|

市場調査レポート

商品コード

1683804

欧州のモーゲージ/ローンブローカー:市場シェア分析、産業動向、成長予測(2025年~2030年)Europe Mortgage / Loan Broker - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 欧州のモーゲージ/ローンブローカー:市場シェア分析、産業動向、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 160 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

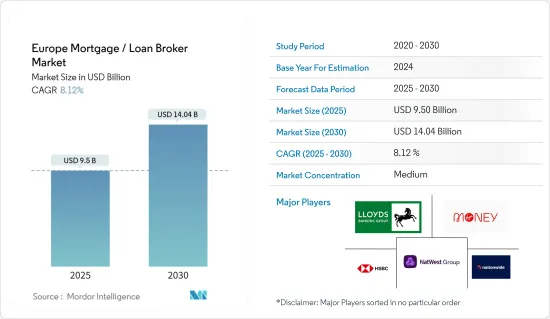

欧州のモーゲージ/ローンブローカー市場規模は2025年に95億米ドルと推定・予測され、予測期間中(2025年~2030年)のCAGRは8.12%で、2030年には140億4,000万米ドルに達すると予測されます。

欧州のローンブローカー市場は近年急成長しています。この背景には、金融に対する意識の高まり、多様な借入要件、利用可能なローン商品の多様化など、いくつかの要因があります。欧州のローン・ブローカー市場の成長は、専門家による財務アドバイスの必要性、ローン検索手続きのアウトソーシング、魅力的なローン条件への需要など、いくつかの理由に起因しています。規制遵守、市場競争、刻々と変化するデジタル環境も、欧州ローンブローカー市場の成長に寄与している要因です。

ローンブローカーは、個人ローンから住宅ローン、自動車ローン、中小企業向けローンまで、消費者のニーズに応えるためにサービスを多様化しています。欧州のローンブローカー市場は、消費者の安全性、透明性、融資の公平性を向上させようとする規制改正の影響を受けています。信頼と信用を維持するために、ブローカーは刻々と変化する規制に準拠し続けなければならないです。

実際、世界最大市場の多くでは、住宅ローン仲介業者が住宅ローン組成の驚くほど多くを担っています。例えば、オランダのブローカーは住宅ローン組成の約60%を占め、オーストラリアのブローカーは約70%を占めています。英国ではさらに高く、75%を占めています。(もうひとつの仲介業者であるオンライン・アグリゲーターも、顧客に透明性と競合サポートを提供することで、ローン組成プロセスにおける重要性を増している)。

欧州ローンブローカー市場動向

住宅市場の拡大がモーゲージブローカーの需要を押し上げる

欧州の住宅ローン/ローンブローカー市場において、住宅ローン分野は実に大きな市場です。欧州の住宅ローン市場は多様性に富んでおり、国ごとにさまざまなタイプのローンやレンダーが存在します。金利、融資条件、審査基準などの要素も大きく異なります。金利、雇用水準、住宅市場の動向などの経済状況は、住宅ローン市場に大きな影響を与えます。これらの要因の変化は、借り手の需要と貸し手の収益性に影響を与える可能性があります。

市場を独占する英国

2021年、英国では住宅ローン貸出市場が活況を呈していました。総貸出額は、パンデミック規制が貸出に大きな悪影響を及ぼした2020年に比べて26%増加し、3,085億ポンドとなりました。とはいえ、2019年の2,690億英ポンドを15%上回りました。

住宅ローンの平均金利は、2020年の2.00%から2.11%へと若干上昇したもの、2019年の平均2.25%を下回る水準にとどまりました。パンデミックを受けて、基準金利は2020年3月に0.75%から0.10%に引き下げられました。より多くの金融機関が余分なリスクを織り込んだり、これらの商品を市場から引き上げると、住宅ローン金利はまず上昇し、特にLTVが大きい(75%超)場合に上昇しました。

欧州ローンブローカー業界の概要

ロイズ・バンキング・グループのような支配的なプレーヤーもいるが、市場は半固体化しています。欧州の住宅ローン/ローンブローカー事業における主な競合他社については、本調査で取り上げています。ローンブローカーは、担当する地域の優良な不動産業者や金融業者との関係に依存しているため、激しい競合に直面しています。市場の主要企業には、ロイズ・バンキング・グループ、ナットウエスト・グループ、ネーションワイドBS、HSBC銀行、ヴァージン・マネーなどがあります。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学と洞察

- 市場概要

- 市場促進要因

- 市場抑制要因

- 業界の魅力- ポーターのファイブフォース分析

- 買い手の交渉力

- 供給企業の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

- 市場における技術革新の洞察

- COVID-19の市場への影響

第5章 市場セグメンテーション

- 企業別

- 大規模

- 小規模

- 中規模

- 用途別

- ホームローン

- 商業・産業ローン

- 自動車ローン

- 政府向けローン

- その他の用途

- エンドユーザー別

- 企業

- 個人

- 地域別

- 英国

- ドイツ

- フランス

- その他の欧州

第6章 競合情勢

- 企業プロファイル

- Lloyds Banking Group

- NatWest Group

- Nationwide BS

- HSBC Bank

- Virgin Money

- Santander UK

- Barclays

- Coventry BS

- Yorkshire BS

- TSB Bank*

第7章 市場機会と今後の動向

第8章 免責事項と出版社について

The Europe Mortgage / Loan Broker Market size is estimated at USD 9.50 billion in 2025, and is expected to reach USD 14.04 billion by 2030, at a CAGR of 8.12% during the forecast period (2025-2030).

The European loan broker market has grown rapidly in recent years. This is due to several factors, including increased financial awareness, a variety of borrowing requirements, and a greater variety of loan products available. The growth of the European loan broker market can be attributed to several reasons, such as the need for specialist financial advice, outsourcing of loan search procedures, and the demand for attractive loan terms. Regulatory compliance, competition in the market, and the ever-changing digital environment are also factors that have contributed to the growth of the Europe loan broker market.

Loan brokers are diversifying their services to meet consumer needs, from personal loans to mortgages and auto loans to small business loans. The European loan brokers market is being affected by regulatory changes that seek to improve consumer safety, transparency, and fairness in lending. To maintain trust and trustworthiness, brokers must remain compliant with ever-changing regulations.

In fact, mortgage brokers in many of the world's largest markets are responsible for a surprising amount of home loan origination. For example, brokers in the Netherlands account for about 60% of all home loan originations, while brokers in Australia account for about 70%. In the UK, it's even higher at 75%. (Another type of intermediary, online aggregators, are also becoming increasingly important in the loan origination process by providing customers with transparency and competitive support.)

Europe Loan Broker Market Trends

The Housing Market's Expansion Drives Up Demand for Mortgage Brokers

The home loan segment is indeed a major market in the mortgage/loan broker market in Europe. The market for home loans in Europe is diverse, with various types of loans and lenders available across different countries. Factors such as interest rates, loan terms, and eligibility criteria can vary widely. Economic conditions, such as interest rates, employment levels, and housing market trends, significantly influence the residential mortgage market. Changes in these factors can impact borrower demand and lender profitability.

United Kingdom is Dominating the Market

In 2021, the mortgage lending market was booming in the United Kingdom. Gross lending increased 26% over 2020, when pandemic restrictions had a significant negative impact on lending, to GBP 308.5 billion. Yet it was also 15% more than the GBP 269.0 billion in 2019.

While slightly rising to 2.11% from 2.00% in 2020, the average mortgage interest rate stayed below the average of 2.25% in 2019. In response to the pandemic, the base rate was decreased in March 2020 from 0.75% to 0.10%. When more lenders priced in the extra risk or pulled these products off the market, mortgage interest rates first rose, especially at larger LTVs (over 75%).

Europe Loan Broker Industry Overview

The market is semi-consolidated, with some dominant players like Lloyds Banking Group. The main competitors in the European mortgage/loan broker business are covered in the research. Loan brokers face intense competition since they depend on their relationships with the best real estate agents and lenders in the communities they cover. Some major players in the market are Lloyds Banking Group, NatWest Group, Nationwide BS, HSBC Bank, and Virgin Money.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS AND INSIGHTS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.3 Market Restraints

- 4.4 Industry Attractiveness - Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Buyers

- 4.4.2 Bargaining Power of Suppliers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitutes

- 4.4.5 Intensity of Competitive Rivalry

- 4.5 Insights of Technology Innovations in the Market

- 4.6 Impact of COVID-19 on the Market

5 MARKET SEGMENTATION

- 5.1 By Enterprise

- 5.1.1 Large

- 5.1.2 Small

- 5.1.3 Mid-sized

- 5.2 By Applications

- 5.2.1 Home Loans

- 5.2.2 Commercial and Industrial Loans

- 5.2.3 Vehicle Loans

- 5.2.4 Loans to Governments

- 5.2.5 Other Applications

- 5.3 By End- User

- 5.3.1 Businesses

- 5.3.2 Individuals

- 5.4 By Geography

- 5.4.1 United Kingdom

- 5.4.2 Germany

- 5.4.3 France

- 5.4.4 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Lloyds Banking Group

- 6.1.2 NatWest Group

- 6.1.3 Nationwide BS

- 6.1.4 HSBC Bank

- 6.1.5 Virgin Money

- 6.1.6 Santander UK

- 6.1.7 Barclays

- 6.1.8 Coventry BS

- 6.1.9 Yorkshire BS

- 6.1.10 TSB Bank*