|

市場調査レポート

商品コード

1911364

水素生成:市場シェア分析、業界動向と統計、成長予測(2026年~2031年)Hydrogen Generation - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 水素生成:市場シェア分析、業界動向と統計、成長予測(2026年~2031年) |

|

出版日: 2026年01月12日

発行: Mordor Intelligence

ページ情報: 英文 125 Pages

納期: 2~3営業日

|

概要

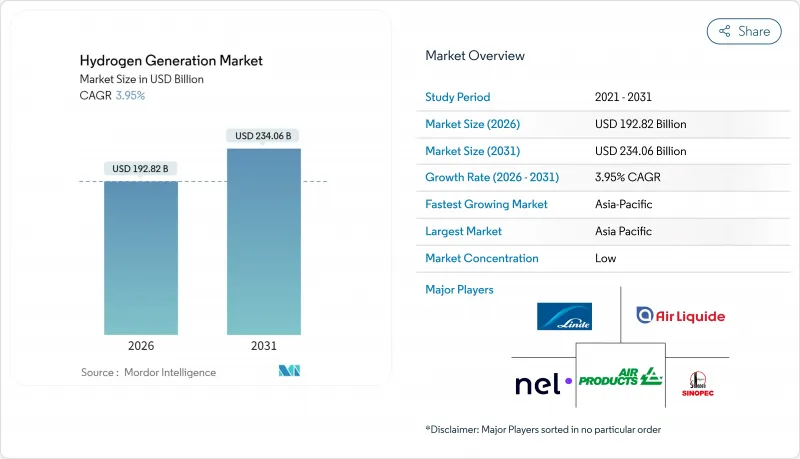

水素生成市場は、2025年に1,854億9,000万米ドルと評価され、2026年の1,928億2,000万米ドルから2031年までに2,340億6,000万米ドルに達すると予測されています。

予測期間(2026-2031年)におけるCAGRは3.95%と見込まれます。

この拡大は、政策支援を受けた低炭素分子の需要が化石由来の供給を置き換えることで生じており、電解および炭素回収設備の改修への投資を加速させています。欧州連合の非生物由来再生可能燃料(RFNBO)規則や米国のセクション45V生産税額控除といった規制メカニズムは、自主的な脱炭素化努力を順守義務へと転換し、水素生成市場に予測可能な収益基盤をもたらしています。再生可能電力価格の低下と電解装置ギガファクトリーの規模拡大に伴い技術コストが再設定される一方、炭素価格制度によりグレー分子とクリーン分子のコスト差が拡大します。同時に、鉄鋼・アンモニア・メタノールなどの産業セクターが長期オフテイク契約を締結することで、ギガワット規模プロジェクトのリスクが低減され、水素生成市場は従来の製油所中心から多様化が進みます。

世界の水素生成市場の動向と展望

EUのRFNBO義務化が認証グリーン水素需要を喚起

RFNBO枠組みは、製油所、化学プラント、鉄鋼メーカーに対し、認証済み再生可能水素の調達を義務付け、グリーン分子をコンプライアンス商品へと転換します。初回7億2,000万ユーロの入札により、化石由来供給と再生可能供給のコスト差が縮小し、ギガワット級電解装置アレイの最終投資決定が可能となりました。追加性および時間的相関性に関する認証規則は、プレミアム製品グレードを差別化し、専用の再生可能エネルギーPPA(電力購入契約)を促進します。EWEなどの公益事業会社は、陸上風力発電所と連動する280MWの電解装置を設置しており、2027年の稼働開始を予定しています。構造化されたオフテイク契約はプロジェクトファイナンスを支え、設備ベンダーに複数年にわたる受注の見通しを提供します。

米国セクション45V税額控除が国内電解装置の建設を加速

2025年1月に確定したセクション45Vは、CO2換算4kg未満で製造された水素に対し最大3米ドル/kgを付与し、多くの米国プロジェクトを即座に採算域に導きます。3段階のインセンティブは時間単位の再生可能エネルギー対応を奨励し、グリッド規模の貯蔵と先進的なエネルギー管理システムを促進します。ネルASAはミシシッピ州電解装置工場拡張のため連邦資金を確保し、プラグパワーはオーストラリアのグリーンアンモニア計画向けに3GWの設備受注を獲得。米国政策が牽引する世界の製造規模を実証しました。10年間の税額控除確実性により長期PPAが実現する一方、開発業者は政治変動シナリオをモデル化し下振れリスクをヘッジしています。

GW規模電解事業向けティア1再生可能PPAの不足

欧州の130GW規模の電解装置計画のうち、資金調達が確定しているのはごく一部に留まっています。開発業者が競争力のある価格で長期の再生可能エネルギーPPAを確保できないためです。データセンター、EV充電ネットワーク、従来型産業が同じ認証済み電力を争うため、水素プロジェクトの利益率が圧迫されています。ドイツの全国水素幹線料金(25ユーロ/kWh)やオランダのグリーン電力使用義務(4%)がPPAプレミアムをさらに押し上げています。洋上風力入札が加速しない限り、多くのプロジェクトは2027年以降にずれ込み、短期的な供給スケジュールが逼迫する見込みです。

セグメント分析

2025年時点で世界の水素需要の97.21%をグレー水素が供給し、水蒸気改質法や石炭ガス化への歴史的依存を固めました。この支配的状況は電解供給の急成長軌道を覆い隠しており、グリーン水素の供給量は2031年までにCAGR32.6%で増加すると予測されています。この急増により、規制順守を重視する顧客が再生可能エネルギー限定の契約枠を設定する動きが広がり、調達パターンが変化しています。グリーン水素の市場規模は、政策インセンティブが平準化コストの上昇を相殺する欧州と北米で最も拡大が見込まれます。既存資産所有者は低炭素認証を確保するため特定プラントに炭素回収設備を後付けし、プロジェクト開発者は再生可能エネルギーPPAとパイプラインアクセスを長期供給契約に組み込んでいます。

ブルー水素は、特に枯渇した貯留層をCO2貯蔵に活用できるガス資源豊富な地域において、過渡的な橋渡し役となります。固体炭素製品別を生成するターコイズ水素の製造プロセスはベンチャー資金を集めていますが、商業化前段階にあります。ピンク水素は、原子力発電容量が高く再生可能エネルギー用地の限られた国々においてニッチな存在を維持しており、電力会社にとって間欠性リスクのないベースロード脱炭素化の選択肢を提供します。各製造プロセスの成熟度に応じた投資タイミングの調整が可能となり、水素生成市場における分散投資ポートフォリオの選択肢が広がります。

水素生成市場レポートは、原料別(グレー水素、ブルー水素、グリーン水素、その他)、技術別(水蒸気改質法、石炭ガス化、電解法、その他)、用途(石油精製、化学プロセス、鉄鋼、輸送用燃料、電力・エネルギー貯蔵、その他)、地域(北米、欧州、アジア太平洋、南米、中東・アフリカ)ごとに分類されています。

地域別分析

2025年時点でアジア太平洋地域は世界収益の54.08%を占めており、中国の広範な石炭ガス化設備群と電解槽導入の加速がこれを支えています。北京の二本立てモデルは既存のグレー水素生産を維持しつつ、内モンゴルと沿岸工業地帯を結ぶ世界最大の専用水素パイプラインを整備しています。インドの「国家グリーン水素ミッション」は、採算ギャップ資金と電解槽スタックの輸入関税免除により支援され、同国を次なる成長フロンティアとして位置づけております。高日射量のASEAN諸国、特にインドネシアとマレーシアは、日本や韓国の買い手と連結した輸出志向型アンモニア回廊を開発中です。

欧州は市場規模では第2位ですが、政策の集中度では首位です。RFNBO割当制度、240億ユーロ規模のドイツ基幹パイプライン、HYBRITのような水素ベースの製鉄事業が、同地域を大規模なクリーン分子導入へと導いています。プロジェクトのボトルネックは主に低コスト再生可能エネルギーの電力購入契約(PPA)不足に起因しますが、洋上風力発電の入札スケジュール加速により追加容量の解放が図られています。北欧の水力発電はスカンジナビアの電解装置プロジェクトに安定的で低炭素な電力供給を提供し、大陸部の競合地域と比較して水素の納入コストを低減しています。

北米では、セクション45Vの優遇措置、豊富な風力・太陽光資源、そしてメキシコ湾岸や中西部における確立された産業クラスターが利点となります。カナダの炭素価格政策と水力資源豊富な州は、アジアや欧州をターゲットとした輸出向けクリーンアンモニアプロジェクトを支えています。米国開発者にとって、特に乾燥した西部諸州では、水資源管理と許可取得のタイムラインが依然として主要な障壁となっています。中東では、サウジアラビア、オマーン、アラブ首長国連邦において、競争力のある再生可能エネルギーを活用し、既存のタンカー航路でグリーンアンモニアを輸送するGW規模の統合ハブが開発されています。アフリカの新興パイプラインはナミビアとモーリタニアに焦点を当てており、世界クラスの太陽光資源、土地の可用性、EUへの近接性が相まって、初期段階の資本を惹きつけています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- アナリストによる3ヶ月間のサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- EUの再生可能・低炭素・非化石エネルギー(RFNBO)義務化がグリーン水素の引き取り契約を加速

- IRA及び米国セクション45V税額控除による国内電解槽建設促進

- 中国の石炭水素混合政策がグレー・ブループロジェクトを持続させる

- 中東アンモニア輸出拠点がGW規模グリーン水素の需要を創出

- 北欧製鉄メーカーのHySustainプログラム

- 日本・オーストラリア液化水素サプライチェーン(HESC)

- 市場抑制要因

- 欧州におけるGW級電解向けTier-1再生可能PPAの不足

- 米国メキシコ湾岸地域の水ストレスがPEM導入に与える制約

- 韓国における既存小型モジュール炉(SMR)ユニットの高コストなCO2回収

- カリブ諸島における水素パイプライン規格と安全許可の制限

- サプライチェーン分析

- 規制情勢

- テクノロジーの展望

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場規模と成長予測

- 由来別

- グレー水素

- ブルー水素

- グリーン水素

- ターコイズ水素

- ピンク水素

- 技術別

- 蒸気メタン改質(SMR)

- 石炭ガス化

- オートサーマル改質(ATR)

- 部分酸化(POX)

- 電解(アルカリ電解、プロトン交換膜(PEM)、固体酸化物電解(SOE))

- 用途別

- 石油精製

- 化学プロセス(アンモニア、メタノール)

- 鉄鋼(直接還元鉄(DRI)、水素製錬(H2-BF))

- 輸送用燃料(FCEV、船舶、航空)

- 電力・エネルギー貯蔵

- 住宅用および商業用暖房

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- 英国

- ドイツ

- フランス

- スペイン

- 北欧諸国

- トルコ

- ロシア

- その他欧州地域

- アジア太平洋地域

- 中国

- インド

- 日本

- 韓国

- ASEAN諸国

- オーストラリア

- その他アジア太平洋地域

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 中東・アフリカ

- アラブ首長国連邦

- サウジアラビア

- エジプト

- 南アフリカ

- その他中東・アフリカ地域

- 北米

第6章 競合情勢

- 市場集中度

- 戦略的動き(M&A、パートナーシップ、PPA)

- 市場シェア分析(主要企業の市場順位・シェア)

- 企業プロファイル

- Linde plc

- Air Liquide

- Air Products & Chemicals

- Sinopec

- Engie SA

- Nel ASA

- Cummins Inc.

- ITM Power plc

- Plug Power Inc.

- Siemens Energy AG

- McPhy Energy SA

- FuelCell Energy

- Enapter AG

- Bloom Energy

- Ballard Power Systems

- Johnson Matthey PLC

- Kawasaki Heavy Industries

- Messer Group GmbH

- Taiyo Nippon Sanso Corp.

- Doosan Fuel Cell