ベトナムの構造用鋼加工-市場シェア分析、産業動向と統計、成長予測(2025年~2030年)

Vietnam Structural Steel Fabrication - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日

- 商品コード

- 1687888

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

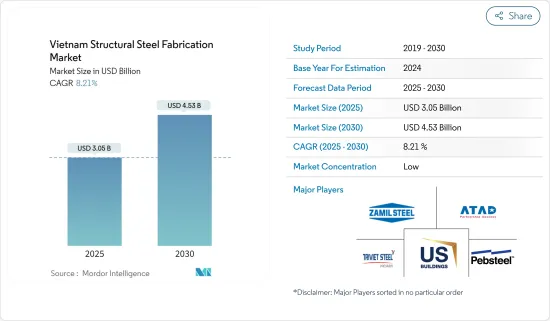

ベトナムの構造用鋼加工市場規模は2025年に30億5,000万米ドルと推定され、予測期間(2025~2030年)のCAGRは8.21%で、2030年には45億3,000万米ドルに達すると予測されます。

主要ハイライト

- 急速な都市化、インフラの成長、国内の鉄鋼の増加により、ベトナムの鉄鋼産業の生産は20%以上の驚異的な伸びを示しました。

- 2022年の鉄鋼完成品消費量は前年比約17%減の約1,250万トンに達しました。完成鋼販売は減少したが、鉄鋼輸出は依然として成長を示しました。最初の6ヶ月間の完成鋼輸出は、2021年の同期間比6.5%増の38億8,100万トンに達しました。

- 産業の専門家によると、ベトナムの一人当たりの鉄鋼消費量は、インフラと不動産投資の増加に牽引され、今後数年間で増加すると予想されます。

- また、ベトナムの建設セクターにおける鉄鋼需要は、今後数年間で10%以上増加すると予想されます。

- グローバリゼーションに伴う社会経済諸国の開発により、土木工事の需要は近年増加傾向にあり、これらの材料を使用する必要性は多くの注目と関心を持っています。

- 鉄骨構造は現在最も普及している構造物の一つであり、高層ビルから工業用ビルまで様々なプロジェクトの設計・建設に全面的に利用・応用されています。

- ベトナム政府が近代的なインフラ開発に力を入れていることもあり、ベトナムにおける構造用鋼の需要が高まっている

ベトナムの構造用鋼市場動向

インフラ活動の増加が生産を後押し

ベトナムは現在、粗鋼生産量の29%を占めており、この地域でトップの生産国です。ベトナムの鉄鋼産業は過去10年間で急成長を遂げ、2021年には国内粗鋼生産量が年間1,950万トンという記録的な水準に達し、世界第13位にランクされると予想されています。

ベトナムは交通、特に道路、空港、港湾に多額の投資を行ってきました。近年、ベトナムの公共・民間インフラ投資はGDPの5.7%に達し、東南アジアで最も高く、アジアでは中国(GDPの6.8%)に次いで2番目に高いです。

最近、ベトナム政府は2021~2030年にかけて、道路、鉄道、内陸水路、海上、航空輸送インフラの建設と改良に430億~650億米ドルを支出する計画を承認しました。

また、政府は2021年3月29日発効の新しい官民パートナーシップ(PPP)法を制定し、特に交通、送電網、発電所セグメントにおけるインフラのアップグレードを拡大するための民間投資を支援・規制しています。この動きは、国家債務と財政施策への負担を軽減するため、より多くの民間投資を誘致するためです。

加えて、ベトナムの急速な都市化は、交通・公共事業セクター開発の強力な推進力となっています。現在、人口の50%が主要都市に居住していると推定され、人口の増加はすでに既存の接続ネットワークや公益事業システムの能力を超えています。

材料の移動に関しては、ベトナムは高炉を使って鉄鉱石と鉄を製錬して鉄鋼にするという標準的な方法をとっています。生産量の約30%を占める電気誘導炉技術に比べ、この技術は70%を占めます。OECD(2021年)の推定によると、ベトナムの製鋼誘導炉能力は163万トンで、ASEAN経済圏の中で第3位です。

ベトナムへのFDI流入が増加

- ここ数年、米国と中国の政治的緊張により、多国籍企業はサプライチェーンを多様化するために国境の南に移動しています。これにより、ベトナムは外国直接投資のホットスポットとなっています。

- ベトナムは2022年の最初の11ヵ月間に251億米ドルをもたらしました。ベトナムに最も投資している国は韓国です。2022年11月までに、韓国はベトナムの外国直接投資プロジェクトに800億米ドル以上を投資しています。

- ベトナムがFDIを必要としているのは、ベトナム経済を成功させるために必要な資本とさまざまな必須スキルが不足しているからです。資本を供給し、工場やその他の施設を建設するFDIのおかげで、ベトナム国民のために何百万もの雇用が創出されています。

- ベトナムへの外国投資は、前年比で減少しているにもかかわらず、ベトナム経済の明るいスポットであり続けています。

- 計画投資省のデータによると、新たに登録された外国直接投資(FDI)プロジェクトは2,036件(124億5,000万米ドル相当)で、件数は前年比17.1%増加したが、金額は18.4%減少しました。

- また、1,107のプロジェクトが資本調整され、その総額は101億2,000万米ドルで、それぞれ前年比12.4%増、12.2%増となりました。

- 外国人投資家は、国家経済分類システムの21部門中19部門に資金を投入し、そのうち、加工製造業は168億米ドル以上の投資総額で、国の総資本の60.6%を占め、FDI誘致の面でリードを維持しました。

ベトナムの構造用鋼加工産業概要

ベトナムの構造用鋼加工市場はセグメント化されており、国内外から多くの企業が進出しています。本レポートでは、ベトナムの構造用鋼加工市場の主要企業を取り上げています。市場シェアの面では、市場の大部分を中小規模の参入企業が占めているため、国内の大手参入企業は主要シェアを獲得するために互いに競争しています。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の成果

- 調査の前提

- 調査範囲

第2章 調査手法

- 分析手法

- 調査フェーズ

第3章 市場力学と洞察

- 市場概要

- 促進要因

- 急速な都市化

- インフラ開発

- 抑制要因

- 熟練労働者の不足

- 原料価格の変動

- 機会

- 高層ビルの需要

- 再生可能エネルギーセグメントの成長

- バリューチェーン/サプライチェーン分析

- 産業の魅力-ポーターのファイブフォース分析

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

- 技術スナップショット

- 政府の規制と主要取り組み

- COVID-19の市場への影響

第4章 市場セグメンテーション

- エンドユーザー産業別

- 製造業

- 電力エネルギー

- 建設

- 石油・ガス

- その他

- 製品タイプ別

- 重量鉄鋼

- 軽量形鋼

- その他

第5章 競合情勢

- 市場競争概要

- 主要企業プロファイル

- Zamil Steel Buildings Vietnam Company Limited.

- PEB Steel

- Atad Steel Structure Corporation

- Universal Vietnam Steel Buildings Company Limited

- Tri Viet Steel

- Kirby Southeast Asia Co. Ltd.

- Metalic Vietnam Co. LTD.

- PMB STEEL

- Dai Dung Metallic Manufacture Construction And Trade Corporation*

第6章 投資分析

第7章 投資分析市場の将来

第8章 付録

目次

The Vietnam Structural Steel Fabrication Market size is estimated at USD 3.05 billion in 2025, and is expected to reach USD 4.53 billion by 2030, at a CAGR of 8.21% during the forecast period (2025-2030).

Key Highlights

- Rapid urbanization, growth in infrastructure and increasing steel within the country have resulted in an astonishing rate of more than 20% growth in the production of Vietnam's steel industry.

- Finished steel consumption reached about approx. 12.5 million tons, down about 17% year-on-year in 2022. Although finished steel sales declined, steel exports still saw growth. Finished steel exports in the first 6 months reached 3,881 million tons, up 6.5% over the same period in 2021.

- As per industry experts, per capita steel consumption in Vietnam is expected to increase in the next few years driven by the rising infrastructure and property investments.

- Also, the demand for steel in the Vietnam construction sector is expected to rise more than 10% over the next few years.

- Due to the development of the socio-economy along with the trend of globalization, the demand for construction of civil works tends to increase in recent years, so the need to use these materials are a lot of attention and interest.

- Steel structure is one of the most popular types of structures today, fully utilized and applied in a variety of designs and construction of various projects from high-rise buildings to industrial buildings.

- The Vietnam's government's emphasis on developing mordern infrastructure has increased the demand for the structural steel in the market.

Vietnam Structural Steel Fabrication Market Trends

Increase In Infrastructure Activities is boosting the production

Vietnam is currently the top producer in the region because it makes up 29% of all the crude steel made. Vietnam's steel industry has grown rapidly over the last ten years, and by 2021 it is expected to rank 13 globally, with domestic crude steel output reaching a record level of 19.5 million tons per year.

Vietnam has heavily invested in transportation, particularly roads, airports, and seaports. Vietnam's public and private investment in infrastructure reached 5.7% of GDP in recent years, the highest in Southeast Asia and second highest in Asia after only China (6.8% of GDP).

Recently, the Vietnamese government approved a plan to spend USD 43-65 billion on building and upgrading road, rail, inland waterways, sea, and air transport infrastructure between 2021-2030.

The government also enacted a new Public Private Partnership (PPP) Law, effective March 29, 2021, to support and regulate private investment to scale up infrastructure upgrades, especially in the transportation, power grid, and power plant sectors. This movement is to attract more private investment to reduce the burden on the national debt and fiscal policy.

In addition, rapid urbanization in Vietnam is a strong driver for developing the transport and utilities sector. With 50% of the population estimated to now live in major cities, the rising population has already exceeded the capacity of the existing connectivity networks and utility systems.

When it comes to moving materials, Vietnam follows the standard method of using blast furnaces to turn iron ore and iron smelting into steel. Compared to electric induction furnace technology, which accounts for about 30% of production, this technique accounts for 70%. The OECD (2021) estimated that Vietnam's steelmaking induction furnace capacity is 1.63 million metric tons, ranking third among ASEAN economies.

FDI Inflows are increasing in Vietnam

- In the past few years, political tensions between the U.S. and China have caused multinational companies to move south of the border to diversify their supply chains. This has made Vietnam a hotspot for foreign direct investment.

- Vietnam brought in USD 25.1 billion in the first 11 months of 2022. The Republic of South Korea is the nation that invests the most in Vietnam. By November 2022, the RoK had committed more than USD 80 billion to foreign direct investment projects in Vietnam.

- Vietnam needs FDI because it lacks the capital and various essential skills required to successfully build its economy. Thanks to FDI, which also supplies capital and constructs factories and other facilities, millions of jobs are created for Vietnamese citizens.

- Foreign investment in Vietnam remains a bright spot on Vietnam's economic picture, despite experiencing a year-on-year decrease in value.

- Data from the Ministry of Planning and Investment showed there were 2,036 newly-registered foreign direct investment (FDI) projects worth USD 12.45 billion, up 17.1 per cent year-on-year in the number of projects, but down 18.4 per cent in value.

- In addition, 1,107 projects had their capital adjusted, with a total amount of USD 10.12 billion, up 12.4 per cent and 12.2 per cent year-on-year, respectively.

- Foreign investors poured funds into 19 out of 21 sectors in the national economic classification system, of which the processing and manufacturing industry maintained its lead in terms of attracting FDI with a total investment of over USD 16.8 billion, accounting for 60.6 per cent of the country's total capital.

Vietnam Structural Steel Fabrication Industry Overview

The Vietnam structural steel fabrication market is fragmented, with many international and domestic players active in the country. Main players in the structural steel fabrication market in Vietnam are covered in the report. In terms of market share, the large players in the country compete with each other to gain a major share as the market is largely occupied by small and medium-sized players.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Deliverables

- 1.2 Study Assumptions

- 1.3 Scope of the Study

2 RESEARCH METHODOLOGY

- 2.1 Analysis Methodology

- 2.2 Research Phases

3 MARKET INSIGHTS AND DYNAMICS

- 3.1 Market Overview

- 3.2 Drivers

- 3.2.1 Rapid Urbanization

- 3.2.2 Infrastructure Development

- 3.3 Restraints

- 3.3.1 Shortage of skilled labour

- 3.3.2 Fluctuating prices of raw materials

- 3.4 Opportunities

- 3.4.1 Demand for high rise buildings

- 3.4.2 The growth of renewable energy sector

- 3.5 Value Chain / Supply Chain Analysis

- 3.6 Industry Attractiveness - Porter's Five Forces Analysis

- 3.6.1 Bargaining Power of Buyers/Consumers

- 3.6.2 Bargaining Power of Suppliers

- 3.6.3 Threat of New Entrants

- 3.6.4 Threat of Substitute Products

- 3.6.5 Intensity of Competitive Rivalry

- 3.7 Technological Snapshot

- 3.8 Government Regulations and Key Initiatives

- 3.9 Impact of COVID-19 on the Mraket

4 MARKET SEGMENTATION

- 4.1 By End-User Industry

- 4.1.1 Manufacturing

- 4.1.2 Power and Energy

- 4.1.3 Construction

- 4.1.4 Oil and Gas

- 4.1.5 Other End-User Industries

- 4.2 By Product Type

- 4.2.1 Heavy Sectional Steel

- 4.2.2 Light Sectional Steel

- 4.2.3 Other Product Types

5 COMPETITIVE LANDSCAPE

- 5.1 Market Competition Overview

- 5.2 Key Company Profiles

- 5.2.1 Zamil Steel Buildings Vietnam Company Limited.

- 5.2.2 PEB Steel

- 5.2.3 Atad Steel Structure Corporation

- 5.2.4 Universal Vietnam Steel Buildings Company Limited

- 5.2.5 Tri Viet Steel

- 5.2.6 Kirby Southeast Asia Co. Ltd.

- 5.2.7 Metalic Vietnam Co. LTD.

- 5.2.8 PMB STEEL

- 5.2.9 Dai Dung Metallic Manufacture Construction And Trade Corporation*

6 INVESTMENT ANALYSIS

7 FUTURE OF THE MARKET

8 APPENDIX

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日