|

市場調査レポート

商品コード

1892901

産業用トラック市場の機会、成長要因、業界動向分析、および2026年から2035年までの予測Industrial Trucks Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

カスタマイズ可能

|

|||||||

| 産業用トラック市場の機会、成長要因、業界動向分析、および2026年から2035年までの予測 |

|

出版日: 2025年12月05日

発行: Global Market Insights Inc.

ページ情報: 英文 250 Pages

納期: 2~3営業日

|

概要

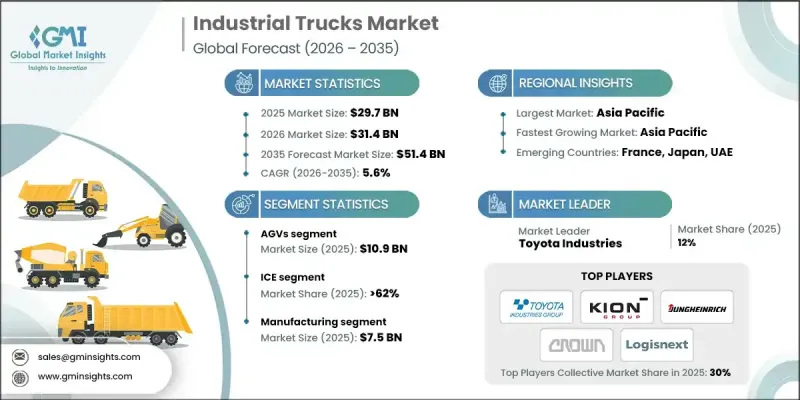

世界の産業用トラック市場は、2025年に297億米ドルと評価され、2035年までにCAGR5.6%で成長し、514億米ドルに達すると予測されています。

電子商取引の急速な拡大はサプライチェーンの再構築を継続的に促し、企業はより迅速かつ効率的な資材運搬ソリューションの導入を迫られています。オンライン注文量の増加に伴い、企業は迅速な配送ニーズに対応するため、大規模な流通拠点と小規模なフルフィルメント拠点への投資を進めています。こうした活動の高まりは、倉庫作業全体における商品の高速移動を支えるフォークリフト、パレットトラック、自律走行車両の需要を増加させています。組織が迅速な内部輸送と処理能力の向上を優先する中、産業用トラックは物流環境において重要な競争優位性となりつつあります。ロボット工学、センサーベースシステム、統合型保管技術を含む倉庫自動化の進歩は、企業が労働力の最適化、精度の最大化、貴重な倉庫スペースの有効活用を追求するにつれ、需要をさらに加速させています。この変化は、自動化プロセスがワークフローを改善し、より高い生産性レベルを支えている密集した都市市場で特に顕著です。

| 市場範囲 | |

|---|---|

| 開始年 | 2025年 |

| 予測年度 | 2026-2035 |

| 開始時価値 | 297億米ドル |

| 予測金額 | 514億米ドル |

| CAGR | 5.6% |

AGVセグメントは2025年に109億米ドルの市場規模を生み出しました。自動誘導車両(AGV)は、レーザーベースのナビゲーション、誘導システム、画像認識ツールなどの技術を用いて自律的に動作します。これらの車両は事前に設定された経路を走行し、リアルタイムで経路を変更することが可能です。これにより、倉庫内での資材の安全かつ効率的な輸送が、手動操作を必要とせずに実現されます。パレットやコンテナ、その他の貨物を一貫性と精度をもって移動させる能力により、現代の資材運搬環境において不可欠な存在となっています。

内燃機関(ICE)セグメントは2025年に62%のシェアを占めました。ディーゼル、ガソリン、LPGを動力源とする内燃機関トラックは、屋内・屋外を問わず過酷な資材運搬作業において依然として高い信頼性を維持しています。高いトルクと耐久性を特徴とするこれらの車両は、困難な条件下での重量物の持ち上げや運搬を必要とする産業に適しています。その性能は鉱業、大規模製造業、建設業などの分野において極めて重要です。

米国産業用トラック市場は2025年に75%のシェアを占め、63億米ドルの規模に達しました。倉庫の拡張と自動化技術の急速な普及が相まって、製造、物流、電子商取引オペレーション全体で堅調な需要を牽引し続けています。電動式機器や高度なハンドリングソリューションへの関心の高まりは、企業の持続可能性目標や安全基準遵守の継続的な取り組みを反映しています。主要な世界のOEMの存在と次世代マテリアルハンドリング技術への多額の投資により、米国は産業用トラック分野における革新の中心地としての地位を確立しています。

よくあるご質問

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 利益率

- 各段階における付加価値

- バリューチェーンに影響を与える要因

- 業界への影響要因

- 促進要因

- 電子商取引の拡大と倉庫の自動化

- インダストリー4.0技術の採用

- 製造業、建設業、物流業における成長

- 先進国市場における労働力不足

- 業界の潜在的リスク&課題

- 初期費用と維持管理費の高さ

- サプライチェーンの混乱と部品不足

- 機会

- 電気・ゼロエミッショントラック

- 自動搬送車(AGV)および自律走行トラック

- 促進要因

- 成長可能性分析

- 将来の市場動向

- 技術とイノベーションの動向

- 現在の技術動向

- 新興技術

- 価格動向

- 地域別

- タイプ別

- 規制情勢

- 規格およびコンプライアンス要件

- 地域別規制枠組み

- 認証基準

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 地域別

- 企業マトリクス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 主な発展

- 合併・買収

- 提携・協業

- 新製品の発売

- 拡大計画

第5章 市場推計・予測:タイプ別、2021-2034

- 無人搬送車(AGV)

- ハンドトラック、プラットフォームトラック、パレットトラック

- オーダーピッカー

- パレットジャッキ

- サイドローダー

- 歩行式スタッカー

第6章 市場推計・予測:推進力別、2021-2034

- 内燃機関(ICE)

- 電気式

第7章 市場推計・予測:事業者別、2021-2034

- 手動式

- 半自動

- 完全自動化

第8章 市場推計・予測:最終用途産業別、2021-2034

- 食品・飲料

- 自動車

- 小売・電子商取引

- 建設・鉱業

- 製造業

- 医薬品

- 物流・倉庫業

- その他

第9章 市場推計・予測:地域別、2021-2034

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- アジア太平洋地域

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第10章 企業プロファイル

- Anhui Heli

- BYD Company

- Clark Material Handling Company

- Combilift

- Crown Equipment

- Doosan Corporation Industrial Vehicle

- Hangcha Group

- Hyster-Yale Materials Handling

- Hyundai Heavy Industries

- Jungheinrich AG

- KION Group AG

- Komatsu

- Manitou Group

- Mitsubishi Logisnext

- Toyota Industries