|

市場調査レポート

商品コード

1773218

商用水素生成の市場機会、成長促進要因、産業動向分析、2025年~2034年予測Merchant Hydrogen Generation Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 商用水素生成の市場機会、成長促進要因、産業動向分析、2025年~2034年予測 |

|

出版日: 2025年06月23日

発行: Global Market Insights Inc.

ページ情報: 英文 125 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

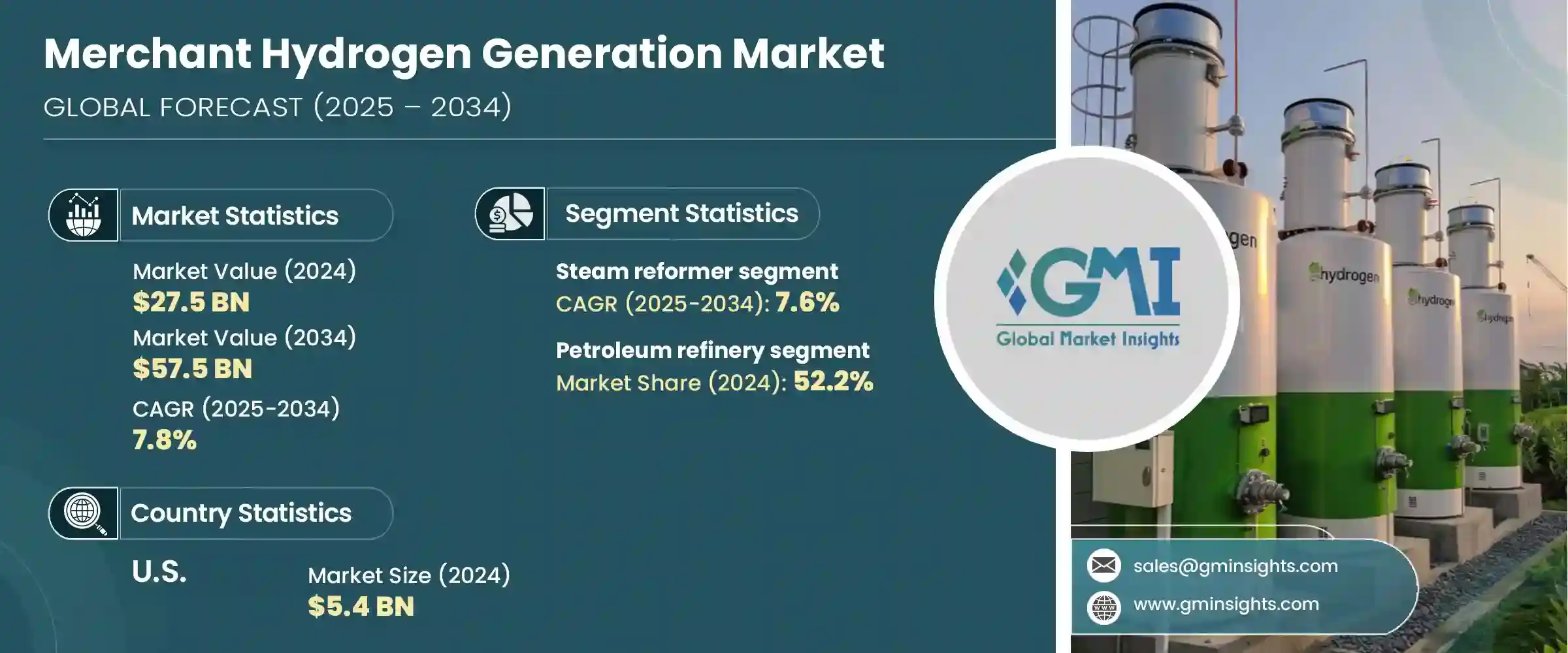

世界の商用水素生成市場は、2024年には275億米ドルとなり、CAGR 7.8%で成長し、2034年には575億米ドルに達すると予測されています。

世界の政府や産業界が二酸化炭素排出量の削減に重点を置くようになり、市場は着実な勢いを見せています。このシフトは、世界の脱炭素化アジェンダの主要企業として台頭してきた水素を含むクリーンエネルギー源の需要を促進しています。ネットゼロ目標の達成を目指す政策と、セクターを超えた気候変動に対する意識の高まりが、商用水素生成拡大の好条件を生み出しています。

成長を可能にする主な要因の一つは、再生可能エネルギーの導入規模の拡大であり、余剰電力の利用を通じて水素製造との相乗効果を生み出しています。エネルギーシステムの多様化と分散化が進むにつれ、水素はエネルギー貯蔵とグリッドバランシングのための重要なツールとなりつつあります。このような状況の中で、プロトン交換膜や固体酸化物電解などの新世代の電解技術が人気を集めています。これらの技術革新は、高い効率とコスト優位性を提供し、商業規模での水素生成をより現実的なものにしています。産業界は、特に鉄鋼、精錬、化学などのエネルギー多消費セクターにおいて、持続可能性目標に沿った事業運営を積極的に進めています。この移行は、生産性を損なうことなく排出量を削減できる水素ベースのプロセスへの段階的な移行を促しています。こうした動向が収束するにつれ、商用水素生成市場は今後10年間で構造的な変革を遂げることになります。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 275億米ドル |

| 予測金額 | 575億米ドル |

| CAGR | 7.8% |

プロセスの種類に基づくと、蒸気改質器のカテゴリーは2034年までCAGR 7.6%で拡大すると予測されます。その継続的な関連性は、コスト効率と既存の天然ガスインフラとの互換性にあります。より新しい方法が脚光を浴びつつあるが、水蒸気改質は産業用水素のニーズに対する拡張性と信頼性により、依然として広く採用されています。パイプラインネットワークとのシームレスな統合により、様々な用途ゾーンにおける商用水素の流通をサポートする役割がさらに強化されます。

用途別では、市場は石油精製、化学、金属、その他のセグメントに分類されます。石油精製セグメントは2024年に市場の52.2%を占め、最大の収益シェアを占めました。製油所では、排出規制の強化に対応し、川下事業の環境フットプリントを削減するため、水素の採用が増加しています。環境に優しい原料やよりクリーンな燃料を求める動きが高まり、製油所はプロセスをアップグレードし、脱硫装置や水素化分解装置に水素を統合するよう求められています。このような精製業界における継続的な変革は、信頼性の高いオンデマンドの商用水素サービスを提供する水素サプライヤーに大きなビジネスチャンスをもたらしています。

地域別では、北米商用水素生成市場が2024年の世界収益の24.3%を占める。この地域では米国が一貫した成長を示しており、市場規模は2022年の49億米ドルから2024年には54億米ドルに増加します。強力な政策枠組みと、連邦政府機関と民間企業間の協力関係の拡大が、全米の水素エコシステムを活性化しています。政府が支援する資金援助プログラムとクリーンエネルギーインセンティブは、特に水素ハブや燃料補給コリドー周辺のインフラ整備を促しています。輸送とロジスティクス能力の拡大は、水素商取引ソリューションの産業規模での採用を加速する上で重要な役割を果たしています。

市場のリーダーたちは、低炭素認証基準に準拠しながら、プロジェクトの経済性を最適化し、生産量を拡大するために多額の投資を行っています。産業クラスターやモビリティゾーンのような需要の高い中心地の近くに商用の水素ハブを配置し、配送コストを最小限に抑え、供給対応力を高めることに戦略的重点が置かれています。これらの企業はまた、業務を合理化し、配送スケジュールを改善し、水素サプライチェーン全体のリアルタイム可視性を維持するためのデジタル技術を模索しています。オンサイト発電、ネットワーク化されたインフラ、スマート配送管理システムを組み合わせた統合ビジネスモデルは、大手企業の間で標準的な慣行となりつつあります。

競争力を高めるため、各社は戦略的パートナーシップを通じて地域的プレゼンスを強化し、規制のロードマップに沿い、大規模展開のための資金支援を確保しています。このような努力を活用することで、業界参加者は、幅広い最終用途部門における低炭素水素の需要拡大に対応し、世界のエネルギー転換の未来を形作ることができます。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- 業界エコシステム

- 規制情勢

- 業界への影響要因

- 促進要因

- 業界の潜在的リスク&課題

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア

- 戦略的ダッシュボード

- 戦略的取り組み

- 競合ベンチマーキング

- イノベーションと持続可能性の情勢

第5章 市場規模・予測:工程別、2021年~2034年

- 主要動向

- 蒸気改質器

- 電解

- その他

第6章 市場規模・予測:用途別、2021年~2034年

- 主要動向

- 石油精製所

- 化学薬品

- 金属

- その他

第7章 市場規模・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- イタリア

- オランダ

- ロシア

- アジア太平洋地域

- 中国

- インド

- 日本

- 中東・アフリカ

- サウジアラビア

- イラン

- アラブ首長国連邦

- 南アフリカ

- ラテンアメリカ

- ブラジル

- アルゼンチン

- チリ

第8章 企業プロファイル

- Air Liquide

- Axpo Holding

- Air Products and Chemicals

- Cummins

- Coregas

- Linde

- Messer Group

- Nel Hydrogen

- Plug Power

- Sumitomo Corporation

- TotalEnergies

- Uniper

The Global Merchant Hydrogen Generation Market was valued at USD 27.5 billion in 2024 and is estimated to grow at a CAGR of 7.8% to reach USD 57.5 billion by 2034. The market is experiencing steady momentum as governments and industries worldwide place greater emphasis on reducing carbon emissions. This shift is driving demand for clean energy sources, including hydrogen, which has emerged as a key player in the global decarbonization agenda. Policies aimed at achieving net-zero goals, along with rising climate awareness across sectors, are creating favorable conditions for the expansion of merchant hydrogen generation.

One of the major growth enablers is the increasing scale of renewable energy deployment, which creates synergies with hydrogen production through surplus power utilization. As energy systems become more diversified and decentralized, hydrogen is becoming an important tool for energy storage and grid balancing. In this landscape, new-generation electrolysis technologies, such as proton exchange membrane and solid oxide electrolysis, are gaining traction. These innovations offer high efficiency and cost advantages, making hydrogen generation more viable at commercial scales. Industries are actively aligning their operations with sustainability targets, particularly in energy-intensive sectors like steel, refining, and chemicals. This transition is encouraging a gradual shift toward hydrogen-based processes that can lower emissions without compromising productivity. As these trends converge, the merchant hydrogen generation market is positioned for structural transformation over the next decade.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $27.5 Billion |

| Forecast Value | $57.5 Billion |

| CAGR | 7.8% |

Based on process type, the steam reformer category is projected to expand at a CAGR of 7.6% through 2034. Its continued relevance lies in its cost efficiency and compatibility with existing natural gas infrastructure. While newer methods are gaining prominence, steam reforming remains widely adopted due to its scalability and reliability for industrial hydrogen needs. Its seamless integration with pipeline networks further strengthens its role in supporting merchant hydrogen distribution across various application zones.

On the basis of application, the market is categorized into petroleum refinery, chemical, metal, and other segments. The petroleum refinery segment accounted for the largest revenue share in 2024, holding 52.2% of the market. Refineries are increasingly adopting hydrogen to meet tightening emission regulations and reduce the environmental footprint of downstream operations. The rising push for green feedstocks and cleaner fuel outputs is prompting refiners to upgrade processes and integrate hydrogen into desulfurization and hydrocracking units. This ongoing transformation within the refining landscape is creating substantial opportunities for hydrogen suppliers offering reliable, on-demand merchant hydrogen services.

Regionally, the North American merchant hydrogen generation market accounted for 24.3% of global revenue in 2024. Within this region, the United States has shown consistent growth, with market values rising from USD 4.9 billion in 2022 to USD 5.4 billion in 2024. A strong policy framework, combined with growing collaboration between federal agencies and private enterprises, is catalyzing the hydrogen ecosystem across the country. Government-backed funding programs and clean energy incentives are encouraging infrastructure buildout, particularly around hydrogen hubs and refueling corridors. The expansion of transportation and logistics capabilities is playing a key role in accelerating industrial-scale adoption of merchant hydrogen solutions.

Market leaders are investing heavily in optimizing project economics and scaling production volumes while complying with low-carbon certification standards. There is a strategic focus on placing merchant hydrogen hubs near high-demand centers like industrial clusters and mobility zones to minimize delivery costs and enhance supply responsiveness. These firms are also exploring digital technologies to streamline operations, improve delivery timelines, and maintain real-time visibility across hydrogen supply chains. Integrated business models that combine on-site generation, networked infrastructure, and smart delivery management systems are becoming standard practice among major players.

To gain a competitive edge, companies are strengthening their regional presence through strategic partnerships, aligning with regulatory roadmaps, and securing funding support for large-scale deployment. By leveraging these efforts, industry participants are well-positioned to meet the growing demand for low-carbon hydrogen across a broad spectrum of end-use sectors, thereby shaping the future of the global energy transition.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.2 Base estimates & calculations

- 1.3 Forecast calculation

- 1.4 Primary research & validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

Chapter 4 Competitive landscape, 2024

- 4.1 Introduction

- 4.2 Company market share

- 4.3 Strategic dashboard

- 4.4 Strategic initiative

- 4.5 Competitive benchmarking

- 4.6 Innovation & sustainability landscape

Chapter 5 Market Size and Forecast, By Process, 2021 - 2034 (USD Billion)

- 5.1 Key trends

- 5.2 Steam reformer

- 5.3 Electrolysis

- 5.4 Others

Chapter 6 Market Size and Forecast, By Application, 2021 - 2034 (USD Billion)

- 6.1 Key trends

- 6.2 Petroleum refinery

- 6.3 Chemical

- 6.4 Metal

- 6.5 Others

Chapter 7 Market Size and Forecast, By Region, 2021 - 2034 (USD Billion)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.2.3 Mexico

- 7.3 Europe

- 7.3.1 Germany

- 7.3.2 Italy

- 7.3.3 Netherlands

- 7.3.4 Russia

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 India

- 7.4.3 Japan

- 7.5 Middle East & Africa

- 7.5.1 Saudi Arabia

- 7.5.2 Iran

- 7.5.3 UAE

- 7.5.4 South Africa

- 7.6 Latin America

- 7.6.1 Brazil

- 7.6.2 Argentina

- 7.6.3 Chile

Chapter 8 Company Profiles

- 8.1 Air Liquide

- 8.2 Axpo Holding

- 8.3 Air Products and Chemicals

- 8.4 Cummins

- 8.5 Coregas

- 8.6 Linde

- 8.7 Messer Group

- 8.8 Nel Hydrogen

- 8.9 Plug Power

- 8.10 Sumitomo Corporation

- 8.11 TotalEnergies

- 8.12 Uniper