|

市場調査レポート

商品コード

1755280

住宅ローン貸し手の市場機会、成長促進要因、産業動向分析、2025~2034年予測Mortgage Lender Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 住宅ローン貸し手の市場機会、成長促進要因、産業動向分析、2025~2034年予測 |

|

出版日: 2025年05月23日

発行: Global Market Insights Inc.

ページ情報: 英文 180 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

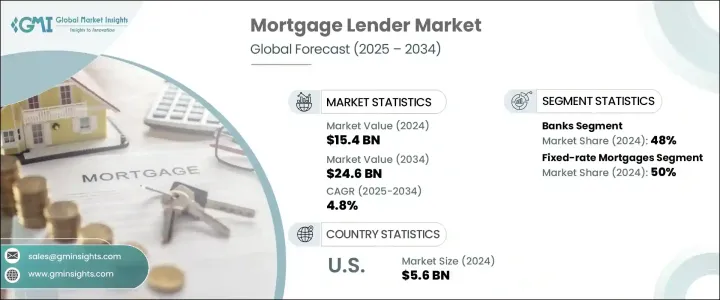

住宅ローン貸し手の世界市場規模は、2024年に154億米ドルとなり、CAGR 4.8%で成長し、2034年には246億米ドルに達すると推定されます。

成長の原動力は、都市部への移住による住宅需要の増加、低金利環境、新興市場における金融サービスへのアクセスの拡大です。デジタルモーゲージソリューションやAIベースの引受ツールの導入が進み、融資プロセスが合理化され、利用者の満足度が向上しています。また、先進技術は運用コストを削減し、透明性を高めています。自動化とデジタル化により、貸出業者の状況は一変し、より迅速な申し込み処理とリアルタイムのローン状況更新が可能になり、借り手の信頼が向上し、すべての貸出プラットフォームで拡張性が高まっています。

環境に配慮した持続可能な融資への注目の高まりは、住宅ローン貸し手市場の拡大を後押ししています。環境意識の高い借り手が持続可能性の目標に沿った金融商品を求める中、エネルギー効率の高い住宅をより良い条件で提供するグリーンモーゲージが人気を集めています。こうした融資商品は、金利の引き下げや税金の軽減など、政府の支援による優遇措置によってさらに後押しされています。気候変動やESGへの配慮が最前線に躍り出る中、持続可能な住宅ローン商品への需要は高まり続けており、金融機関は環境優先事項に沿った独自の引受基準を策定する必要に迫られています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 154億米ドル |

| 予測金額 | 246億米ドル |

| CAGR | 4.8% |

2024年時点では、伝統的な銀行セグメントが48%のシェアを占め、2034年までCAGR 3%で成長すると予測されます。これは、強力なブランド信用力、大規模なインフラ、低コストの預金へのアクセスに起因します。広範な支店網とデジタルツールを持つ銀行は、普通預金口座、保険、投資などの金融商品のクロスセルを含む、全面的な住宅ローンサービスを借り手に提供します。これにより、銀行は永続的な顧客関係を構築し、長期的なロイヤルティを育むことができます。安価な資本と有利な規制へのアクセスにより、銀行は競争力のある金利を維持することができ、特に信用力のある顧客の間で優位に立つことができます。

固定金利住宅ローンは、その予測可能な返済構造により、借り手に長期にわたる経済的安定を提供するため、2024年には50%のシェアを獲得しました。毎月の支払額が変わらない固定金利住宅ローンなら、住宅所有者は金利変動リスクを回避できます。このような予測可能性は、予算に敏感な消費者や初めての購入者にアピールします。低金利の間は、借り手は15年から30年にわたり有利な条件を固定できるため、長期的な借入コストを最小限に抑えることができます。世界経済が不透明な中、この安定性はますます魅力的です。

北米の住宅ローン貸し手市場は84%のシェアを占め、2024年には56億米ドルを創出しました。金利上昇の逆風にもかかわらず、米国の住宅ローン市場は底堅さを維持しています。貸し手は、より信用度の高い借り手に焦点を移し、進化する嗜好に合わせてローンの提供を調整しています。借り換え需要が落ち込む中、金融機関はリスクエクスポージャーを減らすために与信条件を引き締めています。同時に、デジタルトランスフォーメーションへの注目も高まっており、金融機関は自動化ツール、AIベースの信用評価、パーソナライズされた融資プラットフォームなどに投資し、より良い借り手体験を提供し、業務効率を向上させています。

住宅ローン貸し手業界の主要企業には、Rocket Mortgage, JPMorgan Chase, CrossCountry Mortgage, U.S. Bank, Rate, Bank of America, DHI Mortgage, Fairway Independent Mortgage, Veterans United Home Loans, and United Wholesale Mortgage (UWM).などがあります。これらの企業は、デジタルプラットフォームへの戦略的投資を進め、モバイル融資機能を拡大し、AI主導の査定システムを強化しています。また、フィンテック企業と提携し、より柔軟でパーソナライズされたローン商品を導入しています。市場のリーダーは、人との対話とデジタルの利便性を組み合わせたハイブリッド融資モデルの提供に注力する一方、環境意識の高い借り手を引き付け、規制の期待に応えるため、ESGに沿った融資の提供も模索しています。

目次

第1章 調査手法

- 市場の範囲と定義

- 調査デザイン

- 調査アプローチ

- データ収集方法

- データマイニングソース

- 世界

- 地域/国

- 基本推定と計算

- 基準年計算

- 市場予測の主な動向

- 1次調査と検証

- 一次情報

- 予測モデル

- 調査の前提と限界

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 利益率

- コスト構造

- 各段階での付加価値

- バリューチェーンに影響を与える要因

- ディスラプション

- 業界への影響要因

- 促進要因

- デジタル変革と自動化の急増

- 住宅所有需要の増加

- グリーン住宅ローンの導入拡大

- 政府のインセンティブと支援の増加

- 変動金利住宅ローンの人気の高まり

- 業界の潜在的リスク&課題

- 住宅ローンの金利上昇

- 規制圧力とコンプライアンスの課題

- 市場機会

- 未開拓市場への進出

- 住宅ローンの借り換え需要の増加

- 促進要因

- 成長可能性分析

- 規制情勢

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ

- ポーター分析

- PESTEL分析

- テクノロジーとイノベーションの情勢

- 現在の技術動向

- 新興技術

- 特許分析

- 持続可能性と環境側面

- 持続可能な実践

- 廃棄物削減戦略

- 生産におけるエネルギー効率

- 環境に優しい取り組み

- カーボンフットプリントの考慮

- ユースケース

- 最良のシナリオ

- 住宅ローン統計, 2021-2025

- 住宅ローン金利の推移

- 住宅ローン未払い額

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ航空

- 中東・アフリカ

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 戦略的展望マトリックス

- 主な発展

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

- 拡張計画と資金調達

第5章 市場推計・予測:貸し手別、2021年~2034年

- 主要動向

- 銀行

- 信用組合

- 住宅ローンブローカー

- 非銀行系住宅ローン貸付業者

- 政府機関

第6章 市場推計・予測:ローン別、 2021年~2034年

- 主要動向

- 固定金利住宅ローン

- 変動金利住宅ローン(ARM)

- ジャンボローン

- FHAローン

- VAローン

- 利息のみのローン

第7章 市場推計・予測:最終用途別、2021年~2034年

- 主要動向

- 初めて住宅を購入する人

- 住宅を繰り返し購入する人

- 不動産投資家

- 商業用不動産購入者

第8章 市場推計・予測:流通チャネル別、2021年~2034年

- 主要動向

- 直接融資

- ブローカー仲介融資

- オンラインプラットフォーム

第9章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- 北欧諸国

- アジア太平洋地域

- 中国

- インド

- 日本

- 韓国

- オーストラリア・ニュージーランド

- シンガポール

- マレーシア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- アラブ首長国連邦

- サウジアラビア

- 南アフリカ

第10章 企業プロファイル

- AmeriHome Mortgage

- Bank of America

- Citibank

- CrossCountry Mortgage

- DHI Mortgage

- Fairway Independent Mortgage

- Guaranteed Rate

- Guild Mortgage

- JPMorgan Chase

- LoanDepot

- Navy Federal Credit Union

- Newrez

- Pennymac

- Planet Home Lending

- PNC Bank

- Rate

- Rocket Mortgage

- U.S. Bank

- United Wholesale Mortgage(UWM)

- Veterans United Home Loans

The Global Mortgage Lender Market was valued at USD 15.4 billion in 2024 and is estimated to grow at a CAGR of 4.8% to reach USD 24.6 billion by 2034. The growth is fueled by increasing housing demand driven by urban migration, low-interest-rate environments, and greater access to financial services in emerging markets. The rising implementation of digital mortgage solutions and AI-based underwriting tools is streamlining the lending process and improving user satisfaction. Advanced technologies are also reducing operational costs and enhancing transparency. Automation and digitalization are reshaping the lending landscape, enabling lenders to process applications more quickly and provide real-time loan status updates, improving borrower trust and boosting scalability across all lending platforms.

The growing focus on environmentally sustainable financing is helping to expand the mortgage lender market. Green mortgages, which provide better terms for energy-efficient homes, are gaining popularity as eco-conscious borrowers seek financial products aligned with sustainability goals. These lending products are further supported by government-backed incentives such as lower rates and tax relief. As climate and ESG considerations move to the forefront, demand for sustainable mortgage instruments continues to rise, prompting lenders to develop tailored underwriting standards that align with environmental priorities.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $15.4 Billion |

| Forecast Value | $24.6 Billion |

| CAGR | 4.8% |

In 2024, the traditional banks segment accounted for 48% share and is projected to grow at a CAGR of 3% through 2034 attributed to strong brand credibility, large-scale infrastructure, and access to low-cost deposits. With expansive branch networks and digital tools, banks offer borrowers full-spectrum mortgage services that include cross-selling of financial products like savings accounts, insurance, and investments. This allows banks to build enduring customer relationships and foster long-term loyalty. Access to cheap capital and favorable regulations enables them to maintain competitive interest rates, giving them an edge, especially among creditworthy clients.

Fixed-rate mortgages captured a 50% share in 2024 due to their predictable repayment structures, offering borrowers financial stability over time. With a fixed monthly payment that doesn't change, homeowners avoid the risk of rate fluctuations. Such predictability appeals to budget-conscious consumers and first-time buyers. During low interest rates, borrowers take advantage of locking in favorable terms for 15 to 30 years, minimizing the long-term cost of borrowing. This stability is increasingly appealing amid global economic uncertainties.

North America Mortgage Lender Market held an 84% share and generated USD 5.6 billion in 2024. Despite headwinds from higher interest rates, the U.S. mortgage market remains resilient. Lenders are shifting focus toward higher-credit borrowers and tailoring loan offerings to align with evolving preferences. As demand for refinancing dips, institutions are tightening credit conditions to reduce risk exposure. At the same time, the focus on digital transformation has grown stronger, with lenders investing in automation tools, AI-based credit evaluations, and personalized lending platforms to deliver better borrower experience and improve operational efficiency.

Key companies in the Mortgage Lender Industry include Rocket Mortgage, JPMorgan Chase, CrossCountry Mortgage, U.S. Bank, Rate, Bank of America, DHI Mortgage, Fairway Independent Mortgage, Veterans United Home Loans, and United Wholesale Mortgage (UWM). These players are pursuing strategic investments in digital platforms, expanding their mobile lending capabilities, and enhancing AI-driven underwriting systems. They are also forming partnerships with fintech companies to introduce more flexible and personalized loan products. Market leaders are focusing on providing hybrid lending models that combine human interaction with digital convenience, while also exploring ESG-aligned loan offerings to attract eco-conscious borrowers and meet regulatory expectations.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Lender

- 2.2.3 Loan

- 2.2.4 End use

- 2.2.5 Distribution channel

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Surge in digital transformation and automation

- 3.2.1.2 Rise in homeownership demand

- 3.2.1.3 Growing adoption of green mortgages

- 3.2.1.4 Increase in government incentives and support

- 3.2.1.5 Growth in adjustable-rate mortgage popularity

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Higher interest rate on mortgage loans

- 3.2.2.2 Regulatory pressures and compliance challenges

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion into underserved markets

- 3.2.3.2 Rising demand for mortgage refinancing

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Patent analysis

- 3.9 Sustainability and environmental aspects

- 3.9.1 Sustainable Practices

- 3.9.2 Waste reduction strategies

- 3.9.3 Energy efficiency in production

- 3.9.4 Eco-friendly initiatives

- 3.9.5 Carbon footprint considerations

- 3.10 Use cases

- 3.11 Best-case scenario

- 3.12 Mortgage statistics, 2021-2025

- 3.12.1 Historical mortgage interest rates

- 3.12.2 Mortgage debt outstanding

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Lender, 2021 - 2034 (USD Million)

- 5.1 Key trends

- 5.2 Banks

- 5.3 Credit unions

- 5.4 Mortgage brokers

- 5.5 Non-bank mortgage lenders

- 5.6 Government agencies

Chapter 6 Market Estimates & Forecast, By Loan, 2021 - 2034 (USD Million)

- 6.1 Key trends

- 6.2 Fixed-rate mortgages

- 6.3 Adjustable-rate mortgages (ARMs)

- 6.4 Jumbo loans

- 6.5 FHA loans

- 6.6 VA loans

- 6.7 Interest-only loans

Chapter 7 Market Estimates & Forecast, By End Use, 2021 - 2034 (USD Million)

- 7.1 Key trends

- 7.2 First-time homebuyers

- 7.3 Repeat homebuyers

- 7.4 Real estate investors

- 7.5 Commercial property buyers

Chapter 8 Market Estimates & Forecast, By Distribution channel, 2021 - 2034 (USD Million)

- 8.1 Key trends

- 8.2 Direct lending

- 8.3 Broker-mediated lending

- 8.4 Online platforms

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 (USD Million)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Russia

- 9.3.7 Nordics

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 ANZ

- 9.4.6 Singapore

- 9.4.7 Malaysia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 UAE

- 9.6.2 Saudi Arabia

- 9.6.3 South Africa

Chapter 10 Company Profiles

- 10.1 AmeriHome Mortgage

- 10.2 Bank of America

- 10.3 Citibank

- 10.4 CrossCountry Mortgage

- 10.5 DHI Mortgage

- 10.6 Fairway Independent Mortgage

- 10.7 Guaranteed Rate

- 10.8 Guild Mortgage

- 10.9 JPMorgan Chase

- 10.10 LoanDepot

- 10.11 Navy Federal Credit Union

- 10.12 Newrez

- 10.13 Pennymac

- 10.14 Planet Home Lending

- 10.15 PNC Bank

- 10.16 Rate

- 10.17 Rocket Mortgage

- 10.18 U.S. Bank

- 10.19 United Wholesale Mortgage (UWM)

- 10.20 Veterans United Home Loans