|

市場調査レポート

商品コード

1645101

東南アジアの水素生成:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)Southeast Asia Hydrogen Generation - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 東南アジアの水素生成:市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 110 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

概要

東南アジアの水素生成の市場規模は2025年に89億4,000万米ドルと推定され、予測期間(2025-2030年)のCAGRは2.14%で、2030年には99億4,000万米ドルに達すると予測されます。

主なハイライト

- 中期的には、脱硫、温室効果ガス排出、水素の生産と消費の奨励に関する政府の支持的な政策と政策などの要因が、予測期間中に東南アジア地域の水素生成市場を牽引するとみられます。

- 一方、水素エネルギー貯蔵の製造コストが高いことが、水素生成の成長を抑制すると予想されます。

- とはいえ、原子力、風力、太陽光、バイオマス、水力、地熱などの再生可能エネルギー源から水素を抽出する技術の進歩と、燃料としての水素の用途の高まりが相まって、今後数年間は水素生成市場に有利な成長機会がもたらされるものと思われます。

- インドネシアは、予測期間中に東南アジアの水素生成市場で著しい成長を遂げることが期待されています。政府の支援政策と投資によるものです。

東南アジアの水素生成市場の動向

グリーン水素は重要なセグメント

- グリーン水素は、電気を用いて水を水素と酸素に分解する電気分解と呼ばれるプロセスを通じて製造されます。このプロセスで使用される電力は、風力、太陽光、水力などの再生可能エネルギー源から供給されます。このため、製造される水素は純粋に「グリーン」であり、二酸化炭素排出量も最小限に抑えられます。

- 2023年、この地域の水素生産量は約360万トンに達しました。この水素は主に精製プロセスや、アンモニアやメタノールのような化学物質の合成に利用されました。特筆すべきは、この水素のほとんどすべてが天然ガスの水蒸気改質によって生産されたことで、炭素回収・利用・貯蔵(CCUS)技術は組み込まれていないです。

- 大規模な投資は、東南アジアにおけるグリーン水素の野心的な見通しを証明しています。例えば、2024年10月、TTCL公開会社は、ラオスにグリーン水素プラントを設立するため、12億バーツの契約を獲得しました。このプロジェクトは、再生可能エネルギーを利用してラオスの水素生産能力を強化することを目的としています。

- さらに2024年2月には、マレーシア最大のグリーン水素プロジェクトである、浮体式太陽光発電によるペラック州の60MWプラントが、民間投資家から18億8,000万リンギット(3億9,360万米ドル)を獲得しました。このような投資は、東南アジア地域におけるグリーン水素市場の需要の高まりを浮き彫りにしています。

- この地域では、主に石油化学、鉄鋼、発電などの重工業からの排出を最小限に抑えようとする試みが行われており、その結果、グリーン水素の生産と使用を上回る対策がとられています。その結果、グリーン水素インフラへの投資が加速し、東南アジア全域で共同プロジェクトが立ち上がりつつあります。この勢いは、この地域の脱炭素化目標とエネルギー転換の取り組みに大きく貢献すると期待されています。

- 2024年10月、セノコ・エナジーとジェンタリは、マレーシアからシンガポールへの水素ガス輸入を検討するMoUに調印し、2029年までにセノコのガスタービン資産に統合することを目指しています。この協力により、二酸化炭素排出量を大幅に削減し、シンガポールの2050年ネット・ゼロ目標を支援します。

- さらに、鉄鋼メーカーのメランティは2023年、タイに東南アジア初のグリーン平鋼工場を建設する計画を発表しました。この工場では、石炭の代わりに水素を使用し、再生可能エネルギーによる電気アーク炉技術を採用してグリーン・スチールを生産します。2027年までに操業開始予定で、年間生産能力は200万トン、年間400万トンの二酸化炭素排出量を削減します。

- 国際再生可能エネルギー機関(IRENA)によると、2023年、東南アジアの再生可能エネルギー容量は、ベトナムの46,012MWを筆頭に、タイの12,547MW、マレーシアの9,052MW、フィリピンの7,832MW、シンガポールの1,147MWと続く。この充実した再生可能エネルギー・インフラは、グリーン水素製造の強力な基盤となります。

- このような要因から、グリーン水素セグメントは予測期間中、水素生成市場に大きな影響を与えると思われます。

著しい成長を遂げるインドネシア

- インドネシアが2060年までに排出量ネットゼロの目標を達成するために再生可能エネルギーに軸足を移す中、水素エネルギーが注目の的となっています。豊富な資源と戦略的な位置づけを持つインドネシアは、水素製造、特に再生可能な資源に由来するグリーン水素において、地域のリーダーになる準備が整っています。

- インドネシア水素エネルギー見通し2024」の調査結果によると、アンモニア需要の増加により、2060年までにインドネシアの水素需要は年間約200万トン(MTPA)に増加すると予想されています。

- 世界鉄鋼協会によると、インドネシアの鉄鋼生産量は2019年の856万トンから2023年には1,680万トンへと着実に増加しています。この鉄鋼生産量の増加は、産業需要の増加を裏付けており、従来の化石燃料に代わるよりクリーンな水素、主にグリーン水素の必要性を後押ししています。

- インドネシアは、2060年のネット・ゼロ・エミッション目標を達成するため、再生可能エネルギーに重点を移しています。この移行の中心となるのが水素エネルギーです。インドネシアは、その豊富な資源と有利な立地を活かし、水素製造、特に再生可能エネルギーから供給されるグリーン水素製造において、地域の大国としての地位を確立しつつあります。

- 例えば2024年10月、センブコープ・インダストリーズ社は子会社のSembcorp Utilities Pte Ltdを通じて、インドネシアのスマトラ島にグリーン水素製造施設を設立する契約をPT PLN Energi Primer Indonesiaと締結しました。この施設は年間10万トンを生産する予定で、東南アジア最大のグリーン水素の取り組みとなります。このプロジェクトは、スマトラ島、リアウ諸島、シンガポールを結ぶ地域のグリーン水素ハブの創設を目指しています。

- 2024年10月、PTプルタミナ・パワー・インドネシア(「プルタミナNRE」)、PTプルタミナ地熱エネルギーTbk(「PGE」)、Genviaは、覚書(MoU)に署名し、パートナーシップを強固なものにしました。両社の協力関係の中心は、地熱熱源とともに先進的な固体酸化物電解槽(SOEL)技術を活用したグリーン水素製造です。MoUには、グリーン水素製造におけるエネルギー消費の最適化を目的とした、ジェンビアの最先端高温SOEL技術の技術的・経済的評価が含まれます。

- さらに、PT Kilang Pertamina Internasionalは、西パプア州ビントゥニ湾にブルーアンモニア施設の建設を計画しました。この工場は2030年に操業を開始する予定で、ブルーアンモニアの生産能力は約87万5,000TPA(トン/年)を目指しており、これにより約15万TPAのブルー水素の需要が見込まれます。同施設は、1日当たり9,000万標準立方フィート(MMSCFD)の天然ガスを処理するよう設計されています。

- 従って、上記の要因から、インドネシアは予測期間中、東南アジアの水素生成市場で大きな成長を遂げると予想されます。

東南アジアの水素生成産業の概要

東南アジアの水素生成市場は統合されています。同市場の主要企業(順不同)には、Linde PLC、Messer Group GmbH、Air Liquide SA、Air Products and Chemicals Inc.、Engie SAなどがあります。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査範囲

- 市場の定義

- 調査の前提

第2章 エグゼクティブサマリー

第3章 調査手法

第4章 市場概要

- イントロダクション

- 2029年までの市場規模および需要予測(単位:米ドル)

- 最近の動向と開発

- 政府の規制と政策

- 市場力学

- 促進要因

- 精製および工業分野からの需要増加

- 有利な政府政策

- 抑制要因

- 水素エネルギー貯蔵のための高い資本コスト

- 促進要因

- サプライチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

- 投資分析

第5章 市場セグメンテーション

- 由来(定性分析)別

- ブルー水素

- グリーン水素

- 灰色水素

- 技術別

- スチームメタン改質(SMR)

- 石炭ガス化

- その他の技術

- 用途別

- 石油精製

- 化学処理

- 鉄鋼生産

- その他の用途

- 地域別

- インドネシア

- マレーシア

- ベトナム

- シンガポール

- その他の東南アジア地域

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 主要企業の戦略

- 企業プロファイル

- Linde Plc

- Air Liquide SA

- Messer Group GmbH

- Engie S.A.

- Cummins Inc.

- Air Products and Chemicals Inc.

- Taiyo Nippon Sanso Holding Corporation

- Enapter S.r.l.

- 市場ランキング/シェア分析

- その他の有名企業一覧

第7章 市場機会と今後の動向

- 技術の進歩

目次

Product Code: 50002211

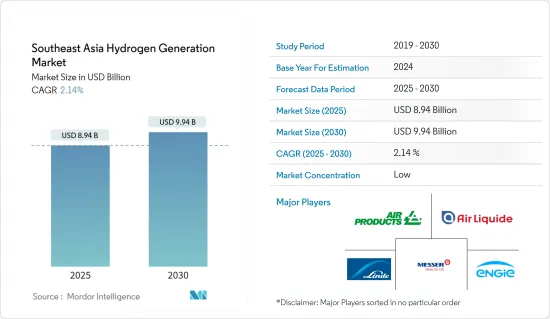

The Southeast Asia Hydrogen Generation Market size is estimated at USD 8.94 billion in 2025, and is expected to reach USD 9.94 billion by 2030, at a CAGR of 2.14% during the forecast period (2025-2030).

Key Highlights

- Over the medium term, factors such as supportive government policies and regulations for desulphurization, greenhouse gas emissions, and encouraging the production and consumption of hydrogen are likely to drive the hydrogen generation market in the Southeast Asian region during the forecast period.

- On the other hand, the high production costs of hydrogen energy storage are expected to restrain the growth of hydrogen generation.

- Nevertheless, technological advancements in extracting hydrogen from renewable sources including nuclear, wind, solar, biomass, hydro, and geothermal coupled with the rising applications of hydrogen as a fuel, are poised to unlock lucrative growth opportunities for the hydrogen generation market in the years ahead.

- Indonesia is expected to witness significant growth in the Southeast Asian hydrogen generation market during the forecast period. Owing to to supportive goverment policies and investments.

Southeast Asia Hydrogen Generation Market Trends

Green Hydrogen is a Significant Segment

- Green hydrogen is produced through a process called electrolysis, which uses electricity to split water into hydrogen and oxygen. The electricity used in this process comes from renewable sources such as wind, solar, or hydropower. This ensures that the hydrogen produced is genuinely "green" and has minimal carbon emissions.

- In 2023, the region's hydrogen production reached approximately 3.6 million tons. This hydrogen was predominantly utilized in refining processes and the synthesis of chemicals like ammonia and methanol. Notably, almost all of this hydrogen was produced via natural gas steam reforming, which did not incorporate carbon capture, utilization, and storage (CCUS) technology.

- Significant investments evidence the ambitious outlook for green hydrogen in Southeast Asia. For instance, in October 2024, TTCL Public Company Limited secured a THB 1.2 billion contract to establish a green hydrogen plant in Laos. This project aims to enhance Laos's hydrogen production capacity using renewable energy.

- Further, in February 2024, Malaysia's largest green hydrogen project, a 60MW plant in Perak state powered by floating solar, secured 1.88 billion ringgit (USD 393.6 million) from private investors. This kind of investments highlights the rising demand for the green hydrogen market in the Southeast Asia region.

- The region's attempt to minimize emissions, mainly from heavy industries like petrochemicals, iron and steel, and power generation, are resulting in measures to exceed green hydrogen production and usage. As a result, investments in green hydrogen infrastructure are accelerating, and collaborative projects are emerging across Southeast Asia. This momentum is expected to significantly contribute to the region's decarbonization goals and energy transition efforts.

- In October 2024, Senoko Energy and Gentari signed an MoU to explore importing hydrogen gas from Malaysia to Singapore, aiming to integrate it into Senoko's gas turbine assets by 2029. This collaboration seeks to reduce carbon emissions significantly, supporting Singapore's 2050 Net Zero target.

- Moreover, In 2023, Meranti, a steel manufacturer, announced plans to build Southeast Asia's first green flat steel plant in Thailand. The plant will use hydrogen to replace coal and employ electric arc furnace technology powered by renewable energy to produce green steel. Expected to be operational by 2027, the facility will have an annual production capacity of 2 million tons, reducing carbon emissions by 4 million tons annually.

- According to International Renewable Energy Agency (IRENA) In 2023, Southeast Asia saw significant renewable energy capacities, with Vietnam leading at 46,012 MW, followed by Thailand at 12,547 MW, Malaysia at 9,052 MW, the Philippines at 7,832 MW, and Singapore at 1,147 MW. This substantial renewable energy infrastructure provides a strong foundation for green hydrogen production.

- Therefore, owing to such factors, the green hydrogen segment is likely to significantly impact the hydrogen generation market during the forecast period.

Indonesia to Witness Significant Growth

- As Indonesia pivots towards renewable energy to achieve its net-zero emissions goal by 2060, hydrogen energy is emerging as a focal point. With its abundant resources and strategic positioning, Indonesia is poised to become a regional leader in hydrogen production, particularly in green hydrogen, which is derived from renewable sources.

- According to the findings in the Indonesia Hydrogen Energy Outlook 2024, by 2060, Indonesia's hydrogen demand is expected to increase to around 2 million tonnes per annum (MTPA) due to the increasing demand for Ammonia.

- According to the World Steel Association, Indonesia's steel production has steadily increased from 8.56 million tonnes in 2019 to 16.8 million tonnes in 2023. This rising steel production underscores the growing industrial demand, which drives the need for hydrogen, mainly green hydrogen, as a cleaner alternative to traditional fossil fuels.

- Indonesia is shifting its focus to renewable energy in pursuit of its net-zero emissions target for 2060. Central to this transition is hydrogen energy. Leveraging its rich resources and advantageous location, Indonesia is on track to establish itself as a regional powerhouse in hydrogen production, especially green hydrogen sourced from renewables.

- For instance, in October 2024, Sembcorp Industries, through its subsidiary Sembcorp Utilities Pte Ltd, signed an agreement with PT PLN Energi Primer Indonesia to establish a green hydrogen production facility in Sumatra, Indonesia. This facility will produce 100,000 metric tonnes annually, making it Southeast Asia's largest green hydrogen initiative. The project aims to create a regional green hydrogen hub connecting Sumatra, the Riau Islands, and Singapore.

- In October 2024, PT Pertamina Power Indonesia ("Pertamina NRE"), PT Pertamina Geothermal Energy Tbk ("PGE"), and Genvia solidified their partnership by signing a Memorandum of Understanding (MoU). Their collaboration centers on green hydrogen production, utilizing advanced solid oxide electrolyzer (SOEL) technology alongside geothermal heat sources. The MoU includes a technical and economic assessment of Genvia's state-of-the-art high-temperature SOEL technology, with the goal of optimizing energy consumption in green hydrogen production.

- Additionally, PT Kilang Pertamina Internasional planned to construct a blue ammonia facility in Bintuni Bay, West Papua Province. The plant is expected to commence operations in 2030, aiming for a blue ammonia production capacity of around 875,000 TPA (tons per annum) of blue ammonia, which is expected to create a demand for blue hydrogen of around 150,000 TPA. The facility is designed to process 90 million standard cubic feet per day (MMSCFD) of natural gas.

- Therefore, based on the above-mentioned factors, Indonesia is expected to witness significant growth in the Southeast Asia hydrogen generation market during the forecast period.

Southeast Asia Hydrogen Generation Industry Overview

The Southeast Asia hydrogen generation market is consolidated. Some of the major players in the market (in no particular order) include Linde PLC, Messer Group GmbH, Air Liquide SA, Air Products and Chemicals Inc., Engie SA, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 EXECUTIVE SUMMARY

3 RESEARCH METHODOLOGY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD, till 2029

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Increasing Demand From Refining And Industrial Sector

- 4.5.1.2 Favourable Government Policies

- 4.5.2 Restraints

- 4.5.2.1 High Capital Costs For Hydrogen Energy Storage

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes Products and Services

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Investment Analysis

5 MARKET SEGMENTATION

- 5.1 Source (Qualitative Analysis)

- 5.1.1 Blue Hydrogen

- 5.1.2 Green Hydrogen

- 5.1.3 Grey Hydrogen

- 5.2 Technology

- 5.2.1 Steam Methane Reforming (SMR)

- 5.2.2 Coal Gasification

- 5.2.3 Other Technologis

- 5.3 Application

- 5.3.1 Oil Refining

- 5.3.2 Chemical Processing

- 5.3.3 Iron & Steel Production

- 5.3.4 Other Applications

- 5.4 Geography

- 5.4.1 Indonesia

- 5.4.2 Malaysia

- 5.4.3 Vietnam

- 5.4.4 Singapore

- 5.4.5 Rest of Southeast Asia

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 Linde Plc

- 6.3.2 Air Liquide SA

- 6.3.3 Messer Group GmbH

- 6.3.4 Engie S.A.

- 6.3.5 Cummins Inc.

- 6.3.6 Air Products and Chemicals Inc.

- 6.3.7 Taiyo Nippon Sanso Holding Corporation

- 6.3.8 Enapter S.r.l.

- 6.4 Market Ranking/ Share Analysis

- 6.5 List of Other Prominent Companies

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Technological Advancements