|

市場調査レポート

商品コード

1766359

キャプティブ水素生成市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測Captive Hydrogen Generation Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| キャプティブ水素生成市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測 |

|

出版日: 2025年06月13日

発行: Global Market Insights Inc.

ページ情報: 英文 127 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

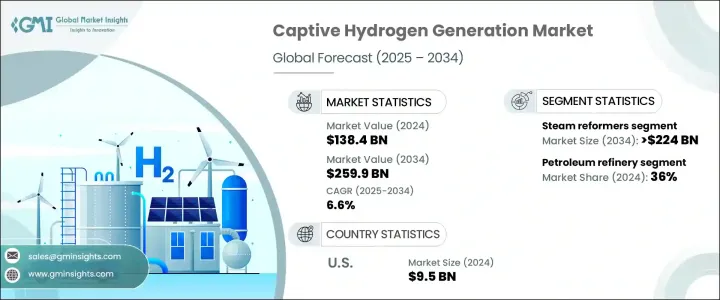

キャプティブ水素生成の世界市場規模は、2024年に1,384億米ドルとなり、CAGR 6.6%で成長し、2034年には2,599億米ドルに達すると予測されています。

持続可能なエネルギー慣行への移行と脱炭素化の推進の高まりが、オンサイト水素製造ソリューションの採用を産業界に促しています。この動向は、よりクリーンで効率的な代替燃料への需要が高まっている精製、化学、輸送などの主要セクターで特に顕著です。世界の産業界が温室効果ガスの排出削減を目指す中、キャプティブ水素システムの役割はより重要なものとなっています。クリーンな水素製造技術の進歩は、拡張性を高め、運用コストを下げ、システム全体の効率を高めることで、この勢いに貢献しており、オンサイト発電は産業ユーザーにとってますます魅力的な選択肢となっています。

特に高純度燃料を必要とするプロセスで使用される水素の需要が着実に増加しているため、市場はコンパクトなモジュール式システムへの大規模な投資から恩恵を受けると予想されます。これらのシステムは、設置の柔軟性を提供し、さまざまな生産能力に合わせることができるため、外部の水素供給業者への依存度を減らしたい中規模施設にとっては特に魅力的です。技術の進化に加え、政府の支援政策も成長を加速させています。税制優遇措置、補助金、カーボンプライシングメカニズムなどのインセンティブは、先行投資コストを相殺することで、産業界のプレーヤーがよりクリーンな燃料ソリューションへと移行するのを支援しています。キャプティブ水素生成はまた、信頼性の高い地域密着型の燃料生産が長期的なエネルギー目標に合致する、より広範なネット・ゼロ・エミッションの課題においても戦略的な役割を果たしています。これらの要因が相まって、世界市場全体が力強い成長を遂げる基盤が整いつつあります。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 1,384億米ドル |

| 予測金額 | 2,599億米ドル |

| CAGR | 6.6% |

市場はプロセス別に水蒸気改質、電気分解、その他の技術に分類されます。このうち、水蒸気改質は圧倒的な地位を占めており、2034年までに2,240億米ドル以上を生み出すと予測されています。このプロセスは、天然ガスのような炭化水素原料を効率的かつ大規模に水素に変換できるため、広く支持されています。高収率の水素生成に対する産業界の嗜好は、水蒸気改質用の確立されたインフラストラクチャーが利用可能であることと相まって、このセグメントの魅力を強化し続けています。加えて、水蒸気改質装置は、精製などの産業における既存のエネルギー・システムとの適合性が高いため、広く採用され、予測期間を通じて持続的な需要が確保されます。

用途別では、市場セグメンテーションは石油精製、化学処理、金属、その他の産業領域に区分されます。2024年には石油精製所が36%のシェアで市場をリードし、2034年までのCAGRは6.3%を超えると予測されています。この成長の原動力は、水素化分解や脱硫などの作業をサポートするために、信頼性が高くコスト効率の高い水素供給が必要とされていることです。製油所では、物流コストを削減し、エネルギーの信頼性を高めるため、オンサイト水素ソリューションへの関心が高まっています。燃料の自家発電への移行は、排出削減目標に沿いながら、供給の途絶に関連するリスクを軽減するのに役立ちます。自家発電は、費用と規制遵守を管理しながら生産継続性を維持することを目指す製油所にとって、戦略的優位性を提供します。

地域別では、米国が世界市場への強力な貢献国として浮上しており、その評価額は2022年に90億米ドル、2023年に92億米ドル、2024年に95億米ドルとなります。北米は2024年の世界市場シェアの約9%を占めており、クリーンエネルギーの採用が加速するにつれてこの割合は増加すると予想されます。米国市場は、エネルギー・コストの削減と業務効率の向上を求める複数の部門にわたる需要増加の恩恵を受けています。これを受けて国内企業は、様々な最終用途向けにオンデマンドで水素を製造できる高度なシステムを開発しています。発電機の設計における革新は、よりコンパクトで拡張可能なソリューションを可能にし、商業および産業環境への幅広い展開を促しています。同時に、水素製造・貯蔵インフラへの設備投資の拡大が、この地域における長期的な産業成長の道を開いています。

キャプティブ水素生成分野の主要企業は、持続可能性、効率性、進化する産業要件への適応性に重点を置いています。これらの企業は、革新的な技術を開発し、世界な足跡を強化するために資源を投入しています。これらの企業は、先進的なシステムの立ち上げ、新興地域への進出、クリーンな水素ソリューションの展開加速を目指したパートナーシップの形成など、新たなビジネスチャンスを積極的に追求しています。オンサイト発電の需要が高まることが予想される中、業界のリーダーたちは、将来の市場開拓から利益を得るための戦略的立場にあります。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- 業界エコシステム

- トランプ政権の関税分析

- 貿易への影響

- 貿易量の混乱

- 報復措置

- 業界への影響

- 供給側の影響(原材料)

- 主要原材料の価格変動

- サプライチェーンの再構築

- 生産コストへの影響

- 需要側の影響(販売価格)

- 最終市場への価格伝達

- 市場シェアの動向

- 消費者の反応パターン

- 供給側の影響(原材料)

- 影響を受ける主要企業

- 戦略的な業界対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 政策関与

- 展望と今後の検討事項

- 貿易への影響

- 規制情勢

- 業界への影響要因

- 促進要因

- 業界の潜在的リスク&課題

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア

- 戦略的ダッシュボード

- 戦略的取り組み

- 競合ベンチマーキング

- イノベーションと持続可能性の情勢

第5章 市場規模・予測:工程別、2021年~2034年

- 主要動向

- 蒸気改質器

- 電解

- その他

第6章 市場規模・予測:用途別、2021年~2034年

- 主要動向

- 石油精製所

- 化学薬品

- 金属

- その他

第7章 市場規模・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- イタリア

- オランダ

- ロシア

- アジア太平洋地域

- 中国

- インド

- 日本

- 中東・アフリカ

- サウジアラビア

- イラン

- アラブ首長国連邦

- 南アフリカ

- ラテンアメリカ

- ブラジル

- アルゼンチン

- チリ

第8章 企業プロファイル

- Air Products and Chemicals

- Cummins

- Enapter

- Hitachi Zosen Corporation

- HoSt Group

- Linde

- McPhy Energy

- Messer Group

- NEL Hydrogen

- NEXT Hydrogen

- Siemens Energy

- Teledyne Energy Systems

The Global Captive Hydrogen Generation Market was valued at USD 138.4 billion in 2024 and is estimated to grow at a CAGR of 6.6% to reach USD 259.9 billion by 2034. The transition toward sustainable energy practices and the increasing push for decarbonization are encouraging industries to adopt on-site hydrogen production solutions. This trend is especially prominent across key sectors like refining, chemicals, and transportation, where the demand for cleaner, more efficient fuel alternatives is gaining traction. As global industries aim to reduce greenhouse gas emissions, the role of captive hydrogen systems has become more pivotal. Advancements in clean hydrogen production technology are contributing to this momentum by enhancing scalability, lowering operational costs, and boosting overall system efficiency, making on-site generation an increasingly attractive option for industrial users.

With demand for hydrogen steadily rising, particularly for use in processes that require high-purity fuel, the market is expected to benefit from significant investments in compact and modular systems. These systems offer installation flexibility and can be tailored to varying production capacities, which is particularly appealing for medium-sized facilities seeking to reduce reliance on external hydrogen suppliers. In addition to technological evolution, supportive government policies are amplifying growth. Incentives like tax breaks, grants, and carbon pricing mechanisms are helping industrial players transition toward cleaner fuel solutions by offsetting upfront capital costs. Captive hydrogen generation is also playing a strategic role in broader net-zero emissions agendas, where reliable and localized fuel production aligns with long-term energy goals. Collectively, these factors are laying the groundwork for robust growth across global markets.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $138.4 Billion |

| Forecast Value | $259.9 Billion |

| CAGR | 6.6% |

The market is categorized by process into steam reforming, electrolysis, and other technologies. Among these, steam reformers hold a dominant position and are anticipated to generate over USD 224 billion by 2034. This process is widely favored due to its ability to convert hydrocarbon feedstocks such as natural gas into hydrogen efficiently and at scale. The ongoing industrial preference for high-yield hydrogen generation, combined with the availability of established infrastructure for steam reforming, continues to strengthen the segment's appeal. Additionally, the compatibility of steam reformers with existing energy systems in industries like refining further contributes to its widespread adoption, ensuring sustained demand throughout the forecast period.

In terms of application, the captive hydrogen generation market is segmented into petroleum refineries, chemical processing, metals, and other industrial domains. Petroleum refineries led the market in 2024 with a 36% share and are forecast to grow at a CAGR exceeding 6.3% through 2034. This growth is driven by the need for a dependable and cost-efficient hydrogen supply to support operations like hydrocracking and desulfurization. Refineries are increasingly turning to on-site hydrogen solutions to cut logistics costs and enhance energy reliability. The transition toward in-house fuel generation helps mitigate risks associated with supply disruptions while aligning with emissions reduction targets. Captive generation offers a strategic edge for refiners aiming to maintain production continuity while managing expenses and regulatory compliance.

Regionally, the United States is emerging as a strong contributor to the global market, with valuations of USD 9 billion in 2022, USD 9.2 billion in 2023, and USD 9.5 billion in 2024. North America accounted for approximately 9% of the global market share in 2024, and this proportion is expected to increase as clean energy adoption accelerates. The U.S. market is benefiting from increased demand across multiple sectors seeking to reduce energy costs and improve operational efficiency. In response, domestic firms are developing advanced systems capable of producing hydrogen on demand for various end-use applications. Innovations in generator design are enabling more compact and scalable solutions, encouraging broader deployment in commercial and industrial settings. At the same time, growing capital investment in hydrogen production and storage infrastructure is paving the way for long-term industry growth in the region.

Leading companies in the captive hydrogen generation space are focused on sustainability, efficiency, and adaptability to meet evolving industrial requirements. These firms are dedicating resources to develop innovative technologies and strengthen their global footprint. They are actively pursuing new business opportunities by launching advanced systems, expanding into emerging regions, and forming partnerships aimed at accelerating the deployment of clean hydrogen solutions. With demand for on-site generation expected to rise, industry leaders are strategically positioned to benefit from future market developments.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.2 Base estimates & calculations

- 1.3 Forecast model

- 1.4 Primary research & validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 – 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem

- 3.2 Trump administration tariff analysis

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.2.1.1 Price volatility in key materials

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.2 Demand-side impact (selling price)

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.3 Key companies impacted

- 3.2.4 Strategic industry responses

- 3.2.4.1 Supply chain reconfiguration

- 3.2.4.2 Pricing and product strategies

- 3.2.4.3 Policy engagement

- 3.2.5 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Regulatory landscape

- 3.4 Industry impact forces

- 3.4.1 Growth drivers

- 3.4.2 Industry pitfalls & challenges

- 3.5 Growth potential analysis

- 3.6 Porter's analysis

- 3.6.1 Bargaining power of suppliers

- 3.6.2 Bargaining power of buyers

- 3.6.3 Threat of new entrants

- 3.6.4 Threat of substitutes

- 3.7 PESTEL analysis

Chapter 4 Competitive landscape, 2024

- 4.1 Introduction

- 4.2 Company market share

- 4.3 Strategic dashboard

- 4.4 Strategic initiative

- 4.5 Competitive benchmarking

- 4.6 Innovation & sustainability landscape

Chapter 5 Market Size and Forecast, By Process, 2021 – 2034 (USD Billion)

- 5.1 Key trends

- 5.2 Steam reformer

- 5.3 Electrolysis

- 5.4 Others

Chapter 6 Market Size and Forecast, By Application, 2021 – 2034 (USD Billion)

- 6.1 Key trends

- 6.2 Petroleum refinery

- 6.3 Chemical

- 6.4 Metal

- 6.5 Others

Chapter 7 Market Size and Forecast, By Region, 2021 – 2034 (USD Billion)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.2.3 Mexico

- 7.3 Europe

- 7.3.1 Germany

- 7.3.2 Italy

- 7.3.3 Netherlands

- 7.3.4 Russia

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 India

- 7.4.3 Japan

- 7.5 Middle East & Africa

- 7.5.1 Saudi Arabia

- 7.5.2 Iran

- 7.5.3 UAE

- 7.5.4 South Africa

- 7.6 Latin America

- 7.6.1 Brazil

- 7.6.2 Argentina

- 7.6.3 Chile

Chapter 8 Company Profiles

- 8.1 Air Products and Chemicals

- 8.2 Cummins

- 8.3 Enapter

- 8.4 Hitachi Zosen Corporation

- 8.5 HoSt Group

- 8.6 Linde

- 8.7 McPhy Energy

- 8.8 Messer Group

- 8.9 NEL Hydrogen

- 8.10 NEXT Hydrogen

- 8.11 Siemens Energy

- 8.12 Teledyne Energy Systems