データセンター用バッテリー市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測

Data Center Battery Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025-2034- 発行日

- ページ情報

- 英文 202 Pages

- 納期

- 2~3営業日

- 商品コード

- 1699399

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

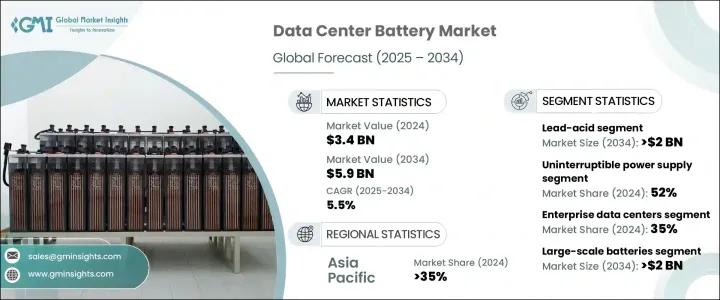

データセンター用バッテリーの世界市場規模は、2024年に34億米ドルとなり、2025年から2034年にかけてCAGR 5.5%で成長すると予測されています。

エネルギー効率の高い技術や持続可能なソリューションに対する需要の高まりが、データセンターの電源管理の展望を再構築しています。世界中の企業が持続可能性を優先する中、データセンターは環境への影響を最小限に抑えるため、エネルギー効率の高いバッテリーソリューションへと戦略的にシフトしています。再生可能エネルギー源の採用が進み、二酸化炭素排出に関する政府の規制が厳しくなっていることも、高度なバッテリー技術に対する需要をさらに押し上げています。

この進化する市場で最も重要な動向のひとつは、従来の鉛蓄電池からリチウムイオン電池への移行です。企業は、より長い寿命、より高いエネルギー密度、メンテナンス要件の削減を提供する高性能エネルギー貯蔵ソリューションを求めています。リチウムイオン電池は、エネルギー効率を改善し、ダウンタイムを削減し、持続可能性の目標をサポートする能力により、好ましい選択肢として浮上しています。さらに、ニッケル亜鉛やその他の革新的なバッテリー化学物質などのエネルギー貯蔵技術の進歩は、より効率的で信頼性の高いソリューションを提供することで、市場をさらに変革しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 34億米ドル |

| 予測金額 | 59億米ドル |

| CAGR | 5.5% |

データセンター用バッテリー市場は、鉛蓄電池、リチウムイオン電池、ニッケル亜鉛電池、その他の技術など、バッテリーの種類によって分類されます。2024年には、鉛蓄電池が市場シェアの40%を占める。古い技術であるにもかかわらず、鉛蓄電池はその手頃な価格と信頼性により、依然として広く使用されています。多くのデータセンターが鉛蓄電池システムへの投資を続けているのは、初期コストが低く、無停電電源装置(UPS)アプリケーションで実績があるからです。さらに、密閉型鉛蓄電池の進歩によりメンテナンスの必要性が最小限に抑えられ、既存のインフラにとって実用的なソリューションとなっています。

市場は用途別にもセグメント化されており、2024年にはUPS分野が52%のシェアを占める。UPSシステムは、停電時に即座にバックアップ電力を供給し、シームレスな運用を保証してデータ損失を防ぐため、データセンターにとって重要です。これらのシステムはまた、運用の中断につながる電圧変動や電力サージから精密機器を保護します。リチウムイオンバッテリーは、その長寿命、高速充電機能、高エネルギー密度により、UPSアプリケーションで人気を集めています。データセンター事業者がより弾力的で効率的なバックアップ電源オプションを求めるにつれ、リチウムイオンソリューションへのシフトが加速しています。

アジア太平洋地域のデータセンター用バッテリー市場は2024年に35%のシェアを占め、さまざまな産業でデジタルインフラが急速に拡大していることがその要因となっています。クラウド・コンピューティング、人工知能、データ駆動型技術への依存の高まりにより、同地域では安定した持続可能な電力ソリューションへのニーズが高まっています。アジア太平洋地域の政府は再生可能エネルギーの導入を積極的に推進しており、これが先進的な蓄電池ソリューションへの投資の増加につながっています。同地域のデータセンターが拡大を続けるなか、高性能で環境に優しいエネルギー貯蔵ソリューションに対する需要は、今後も市場の主要促進要因であり続けると思われます。

目次

第1章 調査手法と調査範囲

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- 原材料サプライヤー

- 部品サプライヤー

- メーカー

- 技術プロバイダー

- サービスプロバイダー

- 流通業者

- 最終用途

- サプライヤーの状況

- 利益率分析

- 技術とイノベーションの展望

- 特許分析

- 主要ニュースと取り組み

- 規制状況

- 価格動向

- コスト内訳分析

- 影響要因

- 促進要因

- バッテリー技術の進歩

- 無停電電源装置(UPS)の需要増加

- データセンターの電力消費の増加

- 世界のデータセンター建設の増加

- 業界の潜在的リスク&課題

- 初期資本コストの高さ

- 既存インフラとの統合が複雑

- 促進要因

- 成長可能性分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業シェア分析

- 競合のポジショニング・マトリックス

- 戦略展望マトリックス

第5章 市場推計・予測:バッテリー別、2021年~2034年

- 主要動向

- 鉛酸

- 構造別

- 浸水型

- VRLA

- AGM

- ゲル

- 構造別

- リチウムイオン

- 化学別

- LFP

- LCO

- LTO

- NMC

- NCA

- LMO

- 化学別

- ニッケル亜鉛

- その他

第6章 市場推計・予測:電池容量別、2021年~2034年

- 主要動向

- 小規模電池(100 kWh以下)

- 中規模電池(100kWh~1MWh)

- 大規模電池(1MWh以上)

第7章 市場推計・予測:データセンター別、2021年~2034年

- 主要動向

- エンタープライズデータセンター

- コロケーションデータセンター

- ハイパースケールデータセンター

- エッジデータセンター

第8章 市場推計・予測:用途別、2021年~2034年

- 主要動向

- 無停電電源装置(UPS)

- バックアップ電源システム

- 蓄電システム(ESS)

- ピークカットと負荷分散

第9章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- 北欧

- アジア太平洋

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- 東南アジア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- UAE

- 南アフリカ

- サウジアラビア

第10章 企業プロファイル

- Alpha Technologies

- C&D Technology

- Permanently closed

- Delta Electronics

- East Penn

- Energon

- EnerSys

- Exide Technologies

- FIAMM Energy Technology

- GS Yuasa

- Huawei Technologies

- Intercel

- Leoch

- LG Energy Solution

- MK BatteryUiPath

- Narada Power Source

- NorthStar Battery Company

- Power Sonic

- Saft Groupe

- Samsung SDI

目次

The Global Data Center Battery Market was valued at USD 3.4 billion in 2024 and is expected to grow at a CAGR of 5.5% between 2025 and 2034. The increasing demand for energy-efficient technologies and sustainable solutions is reshaping the landscape of data center power management. As businesses worldwide prioritize sustainability, data centers are making strategic shifts toward energy-efficient battery solutions to minimize their environmental impact. The growing adoption of renewable energy sources and stringent government regulations on carbon emissions are further driving the demand for advanced battery technologies.

One of the most significant trends in this evolving market is the transition from traditional lead-acid batteries to lithium-ion batteries. Companies are seeking high-performance energy storage solutions that offer longer lifespans, higher energy density, and reduced maintenance requirements. Lithium-ion batteries are emerging as the preferred choice due to their ability to improve energy efficiency, reduce downtime, and support sustainability objectives. Additionally, advancements in energy storage technologies, such as nickel-zinc and other innovative battery chemistries, are further revolutionizing the market by providing more efficient and reliable solutions.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $3.4 Billion |

| Forecast Value | $5.9 Billion |

| CAGR | 5.5% |

The data center battery market is categorized based on battery type, including lead-acid, lithium-ion, nickel-zinc, and other technologies. In 2024, lead-acid batteries accounted for 40% of the market share. Despite being an older technology, lead-acid batteries remain widely used due to their affordability and reliability. Many data centers continue to invest in lead-acid battery systems because of their lower initial costs and proven track record in uninterruptible power supply (UPS) applications. Additionally, sealed lead-acid battery advancements have minimized maintenance needs, making them a practical solution for existing infrastructure.

The market is also segmented by application, with the UPS segment holding a 52% share in 2024. UPS systems are critical for data centers as they provide immediate backup power during outages, ensuring seamless operations and preventing data loss. These systems also protect sensitive equipment from voltage fluctuations and power surges that can lead to operational disruptions. Lithium-ion batteries are gaining traction in UPS applications due to their extended lifespan, faster recharge capabilities, and higher energy density. This shift toward lithium-ion solutions is accelerating as data center operators seek more resilient and efficient backup power options.

Asia Pacific Data Center Battery Market held a 35% share in 2024, fueled by the rapid expansion of digital infrastructure across various industries. The increasing reliance on cloud computing, artificial intelligence, and data-driven technologies has heightened the need for stable and sustainable power solutions in the region. Governments in Asia Pacific are actively promoting renewable energy adoption, which has led to increased investments in advanced battery storage solutions. As data centers in this region continue to expand, the demand for high-performance and environmentally friendly energy storage solutions will remain a key market driver.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates & calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimation

- 1.3 Forecast model

- 1.4 Primary research and validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market scope & definition

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Raw material suppliers

- 3.1.2 Component suppliers

- 3.1.3 Manufacturers

- 3.1.4 Technology providers

- 3.1.5 Service providers

- 3.1.6 Distributors

- 3.1.7 End use

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Technology & innovation landscape

- 3.5 Patent analysis

- 3.6 Key news & initiatives

- 3.7 Regulatory landscape

- 3.8 Price trends

- 3.9 Cost breakdown analysis

- 3.10 Impact forces

- 3.10.1 Growth drivers

- 3.10.1.1 Growing advancements in battery technology

- 3.10.1.2 Rising demand for Uninterrupted Power Supply (UPS)

- 3.10.1.3 Increase in data center power consumption

- 3.10.1.4 Rising construction of data centers across the globe

- 3.10.2 Industry pitfalls & challenges

- 3.10.2.1 High initial capital costs

- 3.10.2.2 Complexity in integration with existing infrastructure

- 3.10.1 Growth drivers

- 3.11 Growth potential analysis

- 3.12 Porter's analysis

- 3.13 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Battery, 2021 - 2034 ($Bn, Units)

- 5.1 Key trends

- 5.2 Lead-acid

- 5.2.1 By construction

- 5.2.1.1 Flooded

- 5.2.1.2 VRLA

- 5.2.1.2.1 AGM

- 5.2.1.2.2 GEL

- 5.2.1 By construction

- 5.3 Lithium-ion

- 5.3.1 By chemistry

- 5.3.1.1 LFP

- 5.3.1.2 LCO

- 5.3.1.3 LTO

- 5.3.1.4 NMC

- 5.3.1.5 NCA

- 5.3.1.6 LMO

- 5.3.1 By chemistry

- 5.4 Nickel zinc

- 5.5 Others

Chapter 6 Market Estimates & Forecast, By Battery Capacity, 2021 - 2034 ($Bn, Units)

- 6.1 Key trends

- 6.2 Small-scale batteries (Below 100 kWh)

- 6.3 Medium-scale batteries (100 kWh - 1 MWh)

- 6.4 Large-scale batteries (Above 1 MWh)

Chapter 7 Market Estimates & Forecast, By Data Center, 2021 - 2034 ($Bn, Units)

- 7.1 Key trends

- 7.2 Enterprise data centers

- 7.3 Colocation data centers

- 7.4 Hyperscale data centers

- 7.5 Edge data centers

Chapter 8 Market Estimates & Forecast, By Application, 2021 - 2034 ($Bn, Units)

- 8.1 Key trends

- 8.2 Uninterruptible power supply (UPS)

- 8.3 Backup power systems

- 8.4 Energy storage systems (ESS)

- 8.5 Peak shaving and load balancing

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn, Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Russia

- 9.3.7 Nordics

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Southeast Asia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 UAE

- 9.6.2 South Africa

- 9.6.3 Saudi Arabia

Chapter 10 Company Profiles

- 10.1 Alpha Technologies

- 10.2 C&D Technology

- 10.3 Permanently closed

- 10.4 Delta Electronics

- 10.5 East Penn

- 10.6 Energon

- 10.7 EnerSys

- 10.8 Exide Technologies

- 10.9 FIAMM Energy Technology

- 10.10 GS Yuasa

- 10.11 Huawei Technologies

- 10.12 Intercel

- 10.13 Leoch

- 10.14 LG Energy Solution

- 10.15 MK BatteryUiPath

- 10.16 Narada Power Source

- 10.17 NorthStar Battery Company

- 10.18 Power Sonic

- 10.19 Saft Groupe

- 10.20 Samsung SDI

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 202 Pages

- 納期

- 2~3営業日