製パン原料の市場機会、成長促進要因、産業動向分析、2025年~2034年予測

Baking Ingredients Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 235 Pages

- 納期

- 2~3営業日

- 商品コード

- 1766362

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

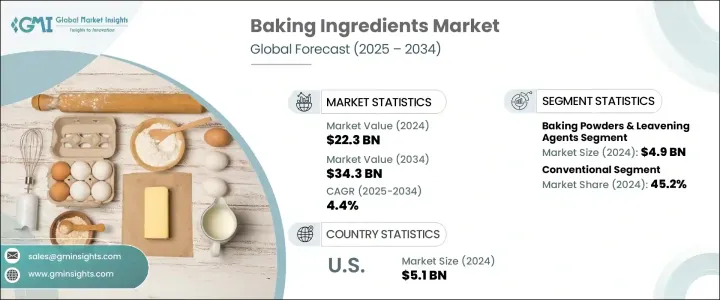

製パン原料の世界市場は、2024年には223億米ドルと評価され、CAGR 4.4%で成長し、2034年には343億米ドルに達すると推定されています。

この市場は、様々なカテゴリーのベーカリー製品における世界の需要の高まりに後押しされ、安定した成長を示しています。世界の消費パターンの広範な変化を反映して、売上高と数量は一貫した増加を示しています。この動向の主要因としては、食生活の変化、都市化の進展、既製食品への嗜好の高まりなどが挙げられます。特に新興地域では、包装された簡便な焼き菓子の人気が高まっており、高性能の製パン原料に対するニーズが加速しています。同時に、成熟経済は引き続き堅調な需要を示しており、市場全体の勢いを維持するのに役立っています。

フードサービスネットワークと組織型小売業態の拡大も、製品へのアクセスを改善し、市場での数量の増加とベーカリー製品の多様化につながっています。都市部でも準都市部でも近代的な小売店舗が増え続けているため、消費者は職人技が光るパンから包装された便利な商品まで、多種多様な焼き菓子に触れる機会が増えています。このような入手しやすさの向上は、衝動買いを後押しするだけでなく、新しい製品タイプや味を試すきっかけにもなっています。さらに、小売チェーンとベーカリーメーカーとの提携により、商品の配置や販促キャンペーン、店内のベーカリーコーナーが充実し、消費者の関心がさらに高まり、複数の人口層や消費シーンにわたってカテゴリーの成長を促進しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年 | 2025~2034年 |

| 開始金額 | 223億米ドル |

| 予測金額 | 343億米ドル |

| CAGR | 4.4% |

2024年、ベーキング粉末と膨脹剤セグメントは49億米ドルを生み出し、2025~2034年にかけてCAGR 4.8%で成長すると予測されています。これらの原料は、安定した通気性、ボリューム、食感を確保する役割を果たすため、焼き菓子製造には欠かせない存在であり続けています。産業用と家庭用の製パンの両方で広く使用されていることが、市場の支配的地位を強化しています。都市人口、特に大都市の人口が増加するにつれて、加工済みと包装済みのベーカリー製品に対する需要は増加の一途をたどっており、そのため膨脹剤の消費量も増加しています。さらに、より新しいクリーンラベルの選択肢や改良された配合は、信頼できる結果をもたらすと同時に、進化する消費者の需要に応えています。コスト効率に優れているため、小規模のベーカリー、業務用厨房、フードサービス業務において不可欠な要素となっています。

従来型原料セグメントは2024年に101億米ドルと評価され、2034年までCAGR 4.6%で成長し、45.2%のシェアを占めると予測されています。従来型製品の信頼性と手頃な価格により、大量生産ニーズを満たすための好ましい選択肢であり続けています。その一方で、クリーンラベルや非遺伝子組み換えの代替品への注目が高まっており、健康志向の選択肢とコスト効率の高いソリューションのバランスを提供することで、市場力学が再構築されつつあります。食の安全や環境への影響に対する懸念から、オーガニックやトレイサブルな選択肢に目を向ける消費者層が増加しており、天然材料フォーマットの牽引力が高まっていることを示しています。

米国の製パン原料2024年の市場規模は51億米ドルで、2025~2034年にかけてCAGR 4.2%で成長する見込みです。この堅調な業績は、強力な食品製造基盤、加工されたベーカリー製品に対する消費者の需要の高まり、強固なサプライチェーンインフラによってもたらされます。特に植物性、グルテンフリー、糖質制限、ヴィーガンなどの需要に合わせた製品では、原料配合の革新が市場成長の維持に大きな役割を果たしています。小売店の拡大や包装入り焼き菓子への嗜好の高まりが、この上昇傾向をさらに後押ししています。

ピュラトス・グループ、レザフレ、カーギルなど、世界の製パン材料産業の主要企業は、世界の事業基盤を強化するため、革新的なアプローチを積極的に展開しています。これらの企業は、現代の食生活の嗜好に合わせたクリーンラベル、機能性、栄養豊富な原料を導入するための研究開発を優先しています。フードサービスチェーンやリテールベーカリーとの提携は、顧客範囲の拡大に役立っています。また、サプライチェーンの効率性と地域の需要への対応力を確保するため、地域の生産拠点に投資しています。多くの企業が製品開発と流通にデジタル化戦略を採用し、敏捷性と顧客エンゲージメントを向上させており、産業用と消費者向けの両セグメントで市場でのリーダーシップを強化しています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

- TAM分析、2025~2034年

- CXOの視点:戦略的必須事項

- 経営上の意思決定ポイント

- 重要な成功要因

- 将来の展望と戦略的提言

第3章 産業考察

- エコシステム分析

- サプライヤーの情勢

- 利益率

- 各段階での付加価値

- バリューチェーンに影響を与える要因

- ディスラプション

- 産業への影響要因

- 促進要因

- インスタント食品の需要増加

- 業務用ベーカリー部門の成長

- 可処分所得の増加

- 変化する消費者のライフスタイル

- 産業の潜在的リスク・課題

- 原料価格の変動

- 添加物に関する健康上の懸念

- 市場機会

- 促進要因

- 成長可能性分析

- 規制情勢

- 北米

- 欧州

- アジア太平洋

- ラテンアメリカ

- 中東・アフリカ

- ポーター分析

- PESTEL分析

- 価格動向

- 地域別

- 製品タイプ別

- 将来の市場動向

- 技術とイノベーションの情勢

- 現在の技術動向

- 新興技術

- 特許情勢

- 貿易統計(HSコード)(注:貿易統計は主要国のみ提供されます)

- 主要輸入国

- 主要輸出国

- 持続可能性と環境側面

- サステイナブルプラクティス

- 廃棄物削減戦略

- 生産におけるエネルギー効率

- エコフレンドリー取り組み

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 地域別

- 北米

- 欧州

- アジア太平洋

- ラテンアメリカ航空

- 中東・アフリカ

- 地域別

- 企業マトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

- 拡大計画

第5章 市場推定・予測、食材別、2021~2034年

- 主要動向

- ベーキング粉末と膨張剤

- 乳化剤

- 酵素

- 油脂、ショートニング

- 甘味料

- 色と味

- 防腐剤

- 小麦粉末

- デンプン

- その他

第6章 市場推定・予測、性質別、2021~2034年

- 主要動向

- 従来型

- オーガニック

- クリーンラベル

- 非遺伝子組み換え

第7章 市場推定・予測、用途別、2021~2034年

- 主要動向

- パン

- ケーキとペストリー

- クッキーとビスケット

- ロールパンとパイ

- ピザ生地

- その他

第8章 市場推定・予測、最終用途別、2021~2034年

- 主要動向

- 業務用/産業用パン屋

- 小売パン屋

- 職人パン屋

- 食品サービス産業

- 家庭/小売消費者

第9章 市場推定・予測、流通チャネル別、2021~2034年

- 主要動向

- B2B

- B2C

- スーパーマーケットとハイパーマーケット

- 専門店

- コンビニエンスストア

- オンライン小売

- その他

第10章 市場推定・予測、地域別、2021~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- オランダ

- その他の欧州

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- オーストラリア

- その他のアジア太平洋

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- その他のラテンアメリカ

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

- その他の中東・アフリカ

第11章 企業プロファイル

- AAK AB

- Archer Daniels Midland Company

- Associated British Foods plc

- Bakels Group

- BASF SE

- Cargill, Incorporated

- Corbion N.V.

- Dawn Food Products, Inc.

- DuPont de Nemours, Inc.

- DSM-Firmenich AG

- Flowers Foods, Inc.

- General Mills, Inc.

- Grupo Bimbo, S.A.B. de C.V.

- Ingredion Incorporated

- Kerry Group plc

- Koninklijke DSM N.V.

- Lesaffre Group

- Mondelez International, Inc.

- Puratos Group

- Tate & Lyle PLC

目次

The Global Baking Ingredients Market was valued at USD 22.3 billion in 2024 and is estimated to grow at a CAGR of 4.4% to reach USD 34.3 billion by 2034. This market demonstrates stable growth, fueled by rising global demand across various categories of baked products. Both revenue and volume have shown consistent increases, reflecting widespread changes in consumption patterns worldwide. Key factors contributing to this trend include shifting dietary habits, growing urbanization, and a rising preference for ready-made food solutions. The growing popularity of packaged and convenience baked items, particularly in emerging regions, is accelerating the need for high-performance baking ingredients. At the same time, mature economies continue to show solid demand, helping to maintain overall market momentum.

Expanding food service networks and organized retail formats have also improved product accessibility, leading to increased sales volumes and broader diversification of baked offerings in the market. As modern retail outlets continue to grow in both urban and semi-urban areas, consumers now have greater exposure to a wide variety of baked goods, ranging from artisanal breads to packaged convenience items. This enhanced availability has not only boosted impulse purchases but has also encouraged experimentation with new product types and flavors. Additionally, partnerships between retail chains and bakery manufacturers have led to better product placement, promotional campaigns, and in-store bakery sections, further elevating consumer interest and driving category growth across multiple demographics and consumption occasions.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $22.3 Billion |

| Forecast Value | $34.3 Billion |

| CAGR | 4.4% |

In 2024, the baking powders and leavening agents segment generated USD 4.9 billion and is forecast to grow at a 4.8% CAGR between 2025 and 2034. These ingredients remain vital in baked goods production due to their role in ensuring consistent aeration, volume, and texture. Their widespread use in both industrial and home baking reinforces their dominant market position. As urban populations grow, particularly in large cities, demand for processed and pre-packaged bakery items continues to rise-driving higher consumption of leavening agents. Additionally, newer clean-label options and improved formulations are catering to evolving consumer demands while delivering reliable results. Their cost-efficiency makes them an essential component across small bakeries, commercial kitchens, and food service operations.

The conventional ingredients segment was valued at USD 10.1 billion in 2024 and is projected to grow at a 4.6% CAGR through 2034, holding a 45.2% share. The reliability and affordability of conventional products ensure they remain a preferred option to meet high-volume production needs. Meanwhile, increased attention toward clean-label and non-GMO alternatives is reshaping market dynamics, offering a balance between health-conscious choices and cost-effective solutions. A growing segment of consumers is turning to organic and traceable options in response to concerns over food safety and environmental impact, signaling rising traction for natural ingredient formats.

United States Baking Ingredients Market was valued at USD 5.1 billion in 2024 and is expected to grow at a 4.2% CAGR from 2025 to 2034. This steady performance is driven by a strong food manufacturing base, rising consumer demand for processed baked items, and a robust supply chain infrastructure. Innovation in ingredient formulations plays a major role in sustaining market growth, especially for products tailored to meet demands for plant-based, gluten-free, sugar-reduced, and vegan options. Retail expansion and increasing preference for packaged baked goods across the country further support this upward trend.

Key players in the Global Baking ingredient industry, including Puratos Group, Lesaffre, Cargill, and others, are actively deploying innovative approaches to strengthen their global footprint. These companies are prioritizing research and development to introduce clean-label, functional, and nutrient-rich ingredients tailored to modern dietary preferences. Collaborations with food service chains and retail bakeries are helping them expand their customer reach. They are also investing in regional production hubs to ensure supply chain efficiency and responsiveness to local demands. Many are adopting digitalization strategies in product development and distribution to improve agility and customer engagement, reinforcing their market leadership across both industrial and consumer-facing segments.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1.1 Regional

- 2.2.1.2 Ingredient type

- 2.2.1.3 Nature

- 2.2.1.4 Application

- 2.2.1.5 End use

- 2.2.1.6 Distribution channel

- 2.3 TAM analysis, 2025-2034

- 2.4 CXO perspectives: strategic imperatives

- 2.5 Executive decision points

- 2.6 Critical success factors

- 2.7 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising demand for convenience foods

- 3.2.1.2 Growth in commercial bakery sector

- 3.2.1.3 Increasing disposable income

- 3.2.1.4 Changing consumer lifestyles

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Fluctuating raw material prices

- 3.2.2.2 Health concerns related to additives

- 3.2.3 Market opportunities

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia pacific

- 3.4.4 Latin America

- 3.4.5 Middle east & Africa

- 3.5 Porter's analysis

- 3.6 Pestel analysis

- 3.6.1 Technology and innovation landscape

- 3.6.2 Current technological trends

- 3.6.3 Emerging technologies

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By product type

- 3.8 Future market trends

- 3.9 Technology and innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent landscape

- 3.11 Trade statistics (HS code) (Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Ingredient Type, 2021-2034 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Baking powders & leavening agents

- 5.3 Emulsifiers

- 5.4 Enzymes

- 5.5 Oils, fats & shortenings

- 5.6 Sweeteners

- 5.7 Colors & flavors

- 5.8 Preservatives

- 5.9 Flour

- 5.10 Starches

- 5.11 Others

Chapter 6 Market Estimates & Forecast, By Nature, 2021-2034 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Conventional

- 6.3 Organic

- 6.4 Clean label

- 6.5 Non-GMO

Chapter 7 Market Estimates & Forecast, By Application, 2021-2034 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Bread

- 7.3 Cakes & pastries

- 7.4 Cookies & biscuits

- 7.5 Rolls & pies

- 7.6 Pizza crusts

- 7.7 Others

Chapter 8 Market Estimates & Forecast, By End Use, 2021-2034 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 Commercial/industrial bakeries

- 8.3 Retail bakeries

- 8.4 Artisanal bakeries

- 8.5 Foodservice industry

- 8.6 Household/retail consumers

Chapter 9 Market Estimates & Forecast, By Distribution Channel, 2021-2034 (USD Billion) (Kilo Tons)

- 9.1 Key trends

- 9.2 B2B

- 9.3 B2C

- 9.3.1 Supermarkets & hypermarkets

- 9.3.2 Specialty stores

- 9.3.3 Convenience stores

- 9.3.4 Online retail

- 9.3.5 Others

Chapter 10 Market Estimates & Forecast, By Region, 2021-2034 (USD Billion) (Kilo Tons)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 Germany

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Netherlands

- 10.3.7 Rest of Europe

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 Australia

- 10.4.6 Rest of Asia Pacific

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.5.4 Rest of Latin America

- 10.6 Middle East and Africa

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

- 10.6.4 Rest of Middle East and Africa

Chapter 11 Company Profiles

- 11.1 AAK AB

- 11.2 Archer Daniels Midland Company

- 11.3 Associated British Foods plc

- 11.4 Bakels Group

- 11.5 BASF SE

- 11.6 Cargill, Incorporated

- 11.7 Corbion N.V.

- 11.8 Dawn Food Products, Inc.

- 11.9 DuPont de Nemours, Inc.

- 11.10 DSM-Firmenich AG

- 11.11 Flowers Foods, Inc.

- 11.12 General Mills, Inc.

- 11.13 Grupo Bimbo, S.A.B. de C.V.

- 11.14 Ingredion Incorporated

- 11.15 Kerry Group plc

- 11.16 Koninklijke DSM N.V.

- 11.17 Lesaffre Group

- 11.18 Mondelez International, Inc.

- 11.19 Puratos Group

- 11.20 Tate & Lyle PLC

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 235 Pages

- 納期

- 2~3営業日