|

市場調査レポート

商品コード

1928944

データセンター液体冷却市場の機会、成長要因、業界動向分析、および2026年から2035年までの予測Data Center Liquid Cooling Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

カスタマイズ可能

|

|||||||

| データセンター液体冷却市場の機会、成長要因、業界動向分析、および2026年から2035年までの予測 |

|

出版日: 2026年01月12日

発行: Global Market Insights Inc.

ページ情報: 英文 215 Pages

納期: 2~3営業日

|

概要

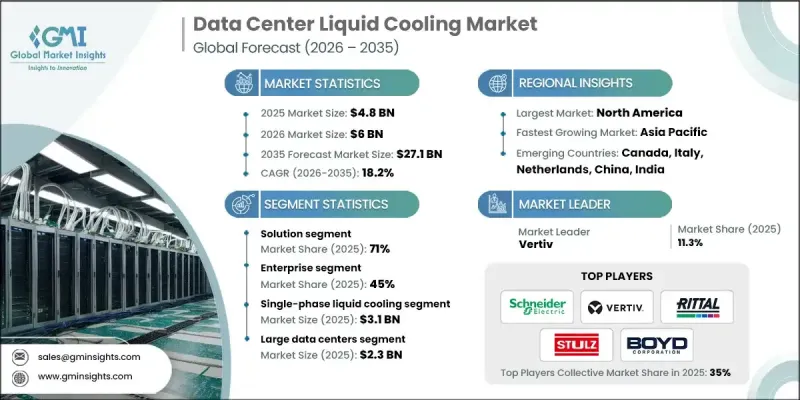

世界のデータセンター向け液体冷却市場は、2025年に48億米ドルと評価され、2035年までにCAGR 18.2%で成長し、271億米ドルに達すると予測されております。

エネルギーコストの上昇に加え、厳格な持続可能性要件が相まって、データセンター全体で液体冷却技術の採用が加速しています。液体冷却システムは、従来の空冷施設における1.4~1.8と比較して、1.05~1.15という大幅に低い電力使用効率(PUE)比率を実現し、電力消費を直接削減するとともに、二酸化炭素排出量を低減します。EUエネルギー効率指令、2027年までにPUE1.3を目標とするドイツのエネルギー効率法、カリフォルニア州のエネルギー効率基準などの規制要件が、事業者に対し先進的な冷却ソリューションの導入を促しています。さらに、廃熱を地域暖房や工業プロセスに回収する液体冷却システムの能力は、データセンターを循環型エネルギー経済への貢献者へと変革し、企業のネットゼロ目標達成を支援するとともに、運営の持続可能性を高めます。北米は、ハイパースケールクラウド事業者、半導体メーカー、高密度AI・HPCインフラを導入するシステムインテグレーターが密集していることを背景に、データセンター液体冷却市場を牽引し続けております。

| 市場範囲 | |

|---|---|

| 開始年 | 2025年 |

| 予測年度 | 2026-2035 |

| 開始時価値 | 48億米ドル |

| 予測金額 | 271億米ドル |

| CAGR | 18.2% |

ソリューションセグメントは2025年に71%のシェアを占め、2026年から2035年にかけてCAGR15%で成長すると予測されています。ダイレクト・トゥ・チップ冷却は最も成長が著しい技術であり、プロセッサ、GPU、メモリに直接取り付けられたコールドプレートやマイクロチャネルクーラーを用いて、熱の60~80%を大気中に入る前に除去します。これらのシステムは、抑制剤やグリコール混合物を含む水などの冷却剤をチップ表面全体に循環させ、0.01~0.05°C/Wという低い熱抵抗を実現します。

単相液体冷却システム市場は2025年に31億米ドルに達しました。これらのシステムはサイクル全体で冷却剤を液相に保ち、相変化なしに伝導・対流による熱伝達を行います。冷却剤は設計に応じて18~50℃でコールドプレート、液浸タンク、または熱交換器を循環し、施設用チラー、ドライクーラー、または冷却塔がループから熱を除去します。

米国データセンター向け液体冷却市場は2025年に12億9,000万米ドル規模に達しました。公共部門データセンターにおける液体冷却導入の主要な促進要因としては、AIおよびHPCプログラムを含む連邦政府の取り組み、CHIPS法に基づく半導体資金援助、ならびにAIを組み込んだ防衛近代化プロジェクトが挙げられます。

よくあるご質問

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- コンポーネントサプライヤー

- 製造業者

- システムインテグレーター

- 配管経路分析

- クラウドサービスプロバイダー様

- エンドユーザー

- コスト構造

- 利益率

- 各段階における付加価値

- サプライチェーンに影響を与える要因

- ディスラプター

- サプライヤーの情勢

- 影響要因

- 促進要因

- AIおよびハイパフォーマンスコンピューティングワークロードの急激な増加

- エネルギーコストの上昇と持続可能性への要請

- ハイパースケールおよびコロケーションデータセンターインフラの拡張

- エッジコンピューティングと分散型アーキテクチャの普及

- 業界の潜在的リスク&課題

- 初期投資額が高く、複雑さが伴います

- 技術的リスクと運用上の懸念事項

- 市場機会

- 既存データセンター施設の改修および近代化

- ハイブリッド冷却アーキテクチャの開発

- 冷却サービスとしての提供(Cooling-as-a-Service)および管理サービスモデルの市場における台頭

- 促進要因

- 成長可能性分析

- 規制情勢

- 北米

- 米国エネルギー政策法(PUE基準)

- カリフォルニア州タイトル24エネルギー効率規制

- NERC重要インフラ保護(冷却信頼性)

- 欧州

- EUエネルギー効率指令(EED)

- ドイツ省エネルギー法(PUE<=1.3)

- 英国エネルギー関連製品政策枠組み

- 気候中立データセンター協定

- フランスデータセンターエネルギー報告法令

- アジア太平洋地域

- 中国GB 50174 PUE基準(1.3以下が義務付け)

- インドデジタル・インディア効率ガイドライン

- シンガポール・グリーンデータセンター・ロードマップ

- 日本地震冷却基準

- オーストラリアデータセンターエネルギー規制

- ラテンアメリカ

- ブラジルANATELエネルギー効率基準

- メキシコデータセンター持続可能性ガイドライン

- チリにおけるグリーンデータセンターの優遇措置

- 中東・アフリカ

- UAEグリーンアジェンダ2030

- サウジアラビアビジョンデータ効率性2030

- 南アフリカ重要インフラ規制

- 北米

- ポーター氏の分析

- PESTEL分析

- 技術とイノベーションの展望

- 現在の技術動向

- 新興技術

- コスト内訳分析

- ラック密度階層別冷却kWあたりのコスト

- 新規導入と改修のコスト差

- 総所有コスト(TCO)

- 特許分析

- 事例研究

- 持続可能性と環境面

- 持続可能な実践

- 廃棄物削減戦略

- 生産におけるエネルギー効率

- 環境に配慮した取り組み

- カーボンフットプリントに関する考慮事項

- アーキテクチャ分析

- ダイレクト・トゥ・チップ液体冷却

- 液浸冷却

- 空冷から液冷への移行分析

- データセンターの電力密度動向

- 高性能コンピューティングに対する需要の増加

- エッジコンピューティングの加速

- 先進冷却技術

- スペースの最適化

- カスタマイズされたワークロードソリューション

- 関係構築とパートナーシップの強化

- 戦略的統合パートナーシップモデル

- 共同エンジニアリングサービス

- 統合基準の共同開発

- ハイパースケールデータセンタープロジェクトへの共同入札

- パイロット導入における協業の機会

- ハイパースケーラーとの実証プロジェクト

- 企業向け改修における戦略的導入

- 戦略的統合パートナーシップモデル

- 既存インフラとの統合及び効率最適化

- 統合戦略

- 改修の道筋

- 既存冷水システムを用いたダイレクト・トゥ・チップ実装

- リアドア熱交換器のドロップイン改造

- 浸漬ポッドのモジュラー追加

- ハイブリッド統合

- 空冷+液冷ゾーン

- 部分ラック液体補助(GPUラック)

- 新規導入環境への適応

- キャンパスの一部である場合、既存システムとの統合設計

- 隔離型液体冷却用二次ループ

- 効率最適化手法

- 熱効率

- ラックレベルでの熱除去最適化

- ホット/コールドアイル封じ込めシステムの統合

- 再循環およびバイパス気流の最小化

- 統合戦略

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 北米

- 欧州

- アジア太平洋地域

- LATAM

- 中東・アフリカ地域

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 戦略的展望マトリックス

- 主な発展

- 合併・買収

- 提携・協業

- 新製品の発売

- 拡張計画と資金調達

- 統合・改修のベンチマーク

- 既存ラックへの液体冷却導入までの所要時間

- 改修時のダウンタイム影響

- 既存のCRAH/CRACまたはインローユニットとの互換性

- 運用複雑性のスケーリング

第5章 市場推計・予測:コンポーネント別、2022-2035

- ソリューション

- ダイレクト・トゥ・チップ

- コールドプレート

- マイクロチャネルクーラー

- 没入型

- ITシャーシ

- 浴槽/オープンバス

- リアドア熱交換器

- アクティブ(ポンプ駆動式)

- 受動部品

- ダイレクト・トゥ・チップ

- サービス

- マネージドサービス

- 遠隔監視

- パフォーマンス最適化

- 保守・サポートサービス

- 専門サービス

- コンサルティング及び設計

- 設置および導入

- マネージドサービス

第6章 市場推計・予測:冷却機構別、2022-2035

- 単相液体冷却

- 二相液体冷却

第7章 市場推計・予測:冷却剤別、2022-2035

- 水系冷却剤

- 誘電体流体

- 合成流体

- 鉱物油

- バイオベース/天然系冷却剤

第8章 市場推計・予測:データセンター別、2022-2035

- 小規模データセンター

- 中規模データセンター

- 大規模データセンター

第9章 市場推計・予測:用途別、2022-2035

- サーバー冷却

- CPU冷却

- GPU/AIアクセラレータの冷却

- ストレージ冷却

- ネットワーク冷却

- その他

第10章 市場推計・予測:最終用途別、2022-2035

- 企業向け

- BFSI

- 小売業および電子商取引

- 政府

- ヘルスケア

- 製造業

- IT関連サービス(ITeS)

- その他

- 通信サービスプロバイダー

- クラウドサービスプロバイダー

第11章 市場推計・予測:地域別、2022-2035

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- ポーランド

- ベネルクス

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- 東南アジア

- ラテンアメリカ

- ブラジル

- コロンビア

- アルゼンチン

- チリ

- 中東・アフリカ地域

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第12章 企業プロファイル

- Global leaders

- Alfa Laval

- Asetek

- Boyd

- CoolIT Systems

- Green Revolution Cooling(GRC)

- LiquidStack

- Rittal

- Schneider Electric

- Stulz

- Vertiv

- 地域プレイヤー

- Asperitas

- DCX Liquid Cooling Systems

- Delta Electronics

- DUG Technology

- Iceotope Technologies

- Kaori Heat Treatment

- Submer Technologies

- 新興企業

- Accelsius

- Chilldyne

- JETCOOL Technologies

- LiquidCool Solutions

- Midas Green Technologies

- Seguente

- ZutaCore