|

市場調査レポート

商品コード

1750510

インテリジェント・プロセス・オートメーションの市場機会と促進要因、業界動向分析、2025年~2034年予測Intelligent Process Automation Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| インテリジェント・プロセス・オートメーションの市場機会と促進要因、業界動向分析、2025年~2034年予測 |

|

出版日: 2025年05月16日

発行: Global Market Insights Inc.

ページ情報: 英文 170 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

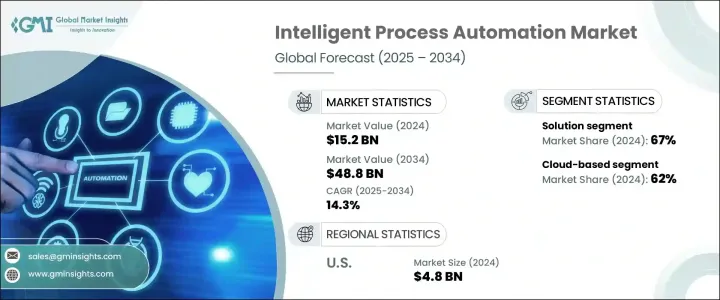

世界のインテリジェント・プロセス・オートメーション(IPA)市場は、2024年に152億米ドルと評価され、CAGR 14.3%で成長し、2034年には488億米ドルに達すると推定されています。

この急成長の主な要因は、業界全体でデジタルトランスフォーメーションの導入が進んでいることと、人工知能や機械学習のような先進技術による業務最適化のニーズが高まっていることです。企業は、業務効率の向上、コスト削減、より良い顧客体験の提供を迫られており、これらすべてがインテリジェントオートメーションへのシフトを加速させています。IPAのソリューションにより、企業は手作業による反復作業を排除し、データ主導の洞察を通じて意思決定を改善できるようになっています。自動化を導入する企業が増えるにつれ、拡張性と適応性に優れたテクノロジーに対する需要は急増し続けています。同市場は、さまざまなコグニティブ技術の融合から恩恵を受けており、企業はワークフローを見直すことで、俊敏性、革新性、パフォーマンスを高めることができます。各分野でIPAツールの導入が増加していることは、自動化がもはやコスト削減メカニズムとしてだけでなく、競争優位性とデジタル・レジリエンスを実現する重要な手段として捉えられるようになったという、より広範な傾向を浮き彫りにしています。

IPAの主要な促進要因の1つは、リアルタイムのデータ処理、パターン認識、継続的学習をサポートする人工知能コンポーネントの統合です。AI機能により、IPAプラットフォームは変化するビジネスニーズに適応し、非構造化データを分析し、予測的な意思決定を行うことができます。組織は透明性を高め、人的ミスを減らし、大量の業務を合理化するために、こうしたツールを活用するようになっています。自動化を推進する動きは、クラウドベースのソリューションやローコード/ノーコード開発プラットフォームの利用可能性の拡大によっても後押しされ、IPAをより身近で多様なビジネス環境に導入しやすくしています。これらの技術革新は、企業がサイロ化を解消し、レガシーシステムや断片化されたデータランドスケープに関連する課題に対処するのに役立っています。その結果、インテリジェント・オートメーションは中核的なビジネス機能にますます組み込まれるようになり、コンプライアンス・モニタリングから顧客エンゲージメントまで、すべてをサポートすると同時に、紙の使用量とエネルギー消費量を削減することで持続可能な取り組みに貢献しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 152億米ドル |

| 予測金額 | 488億米ドル |

| CAGR | 14.3% |

IPA市場は、コンポーネント別にソリューションとサービスに区分されます。ソリューション分野は2024年に約67%の圧倒的シェアを占め、予測期間を通じてCAGR 15%を超える成長が見込まれています。これらのプラットフォームは、高度な機能と導入の容易さのバランスにより、幅広い業界にアピールしています。AI、機械学習、ロボティック・プロセス・オートメーションを組み込むことで、IPAソリューションはバックオフィスとフロントエンドの両方のワークフローを効率的に自動化できます。コンプライアンスを強化し、機能を拡張し、手作業によるプロセスへの依存を減らすことができるため、安定したインテリジェントな自動化システムを求める企業に選ばれています。文書処理から顧客対応管理まで、これらのソリューションはエラーの削減、データ精度の向上、継続的なプロセス改善を可能にします。

導入形態によって、市場はクラウドベースとオンプレミスに分類されます。クラウドベースのIPAは、2024年には62%と大半のシェアを占めており、2025年から2034年にかけて14.9%以上のCAGRで拡大すると予測されています。これらのプラットフォームは、より迅速な実装、より優れた統合機能、リモートアクセシビリティなどの主要な利点を提供し、デジタルトランスフォーメーションが進む企業にとって理想的なものとなっています。一元化されたインフラとSaaSアプリケーションとの互換性により、企業はさまざまな部門や地域にまたがるプロセスをシームレスに自動化できます。中小企業も大企業も、コンプライアンス、オンボーディング、トランザクション処理などの分野で自動化の取り組みを加速させるために、クラウド導入を選択する傾向が強まっています。

テクノロジー別に見ると、市場は機械学習(ML)、自然言語処理(NLP)、ロボティック・プロセス・オートメーション(RPA)、コンピューター・ビジョン、バーチャル・エージェント、その他に区分されます。機械学習は、自動化プラットフォームの適応性とインテリジェンスを強化するという変革的な役割を果たすため、このセグメントをリードしています。MLは、システムがデータから学習し、動向を検出し、手動プログラミングなしで意思決定を行うことを可能にします。機械学習は、予測的洞察や、複雑なデータセットや非構造化データセットの管理能力を必要とするアプリケーションに広く利用されています。機械学習への依存の高まりは、IPAを静的なルールベースのシステムから、戦略的なビジネス目標をサポートする動的な学習対応ソリューションへと進化させる上で、その重要性を強調しています。

地域別では、米国が2024年の北米市場を席巻し、地域別収益の約84.4%を占め、48億米ドル近い収益を上げました。同国は、デジタル革新におけるリーダーシップと、AIを搭載したテクノロジーの強力な企業導入により、インテリジェント・オートメーションの最前線に位置し続けています。米国市場は、成熟したITインフラ、自動化技術への多額の投資、大手ソフトウェアベンダーの集積という利点があります。各業界でデジタルトランスフォーメーションが最重要課題となっていることから、俊敏でインテリジェント、かつ拡張性の高い自動化プラットフォームに対する需要は、予測期間を通じて堅調に推移すると予想されます。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- テクノロジープロバイダー

- システムインテグレーター

- クラウドおよびインフラストラクチャプロバイダー

- 最終用途

- トランプ政権による関税への影響

- 貿易への影響

- 貿易量の混乱

- 報復措置

- 業界への影響

- 供給側の影響(原材料)

- 主要原材料の価格変動

- サプライチェーンの再構築

- 生産コストへの影響

- 需要側の影響(顧客へのコスト)

- 最終市場への価格伝達

- 市場シェアの動向

- 消費者の反応パターン

- 供給側の影響(原材料)

- 影響を受ける主要企業

- 戦略的な業界対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 政策関与

- 展望と今後の検討事項

- 貿易への影響

- 利益率分析

- テクノロジーとイノベーションの情勢

- 特許分析

- ユースケース

- 主なニュースと取り組み

- 規制情勢

- 影響要因

- 促進要因

- 急速なデジタル変革

- ビジネスプロセスにおけるAIと機械学習の統合

- ロボティック・プロセス・オートメーション(RPA)の導入拡大

- クラウドの導入とSaaSの拡張

- 業界の潜在的リスク&課題

- 高い導入コスト

- データのプライバシーとセキュリティに関する懸念

- 促進要因

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 競合ポジショニングマトリックス

- 戦略的展望マトリックス

第5章 市場推計・予測:コンポーネント別、2021-2034

- 主要動向

- ソリューション

- サービス

- 専門サービス

- マネージドサービス

第6章 市場推計・予測:導入モデル別、2021-2034

- 主要動向

- クラウドベース

- オンプレミス

第7章 市場推計・予測:技術別、2021-2034

- 主要動向

- 機械学習(ML)

- 自然言語処理(NLP)

- ロボティック・プロセス・オートメーション(RPA)

- コンピュータービジョン

- 仮想エージェント

- その他

第8章 市場推計・予測:組織規模別、2021-2034

- 主要動向

- 大企業

- 中小企業

第9章 市場推計・予測:用途別、2021-2034

- 主要動向

- ビジネスプロセスの自動化

- IT運用

- アプリケーション管理

- コンテンツ管理

- セキュリティ管理

- その他

第10章 市場推計・予測:最終用途別、2021-2034

- 主要動向

- BFSI

- ヘルスケア

- 小売り

- ITおよび通信

- コミュニケーションとメディアと教育

- 製造業

- 物流、エネルギー、公益事業

- その他

第11章 市場推計・予測:地域別、2021-2034

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- 北欧諸国

- アジア太平洋地域

- 中国

- インド

- 日本

- 韓国

- オーストラリア・ニュージーランド

- 東南アジア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- アラブ首長国連邦

- サウジアラビア

- 南アフリカ

第12章 企業プロファイル

- AntWorks

- Appian

- Automation Anywhere

- Blue Prism

- Cognizant Technology Solutions

- HCLTech

- HelpSystems

- IBM

- Infosys

- Kofax

- Microsoft

- NICE

- Oracle Corporation

- Pegasystems

- Salesforce

- SAP SE

- Tata Consultancy Services(TCS)

- UiPath

- Wipro

- WorkFusion

The Global Intelligent Process Automation (IPA) Market was valued at USD 15.2 billion in 2024 and is estimated to grow at a CAGR of 14.3% to reach USD 48.8 billion by 2034. This rapid growth is largely fueled by the increasing adoption of digital transformation across industries and the rising need for advanced technologies like artificial intelligence and machine learning to optimize business operations. Companies are under pressure to enhance operational efficiency, cut costs, and deliver better customer experiences-all of which are accelerating the shift toward intelligent automation. IPA solutions are enabling organizations to eliminate manual, repetitive tasks and improve decision-making through data-driven insights. As more businesses embrace automation, the demand for scalable and adaptive technologies continues to surge. The market is benefiting from the convergence of various cognitive technologies, allowing businesses to rethink their workflows for greater agility, innovation, and performance. Increasing deployment of IPA tools across sectors highlights a broader trend where automation is no longer viewed solely as a cost-cutting mechanism but as a key enabler of competitive advantage and digital resilience.

One of the major growth drivers for IPA is the integration of artificial intelligence components that support real-time data processing, pattern recognition, and continuous learning. With AI capabilities, IPA platforms can adapt to changing business needs, analyze unstructured data, and make predictive decisions. Organizations are turning to these tools to increase transparency, reduce human error, and streamline high-volume operations. The push toward automation is also being bolstered by the growing availability of cloud-based solutions and low-code/no-code development platforms, making IPA more accessible and easier to implement across diverse business environments. These innovations are helping companies break down silos and address challenges associated with legacy systems and fragmented data landscapes. As a result, intelligent automation is becoming increasingly embedded in core business functions, supporting everything from compliance monitoring to customer engagement, all while contributing to sustainability efforts by reducing paper usage and energy consumption.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $15.2 Billion |

| Forecast Value | $48.8 Billion |

| CAGR | 14.3% |

In terms of components, the IPA market is segmented into solutions and services. The solutions segment held a dominant share of approximately 67% in 2024 and is anticipated to grow at a CAGR exceeding 15% throughout the forecast period. These platforms appeal to a wide range of industries due to their balance of advanced features and ease of deployment. By incorporating AI, machine learning, and robotic process automation, IPA solutions can automate both back-office and front-end workflows efficiently. Their ability to enhance compliance, scale across functions, and reduce dependency on manual processes makes them a preferred choice for enterprises seeking stable, intelligent automation systems. From document processing to customer interaction management, these solutions enable error reduction, improve data accuracy, and support continuous process improvement.

Based on deployment, the market is categorized into cloud-based and on-premises models. Cloud-based IPA held the majority share of 62% in 2024 and is projected to expand at a CAGR of over 14.9% from 2025 to 2034. These platforms offer key advantages such as faster implementation, better integration capabilities, and remote accessibility, making them ideal for businesses undergoing digital transformation. Their centralized infrastructure and compatibility with SaaS applications allow companies to automate processes seamlessly across different departments and geographies. Both small and large organizations are increasingly opting for cloud deployment to speed up automation efforts in areas like compliance, onboarding, and transactional processing.

By technology, the market is segmented into machine learning (ML), natural language processing (NLP), robotic process automation (RPA), computer vision, virtual agents, and others. Machine learning leads the segment due to its transformative role in enhancing the adaptability and intelligence of automation platforms. ML allows systems to learn from data, detect trends, and make decisions without manual programming. It is widely used for applications that require predictive insights and the ability to manage complex or unstructured datasets. The growing reliance on machine learning underscores its importance in driving the evolution of IPA from static rule-based systems to dynamic, learning-enabled solutions that support strategic business goals.

Regionally, the United States dominated the North American market in 2024, capturing around 84.4% of the regional revenue and generating close to USD 4.8 billion. The country's leadership in digital innovation, combined with strong enterprise adoption of AI-powered technologies, continues to position it at the forefront of intelligent automation. The U.S. market benefits from a mature IT infrastructure, substantial investment in automation technologies, and a high concentration of major software vendors. With digital transformation being a top priority across industries, the demand for agile, intelligent, and scalable automation platforms is expected to remain strong throughout the forecast period.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates and calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimates

- 1.3 Forecast model

- 1.4 Primary research & validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Supplier landscape

- 3.2.1 Technology providers

- 3.2.2 System integrators

- 3.2.3 Cloud and infrastructure providers

- 3.2.4 End use

- 3.3 Impact of Trump administration tariffs

- 3.3.1 Trade impact

- 3.3.1.1 Trade volume disruptions

- 3.3.1.2 Retaliatory measures

- 3.3.2 Impact on industry

- 3.3.2.1 Supply-side impact (raw materials)

- 3.3.2.1.1 Price volatility in key materials

- 3.3.2.1.2 Supply chain restructuring

- 3.3.2.1.3 Production cost implications

- 3.3.2.2 Demand-side impact (Cost to customers)

- 3.3.2.2.1 Price transmission to end markets

- 3.3.2.2.2 Market share dynamics

- 3.3.2.2.3 Consumer response patterns

- 3.3.2.1 Supply-side impact (raw materials)

- 3.3.3 Key companies impacted

- 3.3.4 Strategic industry responses

- 3.3.4.1 Supply chain reconfiguration

- 3.3.4.2 Pricing and product strategies

- 3.3.4.3 Policy engagement

- 3.3.5 Outlook & future considerations

- 3.3.1 Trade impact

- 3.4 Profit margin analysis

- 3.5 Technology & innovation landscape

- 3.6 Patent analysis

- 3.7 Use cases

- 3.8 Key news & initiatives

- 3.9 Regulatory landscape

- 3.10 Impact forces

- 3.10.1 Growth drivers

- 3.10.1.1 Rapid digital transformation

- 3.10.1.2 Integration of AI and machine learning in business processes

- 3.10.1.3 Growing adoption of Robotic Process Automation (RPA)

- 3.10.1.4 Cloud adoption and SaaS expansion

- 3.10.2 Industry pitfalls & challenges

- 3.10.2.1 High implementation costs

- 3.10.2.2 Data privacy and security concerns

- 3.10.1 Growth drivers

- 3.11 Growth potential analysis

- 3.12 Porter's analysis

- 3.13 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Component, 2021 - 2034 ($Mn)

- 5.1 Key trends

- 5.2 Solution

- 5.3 Services

- 5.3.1 Professional services

- 5.3.2 Managed services

Chapter 6 Market Estimates & Forecast, By Deployment Model, 2021 - 2034 ($Mn)

- 6.1 Key trends

- 6.2 Cloud-based

- 6.3 On-premises

Chapter 7 Market Estimates & Forecast, By Technology, 2021 - 2034 ($Mn)

- 7.1 Key trends

- 7.2 Machine Learning (ML)

- 7.3 Natural Language Processing (NLP)

- 7.4 Robotic Process Automation (RPA)

- 7.5 Computer vision

- 7.6 Virtual agents

- 7.7 Others

Chapter 8 Market Estimates & Forecast, By Organization Size, 2021 - 2034 ($Mn)

- 8.1 Key trends

- 8.2 Large enterprise

- 8.3 SME

Chapter 9 Market Estimates & Forecast, By Application, 2021 - 2034 ($Mn)

- 9.1 Key trends

- 9.2 Business process automation

- 9.3 IT operations

- 9.4 Application management

- 9.5 Content management

- 9.6 Security management

- 9.7 Others

Chapter 10 Market Estimates & Forecast, By End Use, 2021 - 2034 ($Mn)

- 10.1 Key trends

- 10.2 BFSI

- 10.3 Healthcare

- 10.4 Retail

- 10.5 IT & telecom

- 10.6 Communication and media & education

- 10.7 Manufacturing

- 10.8 Logistics, energy & utilities

- 10.9 Others

Chapter 11 Market Estimates & Forecast, By Region, 2021 - 2034 ($Mn)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 UK

- 11.3.2 Germany

- 11.3.3 France

- 11.3.4 Italy

- 11.3.5 Spain

- 11.3.6 Russia

- 11.3.7 Nordics

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 South Korea

- 11.4.5 ANZ

- 11.4.6 Southeast Asia

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.6 MEA

- 11.6.1 UAE

- 11.6.2 Saudi Arabia

- 11.6.3 South Africa

Chapter 12 Company Profiles

- 12.1 AntWorks

- 12.2 Appian

- 12.3 Automation Anywhere

- 12.4 Blue Prism

- 12.5 Cognizant Technology Solutions

- 12.6 HCLTech

- 12.7 HelpSystems

- 12.8 IBM

- 12.9 Infosys

- 12.10 Kofax

- 12.11 Microsoft

- 12.12 NICE

- 12.13 Oracle Corporation

- 12.14 Pegasystems

- 12.15 Salesforce

- 12.16 SAP SE

- 12.17 Tata Consultancy Services (TCS)

- 12.18 UiPath

- 12.19 Wipro

- 12.20 WorkFusion