|

市場調査レポート

商品コード

1699277

プログラマブルロジックコントローラ市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測Programmable Logic Controller (PLC) Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025-2034 |

||||||

カスタマイズ可能

|

|||||||

| プログラマブルロジックコントローラ市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測 |

|

出版日: 2025年02月18日

発行: Global Market Insights Inc.

ページ情報: 英文 200 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

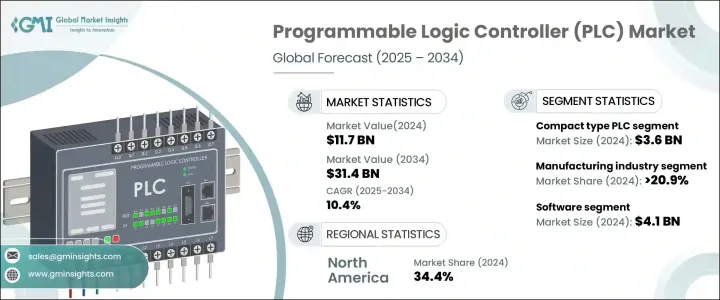

プログラマブルロジックコントローラの世界市場は、2024年に117億米ドルとなり、2025年から2034年にかけてCAGR 10.4%で成長すると予測されています。

インダストリー4.0、デジタルツイン技術、自動化主導型ソリューションの採用が増加していることが、市場拡大に拍車をかけています。電気自動車(EV)の需要の高まりは、PLCベースのシステムが生産ラインの自動化と製造効率の最適化に重要な役割を果たすため、成長をさらに加速させています。自動車メーカーは、EVの生産を合理化し、拡張性を高め、ダウンタイムを削減するために、PLC駆動ソリューションに依存しています。さらに、これらのシステムはバッテリー製造や複雑な組立工程に不可欠であり、最大の生産性を確保します。

AI主導のアナリティクス、マシンコミュニケーション、クラウドコンピューティングを統合するインダストリー4.0構想は、高度なPLCへの大きな需要を促進しています。これらのシステムはリアルタイムのデータ処理とシームレスな接続性を促進し、スマート製造に不可欠なものとなっています。デジタルツインテクノロジーとPLCベースのシステムを統合することで、メーカーは物理的なオペレーションを中断することなく、性能をテストし最適化するための仮想モデルを作成することができます。予知保全と効率改善のためにデジタルツインを採用する企業が増えているため、PLCメーカーはこうした進歩に対応するソリューションの開発に注力しています。さまざまな産業でインテリジェントオートメーションへのニーズが高まっているため、PLCの需要が持続し、現代の産業エコシステムに不可欠なコンポーネントとして位置づけられています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 117億米ドル |

| 予測金額 | 314億米ドル |

| CAGR | 10.4% |

市場はタイプ別にモジュール型PLC、コンパクトPLC、ラックマウント型PLCに区分されます。なかでもモジュール型PLCは、予測期間中にCAGR 11.1%を記録し、最も高い成長が見込まれます。これらのPLCは優れた拡張性と柔軟性を備えているため、製造、エネルギー、水処理、食品加工などの業界で好んで選ばれています。システム全体を中断させることなく故障したモジュールを交換できるため、ダウンタイムを最小限に抑えることができ、普及の原動力となっています。

市場は最終用途別に、航空宇宙・防衛、自動車、化学、エネルギー・公益、食品・飲料、ヘルスケア、製造、鉱業・金属、石油・ガス、運輸に分けられます。スマート工場や自動化生産ラインへのPLC導入が増加していることから、2024年の市場シェアは製造業が全体の20.9%以上を占めました。最新のPLCシステムは、リアルタイムのデータ処理、予知保全、適応型自動化によって効率を高め、産業の進歩に不可欠なものとなっています。

市場はまた、コンポーネント別にソフトウェア、ハードウェア、サービスに分類されます。ソフトウェア・セグメントは、急速なインダストリー4.0の採用とIoT統合によって、2024年に41億米ドルを占める。ソフトウェアベースのPLCは、リアルタイムのモニタリング、予測分析、プロセスの最適化をサポートし、産業界の効率向上と操作ミスの最小化を支援します。システムのダウンタイムを減らし、生産プロセスを合理化するPLCの役割は、スマート製造が勢いを増すにつれて拡大し続けています。

地域別では、北米が2024年の世界PLC市場で34.4%のシェアを占め、スマートインフラと自動化技術への投資増がその要因となっています。米国はこの地域市場をリードし、2024年には31億米ドルを生み出し、CAGR 10.8%で成長すると予測されています。インダストリー4.0イニシアチブの拡大とEV生産への注目の高まりが、この地域でのPLC採用を促進する主な要因です。

目次

第1章 調査手法と調査範囲

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- 業界への影響要因

- 促進要因

- インダストリー4.0とデジタルツイン構想の採用

- 業界全体における自動化需要の高まり

- 産業用ロボットに対する需要の高まり

- 老朽化したインフラのアップグレード

- 電気自動車(EV)産業の台頭

- 促進要因

- 業界の潜在的リスク&課題

- 高い投資コスト

- サイバーセキュリティ攻撃の脅威

- 規制状況

- 技術情勢

- 今後の市場動向

- ギャップ分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業シェア分析

- 主要市場プレーヤーの競合分析

- 競合のポジショニングマトリックス

- 戦略ダッシュボード

第5章 市場推計・予測:タイプ別、2021年~2034年

- 主要動向

- モジュラー

- コンパクト

- ラックマウント

第6章 市場推計・予測:コンポーネント別、2021年~2034年

- 主要動向

- ハードウェア

- 中央処理装置(CPU)

- メモリーモジュール

- 入力モジュール

- 出力モジュール

- 通信モジュール

- 電源ユニット

- ヒューマン・マシン・インターフェース(HMI)

- その他

- ソフトウェア

- サービス

第7章 市場推計・予測:最終用途別、2021年~2034年

- 主要動向

- 航空宇宙・防衛

- 自動車

- 化学

- エネルギー・公益事業

- 飲食品

- ヘルスケア

- 製造業

- 鉱業・金属

- 石油・ガス

- 運輸

- その他

第8章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

第9章 企業プロファイル

- ABB

- Bosch Rexroth

- Delta Electronics

- Eaton

- General Electric

- Honeywell International

- Keyence

- Mitsubishi Electric

- Omron

- Panasonic

- Phoenix Contact

- Rockwell Automation

- Schneider Electric

- Siemens

- Yokogawa Electric

The Global Programmable Logic Controller Market was valued at USD 11.7 billion in 2024 and is projected to grow at a CAGR of 10.4% from 2025 to 2034. The increasing adoption of Industry 4.0, digital twin technology, and automation-driven solutions is fueling market expansion. The rising demand for electric vehicles (EVs) is further accelerating growth, as PLC-based systems play a critical role in automating production lines and optimizing manufacturing efficiency. Automakers rely on PLC-driven solutions to streamline EV production, enhance scalability, and reduce downtime. Additionally, these systems are essential for battery manufacturing and complex assembly processes, ensuring maximum productivity.

Industry 4.0 initiatives, which integrate AI-driven analytics, machine communication, and cloud computing, are driving significant demand for advanced PLCs. These systems facilitate real-time data processing and seamless connectivity, making them indispensable for smart manufacturing. The integration of digital twin technology with PLC-based systems enables manufacturers to create virtual models for testing and optimizing performance without disrupting physical operations. As companies increasingly adopt digital twins for predictive maintenance and efficiency improvements, PLC manufacturers are focusing on developing solutions that align with these advancements. The growing need for intelligent automation across various industries ensures sustained demand for PLCs, positioning them as essential components of modern industrial ecosystems.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $11.7 Billion |

| Forecast Value | $31.4 Billion |

| CAGR | 10.4% |

The market is segmented based on type into modular, compact, and rack-mounted PLCs. Among these, modular PLCs are expected to witness the highest growth, registering a CAGR of 11.1% during the forecast period. These PLCs offer superior scalability and flexibility, making them a preferred choice across industries, including manufacturing, energy, water treatment, and food processing. Their ability to minimize downtime by enabling faulty module replacements without disrupting entire systems drives their widespread adoption.

By end-use, the market is divided into aerospace and defense, automotive, chemicals, energy and utilities, food and beverages, healthcare, manufacturing, mining and metals, oil and gas, and transportation. The manufacturing sector accounted for over 20.9% of the total market share in 2024, driven by the increasing deployment of PLCs in smart factories and automated production lines. Modern PLC systems enhance efficiency through real-time data processing, predictive maintenance, and adaptive automation, making them integral to industrial advancements.

The market is also categorized by component into software, hardware, and services. The software segment accounted for USD 4.1 billion in 2024, driven by rapid Industry 4.0 adoption and IoT integration. Software-based PLCs support real-time monitoring, predictive analytics, and process optimization, helping industries improve efficiency and minimize operational errors. Their role in reducing system downtime and streamlining production processes continues to expand as smart manufacturing gains momentum.

Geographically, North America held a 34.4% share of the global PLC market in 2024, fueled by increased investments in smart infrastructure and automation technologies. The U.S. led the regional market, generating USD 3.1 billion in 2024, and is projected to grow at a CAGR of 10.8%. The expansion of Industry 4.0 initiatives and the rising focus on EV production are key factors driving PLC adoption in the region.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Adoption of industry 4.0 and digital twin initiatives

- 3.2.1.2 Growing demand for automation across industries

- 3.2.1.3 Rising demand for Industrial robotics

- 3.2.1.4 Upgradation of aging infrastructure

- 3.2.1.5 The rise of electric vehicles (EV) industry

- 3.2.1 Growth drivers

- 3.3 Industry pitfalls and challenges

- 3.3.1.1 High investment costs

- 3.3.1.2 Threats of cybersecurity attacks

- 3.4 Regulatory landscape

- 3.5 Technology landscape

- 3.6 Future market trends

- 3.7 Gap analysis

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Type, 2021 – 2034 (USD Bn & Units)

- 5.1 Key trends

- 5.2 Modular

- 5.3 Compact

- 5.4 Rack mounted

Chapter 6 Market Estimates and Forecast, By Component, 2021 – 2034 (USD Bn & Units)

- 6.1 Key trends

- 6.2 Hardware

- 6.2.1 Central Processing Unit (CPU)

- 6.2.2 Memory modules

- 6.2.3 Input modules

- 6.2.4 Output modules

- 6.2.5 Communication modules

- 6.2.6 Power supply unit

- 6.2.7 Human Machine Interface (HMI)

- 6.2.8 Others

- 6.3 Software

- 6.4 Services

Chapter 7 Market Estimates and Forecast, By End Use, 2021 – 2034 (USD Bn & Units)

- 7.1 Key trends

- 7.2 Aerospace & defence

- 7.3 Automotive

- 7.4 Chemical

- 7.5 Energy & utilities

- 7.6 Food & beverages

- 7.7 Healthcare

- 7.8 Manufacturing

- 7.9 Mining & metal

- 7.10 Oil & gas

- 7.11 Transportation

- 7.12 Others

Chapter 8 Market Estimates and Forecast, By Region, 2021 – 2034 (USD Bn & Units)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 ABB

- 9.2 Bosch Rexroth

- 9.3 Delta Electronics

- 9.4 Eaton

- 9.5 General Electric

- 9.6 Honeywell International

- 9.7 Keyence

- 9.8 Mitsubishi Electric

- 9.9 Omron

- 9.10 Panasonic

- 9.11 Phoenix Contact

- 9.12 Rockwell Automation

- 9.13 Schneider Electric

- 9.14 Siemens

- 9.15 Yokogawa Electric