ビーガン食材の市場機会、成長促進要因、産業動向分析、2025年~2034年予測

Vegan Ingredients Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 235 Pages

- 納期

- 2~3営業日

- 商品コード

- 1750453

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

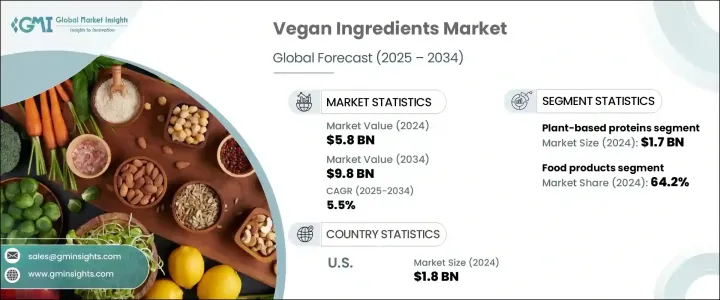

ビーガン食材の世界市場規模は2024年に58億米ドルとなり、植物性食品へのシフトと消費者の嗜好の変化、環境意識の高まり、従来の動物性食品に比べより健康的な代替食品へのアクセスの増加などを背景に、CAGR 5.5%で成長し、2034年には98億米ドルに達すると推定されます。

人々が食品の選択や動物に対する倫理的治療により意識を向けるようになるにつれて、ビーガン食材は食品イノベーションにおける重要な焦点となっています。植物性栄養への関心の高まりは、大豆、エンドウ豆、米、レンズ豆を含む植物性タンパク質への需要の高まりにつながっており、これらはより持続可能であるだけでなく、様々な食品用途において機能的な利点を提供します。このことは、食品の生産、流通、消費のあり方に変革をもたらしています。

この動向の大きな原動力となっているのは、植物ベースの食生活の普及であり、その結果、調理済み食品、スナック、飲食品、さらには栄養補助食品など、複数のカテゴリーにわたってビーガン食品が爆発的に増えています。動物性食品よりも生産に必要な資源が少ないという植物性食品の環境面での利点も、このシフトに拍車をかけています。持続可能な農業を支援する政府の取り組みや、代替タンパク源の促進が、市場の拡大をさらに後押ししています。こうした製品に対する需要が高まる中、技術革新は引き続き重要な役割を果たしており、植物性食品の食感や栄養プロファイルを強化する発酵マイコプロテインなどの新しい原料が市場に参入しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 58億米ドル |

| 予測金額 | 98億米ドル |

| CAGR | 5.5% |

植物性タンパク質セグメントは30.2%のシェアを占め、2024年の市場規模は17億米ドルでした。大豆、エンドウ豆、レンズ豆などの作物を原料とするこれらのタンパク質は、消費者が肉の代替品を求めるにつれて人気が高まっています。植物性タンパク質への注目の高まりはタンパク質源の多様化につながり、各国政府も豆類や豆類を持続可能な農業に不可欠な作物として推進しています。これらの植物性タンパク質は、肉の代用品としてだけでなく、焼き菓子、スナック菓子、コンビニエンス・ミールなどの他の食品にも使用されており、そのタンパク質含有量は健康上の利点として販売されています。

2024年に37億米ドルと評価された食品分野は、2034年までのシェア64.2%を占め、ビーガン食材市場で圧倒的な地位を占めています。このカテゴリーには、植物由来の乳製品や代替肉、調理済み製品、スナック、菓子など、幅広い製品が含まれます。この分野におけるビーガン食材の大きな需要は、健康上の利点、畜産に対する倫理的懸念、従来の動物性食品生産が環境に与える影響に関する消費者の意識の高まりが主な要因となっています。

米国のビーガン食材市場は、2024年には18億米ドルとなり、2034年までCAGR 6.3%の堅調な成長を続けると予測されています。米国は消費と技術革新の両面でリードしており、世界市場の主要な牽引役となっています。この急成長の要因には、個人の健康に対する意識の高まり、工場耕作の倫理的意味合いに対する懸念の高まり、植物ベースの食事へのシフトなどがあります。アメリカ市場は、より健康的で持続可能な食品オプションに対する需要に応えているだけでなく、ビーガン食品のイノベーションを推進しています。

世界ビーガン食材市場の主要企業には、カーギル、ADM、エボニック、BASF、ビヨンド・ミートなどがあります。これらの企業は、革新的な技術を採用することで、ポートフォリオの拡大と製品提供の改善に注力しています。また、環境に優しい生産プロセスへの投資や、様々な産業分野での植物由来原料の採用を促進するためのパートナーシップの構築により、持続可能性への取り組みを強化しています。製品群を多様化し、ビーガン食材の新たな用途を模索することで、これらの企業は急速に成長する市場での地位を確固たるものにすることを目指しています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- バリューチェーンに影響を与える要因

- 利益率分析

- ディスラプション

- 将来の展望

- 製造業者

- 販売代理店

- トランプ政権による関税への影響

- 貿易への影響

- 貿易量の混乱

- 報復措置

- 業界への影響

- 供給側の影響(原材料)

- 主要原材料の価格変動

- サプライチェーンの再構築

- 生産コストへの影響

- 供給側の影響(原材料)

- 需要側の影響(販売価格)

- 最終市場への価格伝達

- 市場シェアの動向

- 消費者の反応パターン

- 影響を受ける主要企業

- 戦略的な業界対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 政策関与

- 展望と今後の検討事項

- 貿易への影響

- 貿易統計(HSコード)

- 主要輸出国、2021-2024

- 主要輸入国、2021-2024

- サプライヤーの情勢

- 利益率分析

- 主なニュースと取り組み

- 規制情勢

- 世界の規制枠組みの概要

- FDA規制

- EUの化粧品規制

- 中国のCSAR(化粧品監督管理規制)

- 影響要因

- 促進要因

- 健康意識の高まり

- 環境の持続可能性

- 植物由来食品の技術進歩

- 政府の支援と政策イニシアチブ

- 業界の潜在的リスク&課題

- 高い生産コスト

- 消費者の認知度と受容度の低さ

- 促進要因

- 市場機会

- 発展新興経済諸国への進出

- 機能性食品および化粧品の革新ビーガン食材

- 食品サービスとプライベートラベル向けのカスタマイズされたB2Bソリューション

- 持続可能な包装とクリーンラベルの位置付け

- 市場参入と拡大戦略

- 市場参入障壁と課題

- 規制上のハードルとコンプライアンスコスト

- 知的財産の制約

- 確立されたプレーヤーの優位性

- 技術的専門知識の要件

- 市場参入戦略

- 合弁事業と戦略的提携

- ライセンシングと技術移転

- 買収とブラウンフィールドへの参入

- グリーンフィールド投資と有機的成長

- 地理的拡大の機会

- 高成長地域市場

- 未開拓市場の潜在的評価

- 文化的および規制上の考慮事項

- ローカリゼーションと適応戦略

- 製品ポートフォリオ拡大戦略

- ライン拡張と製品バリエーション

- カテゴリー間の拡張

- プレミアムおよびバリューセグメントのターゲティング

- カスタマイズとパーソナライゼーションのアプローチ

- 市場参入障壁と課題

- リスク評価と軽減戦略

- 市場リスク

- 需要の変動性と循環性

- 競争の激化と価格圧力

- 代替製品と技術

- 消費者の嗜好の変化

- 運用リスク

- サプライチェーンの混乱

- 品質管理と製品安全

- 製造と配合の課題

- 人材管理と人材管理

- 規制およびコンプライアンスリスク

- 規制状況の変化

- 原材料の制限と禁止

- ラベル表示とマーケティングクレームのリスク

- 市場リスク

- 将来の見通しと市場予測

- 短期市場見通し(1~2年)

- すぐに成長機会

- 短期的な課題

- 競合情勢の進化

- 中期市場見通し(3~5年)

- 新興市場セグメント

- テクノロジー採用曲線

- 需給バランス予測

- 長期市場見通し(5~10年)

- 破壊的技術とイノベーション

- 持続可能性主導の市場変革

- 消費者行動の進化

- 業界の統合と再編のシナリオ

- シナリオ分析と緊急時対応計画

- 最良の成長シナリオ

- ベースケース市場の進化

- 最悪の市場縮小

- 破壊的シナリオ分析

- 短期市場見通し(1~2年)

- 投資機会と戦略的提言

- 投資魅力度評価

- 高成長市場セグメント

- テクノロジー投資機会

- 地理的投資ホットスポット

- M&Aとパートナーシップの機会

- 原料メーカー向けの戦略的提言

- 製品開発とイノベーションの重点分野

- 市場ポジショニングと差別化戦略

- 持続可能性とコンプライアンスのロードマップ

- パートナーシップとコラボレーションの機会

- 最終製品メーカー向けの戦略的推奨事項

- 処方と製品開発の優先順位

- 消費者エンゲージメントとマーケティング戦略

- 流通とチャネルの最適化

- 持続可能性とブランドポジショニング

- 投資家および金融利害関係者への戦略的提言

- 潜在性の高い投資対象

- リスク評価と軽減アプローチ

- ポートフォリオ分散戦略

- 出口戦略の検討

- 投資魅力度評価

- 成長可能性分析

- ポーターの分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 競合ポジショニングマトリックス

- 戦略的展望マトリックス

第5章 市場推計・予測:製品別、2021-2034

- 主要動向

- 植物性タンパク質

- 大豆タンパク質

- 大豆タンパク質分離物

- 大豆タンパク質濃縮物

- テクスチャード大豆タンパク質

- 大豆粉

- その他

- エンドウ豆タンパク質

- エンドウ豆タンパク質分離物

- エンドウ豆タンパク質濃縮物

- テクスチャードエンドウ豆タンパク質

- 小麦タンパク質

- 必須小麦グルテン

- 小麦タンパク質分離物

- テクスチャード小麦タンパク質

- 米タンパク質

- 米タンパク質分離物

- 米タンパク質濃縮物

- その他

- ジャガイモタンパク質

- 藻類タンパク質

- スピルリナ

- クロレラ

- その他

- 大豆タンパク質

- 植物由来の乳製品代替品

- 植物性ミルク

- アーモンドミルクの材料

- 豆乳の材料

- オートミルクの材料

- ココナッツミルクの材料

- ライスミルクの材料

- その他

- 植物由来のチーズ原料

- タンパク質塩基

- 油脂

- 香料

- 機能性成分

- 植物性ヨーグルトの材料

- タンパク質塩基

- 培養物および発酵剤

- テクスチャ剤

- 香料成分

- 植物由来のバターとスプレッドの原料

- 植物油脂

- 乳化剤

- 香料

- 着色剤

- 植物由来のアイスクリームの材料

- 植物性ミルクベース

- 油脂

- 甘味料

- 安定剤および乳化剤

- 植物性ミルク

- 卵代替品

- デンプンベースの卵代替品

- タンパク質ベースの卵代替品

- 繊維ベースの卵代替品

- 豆類ベースの卵代替品

- フルーツベースの卵代替品

- アクアファバ

- 植物由来の油脂

- ココナッツオイル

- パーム油

- オリーブ油

- アボカドオイル

- ひまわり油

- キャノーラ油

- 特殊植物油

- 構造化植物脂質

- 天然香料と調味料

- 植物由来の風味豊かなフレーバー

- 植物由来の甘いフレーバー

- うま味増強剤

- スモークフレーバー

- スパイスエキス

- ハーブエキス

- 自然な色

- アントシアニン

- カロテノイド

- クロロフィル

- クルクミン

- ビートルート

- その他

- ハイドロコロイドとテクスチャライザー

- 寒天

- カラギーナン

- グアーガム

- ローカストビーンガム

- ペクチン

- キサンタンガム

- こんにゃくガム

- 加工デンプン

- ビーガン甘味料

- サトウキビ糖

- ビート糖

- ココナッツシュガー

- メープルシロップ

- アガベネクター

- デーツシロップ

- ステビア

- ラカンカ果実エキス

- ビーガン乳化剤

- レシチン(大豆、ヒマワリ)

- モノグリセリドおよびジグリセリド(植物由来)

- 柑橘類の繊維

- その他

- ビーガン防腐剤

- ローズマリーエキス

- トコフェロール

- アスコルビン酸

- その他

- 専門分野ビーガン食材

- 栄養酵母

- 海藻および藻類由来製品

- 発酵食品

- その他

第6章 市場推計・予測:用途別、2021-2034

- 主要動向

- 食品

- 植物由来の代替肉

- ハンバーガーとパテ

- ソーセージとホットドッグ

- ナゲットとストリップ

- ひき肉の代替品

- デリスライス

- 植物由来の乳製品代替品

- 牛乳代替品

- チーズの代替品

- ヨーグルトの代替品

- バターとスプレッドの代替品

- アイスクリームの代替品

- ベーカリー製品

- パンとロールパン

- ケーキとペストリー

- クッキーとビスケット

- 菓子類

- スナック

- 風味豊かなスナック

- エネルギーバー

- スープとブロス

- ソースとグレービー

- ドレッシングとマヨネーズの代替品

- 調理済み食事

- 冷凍食品

- 乳児用調製粉乳とベビーフード

- 植物由来の代替肉

- 飲み物

- 植物性ミルク

- 植物性プロテインドリンク

- スムージーとジュース

- コーヒーと紅茶の添加物

- アルコール飲料

- パーソナルケアと化粧品

- スキンケア製品

- ヘアケア製品

- カラー化粧品

- オーラルケア製品

- 栄養補助食品

- 動物飼料の代替品

- ペットフード

- 家畜飼料

- 養殖飼料

- その他

第7章 市場推計・予測:地域別、2021-2034

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- オランダ

- アジア太平洋地域

- 中国

- インド

- 日本

- 韓国

- オーストラリア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第8章 企業プロファイル

- Aadhunik Ayurveda

- ADM

- BASF

- Beyond Meat

- Cargill

- Evonik

- Schouten

- Symega

- Tofurky

- Trader Joe’s

目次

The Global Vegan Ingredients Market was valued at USD 5.8 billion in 2024 and is estimated to grow at a CAGR of 5.5% to reach USD 9.8 billion by 2034, driven by the shift toward plant-based foods and changes in consumer preferences, increasing environmental awareness, and greater access to healthier alternatives compared to traditional animal-based options. As people become more conscious of their food choices and ethical treatment of animals, vegan ingredients have become a key focus in food innovation. The growing interest in plant-based nutrition has led to increased demand for plant proteins, including soy, pea, rice, and lentils, which are not only more sustainable but also offer functional benefits in a variety of food applications. This has sparked a transformation in how food is produced, distributed, and consumed.

A major driving force behind this trend is the growing adoption of plant-based diets, which has led to an explosion of vegan food products across multiple categories, such as ready-to-eat meals, snacks, beverages, and even dietary supplements. The environmental benefits of plant-based ingredients-requiring fewer resources to produce than animal products-have also spurred the shift. Government initiatives supporting sustainable agriculture and the promotion of alternative protein sources are further boosting the market's expansion. As demand for these products rises, innovation continues to play a significant role, with new ingredients such as fermented mycoprotein entering the market to enhance the texture and nutritional profile of plant-based foods.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $5.8 Billion |

| Forecast Value | $9.8 Billion |

| CAGR | 5.5% |

The plant-based proteins segment held a 30.2% share and was valued at USD 1.7 billion in 2024. These proteins, sourced from crops like soy, peas, and lentils, are becoming increasingly popular as consumers seek alternatives to meat. The growing focus on plant proteins has led to a diversification of protein sources, as governments also promote legumes and pulses as vital crops in sustainable agriculture. These plant-based proteins are being used not only in meat substitutes but also in other food items, such as baked goods, snacks, and convenience meals, where their protein content is marketed as a health benefit.

The food products segment, valued at USD 3.7 billion in 2024, holds a dominant position in the vegan ingredients market, representing 64.2% share through 2034. This category encompasses a wide range of offerings, including plant-based dairy and meat alternatives, ready-to-bake items, snacks, and sweets. The significant demand for vegan ingredients within this sector is largely driven by increasing consumer awareness regarding health benefits, ethical concerns about animal farming, and the environmental impact of traditional animal-based food production.

United States Vegan Ingredients Market was valued at USD 1.8 billion in 2024 and is expected to continue growing at a robust CAGR of 6.3% through 2034. The U.S. leads both in terms of consumption and innovation, serving as a key driver of the global market. Factors contributing to this surge include rising awareness about personal health, a growing concern over the ethical implications of factory farming, and a shift towards plant-based diets. The American market is not only responding to the demand for healthier and more sustainable food options but also driving forward innovation in vegan food products.

Key companies in the Global Vegan Ingredients Market include Cargill, ADM, Evonik, BASF, and Beyond Meat. These companies have been focusing on expanding their portfolios and improving product offerings by adopting innovative technologies. They are also enhancing their sustainability efforts by investing in eco-friendly production processes and forging partnerships to promote the adoption of plant-based ingredients across various industries. By diversifying their product ranges and exploring new applications for vegan ingredients, these firms aim to solidify their positions in the rapidly growing market.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculations

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Trump administration tariffs

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.2.1.1 Price volatility in key materials

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.3 Demand-side impact (selling price)

- 3.2.3.1 Price transmission to end markets

- 3.2.3.2 Market share dynamics

- 3.2.3.3 Consumer response patterns

- 3.2.4 Key companies impacted

- 3.2.5 Strategic industry responses

- 3.2.5.1 Supply chain reconfiguration

- 3.2.5.2 Pricing and product strategies

- 3.2.5.3 Policy engagement

- 3.2.6 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Trade statistics (HS code)

- 3.3.1 Major exporting countries, 2021-2024 (kilo tons)

- 3.3.2 Major importing countries, 2021-2024 (kilo tons)

- 3.4 Supplier landscape

- 3.5 Profit margin analysis

- 3.6 Key news & initiatives

- 3.7 Regulatory landscape

- 3.7.1 Global regulatory framework overview

- 3.7.2 FDA regulations

- 3.7.3 EU cosmetics regulation

- 3.7.4 China's CSAR (cosmetic supervision and administration regulation)

- 3.8 Impact forces

- 3.8.1 Growth drivers

- 3.8.1.1 Rising health consciousness

- 3.8.1.2 Environmental sustainability

- 3.8.1.3 Technological advancements in plant-based foods

- 3.8.1.4 Government support and policy initiatives

- 3.8.2 Industry pitfalls & challenges

- 3.8.2.1 High production costs

- 3.8.2.2 Limited consumer awareness and acceptance

- 3.8.1 Growth drivers

- 3.9 Market opportunities

- 3.9.1 Expansion into developing economies

- 3.9.2 Innovation in functional vegan ingredients for nutraceuticals and cosmetics

- 3.9.3 Customized B2B solutions for food service and private label

- 3.9.4 Sustainable packaging and clean label positioning

- 3.10 Market entry and expansion strategies

- 3.10.1 Market entry barriers and challenges

- 3.10.1.1 Regulatory hurdles and compliance costs

- 3.10.1.2 Intellectual property constraints

- 3.10.1.3 Established player dominance

- 3.10.1.4 Technical expertise requirements

- 3.10.2 Market entry strategies

- 3.10.2.1 Joint ventures and strategic alliances

- 3.10.2.2 Licensing and technology transfer

- 3.10.2.3 Acquisition and brownfield entry

- 3.10.2.4 Greenfield investment and organic growth

- 3.10.3 Geographic expansion opportunities

- 3.10.3.1 High-growth regional markets

- 3.10.3.2 Untapped market potential assessment

- 3.10.3.3 Cultural and regulatory considerations

- 3.10.3.4 Localization and adaptation strategies

- 3.10.4 Product portfolio expansion strategies

- 3.10.4.1 Line extensions and product variants

- 3.10.4.2 Cross-category expansion

- 3.10.4.3 Premium and value segment targeting

- 3.10.4.4 Customization and personalization approaches

- 3.10.1 Market entry barriers and challenges

- 3.11 Risk assessment and mitigation strategies

- 3.11.1 Market risks

- 3.11.1.1 Demand volatility and cyclicality

- 3.11.1.2 Competitive intensity and price pressure

- 3.11.1.3 Substitute products and technologies

- 3.11.1.4 Consumer preference shifts

- 3.11.2 Operational risks

- 3.11.2.1 Supply chain disruptions

- 3.11.2.2 Quality control and product safety

- 3.11.2.3 Manufacturing and formulation challenges

- 3.11.2.4 Workforce and talent management

- 3.11.3 Regulatory and compliance risks

- 3.11.3.1 Changing regulatory landscape

- 3.11.3.2 Ingredient restrictions and bans

- 3.11.3.3 Labeling and marketing claim risks

- 3.11.1 Market risks

- 3.12 Future outlook and market projections

- 3.12.1 Short-term market outlook (1-2 years)

- 3.12.1.1 Immediate growth opportunities

- 3.12.1.2 Near-term challenges

- 3.12.1.3 Competitive landscape evolution

- 3.12.2 Medium-term market outlook (3-5 years)

- 3.12.2.1 Emerging market segments

- 3.12.2.2 Technology adoption curves

- 3.12.2.3 Supply-demand balance projections

- 3.12.3 Long-term market outlook (5-10 years)

- 3.12.3.1 Disruptive technologies and innovations

- 3.12.3.2 Sustainability-driven market transformation

- 3.12.3.3 Consumer behavior evolution

- 3.12.3.4 Industry consolidation and restructuring scenarios

- 3.12.4 Scenario analysis and contingency planning

- 3.12.4.1 Best-case growth scenario

- 3.12.4.2 Base-case market evolution

- 3.12.4.3 Worst-case market contraction

- 3.12.4.4 Disruptive scenario analysis

- 3.12.1 Short-term market outlook (1-2 years)

- 3.13 Investment opportunities and strategic recommendations

- 3.13.1 Investment attractiveness assessment

- 3.13.1.1 High-growth market segments

- 3.13.1.2 Technology investment opportunities

- 3.13.1.3 Geographic investment hotspots

- 3.13.1.4 M&A and partnership opportunities

- 3.13.2 Strategic recommendations for ingredient manufacturers

- 3.13.2.1 Product development and innovation focus areas

- 3.13.2.2 Market positioning and differentiation strategies

- 3.13.2.3 Sustainability and compliance roadmap

- 3.13.2.4 Partnership and collaboration opportunities

- 3.13.2.5 Strategic recommendations for end-product manufacturers

- 3.13.2.6 Formulation and product development priorities

- 3.13.2.7 Consumer engagement and marketing strategies

- 3.13.2.8 Distribution and channel optimization

- 3.13.2.9 Sustainability and brand positioning

- 3.13.3 Strategic recommendations for investors and financial stakeholders

- 3.13.3.1 High-potential investment targets

- 3.13.3.2 Risk assessment and mitigation approaches

- 3.13.3.3 Portfolio diversification strategies

- 3.13.3.4 Exit strategy considerations

- 3.13.1 Investment attractiveness assessment

- 3.14 Growth potential analysis

- 3.15 Porter’s analysis

- 3.16 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Product, 2021 - 2034 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Plant-based proteins

- 5.2.1 Soy protein

- 5.2.1.1 Soy protein isolates

- 5.2.1.2 Soy protein concentrates

- 5.2.1.3 Textured soy protein

- 5.2.1.4 Soy flour

- 5.2.1.5 Others

- 5.2.2 Pea protein

- 5.2.2.1 Pea protein isolates

- 5.2.2.2 Pea protein concentrates

- 5.2.2.3 Textured pea protein

- 5.2.3 Wheat protein

- 5.2.3.1 Vital wheat gluten

- 5.2.3.2 Wheat protein isolates

- 5.2.3.3 Textured wheat protein

- 5.2.4 Rice protein

- 5.2.4.1 Rice protein isolates

- 5.2.4.2 Rice protein concentrates

- 5.2.4.3 Others

- 5.2.5 Potato protein

- 5.2.6 Algae protein

- 5.2.6.1 Spirulina

- 5.2.6.2 Chlorella

- 5.2.6.3 Others

- 5.2.1 Soy protein

- 5.3 Plant-based dairy alternatives

- 5.3.1 Plant milks

- 5.3.1.1 Almond milk ingredients

- 5.3.1.2 Soymilk ingredients

- 5.3.1.3 Oat milk ingredients

- 5.3.1.4 Coconut milk ingredients

- 5.3.1.5 Rice milk ingredients

- 5.3.1.6 Others

- 5.3.2 Plant-based cheese ingredients

- 5.3.2.1 Protein bases

- 5.3.2.2 Oils and fats

- 5.3.2.3 Flavoring agents

- 5.3.2.4 Functional ingredients

- 5.3.3 Plant-based yogurt ingredients

- 5.3.3.1 Protein bases

- 5.3.3.2 Cultures and fermentation agents

- 5.3.3.3 Texturizing agents

- 5.3.3.4 Flavoring ingredients

- 5.3.4 Plant-based butter and spreads ingredients

- 5.3.4.1 Plant oils and fats

- 5.3.4.2 Emulsifiers

- 5.3.4.3 Flavoring agents

- 5.3.4.4 Coloring agents

- 5.3.5 Plant-based ice cream ingredients

- 5.3.5.1 Plant milk bases

- 5.3.5.2 Fats and oils

- 5.3.5.3 Sweeteners

- 5.3.5.4 Stabilizers and emulsifiers

- 5.3.1 Plant milks

- 5.4 Egg replacers

- 5.4.1 Starch-based egg replacers

- 5.4.2 Protein-based egg replacers

- 5.4.3 Fiber-based egg replacers

- 5.4.4 Legume-based egg replacers

- 5.4.5 Fruit-based egg replacers

- 5.4.6 Aquafaba

- 5.5 Plant-based fats and oils

- 5.5.1 Coconut oil

- 5.5.2 Palm oil

- 5.5.3 Olive oil

- 5.5.4 Avocado oil

- 5.5.5 Sunflower oil

- 5.5.6 Canola oil

- 5.5.7 Specialty plant oils

- 5.5.8 Structured plant lipids

- 5.6 Natural flavors and enhancers

- 5.6.1 Plant-based savory flavors

- 5.6.2 Plant-based sweet flavors

- 5.6.3 Umami enhancers

- 5.6.4 Smoke flavors

- 5.6.5 Spice extracts

- 5.6.6 Herb extracts

- 5.7 Natural colors

- 5.7.1 Anthocyanins

- 5.7.2 Carotenoids

- 5.7.3 Chlorophyll

- 5.7.4 Curcumin

- 5.7.5 Beetroot

- 5.7.6 Others

- 5.8 Hydrocolloids and texturizers

- 5.8.1 Agar-agar

- 5.8.2 Carrageenan

- 5.8.3 Guar gum

- 5.8.4 Locust bean gum

- 5.8.5 Pectin

- 5.8.6 Xanthan gum

- 5.8.7 Konjac gum

- 5.8.8 Modified starches

- 5.9 Vegan sweeteners

- 5.9.1 Cane sugar

- 5.9.2 Beet sugar

- 5.9.3 Coconut sugar

- 5.9.4 Maple syrup

- 5.9.5 Agave nectar

- 5.9.6 Date syrup

- 5.9.7 Stevia

- 5.9.8 Monk fruit extract

- 5.10 Vegan emulsifiers

- 5.10.1 Lecithin (soy, sunflower)

- 5.10.2 Mono- and diglycerides (plant-derived)

- 5.10.3 Citrus fiber

- 5.10.4 Others

- 5.11 Vegan preservatives

- 5.11.1 Rosemary extract

- 5.11.2 Tocopherols

- 5.11.3 Ascorbic acid

- 5.11.4 Others

- 5.12 Specialty vegan ingredients

- 5.12.1 Nutritional yeast

- 5.12.2 Seaweed and algae derivatives

- 5.12.3 Fermented ingredients

- 5.12.4 Others

Chapter 6 Market Estimates & Forecast, By Application, 2021 - 2034 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Food products

- 6.2.1 Plant-based meat alternatives

- 6.2.1.1 Burgers and patties

- 6.2.1.2 Sausages and hot dogs

- 6.2.1.3 Nuggets and strips

- 6.2.1.4 Ground meat alternatives

- 6.2.1.5 Deli slices

- 6.2.2 Plant-based dairy alternatives

- 6.2.2.1 Milk alternatives

- 6.2.2.2 Cheese alternatives

- 6.2.2.3 Yogurt alternatives

- 6.2.2.4 Butter and spread alternatives

- 6.2.2.5 Ice cream alternatives

- 6.2.3 Bakery products

- 6.2.3.1 Breads and rolls

- 6.2.3.2 Cakes and pastries

- 6.2.3.3 Cookies and biscuits

- 6.2.4 Confectionery

- 6.2.5 Snacks

- 6.2.5.1 Savory snacks

- 6.2.5.2 Energy bars

- 6.2.6 Soups and broths

- 6.2.6.1 Sauces and gravies

- 6.2.6.2 Dressings and mayonnaise alternatives

- 6.2.7 Ready meals

- 6.2.8 Frozen meals

- 6.2.9 Infant formula and baby food

- 6.2.1 Plant-based meat alternatives

- 6.3 Beverages

- 6.3.1 Plant-based milk

- 6.3.2 Plant-based protein drinks

- 6.3.3 Smoothies and juices

- 6.3.4 Coffee and tea additives

- 6.3.5 Alcoholic beverages

- 6.4 Personal care and cosmetics

- 6.4.1 Skincare products

- 6.4.2 Haircare products

- 6.4.3 Color cosmetics

- 6.4.4 Oral care products

- 6.5 Dietary supplements

- 6.6 Animal feed alternatives

- 6.7 Pet food

- 6.7.1 Livestock feed

- 6.7.2 Aquaculture feed

- 6.7.3 Others

Chapter 7 Market Estimates & Forecast, By Region, 2021 - 2034 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.3 Europe

- 7.3.1 UK

- 7.3.2 Germany

- 7.3.3 France

- 7.3.4 Italy

- 7.3.5 Spain

- 7.3.6 Netherlands

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 India

- 7.4.3 Japan

- 7.4.4 South Korea

- 7.4.5 Australia

- 7.5 Latin America

- 7.5.1 Brazil

- 7.5.2 Mexico

- 7.5.3 Argentina

- 7.6 MEA

- 7.6.1 South Africa

- 7.6.2 Saudi Arabia

- 7.6.3 UAE

Chapter 8 Company Profiles

- 8.1 Aadhunik Ayurveda

- 8.2 ADM

- 8.3 BASF

- 8.4 Beyond Meat

- 8.5 Cargill

- 8.6 Evonik

- 8.7 Schouten

- 8.8 Symega

- 8.9 Tofurky

- 8.10 Trader Joe’s

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 235 Pages

- 納期

- 2~3営業日