|

市場調査レポート

商品コード

1431565

日本の住宅ローン/ローンブローカー市場:市場シェア分析、産業動向・統計、成長予測(2024年~2029年)Japan Mortgage/Loan Brokers - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 日本の住宅ローン/ローンブローカー市場:市場シェア分析、産業動向・統計、成長予測(2024年~2029年) |

|

出版日: 2024年02月15日

発行: Mordor Intelligence

ページ情報: 英文 150 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

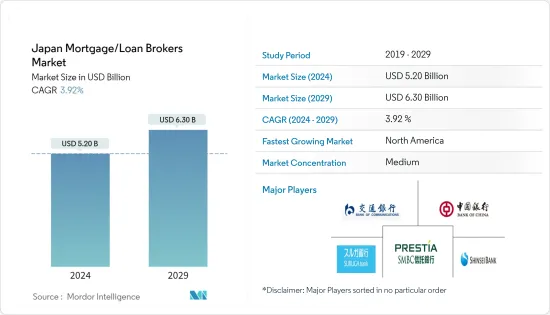

世界の住宅ローン/ローンブローカーの市場規模は、2024年に52億米ドルと推定され、2029年には63億米ドルに達し、予測期間中(2024年~2029年)にCAGR3.92%で成長すると予測されています。

日本では、住宅ローンには固定金利、変動金利、当初固定金利、以後変動金利期間という形態があります。日本の商業用不動産および住宅用不動産の住宅ローン金利は、長年にわたり安定した傾向を示しています。住宅ローン投資家は、これらの住宅ローンを購入する際に重要な役割を果たしており、債務不履行が発生した場合に、債券市場の一般投資家に保険を提供しています。

COVID-19の出現により、日本のGDPは5兆401億1,000万米ドルから4兆9,121億5,000万米ドルへと減少し、国民の一人当たり所得は継続的に減少しました。

日本の地価動向は上昇傾向にあり、住宅価格指数と実質住宅価格指数は毎月上昇を続けています。このことは、一定の金利水準と相まって、日本の国民にとって、安定した金利で既存の不動産から大きな融資額を得ることができる住宅ローンが、より良い選択肢となることを意味します。

日本の住宅ローン市場動向

安定した金利水準と不動産価格の上昇が日本の住宅ローン/ローンブローカー市場に影響を与えています。

日銀の基本金利は長年にわたり0.3%で推移しています。実物投資の増加と資産価格の上昇により、民間債務の累積と資産価格の上昇に伴う活発な投資が行われました。過去10年間の総与信増加のほぼ半分は、住宅・不動産ローンの増加が観察されます。

国内投資家による不動産取得は、外国人投資家による不動産取得が継続的に増加する動向とは別に、過去10年間は外国人投資家による不動産取得が減少する中で増加が観察されました。日本では、関東、中部、近畿などの不動産投資ファンド向けに大手銀行の不動産ローンが増加し続けています。

日本の住宅ローン/ローンブローカー市場に影響を与えるローン業界の借り手タイプ

COVID-19の出現により、不動産業向けローンは増加の一途をたどっており、製造業、卸売業がこれに続いています。住宅ローンは、前年度比約3.5%増と個人に占める割合が大きくなっています。

日本の実質住宅価格指数は継続的な伸びを示しており、住宅ローンの抵当権設定額が増加し、住宅の抵当権設定額の急増に伴い、小規模物件でも十分な融資を受けることができます。借り入れを考慮した場合、不動産は住宅ローン業界のトップに位置しています。

日本の住宅ローン業界の概要

民間金融機関の住宅ローン残高は、昨年1年間で公的金融機関が1兆4,300億米ドル、公的金融機関が1,600億米ドルと、公的金融機関に比べ増加の一途をたどっており、民間金融機関が住宅ローンにおいて有効な役割を果たしています。住宅金融支援機構は、公的住宅ローンの主要な貸し手として機能しています。日本で住宅ローンを提供している主な銀行には、UOB(United Overseas Bank)、Bank of China、オリックス、OCBC(Overseas-Chinese Banking Corporation, Limited)などがあります。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学と洞察

- 市場概要

- 市場促進要因

- 金融住宅ローンソリューションに対する需要の増加

- ローンブローカー・サービスへのアクセスの拡大

- 市場抑制要因

- リスク評価能力の欠如

- 仲介手数料の高さ

- 市場機会

- 市場を拡大するフィンテックの革新的商品

- フィンテックと伝統的銀行のパートナーシップ

- 業界の魅力- ポーターのファイブフォース分析

- 買い手の交渉力

- 供給企業の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

- 市場における技術革新の洞察

- 各種規制状況に関する洞察

- COVID-19の市場への影響

第5章 市場セグメンテーション

- 住宅ローンタイプ別

- 従来型住宅ローン

- ジャンボローン

- 政府保証付住宅ローン

- その他の住宅ローン

- 住宅ローン期間別

- 30年住宅ローン

- 20年住宅ローン

- 15年住宅ローン

- その他の住宅ローン期間

- 金利別

- 固定金利

- 変動金利

- プロバイダー別

- プライマリー住宅ローンレンダー

- セカンダリー住宅ローンレンダー

第6章 競合情勢

- 市場集中度の概要

- 企業プロファイル

- Bank of Japan

- Bank of China

- Suruga bank Ltd.

- SMBC trust bank

- Shinseibank

- United Overseas Bank

- Overseas Chinese Banking Corp

- Sumitomo Mitsui Financial Group

- Mitsubishi UFJ Financial Group

- Mizuho Financial Group*

第7章 市場の今後の動向

第8章 免責事項と出版社について

The Japan Mortgage/Loan Brokers Market size is estimated at USD 5.20 billion in 2024, and is expected to reach USD 6.30 billion by 2029, growing at a CAGR of 3.92% during the forecast period (2024-2029).

In Japan, the mortgage loan is available in the form of a fixed interest rate, Variable interest rate, Initial Fixed interest rate and a variable interest rate period thereafter. The interest rate on mortgage loans for commercial and residential real estate in Japan has observed a steady trend over the years. Mortgage Investors play a significant role in buying these mortgage loans providing insurance to a regular investor in the bond market in case of default.

With the advent of COVID-19 in Japan, its GDP observed a decline from a level of 5040.11 billion USD to 4,912.15 bn USD over the period showing a continuous decline in the per capita income of people and resulting in a constant increase in the value of mortgage debt outstanding in Japan with an increase in the issuance of new housing loans combined with a stable mortgage interest rate.

The growth rate of land prices in Japan has observed an increasing trend, with a continuous increase in the monthly residential property price index and real house price index. This, combined with a constant level of interest rate, will make mortgage loans a better option for the population of Japan to get a large loan value from the existing property at a stable interest rate.

Japan Mortgage/Loan Brokers Market Trends

Consistent level of interest rate and Increasing Real Estate price affecting Japan's Mortgage/Loan Broker Market.

Bank of Japan's Basic loan rate is at 0.3% over the years. An increase in real investment and a rise in asset price resulted in an accumulation of private debt and active investment with an increase in asset price. Almost half of the increase in total credit for the past decade is observed with increased housing and real estate loans.

Real estate property acquisition by domestic investors had observed an increase with a decline in foreign investor acquisition during covid other than a trend of continuous increase in foreign investor acquisition of real estate property. In Japan, real estate loans by major banks have kept rising for real estate investment funds such as Kanto, Chubu, Kinki, etc.

Borrower type in Loan industry affecting Japan Mortgage /Loan Broker Market

Over the years real estate business has been observing a steady loan borrowing; with the advent of COVID-19, loans in the real estate business sector have grown at an increasing rate, followed by manufacturing and wholesale industries. Housing loans account for a large share of an individual with a y/y% change of around 3.5 % during the previous year.

The real house price index in Japan has observed continuous growth, creating an increase in mortgage value for a home loan and a small property sufficient amount of loan can be taken with the surge in mortgage price of the house. When borrowing is considered, real estate is at the top of the mortgage industry.

Japan Mortgage/Loan Brokers Industry Overview

The outstanding amount of housing loans granted by private lending institutions had observed continuous growth as compared to Public financial institutions with an outstanding value of 1.43 trillion USD during last year for public financial institutions and 0.16 trillion USD for public financial institutions, leading to an effective role been played by a private financial institution for mortgage loans. Japan Housing Finance Agency is acting as a leading public housing loan lender. A few of the major banks in Japan offering mortgage loans are UOB (United Overseas Bank), Bank of China, Orix, OCBC (Overseas-Chinese Banking Corporation, Limited) etc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS AND INSIGHTS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increase in demand for Financial Home Loan Solutions

- 4.2.2 Increased Accessibility to Loan Broker Services

- 4.3 Market Restraints

- 4.3.1 Lack of Risk Valuation Capabilities

- 4.3.2 High level of Brokerage Service Charges and Commission

- 4.4 Market Opportunities

- 4.4.1 Fintechs Innovative products expanding the Market

- 4.4.2 Partnership between fintech and traditional Banks

- 4.5 Industry Attractiveness - Porter's Five Forces Analysis

- 4.5.1 Bargaining Power of Buyers

- 4.5.2 Bargaining Power of Suppliers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Intensity of Competitive Rivalry

- 4.6 Insights of Technology Innovations in the Market

- 4.7 Insights on various regulatory landscape

- 4.8 Impact of COVID-19 on the Market

5 MARKET SEGMENTATION

- 5.1 By Type of Mortgage Loan

- 5.1.1 Conventional Mortgage Loan

- 5.1.2 Jumbo Loans

- 5.1.3 Government-insured Mortgage Loans

- 5.1.4 Other Types of Mortgage Loan

- 5.2 By Mortgage Loan terms

- 5.2.1 30- years Mortgage

- 5.2.2 20-year Mortgage

- 5.2.3 15-year Mortgage

- 5.2.4 Other Mortgage Loan Terms

- 5.3 By Interest Rate

- 5.3.1 Fixed-Rate

- 5.3.2 Adjustable-Rate

- 5.4 By Provider

- 5.4.1 Primary Mortgage Lender

- 5.4.2 Secondary Mortgage Lender

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration Overview

- 6.2 Company Profiles

- 6.2.1 Bank of Japan

- 6.2.2 Bank of China

- 6.2.3 Suruga bank Ltd.

- 6.2.4 SMBC trust bank

- 6.2.5 Shinseibank

- 6.2.6 United Overseas Bank

- 6.2.7 Overseas Chinese Banking Corp

- 6.2.8 Sumitomo Mitsui Financial Group

- 6.2.9 Mitsubishi UFJ Financial Group

- 6.2.10 Mizuho Financial Group*