後押ししています。

同市場の主要企業には、Roquette Freres、Ingredion Incorporated、Archer Daniels Midland Company(ADM)、SunOpta Inc.、Associated British Foods plcなどがあります。機能性粉分野のトップ企業は、多様化、健康主導のイノベーション、サプライチェーンの堅牢性に注力しています。これらの企業は、植物性タンパク質の穀粉や代替穀物など、製品レンジを拡大しています。研究開発への重点的な投資により、血糖コントロール、腸の健康、高タンパク食をサポートするカスタムメイドの穀粉ブレンドの開発が可能になっています。ベーカリーメーカーや食品メーカーとの戦略的提携により、製品の普及と最終用途への適合性が向上しています。これらの企業は、原材料価格の変動をヘッジするために、調達パートナーシップや保管インフラを通じてグローバルサプライチェーンを強化しています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- 主要メーカー

- 販売代理店

- 業界全体の利益率

- サプライチェーンと流通分析

- 原材料調達

- 生産と製造

- コールドチェーンインフラ

- 流通チャネル

- サプライチェーンの課題と最適化

- 持続可能な慣行

- 貿易統計(HSコード)

- 主要輸出国, 2021-2024

- 主要輸出国, 2021-2024

(注:上記の貿易統計は主要国のみに提供されます)

- 影響要因

- 促進要因

- 健康意識の高まり

- グルテンフリー製品の需要増加

- タンパク質摂取量の増加

- クリーンラベルの動向

- 業界の潜在的リスク&課題

- 従来の穀粉に比べて高価

- 保存期間が限られている

- 処理上の課題

- 味と食感の制限

- 市場機会

- アジア太平洋の新興市場

- 植物由来製品におけるイノベーション

- 機能性食品の応用

- eコマースの拡大

- 促進要因

- 原材料の情勢

- 製造業の動向

- 技術の進化

- 加工技術

- 要塞化の方法

- 品質テストと分析

- パッケージングの革新

- 価格分析とコスト構造

- 価格動向(米ドル/トン)

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東アフリカ

- 価格要因(原材料、エネルギー、労働力)

- 地域による価格差

- コスト構造の内訳

- 収益性分析

- 価格動向(米ドル/トン)

- 規制の枠組みと基準

- FDA規制(米国)

- EU規制

- コーデックス食品規格

- 地域規制機関

- ラベル要件

- 品質基準

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 企業ヒートマップ分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 戦略ダッシュボード

- Expansion

- Mergers &acquisition

- Collaborations

- New product launches

- Research &development

- 主要プレーヤーによる最近の動向と影響分析

- 企業分類

- 参加者の概要

- 財務実績

- 製品ベンチマーク

第5章 市場推計・予測:供給源別、2021年~2034年

- 主要動向

- 穀物

- 小麦

- 米

- トウモロコシ

- オート麦

- 大麦

- キヌア

- その他の穀物

- マメ科植物

- ひよこ豆

- レンズ豆

- エンドウ豆

- 豆

- その他の豆類

- ナッツと種子

- アーモンド

- ココナッツ

- ヒマワリの種

- 亜麻の種子

- その他のナッツ類

- 果物と野菜

- バナナ

- サツマイモ

- キャッサバ

- その他の果物と野菜

- その他の供給源

- 昆虫

- 藻類

- キノコ

第6章 市場推計・予測:機能別、2021年~2034年

- 主要動向

- タンパク質強化

- 食物繊維が豊富

- グルテンフリー

- ビタミン&ミネラル強化

- 低炭水化物

- プロバイオティクス

- 抗酸化物質が豊富

- その他の機能

第7章 市場推計・予測:用途別、2021年~2034年

- 主要動向

- ベーカリー&菓子類

- パン

- ケーキとペストリー

- クッキーとビスケット

- マフィンとカップケーキ

- その他のベーカリー製品

- スナック

- 押し出しスナック

- クラッカー

- チップス

- その他のスナック

- 飲み物

- プロテインドリンク

- スムージー

- 機能性飲料

- その他の飲み物

- パスタと麺類

- 朝食用シリアル

- スープとソース

- 肉の代替品

- その他

第8章 市場推計・予測:形態別、2021年~2034年

- 主要動向

- 粉末

- 顆粒

- フレーク

- ペレット

第9章 市場推計・予測:流通チャネル別、2021年~2034年

- 主要動向

- B2B(企業間取引)

- 食品メーカー

- パン屋

- フードサービス

- その他のB2Bチャネル

- B2C(企業対消費者)

- スーパーマーケットとハイパーマーケット

- 専門店

- オンライン小売

- コンビニエンスストア

- その他のB2Cチャネル

第10章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- その他欧州地域

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- その他アジア太平洋地域

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- その他ラテンアメリカ地域

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

- その他中東・アフリカ地域

第11章 企業プロファイル

- Cargill, Incorporated

- Archer Daniels Midland Company(ADM)

- Associated British Foods plc

- General Mills, Inc.

- Ingredion Incorporated

- Roquette Freres

- Tate &Lyle PLC

- SunOpta Inc.

- The Scoular Company

- Agrana Beteiligungs-AG

- Limagrain

- Bunge Limited

- The Andersons, Inc.

- Grain Millers, Inc.

- Hodgson Mill, Inc.

- Lifeway Foods, Inc.

- Manildra Group

- Unicorn Grain Specialties

- Bluebird Grain Farms

目次

The Global Functional Flours Market was valued at USD 94.9 billion in 2024 and is estimated to grow at a CAGR of 8.2% to reach USD 208.9 billion by 2034. This surge is being driven by growing awareness of the health advantages that fortified flours offer-particularly their roles in managing lifestyle-related conditions like obesity and diabetes. Consumers increasingly seek nutritious alternatives, leading manufacturers to enrich flours with fibers, proteins, and micronutrients. Additionally, rising demand across applications such as bakery, snacks, and convenience foods-especially clean-label and gluten-free segments-has strengthened market momentum. Technological enhancements in milling and production have also raised the bar, enabling the creation of flours with improved texture, nutritional value, and functional performance.

These advancements allow producers to meet diverse consumer expectations, further fueling market expansion by enabling the development of highly specialized flour products tailored to specific dietary preferences, health needs, and cultural trends. As consumers increasingly demand transparency, functionality, and clean-label ingredients, manufacturers are leveraging these innovations to create flours with enhanced nutritional value, better digestibility, and improved shelf life. The ability to customize flour formulations-whether gluten-free, low-carb, protein-rich, or allergen-friendly-empowers brands to cater to niche markets while broadening their overall consumer base. In turn, this strategic alignment with evolving food trends supports both premium product positioning and mass-market scalability, reinforcing the momentum of the global functional flour industry.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $94.9 Billion |

| Forecast Value | $208.9 Billion |

| CAGR | 8.2% |

The cereals & grains segment is forecasted to reach USD 87.1 billion by 2034, expanding at a CAGR of 5.4%. Its strong market presence is supported by widespread incorporation in everyday products like bread, breakfast cereals, snack bars, and ready-to-eat foods. A surge in consumer preference for better-for-you options-especially gluten-free, whole-grain, and high-fiber formulations-is fueling this segment's growth. As health and wellness trends continue to shape eating habits globally, this segment remains a staple in both developed and emerging markets. Despite this momentum, fluctuating raw material prices, transportation costs, and occasional supply chain interruptions pose ongoing risks. To counteract these challenges, producers are focusing on increasing the nutritional density of cereal-based flours by fortifying them with added fiber, vitamins, and minerals to appeal to health-conscious buyers.

In 2024, protein-enriched flours segment held 30.5% share. This segment is projected to grow at a CAGR of 5.2% through 2034, driven by surging demand for protein-rich diets, which are widely associated with improved physical performance, muscle health, satiety, and weight management. Heightened consumer awareness of the negative impacts of protein deficiency, especially among older adults and specific demographic groups, is intensifying interest in functional flours with added protein. In response, manufacturers are developing innovative offerings using plant-based proteins like lentils, peas, and soy to support growing vegetarian and vegan populations, while also catering to consumers with dairy or soy allergies.

North America Functional Flours Market held a 33.9% share in 2024. The region's leading share is largely attributed to rising awareness around dietary customization, with consumers actively seeking flours suited for gluten intolerance, celiac disease, and other lifestyle-based eating patterns. This demand is driving the production and consumption of flours derived from nutrient-dense sources like chickpeas, quinoa, and brown rice. The strong presence of established industry players, who are consistently expanding their product portfolios through innovation and product diversification, is further supporting market growth.

Major players in the market include Roquette Freres, Ingredion Incorporated, Archer Daniels Midland Company (ADM), SunOpta Inc., and Associated British Foods plc. Top companies in the functional flour space are focusing on diversification, health-driven innovation, and supply chain robustness. They are expanding their product ranges to include plant-based protein flours and alternative grains. Heavy investment in R&D is enabling the development of custom-tailored flour blends that support blood sugar control, gut health, or high-protein diets. Strategic alliances with bakery and food manufacturers are improving product penetration and end-use compatibility. These players are strengthening global supply chains through sourcing partnerships and storage infrastructure to hedge against raw material price fluctuations.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculations

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021-2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Key manufacturers

- 3.1.2 Distributors

- 3.1.3 Profit margins across the industry

- 3.1.4 Supply chain and distribution analysis

- 3.1.4.1 Raw material sourcing

- 3.1.4.2 Production and manufacturing

- 3.1.4.3 Cold chain infrastructure

- 3.1.4.4 Distribution channels

- 3.1.4.5 Supply chain challenges and optimization

- 3.1.4.6 Sustainable practices

- 3.2 Trade statistics (HS code)

- 3.2.1 Major exporting countries, 2021-2024 (Kilo Tons)

- 3.2.2 Major exporting countries, 2021-2024 (Kilo Tons)

( Note: the above trade statistics will be provided for key countries only)

- 3.3 Impact forces

- 3.3.1 Growth drivers

- 3.3.1.1 Rising health consciousness

- 3.3.1.2 Growing demand for gluten-free products

- 3.3.1.3 Increasing protein consumption

- 3.3.1.4 Clean label trends

- 3.3.2 Industry pitfalls & challenges

- 3.3.2.1 High cost compared to conventional flour

- 3.3.2.2 Limited shelf life

- 3.3.2.3 Processing challenges

- 3.3.2.4 Taste and texture limitations

- 3.3.3 Market opportunity

- 3.3.3.1 Emerging markets in Asia-Pacific

- 3.3.3.2 Innovation in plant-based products

- 3.3.3.3 Functional food applications

- 3.3.3.4 E-commerce expansion

- 3.3.1 Growth drivers

- 3.4 Raw material landscape

- 3.4.1 Manufacturing trends

- 3.4.2 Technology evolution

- 3.4.2.1 Processing technologies

- 3.4.2.2 Fortification methods

- 3.4.2.3 Quality testing & analysis

- 3.4.2.4 Packaging innovations

- 3.5 Pricing analysis and cost structure

- 3.5.1 Pricing trends (USD/Ton)

- 3.5.1.1 North America

- 3.5.1.2 Europe

- 3.5.1.3 Asia Pacific

- 3.5.1.4 Latin America

- 3.5.1.5 Middle East Africa

- 3.5.2 Pricing factors (raw materials, energy, labor)

- 3.5.3 Regional price variations

- 3.5.4 Cost structure breakdown

- 3.5.5 Profitability analysis

- 3.5.1 Pricing trends (USD/Ton)

- 3.6 Regulatory framework and standards

- 3.6.1 FDA regulations (U.S.)

- 3.6.2 EU regulations

- 3.6.3 Codex alimentarius standards

- 3.6.4 Regional regulatory bodies

- 3.6.5 Labeling requirements

- 3.6.6 Quality standards

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis, 2024

- 4.3 Company heat map analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

- 4.6.1 Expansion

- 4.6.2 Mergers & acquisition

- 4.6.3 Collaborations

- 4.6.4 New product launches

- 4.6.5 Research & development

- 4.7 Recent developments & impact analysis by key players

- 4.7.1 Company categorization

- 4.7.2 Participant’s overview

- 4.7.3 Financial performance

- 4.8 Product benchmarking

Chapter 5 Market Estimates & Forecast, By Source, 2021-2034 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Cereals & grains

- 5.2.1 Wheat

- 5.2.2 Rice

- 5.2.3 Corn

- 5.2.4 Oats

- 5.2.5 Barley

- 5.2.6 Quinoa

- 5.2.7 Other cereals & grains

- 5.3 Legumes

- 5.3.1 Chickpeas

- 5.3.2 Lentils

- 5.3.3 Peas

- 5.3.4 Beans

- 5.3.5 Other legumes

- 5.4 Nuts & seeds

- 5.4.1 Almonds

- 5.4.2 Coconut

- 5.4.3 Sunflower seeds

- 5.4.4 Flax seeds

- 5.4.5 Other nuts & seeds

- 5.5 Fruits & vegetables

- 5.5.1 Banana

- 5.5.2 Sweet potato

- 5.5.3 Cassava

- 5.5.4 Other fruits & vegetables

- 5.6 Other sources

- 5.6.1 Insects

- 5.6.2 Algae

- 5.6.3 Mushrooms

Chapter 6 Market Estimates & Forecast, By Functionality, 2021-2034 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Protein enriched

- 6.3 Fiber enriched

- 6.4 Gluten-free

- 6.5 Vitamin & mineral fortified

- 6.6 Low carbohydrate

- 6.7 Probiotic

- 6.8 Antioxidant rich

- 6.9 Other functionalities

Chapter 7 Market Estimates & Forecast, By Application, 2021-2034 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Bakery & confectionery

- 7.2.1 Bread

- 7.2.2 Cakes & pastries

- 7.2.3 Cookies & biscuits

- 7.2.4 Muffins & cupcakes

- 7.2.5 Other bakery products

- 7.3 Snacks

- 7.3.1 Extruded snacks

- 7.3.2 Crackers

- 7.3.3 Chips

- 7.3.4 Other snacks

- 7.4 Beverages

- 7.4.1 Protein drinks

- 7.4.2 Smoothies

- 7.4.3 Functional beverages

- 7.4.4 Other beverages

- 7.5 Pasta & noodles

- 7.6 Breakfast cereals

- 7.7 Soups & sauces

- 7.8 Meat alternatives

- 7.9 Others

Chapter 8 Market Estimates & Forecast, By Form, 2021-2034 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 Powder

- 8.3 Granules

- 8.4 Flakes

- 8.5 Pellets

Chapter 9 Market Estimates & Forecast, By Distribution Channel, 2021-2034 (USD Billion) (Kilo Tons)

- 9.1 Key trends

- 9.2 B2b (business-to-business)

- 9.2.1 Food manufacturers

- 9.2.2 Bakeries

- 9.2.3 Foodservice

- 9.2.4 Other b2b channels

- 9.3 B2c (business-to-consumer)

- 9.3.1 Supermarkets & hypermarkets

- 9.3.2 Specialty stores

- 9.3.3 Online retail

- 9.3.4 Convenience stores

- 9.3.5 Other b2c channels

Chapter 10 Market Estimates & Forecast, By Region, 2021-2034 (USD Billion) (Kilo Tons)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Rest of Europe

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.4.6 Rest of Asia Pacific

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.5.4 Rest of Latin America

- 10.6 MEA

- 10.6.1 Saudi Arabia

- 10.6.2 South Africa

- 10.6.3 UAE

- 10.6.4 Rest of Middle East and Africa

Chapter 11 Company Profiles

- 11.1 Cargill, Incorporated

- 11.2 Archer Daniels Midland Company (ADM)

- 11.3 Associated British Foods plc

- 11.4 General Mills, Inc.

- 11.5 Ingredion Incorporated

- 11.6 Roquette Freres

- 11.7 Tate & Lyle PLC

- 11.8 SunOpta Inc.

- 11.9 The Scoular Company

- 11.10 Agrana Beteiligungs-AG

- 11.11 Limagrain

- 11.12 Bunge Limited

- 11.13 The Andersons, Inc.

- 11.14 Grain Millers, Inc.

- 11.15 Hodgson Mill, Inc.

- 11.16 Lifeway Foods, Inc.

- 11.17 Manildra Group

- 11.18 Unicorn Grain Specialties

- 11.19 Bluebird Grain Farms

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 225 Pages

- 納期

- 2~3営業日