データセンター冷却市場の機会、成長要因、業界動向分析、および2025年から2034年までの予測

Data Center Cooling Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 230 Pages

- 納期

- 2~3営業日

- 商品コード

- 1876801

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

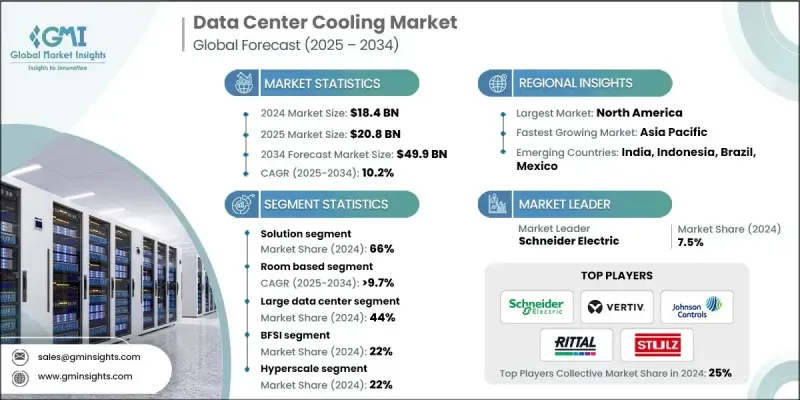

世界のデータセンター冷却市場は、2024年に184億米ドルと評価され、2034年までにCAGR10.2%で成長し、499億米ドルに達すると予測されています。

AIおよび高性能コンピューティング(HPC)ワークロードの増加により、従来の空気冷却から先進的な液体冷却ソリューションへの移行が進んでいます。ダイレクト・トゥ・チップ冷却および液浸冷却技術は、50~120kWのラック密度を管理するケースが増加しており、最新のコンピューティングインフラを現代のデータセンターが処理することを可能にしています。多様な環境で稼働するエッジデータセンターでは、コンパクトかつ遠隔地での信頼性を維持するため、柔軟な熱管理が求められます。ラック電力密度が5kWから8~10kWへとほぼ倍増する中、従来の空冷システムでは需要を満たせなくなり、ハイパースケールおよびエンタープライズ施設では液体冷却ソリューションの採用が進んでいます。ダイレクト・トゥ・チップ液体冷却は、高ワット数CPUやGPUの温度安定性を確保しつつ、エネルギー消費を削減しシステム信頼性を高める方法として、好まれる選択肢として台頭しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024年 |

| 予測年度 | 2025-2034 |

| 開始時価値 | 184億米ドル |

| 予測金額 | 499億米ドル |

| CAGR | 10.2% |

ソリューション分野は2024年に66%のシェアを占め、2034年までCAGR 10.4%で成長すると予測されています。この成長は、高密度AIおよびHPCワークロードをサポート可能な次世代液体冷却システムへの投資、インフラ支出の増加、高度な熱管理技術の採用促進によって牽引されています。

ルームベース冷却セグメントは2024年に76.4%のシェアを占め、2034年までCAGR 9.7%で成長すると予測されています。現代のルームベースシステムは、AI支援による最適化、可変速ファン、封じ込めソリューションを統合し、リアルタイムの気流調整とエネルギー効率の向上を実現しています。これらの革新により、システムの寿命が延び、全体的な持続可能性と信頼性が向上します。

米国データセンター冷却市場は2024年に89%のシェアを占め、63億米ドルの規模に達しました。AIワークロードによる熱密度の増加に伴い、液体冷却や液浸冷却の導入が加速しています。特に大規模キャンパス環境において、80kWを超えるラック密度を管理するため、事業者が施設のアップグレードを進めているためです。

データセンター冷却市場の主要企業には、エマーソン・ネットワークパワー、ジョンソンコントロールズ、バーティブ、シュナイダーエレクトリック、モティベアー、シュトゥルツ、ディグリーコントロールズ、リタール、エアデールインターナショナル、クールセントリックなどが挙げられます。データセンター冷却市場の企業は、市場での存在感を強化するため複数の戦略を採用しています。極端な熱密度に対応可能な高効率液体冷却・液浸冷却技術の開発に向け、研究開発(R&D)への投資を進めています。ハイパースケールおよびエンタープライズデータセンター事業者との提携は、先進的な冷却ソリューションの普及拡大に寄与しております。また、リアルタイムのエネルギー管理を実現するAIベースの最適化ツールの強化にも注力しております。戦略的な合併・買収により、技術ポートフォリオと地理的展開範囲の拡大を図っております。

よくあるご質問

目次

第1章 調査手法

- 市場範囲と定義

- 調査設計

- 調査アプローチ

- データ収集方法

- データマイニングの情報源

- グローバル

- 地域別/国別

- 基本推定値と計算

- 基準年計算

- 市場推定における主要な動向

- 1次調査および検証

- 一次情報

- 予測モデル

- 調査の前提条件と制限事項

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 利益率分析

- コスト構造

- 各段階における付加価値

- バリューチェーンに影響を与える要因

- ディスラプション

- 業界への影響要因

- 促進要因

- 高密度AIおよびHPCワークロードの導入増加

- 持続可能性とエネルギー効率への関心の高まり

- 新興地域におけるデータセンター容量拡大の増加傾向

- DCIMとAIベースの冷却最適化の統合

- 業界の潜在的リスク&課題

- 初期費用の高さと改修の課題

- 液体冷却インフラ管理の複雑性

- 冷媒に関する環境規制の強化

- 市場機会

- アジア太平洋地域(APAC)および中東・アフリカ地域(MEA)におけるハイパースケール施設およびコロケーション施設の成長

- AI駆動型熱管理の統合

- モジュール式・プレハブ型データセンターへの移行

- 促進要因

- 成長可能性分析

- 規制情勢

- 北米

- 欧州

- アジア太平洋地域

- 南米

- 中東・アフリカ

- ポーター分析

- PESTEL分析

- 技術とイノベーションの動向

- 現在の技術動向

- 新興技術

- 価格動向

- 地域別

- 製品別

- コスト内訳分析

- 特許分析

- サステナビリティと環境面

- 持続可能な実践

- 廃棄物削減戦略

- 生産におけるエネルギー効率

- 環境に配慮した取り組み

- カーボンフットプリントに関する考慮事項

- 市場の成熟度と普及状況の分析

- 将来の動向と市場変革

- 冷却における人工知能の統合

- 量子コンピューティングの冷却要件

- 持続可能で環境に優しい冷却技術

- モジュラー型およびプレハブ型冷却ソリューション

- 廃熱回収・再利用システム

- 先端材料・ナノテクノロジー

- 自律冷却システム管理

- ブロックチェーンと分散コンピューティングの影響

- 6Gインフラの冷却要件

- データセンター冷却市場動向とギャップ分析

- 電力密度の動向と冷却要件

- 冷却技術の移行パターン

- 市場ギャップ分析

- エネルギー効率と持続可能性の重要性

- データセンターにおける機械システムの進化

- 戦略的R&D及び市場整合性フレームワーク

- HVAC企業における研究開発投資の優先事項

- 市場整合戦略とフレームワーク

- 先進的ソリューション開発の道筋

- パートナーシップおよびエコシステム構築

- 導入ロードマップ

- 投資分析と市場機会

- 投資環境の概要

- ベンチャーキャピタル及びプライベートエクイティ活動

- 戦略的投資機会

- 市場参入戦略

- 技術ライセンシングの機会

- 地域拡大戦略

- 投資収益率分析

- 将来の投資動向

- 電力使用効率(PUE)の動向と分析

- PUEの概要とその重要性について

- データセンタータイプ別平均PUEベンチマーク

- 冷却技術がPUEに与える影響

- PUE最適化戦略とAI駆動制御

- PUE基準の地域的・規制の影響

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 戦略的展望マトリックス

- 主な発展

- 合併・買収

- 提携・協業

- 新製品の発売

- 事業拡大計画と資金調達

第5章 市場推計・予測:コンポーネント別、2021-2034

- 主要動向

- ソリューション

- エアコン

- 空調処理装置

- スプリットエアコンシステム

- パッケージ型空調ユニット(PAC)

- その他

- 冷却ユニット

- 空冷式チラー

- 水冷式チラー

- グリコール冷却式チラー

- 冷却塔

- 蒸発冷却

- ドライ

- その他

- 制御システム

- エコノマイザーシステム

- 凝縮式

- 不凝縮

- 液体冷却システム

- ダイレクト・トゥ・チップ

- 没入型

- 単相

- 二相

- その他

- エアコン

- サービス

- コンサルティング

- 保守およびサポート

- 設置および導入

第6章 市場推計・予測:冷却技術別、2021-2034

- 主要動向

- ラック/列ベース

- ルームベース

第7章 市場推計・予測:データセンター規模別、2021-2034

- 主要動向

- 小規模データセンター

- 中規模データセンター

- 大規模データセンター

第8章 市場推計・予測:用途別、2021-2034

- 主要動向

- BFSI(銀行・金融・保険)

- コロケーション

- エネルギー

- 政府

- ヘルスケア

- 製造業

- IT・通信

- その他

第9章 市場推計・予測:データセンター別、2021-2034

- 主要動向

- ハイパースケール

- コロケーション

- 企業向け

- エッジ

- クラウド

第10章 市場推計・予測:地域別、2021-2034

- 主要動向

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- ロシア

- 北欧諸国

- ポーランド

- ベネルクス

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- 東南アジア

- ブルネイ

- カンボジア

- インドネシア

- ラオス

- マレーシア

- ミャンマー

- フィリピン

- シンガポール

- タイ

- 東ティモール

- ベトナム

- 南米

- ブラジル

- アルゼンチン

- コロンビア

- チリ

- 中東・アフリカ地域

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第11章 企業プロファイル

- グローバルプレイヤー

- Carrier Global

- Daikin Industries

- Emerson Electric

- Honeywell International

- Johnson Controls

- Mitsubishi

- Schneider Electric

- Siemens

- Trane Technologies

- Vertiv

- 地域プレイヤー

- Airedale International

- Asetek

- Coolcentric

- CoolIT Systems

- Green Revolution Cooling(GRC)

- LiquidStack

- Motivair

- Rittal

- STULZ

- Submer Technologies

- 新興企業

- Boyd

- Chilldyne

- ExaScaler

- Hardcore Computer

- Iceotope Technologies

- Kaltra

- Midas Green Technologies

- Phononic

- TMGcore

- ZutaCore

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 230 Pages

- 納期

- 2~3営業日