|

市場調査レポート

商品コード

1892850

自動車物流市場の機会、成長要因、業界動向分析、および2026年から2035年までの予測Automotive Logistics Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

カスタマイズ可能

|

|||||||

| 自動車物流市場の機会、成長要因、業界動向分析、および2026年から2035年までの予測 |

|

出版日: 2025年12月09日

発行: Global Market Insights Inc.

ページ情報: 英文 235 Pages

納期: 2~3営業日

|

概要

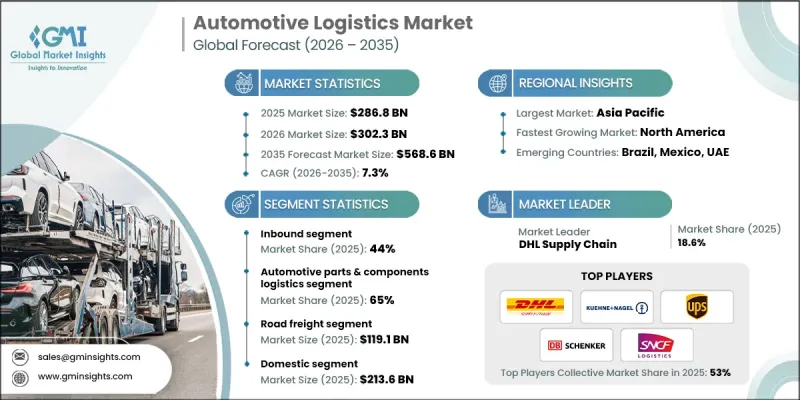

世界の自動車物流市場は、2025年に2,868億米ドルと評価され、2035年までにCAGR7.3%で成長し、5,686億米ドルに達すると予測されています。

拡大を続ける自動車産業では、サプライチェーン全体で車両や部品、コンポーネントを輸送するための効率的な物流ソリューションの必要性が高まっています。企業は、輸送ルートの最適化、在庫管理、リアルタイムの出荷追跡を可能にするソフトウェアの重要性を認識しています。多くの自動車メーカーは、物流管理において依然として旧式のソフトウェアやレガシーシステムに依存しており、これが現代的なソリューションの統合を困難にしています。そのため、大規模なデータ移行やカスタマイズが必要となります。エンドツーエンドのサプライチェーンにおけるリアルタイム可視性の不足、複雑な輸送ネットワーク、パートナー間のデータ透明性のばらつきが、さらなる障壁となっています。これらの課題に対処するため、ソフトウェアプロバイダーはAIと機械学習を組み込み、ルート計画の改善、反復作業の自動化、意思決定の強化を図っています。予測分析と需要予測機能により、企業は将来の需要を予測し、在庫を最適化し、リソースをより効率的に配分できるようになり、サプライチェーンの混乱に対する先制的な解決策が可能となります。

| 市場範囲 | |

|---|---|

| 開始年 | 2025年 |

| 予測年度 | 2026-2035 |

| 開始時価値 | 2,868億米ドル |

| 予測金額 | 5,686億米ドル |

| CAGR | 7.3% |

インバウンド物流セグメントは2025年に44%のシェアを占め、2026年から2035年にかけてCAGR 8%で成長すると予測されています。インバウンド物流は、原材料、部品、サブアセンブリをサプライヤーからOEM組立工場へ効率的に輸送する役割を担い、自動車物流市場において極めて重要な位置を占めています。その高頻度・大量輸送オペレーションは、ジャストインタイム(JIT)およびジャストインシーケンス(JIS)生産を支援し、在庫保有コストを削減しながら、円滑な生産フローを確保します。道路、鉄道、航空、海上を含むマルチモーダル輸送の活用は、インバウンドサプライチェーンの速度、信頼性、コスト効率をさらに向上させます。

自動車部品・コンポーネント物流セグメントは、2025年に65%のシェアを占め、2026年から2035年にかけてCAGR 7.6%で成長すると予測されています。このセグメントが支配的な理由は、OEM(自動車メーカー)およびティア1・ティア2サプライヤーネットワーク間における部品移動の複雑さ、量、頻度にあります。これにより、部品が組立工場、地域流通センター、アフターマーケットサービスネットワークへ安全かつ時間通りに、かつコスト効率良く配送され、生産と運営の円滑な維持が保証されます。

中国自動車物流市場は2025年に432億米ドルを生み出し、39%のシェアを占めました。中国の優位性は、自動車生産の急成長、乗用車・商用車への強い需要、先進物流技術への大規模投資によって推進されています。同地域は、発達した輸送ネットワーク、広範な倉庫・流通インフラ、デジタルサプライチェーンソリューション、IoTベースの追跡システム、自動化資材搬送システムの普及拡大といった利点を有しています。

よくあるご質問

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 利益率

- コスト構造

- 各段階における付加価値

- バリューチェーンに影響を与える要因

- ディスラプション

- 業界への影響要因

- 促進要因

- 世界の自動車生産の増加とアフターマーケットの拡大

- デジタル・インテリジェント物流技術の採用

- 電気自動車製造およびバッテリー物流の成長

- 世界化されたサプライチェーンと越境貿易の拡大

- 業界の潜在的リスク&課題

- サプライチェーンの混乱と生産能力のボトルネック

- 高い運用コストとEV部品の取り扱いの複雑さ

- 市場機会

- 持続可能で環境に配慮した物流への需要の高まり

- アフターマーケットにおける電子商取引流通の急速な成長

- 先進技術の統合

- 新興市場における事業拡大

- 促進要因

- 成長可能性分析

- 規制情勢

- 北米

- FMCSA、NHTSA、EPA排出ガス基準

- カナダ運輸省安全規制

- 欧州

- ドイツEU自動車安全規制、TUV認証

- フランス国立科学研究センター(CNRS)排出ガス及び安全基準

- 英国DVSA車両安全・適合性

- イタリア運輸省車両規制

- アジア太平洋地域

- 中国交通運輸省安全規則、NEV政策

- 日本自動車工業会(JAMA)車両安全規制、排出ガス基準

- 韓国産業通商資源省(MOTIE)安全・環境コンプライアンス

- インド自動車産業規格(AIS)

- ラテンアメリカ

- CONTRAN車両安全・排出ガス規制

- NOM自動車安全基準

- 中東・アフリカ

- アラブ首長国連邦標準化・計量庁車両規制

- SASO車両安全・環境基準

- 北米

- ポーター分析

- PESTEL分析

- 技術とイノベーションの動向

- 現在の技術動向

- 新興技術

- 価格動向

- 地域別

- 製品別

- コスト内訳分析

- 特許分析

- 持続可能性と環境面

- 持続可能な取り組み

- 廃棄物削減戦略

- 生産におけるエネルギー効率

- 環境に配慮した取り組み

- カーボンフットプリントに関する考慮事項

- ユースケースシナリオ

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 戦略的展望マトリックス

- 主な発展

- 合併・買収

- 提携・協業

- 新製品の発売

- 事業拡大計画と資金調達

第5章 市場推計・予測:サービス別、2022-2035

- 主要動向

- インバウンド・ロジスティクス

- アウトバウンド

- 逆

- アフターマーケット

第6章 市場推計・予測:製品別、2022-2035

- 主要動向

- 完成車

- 乗用車

- ハッチバック

- セダン

- SUV

- 商用車

- 小型車

- 中型

- 大型車両

- 乗用車

- 自動車部品・コンポーネント

- 車輪およびタイヤ

- 電気・電子機器

- ボディおよびシャーシ

- サスペンションおよびステアリング

- ブレーキシステム

- エンジンおよびパワートレイン

第7章 市場推計・予測:輸送手段別、2022-2035

- 主要動向

- 道路貨物輸送

- 海上輸送

- 航空貨物

- 鉄道貨物輸送

第8章 市場推計・予測:流通別、2022-2035

- 主要動向

- 国内

- 国際

第9章 市場推計・予測:地域別、2022-2035

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ベルギー

- オランダ

- スウェーデン

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- シンガポール

- 韓国

- ベトナム

- インドネシア

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ地域

- アラブ首長国連邦

- 南アフリカ

- サウジアラビア

第10章 企業プロファイル

- Global Player

- C.H. Robinson Worldwide

- CEVA Logistics

- DHL Supply Chain &Global Forwarding

- DSV-Schenker

- Expeditors International of Washington

- GEODIS(SNCF)

- Hellmann Worldwide Logistics

- Kuehne+Nagel International

- Penske Logistics

- XPO Logistics

- Regional Player

- BLG Logistics

- Hyundai Glovis

- Kintetsu World Express

- Mosolf

- Nippon Express

- Schnellecke Logistics

- Toll

- Yusen Logistics

- 新興企業

- Flexport

- FourKites

- Hodlmayr International

- project44

- Uber Freight