海底ケーブルシステム市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測

Submarine Cable Systems Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025-2034- 発行日

- ページ情報

- 英文 100 Pages

- 納期

- 2~3営業日

- 商品コード

- 1699237

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

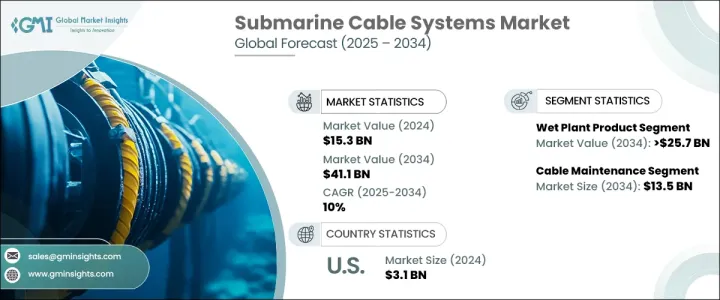

世界の海底ケーブルシステム市場は、2024年に153億米ドルと評価され、2025年から2034年にかけてCAGR 10%で拡大すると予想されています。

この成長の主な要因は、新興国における工業化の進展と高度な配線およびケーブルネットワークに対する需要の高まりです。インフラ開発が加速するにつれ、堅牢な電気接続ソリューションのニーズは高まり続け、海底ケーブルシステムへの投資に拍車をかけています。

世界各国政府は、環境問題の高まりと従来型資源の枯渇を理由に、再生可能エネルギー発電に積極的に舵を切っています。相互接続プロジェクトの増加は、効率的なエネルギー・トランスミッションを保証する海底ケーブル・システムの需要増加に寄与しています。さらに、帯域幅容量と光ファイバーケーブルの耐久性の継続的な進歩により、これらのシステムの信頼性とコスト効率が高まっています。業界各社は、データ伝送効率を高めるため、大容量マルチファイバー海底ケーブルなどの革新的なソリューションを導入しています。こうした開発は市場開拓を大きく後押しし、さらなる投資と技術改良を促しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 153億米ドル |

| 予測金額 | 411億米ドル |

| CAGR | 10% |

ウェットプラント製品分野は、再生可能エネルギーに対する世界の関心の高まりに支えられ、2034年までに257億米ドルを超える見通しです。再生可能エネルギーの普及に伴い、効率的な水中トランスミッション・ネットワークの必要性が高まっています。持続可能性への強い後押しにより、政府や企業は洋上風力発電所やエネルギーグリッドの相互接続への投資を強化しており、海底ケーブルの需要も強まっています。

ケーブル敷設サービス分野は、2034年までのCAGRが8.5%を超えると予想されています。この増加傾向は、エネルギー需要の急増、産業の拡大、さまざまな地域で起こっている急速な都市化に起因しています。産業が近代化し、都市が成長するにつれ、シームレスな接続性へのニーズが海底ケーブル配備への投資を後押ししています。こうした海底ネットワークの信頼性と長寿命を確保する上で、効率的な敷設サービスが重要な役割を果たしています。

米国では、海底ケーブルシステム市場は安定した成長を遂げています。2022年の市場規模は28億米ドル、2023年には29億米ドル、2024年には31億米ドルとなりました。都市化と工業化の進展が高性能海底ケーブルの需要を押し上げ、シームレスなデータとエネルギーのトランスミッションを可能にしています。これらのシステムへの依存度が高まっていることは、将来の拡大が堅調であることを示しており、海底ケーブル・インフラの主要市場としての同地域の地位を強化しています。

技術の進歩によりケーブルの性能と効率が向上し続けているため、海底ケーブル・システム市場は今後数年間で力強い成長を遂げると思われます。最先端の光ファイバーの統合、帯域幅能力の向上、進化するエネルギー・トランスミッションの要件が、業界の軌跡を総合的に形成しており、世界のインフラ整備の重要な要素となっています。

目次

第1章 調査手法と調査範囲

- 市場の定義

- 基本推定と計算

- 予測計算

- データソース

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- 規制状況

- 業界への影響要因

- 促進要因

- 業界の潜在的リスク&課題

- 成長ポテンシャル分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- 戦略ダッシュボード

- イノベーションと持続可能性の展望

第5章 市場規模・予測:コンポーネント別、2021年~2034年

- 主要動向

- ドライプラント製品

- ウェットプラント製品

第6章 市場規模・予測:オファリング別、2021年~2034年

- 主要動向

- ケーブル敷設サービス

- ケーブル保守・修理サービス

- アップグレードサービス

第7章 市場規模・予測:展開別、2021年~2034年

- 主要動向

- 浅海

- 深海

第8章 市場規模・予測:アプリケーション別2021年~2034年

- 主要動向

- 海底電力ケーブル

- 海底通信ケーブル

第9章 市場規模・予測:最終用途別、2021年~2034年

- 主要動向

- 洋上風力発電

- 国間・島間接続

- 海洋石油・ガス

第10章 市場規模・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- ロシア

- アジア太平洋

- 中国

- 日本

- インド

- 韓国

- オーストラリア

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- 南アフリカ

- ラテンアメリカ

- ブラジル

- アルゼンチン

第11章 企業プロファイル

- Alcatel-Lucent Submarine Networks(ASN)

- Corning Incorporated

- Fujitsu Limited

- Global Marine Systems

- Gulf Bridge International(GBI)

- Hengtong Marine Cable Systems

- NEC Corporation

- Nexans

- Orange Marine

- Prysmian

- SEACOM

目次

The Global Submarine Cable Systems Market was valued at USD 15.3 billion in 2024 and is expected to expand at a CAGR of 10% from 2025 to 2034. This growth is primarily driven by increasing industrialization and the rising demand for advanced wiring and cable networks in emerging economies. As infrastructure development accelerates, the need for robust electrical connectivity solutions continues to grow, fueling investments in submarine cable systems.

Governments worldwide are actively shifting their focus toward renewable energy generation due to rising environmental concerns and the depletion of conventional resources. The increasing number of interconnection projects is contributing to the rising demand for submarine cable systems, ensuring efficient energy transmission. Additionally, continuous advancements in bandwidth capacity and the durability of fiber optic cables are making these systems more reliable and cost-effective. Industry players are introducing innovative solutions, such as high-capacity multi-fiber submarine cables, to enhance data transmission efficiency. These developments are significantly boosting market expansion, thus encouraging further investments and technological improvements.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $15.3 Billion |

| Forecast Value | $41.1 Billion |

| CAGR | 10% |

The wet plant product segment is poised to exceed USD 25.7 billion by 2034, supported by the growing global emphasis on renewable energy. As renewable energy sources gain traction, the need for efficient underwater transmission networks is increasing. With a strong push toward sustainability, governments and enterprises are ramping up investments in offshore wind farms and energy grid interconnections, which in turn is strengthening the demand for submarine cables.

The cable installation services segment is expected to witness a CAGR of over 8.5% through 2034. This upward trend is attributed to surging energy demand, industrial expansion, and the rapid urbanization taking place across various regions. As industries modernize and cities grow, the need for seamless connectivity is propelling investments in submarine cable deployment. Efficient installation services play a crucial role in ensuring the reliability and longevity of these underwater networks.

In the United States, the submarine cable systems market has been experiencing steady growth. The market was valued at USD 2.8 billion in 2022, USD 2.9 billion in 2023, and USD 3.1 billion in 2024. The increasing pace of urbanization and industrialization is driving the demand for high-performance submarine cables, enabling seamless data and energy transmission. The growing reliance on these systems indicates strong future expansion, reinforcing the region's position as a key market for submarine cable infrastructure.

As technological advancements continue to refine cable performance and efficiency, the submarine cable systems market is set to experience robust growth in the coming years. The integration of cutting-edge fiber optics, enhanced bandwidth capabilities, and evolving energy transmission requirements are collectively shaping the industry's trajectory, making it a crucial component of global infrastructure development.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid

- 1.4.2.2 Public

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

Chapter 4 Competitive landscape, 2024

- 4.1 Strategic dashboard

- 4.2 Innovation & sustainability landscape

Chapter 5 Market Size and Forecast, By Component, 2021 – 2034 (USD Million)

- 5.1 Key trends

- 5.2 Dry plant product

- 5.3 Wet plant product

Chapter 6 Market Size and Forecast, By Offering 2021 – 2034 (USD Million)

- 6.1 Key trends

- 6.2 Cable installation services

- 6.3 Cable maintenance and repair services

- 6.4 Upgradate services

Chapter 7 Market Size and Forecast, By Deployment 2021 – 2034 (USD Million)

- 7.1 Key trends

- 7.2 Shallow water

- 7.3 Deep water

Chapter 8 Market Size and Forecast, By Application 2021 – 2034 (USD Million)

- 8.1 Key trends

- 8.2 Submarine power cables

- 8.3 Submarine communication cables

Chapter 9 Market Size and Forecast, By End Use 2021 – 2034 (USD Million)

- 9.1 Key trends

- 9.2 Offshore wind power generation

- 9.3 Inter country & island connection

- 9.4 Offshore oil & gas

Chapter 10 Market Size and Forecast, By Region, 2021 – 2034 (USD Million)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Russia

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 Japan

- 10.4.3 India

- 10.4.4 South Korea

- 10.4.5 Australia

- 10.5 Middle East & Africa

- 10.5.1 Saudi Arabia

- 10.5.2 UAE

- 10.5.3 South Africa

- 10.6 Latin America

- 10.6.1 Brazil

- 10.6.2 Argentina

Chapter 11 Company Profiles

- 11.1 Alcatel-Lucent Submarine Networks (ASN)

- 11.2 Corning Incorporated

- 11.3 Fujitsu Limited

- 11.4 Global Marine Systems

- 11.5 Gulf Bridge International (GBI)

- 11.6 Hengtong Marine Cable Systems

- 11.7 NEC Corporation

- 11.8 Nexans

- 11.9 Orange Marine

- 11.10 Prysmian

- 11.11 SEACOM

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 100 Pages

- 納期

- 2~3営業日