|

市場調査レポート

商品コード

1929001

スタティック・ランダムアクセスメモリ(SRAM)市場の機会、成長要因、業界動向分析、および2026年から2035年までの予測Static Random-Access Memory (SRAM) Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

カスタマイズ可能

|

|||||||

| スタティック・ランダムアクセスメモリ(SRAM)市場の機会、成長要因、業界動向分析、および2026年から2035年までの予測 |

|

出版日: 2026年01月15日

発行: Global Market Insights Inc.

ページ情報: 英文 160 Pages

納期: 2~3営業日

|

概要

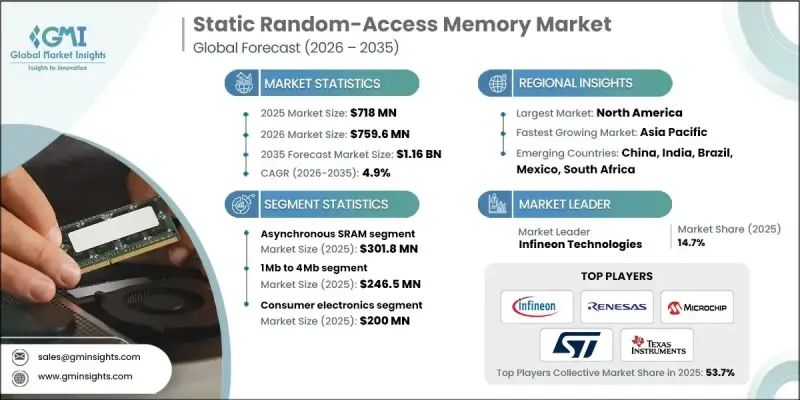

世界のスタティックランダムアクセスメモリ(SRAM)市場は、2025年に7億1,800万米ドルと評価され、2035年までにCAGR 4.9%で成長し、11億6,000万米ドルに達すると予測されております。

市場拡大の背景には、高度な電子システム全体で高速性、最小限のレイテンシ、信頼性の高い性能を提供するメモリソリューションへの需要増加があります。次世代半導体設計におけるSRAMの統合増加、およびコンピューティング、ネットワーキング、自動車エレクトロニクス分野における応用範囲の拡大が、長期的な成長を後押ししています。半導体製造技術の継続的な進歩は、SRAM製品の高密度化と効率向上を支えています。データ集約型デジタルインフラへの投資拡大も採用を加速させています。SRAMは高速なデータアクセスと処理を保証する上で重要な役割を果たすためです。現代のアプリケーションがより大量のデータを生成・処理し続ける中、高速かつ安定したオンチップメモリの重要性は高まっています。スタティック・ランダムアクセスメモリ(SRAM)は、電源供給中のみデータを保持する揮発性半導体メモリであり、他のメモリタイプと比較して高速なアクセス速度を実現します。システム設計者が速度、信頼性、低消費電力を優先する中、こうした性能上の優位性が需要を支えています。

| 市場範囲 | |

|---|---|

| 開始年 | 2025年 |

| 予測年度 | 2026-2035 |

| 開始時価値 | 7億1,800万米ドル |

| 予測金額 | 11億6,000万米ドル |

| CAGR | 4.9% |

非同期SRAMセグメントは2025年に3億180万米ドルの市場規模を生み出しました。このセグメントは、安定した動作、簡素化されたインターフェース設計、幅広い電子アーキテクチャとの互換性により、強固な地位を維持しています。実証済みの信頼性と統合の容易さは、複数のシステム設計における広範な利用を継続的に支えています。

16Mb以上のSRAMセグメントは、CAGR6.3%で成長し、2035年までに1億9,470万米ドルに達すると予測されています。このセグメントの成長は、データ処理の高速化と外部メモリ部品への依存度低減を実現するための、オンチップメモリ容量の増大する要求によって支えられています。

北米のスタティックランダムアクセスメモリ(SRAM)市場は、2025年に31.2%のシェアを占めました。地域の成長は、強力な半導体製造能力、先進的な技術インフラ、およびメモリ技術革新に焦点を当てた研究開発活動への持続的な投資によって支えられています。

よくあるご質問

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 利益率

- コスト構造

- 各段階における付加価値

- バリューチェーンに影響を与える要因

- ディスラプション

- 業界への影響要因

- 促進要因

- AIおよび機械学習アプリケーションの拡大

- エッジコンピューティングとIoTデバイスの普及

- プロセッサ向け高性能キャッシュメモリの需要増加

- 半導体技術とノード微細化の進展

- 自動車および5Gインフラ電子機器分野における成長

- 業界の潜在的リスク&課題

- 高い製造コストとスケーリングの限界

- 半導体サプライチェーンの変動性と原材料の入手可能性

- 市場機会

- AIアクセラレータおよび高性能コンピューティングにおけるSRAMの採用拡大

- 先進的なSoC設計における組み込みSRAMの統合拡大

- 促進要因

- 成長可能性分析

- 規制情勢

- ポーターの分析

- PESTEL分析

- 技術とイノベーションの動向

- 現在の技術動向

- 新興技術

- 価格動向

- 地域別

- 製品別

- 価格戦略

- 新興ビジネスモデル

- コンプライアンス要件

- 持続可能性対策

- 消費者心理分析

- 特許および知的財産分析

- 地政学的・貿易動向

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 地域別

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ

- 市場集中度分析

- 地域別

- 主要企業の競合ベンチマーキング

- 財務実績比較

- 収益

- 利益率

- 研究開発

- 製品ポートフォリオ比較

- 製品ラインの幅広さ

- 技術

- イノベーション

- 地域別事業展開比較

- 世界展開分析

- サービスネットワークカバレッジ

- 地域別市場浸透率

- 競合ポジショニングマトリックス

- リーダー企業

- 課題者

- フォロワー

- ニッチプレイヤー

- 戦略的展望マトリックス

- 財務実績比較

- 主な発展, 2021-2024

- 合併・買収

- 提携および協力関係

- 技術的進歩

- 拡大と投資戦略

- サステナビリティへの取り組み

- デジタルトランスフォーメーションの取り組み

- 新興/スタートアップ競合の動向

第5章 市場推計・予測:タイプ別、2022-2035

- 非同期SRAM

- 同期型SRAM

- その他

第6章 市場推計・予測:メモリサイズ別、2022-2035

- 1Mb以下

- 1Mb~4Mb

- 4Mb~16Mb

- 16Mb以上

第7章 市場推計・予測:最終用途産業別、2022-2035

- IT・通信

- 民生用電子機器

- 自動車

- 航空宇宙・防衛

- 産業用

- ヘルスケア

- その他

第8章 市場推計・予測:地域別、2022-2035

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- オランダ

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第9章 企業プロファイル

- Alliance Memory, Inc.

- Analog Devices, Inc.

- GSI Technology Inc.

- Infineon Technologies

- Integrated Silicon Solution Inc.(ISSI)

- Microchip Technology Inc.

- NXP Semiconductors

- ON Semiconductor

- Renesas Electronics Corporation

- Samsung Electronics Co., Ltd.

- STMicroelectronics NV

- Texas Instruments

- Toshiba Corporation

- Winbond Electronics Corporation