|

|

市場調査レポート

商品コード

1352084

次世代アノード材料市場- 世界および地域別分析:エンドユーザー別、タイプ別、地域別 - 分析と予測(2023年~2032年)Next-Generation Anode Materials Market - A Global and Regional Analysis: Focus on End User, Type, and Region - Analysis and Forecast, 2023-2032 |

||||||

カスタマイズ可能

|

|||||||

| 次世代アノード材料市場- 世界および地域別分析:エンドユーザー別、タイプ別、地域別 - 分析と予測(2023年~2032年) |

|

出版日: 2023年09月26日

発行: BIS Research

ページ情報: 英文 233 Pages

納期: 1~5営業日

|

- 全表示

- 概要

- 図表

- 目次

世界の次世代アノード材料の市場規模は2022年に26億5,060万米ドルとなりました。

同市場は今後、16.29%のCAGRで拡大し、2032年には115億5,460万米ドルに達すると予測されています。世界の次世代アノード材料市場の成長は、より高速な充電特性と出力密度の向上を備えた次世代アノード材料に対する需要の高まりが牽引すると予想されます。

| 主要市場統計 | |

|---|---|

| 予測期間 | 2023 - 2032 |

| 2023の評価 | 29億6,990万米ドル |

| 2032の予測 | 115億5,460万米ドル |

| CAGR | 16.29% |

世界の次世代アノード材料市場は成長段階にあり、次世代アノード材料を提供する企業の数は急速に増加しています。電池技術における最新の技術進歩、電気自動車やエネルギー貯蔵分野の増加が、世界中で次世代アノード材料市場の採用を後押ししています。さらに、高度なエネルギー貯蔵技術への支出の増加は、次世代アノード材料産業の拡大を後押しする主な要因の一つです。二酸化炭素排出量を最小限に抑え、製造コストも競合しないことから、再生可能エネルギーへの投資は世界中で急増しています。さらに、次世代アノード材料は、従来の電池技術よりも優れた効果を発揮することが、その主な利点のひとつです。さらに、予測期間中、主に輸送、エネルギー貯蔵、電気・電子部門から次世代アノード材料に対する大きな需要があるため、次世代アノード材料業界では、既存の次世代アノード材料プロバイダーと新興の次世代アノード材料プロバイダーの間で市場競争が大幅に拡大すると予想されます。

世界の次世代アノード材料市場は、電池競争を強化するための研究開発プロジェクトの頻度の増加、急速充電や高密度電池のニーズの高まり、環境やカーボンニュートラル目標への関心の高まりなど、いくつかの要因によって牽引されています。

次世代アノード材料は、容量と安定性の向上、ライフサイクルの改善、高エネルギー密度などの利点により、ますます需要が高まっています。さらに、次世代負極コンポーネントは、高容量正極物質と効率的に機能するように設計することができます。このような一貫性により、より大きな合体容積とエネルギー消費の少ない、最適化された高性能バッテリーを実現することができます。次世代アノード材料は、環境スチュワードシップガイドラインに準拠した長期的なソリューションを提供し、次世代の環境保護に貢献します。さらに、次世代アノード材料のエネルギー密度を高めることで、バッテリーをより軽量化できる可能性があり、これはバッテリーの有効性と耐久性を高めるため、電気自動車にとって極めて重要です。さらに、最先端かつ持続可能な製品を顧客に提供することで、企業は研究開発投資を増やしながら、大規模な国際的顧客基盤を確立しています。世界の次世代アノード材料市場の成長は、充電・放電能力の高速化と、さまざまな主要市場での採用によって大きく左右されます。現在の市場シナリオでは、シリコン負極の数量増加と劣化、高品質グラフェンの大規模生産の不足のいずれかが、市場成長の足かせとなっています。予測期間(2023年~2032年)には、この市場環境がより良好になり、市場拡大を促進する一助となると予測されます。

当レポートでは、世界の次世代アノード材料市場について調査し、市場の概要とともに、エンドユーザー別、タイプ別、地域別の動向、および市場に参入する企業のプロファイルなどを提供しています。

目次

第1章 市場

- 業界の展望

- ビジネスダイナミクス

- スタートアップの情勢

第2章 用途

第3章 製品

- 世界の次世代アノード材料市場(製品と仕様)

- 次世代アノード材料のタイプ間の比較分析

- 世界の次世代アノード材料市場の需要分析(タイプ別)、数量および価値データ

- 製品ベンチマーク:成長率- 市場シェアマトリックス(タイプ別)、2022年

- 特許分析

- 価格分析

第4章 地域

- 北米

- 欧州

- 英国

- 中国

- アジア太平洋と日本

- その他の地域

第5章 市場-競合ベンチマーキングと企業プロファイル

- 競合ベンチマーキング

- 競争力マトリックス

- 主要企業の製品マトリクス(タイプ別)

- 主要企業の市場シェア分析、2022年

- 企業プロファイル

- Altairnano

- LeydnJar Technologies BV

- Nexeon Ltd.

- pH Matter LLC

- Sila Nanotechnologies Inc.

- Cuberg

- Shanghai Shanshan Technology Co., Ltd.

- AMPIRUS TECHNOLOGIES

- California Lithium Battery

- Enovix

- Albemarle Corporation

- Talga Group.

- Tianqi Lithium Corporation

- Jiangxi Ganfeng Lithium Co., Ltd.

- POSCO CHEMICAL

第6章 調査手法

List of Figures

- Figure 1: Global Next-Generation Anode Materials Market, $Million, 2022, 2023, and 2032

- Figure 2: Global Next-Generation Anode Materials Market (by End User), $Million, 2022 and 2032

- Figure 3: Global Next-Generation Anode Materials Market (by Type), $Million, 2022 and 2032

- Figure 4: Global Next-Generation Anode Materials Market (by Region), $Million, 2022 and 2032

- Figure 5: Global Next-Generation Anode Materials Market Coverage

- Figure 6: Global Electric Vehicle Sales, Million Units, 2020, 2025, and 2030

- Figure 7: Production Data of Ferrosilicon and Silicon, Thousand Metric Tons, 2018-2022

- Figure 8: Recycling Process of Silicon into Anode Material for Lithium-Ion Batteries

- Figure 9: Supply Chain Analysis of the Global Next-Generation Anode Materials Market

- Figure 10: Anode and Cathode Materials

- Figure 11: Comparison Analysis between Anode and Cathode Materials

- Figure 12: Business Dynamics for Next-Generation Anode Materials Market

- Figure 13: Production and Reserves Data of Silicon, Thousand Metric Tons, 2021 and 2022

- Figure 14: Battery Storage Capabilities (by Country), 2020 and 2026

- Figure 15: Stability of Silicon Particles Varying with Diameter Size

- Figure 16: Clean Energy Investment in the Net Zero Pathway, $Trillion, 2016-2020, 2030, and 2050

- Figure 17: Advancements in Polymer Binders for Silicon based Anodes

- Figure 18: Components of Electrolytes in Lithium-ion Batteries

- Figure 19: Next-Generation Anode Materials Market (by Application)

- Figure 20: Global Electric Vehicle Sales (by Type), 2020-2022

- Figure 21: Australian State Data for Battery Installations with Small-Scale Systems, 2020-August 2022

- Figure 22: Average Annual Net Renewable Capacity Additions, Gigawatt (GW), 2011-2022

- Figure 23: Next-Generation Anode Materials Market (by Type)

- Figure 24: Advantages Offered by GCA

- Figure 25: Total Year-Wise Patents Filed for Global Next-Generation Anode Materials Market, January 2020-July 2023

- Figure 26: Total Year-Wise Patents Granted for Global Next-Generation Anode Materials Market, January 2020-July 2023

- Figure 27: Global Next-Generation Anode Materials Market, Patent Analysis (by Status), January 2020-July 2023

- Figure 28: Global Next-Generation Anode Materials Market, Patent Analysis (by Organization), January 2020-July 2023

- Figure 29: Research Methodology

- Figure 30: Top-Down and Bottom-Up Approach

- Figure 31: Global Next-Generation Anode Materials Market: Influencing Factors

- Figure 32: Assumptions and Limitations

List of Tables

- Table 1: Major Key Investor of Solid-State Batteries

- Table 2: Stakeholders of the Next-Generation Anode Materials Market

- Table 3: List of Regulatory/Certification Bodies

- Table 4: List of Government Programs for the Next-Generation Anode Materials Market

- Table 5: List of Programs by Research Institutions and Universities

- Table 6: Key Investments by Companies

- Table 7: Comparison Table of Key Metrics

- Table 8: Key Product and Market Development

- Table 9: Key Mergers and Acquisitions, Partnerships, Collaborations, and Joint Ventures

- Table 10: Global Next-Generation Anode Materials Market (by End User), Kilo Tons, 2022-2032

- Table 11: Global Next-Generation Anode Materials Market (by End User), $Million, 2022-2032

- Table 12: Technical Difference between Different Types of Next-Generation Anode Materials Market

- Table 13: Commercial Difference between Different Types of Next-Generation Anode Materials Market

- Table 14: Global Next-Generation Anode Materials Market (by Type), Kilo Tons, 2022-2032

- Table 15: Global Next-Generation Anode Materials Market (by Type), $Million, 2022-2032

- Table 16: Global Pricing Analysis, Next-Generation Anode Materials Market, $/Kg, 2022-2032

- Table 17: Average Pricing Analysis, Next-Generation Anode Materials Market (by Region), $/Kg, 2022-2032

- Table 18: Global Next-Generation Anode Materials Market (by Region), Kilo Tons, 2022-2032

- Table 19: Global Next-Generation Anode Materials Market (by Region), $Million, 2022-2032

- Table 20: North America Next-Generation Anode Materials Market (by End User), Tons, 2022-2032

- Table 21: North America Next-Generation Anode Materials Market (by End User), $Million, 2022-2032

- Table 22: North America Next-Generation Anode Materials Market (by Type), Tons, 2022-2032

- Table 23: North America Next-Generation Anode Materials Market (by Type), $Million, 2022-2032

- Table 24: U.S. Next-Generation Anode Materials Market (by End User), Tons, 2022-2032

- Table 25: U.S. Next-Generation Anode Materials Market (by End User), $Million, 2022-2032

- Table 26: U.S. Next-Generation Anode Materials Market (by Type), Tons, 2022-2032

- Table 27: U.S. Next-Generation Anode Materials Market (by Type), $Million, 2022-2032

- Table 28: Canada Next-Generation Anode Materials Market (by End User),Tons, 2022-2032

- Table 29: Canada Next-Generation Anode Materials Market (by End User), $Million, 2022-2032

- Table 30: Canada Next-Generation Anode Materials Market (by Type), Tons, 2022-2032

- Table 31: Canada Next-Generation Anode Materials Market (by Type), $Million, 2022-2032

- Table 32: Mexico Next-Generation Anode Materials Market (by End User), Tons, 2022-2032

- Table 33: Mexico Next-Generation Anode Materials Market (by End User), $Million, 2022-2032

- Table 34: Mexico Next-Generation Anode Materials Market (by Type), Tons, 2022-2032

- Table 35: Mexico Next-Generation Anode Materials Market (by Type), $Million, 2022-2032

- Table 36: Europe America Next-Generation Anode Materials Market (by End User), Tons, 2022-2032

- Table 37: Europe Next-Generation Anode Materials Market (by End User), $Million, 2022-2032

- Table 38: Europe Next-Generation Anode Materials Market (by Type), Tons, 2022-2032

- Table 39: Europe Next-Generation Anode Materials Market (by Type), $Million, 2022-2032

- Table 40: Germany Next-Generation Anode Materials Market (by End User), Tons, 2022-2032

- Table 41: Germany Next-Generation Anode Materials Market (by End User), $Million, 2022-2032

- Table 42: Germany Next-Generation Anode Materials Market (by Type), Tons, 2022-2032

- Table 43: Germany Next-Generation Anode Materials Market (by Type), $Million, 2022-2032

- Table 44: Spain Next-Generation Anode Materials Market (by End User), Tons, 2022-2032

- Table 45: Spain Next-Generation Anode Materials Market (by End User), $Million, 2022-2032

- Table 46: Spain Next-Generation Anode Materials Market (by Type), Tons, 2022-2032

- Table 47: Spain Next-Generation Anode Materials Market (by Type), $Million, 2022-2032

- Table 48: Poland Next-Generation Anode Materials Market (by End User), Tons, 2022-2032

- Table 49: Poland Next-Generation Anode Materials Market (by End User), $Million, 2022-2032

- Table 50: Poland Next-Generation Anode Materials Market (by Type), Tons, 2022-2032

- Table 51: Poland Next-Generation Anode Materials Market (by Type), $Million, 2022-2032

- Table 52: Hungary Next-Generation Anode Materials Market (by End User), Tons, 2022-2032

- Table 53: Hungary Next-Generation Anode Materials Market (by End User), $Million, 2022-2032

- Table 54: Hungary Next-Generation Anode Materials Market (by Type), Tons, 2022-2032

- Table 55: Hungary Next-Generation Anode Materials Market (by Type), $Million, 2022-2032

- Table 56: Rest-of-Europe Next-Generation Anode Materials Market (by End User), Tons, 2022-2032

- Table 57: Rest-of-Europe Next-Generation Anode Materials Market (by End User), $Million, 2022-2032

- Table 58: Rest-of-Europe Next-Generation Anode Materials Market (by Type), Tons, 2022-2032

- Table 59: Rest-of-Europe Next-Generation Anode Materials Market (by Type), $Million, 2022-2032

- Table 60: U.K. Next-Generation Anode Materials Market (by End User), Tons, 2022-2032

- Table 61: U.K. Next-Generation Anode Materials Market (by End User), $Million, 2022-2032

- Table 62: U.K. Next-Generation Anode Materials Market (by Type), Tons, 2022-2032

- Table 63: U.K. Next-Generation Anode Materials Market (by Type), $Million, 2022-2032

- Table 64: China Next-Generation Anode Materials Market (by End User), Kilo Tons, 2022-2032

- Table 65: China Next-Generation Anode Materials Market (by End User), $Million, 2022-2032

- Table 66: China Next-Generation Anode Materials Market (by Type), Kilo Tons, 2022-2032

- Table 67: China Next-Generation Anode Materials Market (by Type), $Million, 2022-2032

- Table 68: Asia-Pacific and Japan Next-Generation Anode Materials Market (by End User), Tons, 2022-2032

- Table 69: Asia-Pacific and Japan Next-Generation Anode Materials Market (by End User), $Million, 2022-2032

- Table 70: Asia-Pacific and Japan Next-Generation Anode Materials Market (by Type), Tons, 2022-2032

- Table 71: Asia-Pacific and Japan Next-Generation Anode Materials Market (by Type), $Million, 2022-2032

- Table 72: Japan Next-Generation Anode Materials Market (by End User), Tons, 2022-2032

- Table 73: Japan Next-Generation Anode Materials Market (by End User), $Million, 2022-2032

- Table 74: Japan Next-Generation Anode Materials Market (by Type), Tons, 2022-2032

- Table 75: Japan Next-Generation Anode Materials Market (by Type), $Million, 2022-2032

- Table 76: South Korea Next-Generation Anode Materials Market (by End User), Tons, 2022-2032

- Table 77: South Korea Next-Generation Anode Materials Market (by End User), $Million, 2022-2032

- Table 78: South Korea Next-Generation Anode Materials Market (by Type), Tons, 2022-2032

- Table 79: South Korea Next-Generation Anode Materials Market (by Type), $Million, 2022-2032

- Table 80: India Next-Generation Anode Materials Market (by End User), Tons, 2022-2032

- Table 81: India Next-Generation Anode Materials Market (by End User), $Million, 2022-2032

- Table 82: India Next-Generation Anode Materials Market (by Type), Tons, 2022-2032

- Table 83: India Next-Generation Anode Materials Market (by Type), $Million, 2022-2032

- Table 84: Rest-of-Asia-Pacific and Japan Next-Generation Anode Materials Market (by End User), Tons, 2022-2032

- Table 85: Rest-of-Asia-Pacific and Japan Next-Generation Anode Materials Market (by End User), $Million, 2022-2032

- Table 86: Rest-of-Asia-Pacific and Japan Next-Generation Anode Materials Market (by Type), Tons, 2022-2032

- Table 87: Rest-of-Asia-Pacific and Japan Next-Generation Anode Materials Market (by Type), $Million, 2022-2032

- Table 88: Rest-of-the-World Next-Generation Anode Materials Market (by End User), Tons, 2022-2032

- Table 89: Rest-of-the-World Next-Generation Anode Materials Market (by End User), $Million, 2022-2032

- Table 90: Rest-of-the-World Next-Generation Anode Materials Market (by Type), Tons, 2022-2032

- Table 91: Rest-of-the-World Next-Generation Anode Materials Market (by Type), $Million, 2022-2032

- Table 92: South America Next-Generation Anode Materials Market (by End User), Tons, 2022-2032

- Table 93: South America Next-Generation Anode Materials Market (by End User), $Million, 2022-2032

- Table 94: South America Next-Generation Anode Materials Market (by Type), Tons, 2022-2032

- Table 95: South America Next-Generation Anode Materials Market (by Type), $Million, 2022-2032

- Table 96: Middle East and Africa Next-Generation Anode Materials Market (by End User), Tons, 2022-2032

- Table 97: Middle East and Africa Next-Generation Anode Materials Market (by End User), $Million, 2022-2032

- Table 98: Middle East and Africa Next-Generation Anode Materials Market (by Type), Tons, 2022-2032

- Table 99: Middle East and Africa Next-Generation Anode Materials Market (by Type), $Million, 2022-2032

- Table 100: Product Matrix of Key Companies (by Type)

- Table 101: Market Shares of Key Companies, 2022

“Global Next-Generation Anode Materials Market to Reach $11,554.6 Million by 2032.”

The global next-generation anode materials market was valued at $2,650.6 million in 2022, and it is expected to grow at a CAGR of 16.29% and reach $11,554.6 million by 2032. The growth in the global next-generation anode materials market is expected to be driven by growing demand for next-generation anode materials with faster charging properties and enhanced power density.

Introduction of Next-Generation Anode Materials Market

| KEY MARKET STATISTICS | |

|---|---|

| Forecast Period | 2023 - 2032 |

| 2023 Evaluation | $2,969.9 Million |

| 2032 Forecast | $11,554.6 Million |

| CAGR | 16.29% |

Both consumer electronics and the transportation sectors have had substantial growth over the past 10 years, yet these sectors are still constrained by the inefficient power sources employed in product manufacturing. In most laptops and phones, batteries occupy almost half of the space. Thus, a 50% increase in battery energy density can increase product efficiency while making room for additional features such as upgraded cameras, better sound, and improved communication. However, there has not been much progress in battery technology, and lithium-ion batteries remain the dominant energy storage paradigm today. Additionally, it is anticipated that within the next few years, lithium-ion battery technology is expected to reach an energy limit with the current materials and cell designs, thereby generating a demand for the next generation of anode materials, which have a higher energy density.

Market Introduction

The global next-generation anode materials market is in a growth phase, wherein the number of companies offering next-generation anode materials is increasing rapidly. Latest technological advancements in battery technologies and the growing number of electric vehicles, as well as energy storage sectors, are boosting the adoption of next-generation anode materials market across the globe. Moreover, increased expenditures in advanced energy storage technologies are one of the primary factors fuelling the expansion of the next-generation anode materials industry. As a result of its minimal carbon footprint and competitive manufacturing expenditures, energy from renewable sources has seen an upsurge in investments worldwide. Furthermore, next-generation anode materials' capacity to outperform more traditional battery technologies in terms of effectiveness is one of its primary benefits. Additionally, with significant demand for next-generation anode materials during the forecast period, primarily from the transportation, energy storage, and electrical and electronics sectors, the market competition is expected to grow considerably among established and emerging next-generation anode materials providers in the next-generation anode materials industry.

Industrial Impact

The global next-generation anode materials market is driven by several factors, such as the increasing frequency of R&D projects to enhance battery competition, the increasing need for fast charging and high-density batteries, and growing concerns for the environment and carbon neutrality targets.

Next-generation anode materials are increasingly growing in demand, owing to benefits such as enhanced capacity and stability, improved life cycle, and high energy density. Additionally, next-generation anode components can be designed to function efficiently with high-capacity cathode substances. This coherence can result in optimized and high-performing batteries with greater combined volume and lower consumption of energy. Next-generation anode materials offer long-term solutions that comply with environmental stewardship guidelines and aid in protecting the environment for upcoming generations. Additionally, increased density of energy within next-generation anode materials may assist in making batteries more lightweight, which is crucial for electric vehicles as it increases their effectiveness and endurance. Furthermore, by providing customers with cutting-edge and sustainable products, the companies are establishing a large international customer base while increasing R&D investments. The growth of the global next-generation anode materials market largely depends on faster charging and discharging abilities and their adoption across various major markets. In the current market scenario, the market growth is held back either due to the increased volume and degradation of silicon anodes and lack of large-scale production of high-quality graphene. Over the projected period (2023-2032), it is anticipated that this market environment will become more favorable and assist in promoting market expansion.

Market Segmentation:

Segmentation 1: By End User

- Transportation

- Passenger Electric Vehicles

- Commercial Electric Vehicles

- Others

- Electrical and Electronics

- Energy Storage

- Others

Transportation Segment to Dominate the Global Next-Generation Anode Materials Market (by End User)

The transportation segment based on end user led the next-generation anode materials market in 2022 and was the largest segment due to rising sales of electric vehicles globally. The demand for electric cars has increased dramatically in recent years, notably in countries such as the U.S., China, and Japan. According to the International Energy Agency (IEA), more than 10 million electric vehicles have been sold by 2022. The growing popularity of electric vehicles is driving up demand for next-generation anode materials for batteries. The producers and suppliers of next-generation anode materials for the transportation sector are anticipated to benefit from this during the projected period (2023-2032).

Segmentation 2: By Type

- Silicon/Silicon Oxide Blend

- Lithium Titanium Oxide

- Silicon-Carbon Composite

- Silicon-Graphene Composite

- Lithium Metal

- Others

Silicon/Silicon Oxide Blend Segment to Lead the Global Next-Generation Anode Materials Market (by Type)

Next-generation anode materials include silicon/silicon oxide blend, silicon-carbon composite, Siliocn-graphene composite, lithium titanium oxide, lithium metal, and others. Due to their distinct properties, these materials are projected to cause a disruption in the existing anode material industry during the forecast period 2023-2032. In the coming years, there could be a significant increase in the consumption of silicon/silicon oxide blend anode material. Over the next 10 years, these next-generation anode materials are expected to cannibalize a large share of the worldwide anode materials market from conventional pure graphite and carbon anode materials.

Segmentation 3: by Region

- North America: U.S., Canada, and Mexico

- Europe: Germany, Spain, Poland, Hungary, and Rest-of-Europe

- U.K.

- China

- Asia-Pacific and Japan: Japan, South Korea, India, and Rest-of-Asia-Pacific and Japan

- Rest-of-the-World: Middle East and Africa and South America

The global next-generation anode materials market is expected to witness significant growth in the coming years, with major contributions from China, Asia-Pacific and Japan, Europe, and North America regional markets. In terms of revenue generation, China dominates the global market for next-generation anode materials due to the presence of major businesses, expanded battery production, increased R&D expenditure in this sector, and supporting infrastructure. The early adoption of lithium-ion battery technology, as well as the presence of a substantial EV fleet, is another factor driving market growth. Furthermore, China's rapidly rising economy and the presence of key industry players along the supply chain of next-generation anode material components are having a significant impact on the market's growth.

Recent Developments in the Global Next-Generation Anode Materials Market

- In May 2022, Sila Nanotechnologies Inc. disclosed the purchase of a 600,000-square-foot facility in Moses Lake, Washington. Sila intends to employ the facility to manufacture lithium-ion anode materials at the high standard and volume required for serving the automotive industry.

- In July 2023, to improve the efficiency of lithium-ion batteries for electric vehicles (EVs), Panasonic Energy Co., Ltd. stated that it had signed a contract with Nexeon Ltd. for the acquisition of silicon anode material for automobile batteries.

- In February 2023, NanoRial Technologies Ltd. and NEO Battery Materials Ltd. entered a mutually exclusive partnership contract. By using NanoRial's high-performance carbon nanotubes (CNT) materials as a durable nano coating material, NEO and NanoRial are collaborating to improve the durability and efficacy of NEO's silicon anode materials, NBMSiDE.

- In August 2022, to increase the research of silicon battery anode substances, Nexeon raised $90 million, extending its total financing to $170 million. It is expected that the company will be able to manufacture large quantities of its silicon-based anode materials for lithium-ion batteries with the funding it received from subsequent rounds of investment.

- In September 2022, a collaborative strategic framework contract was executed by Jiangxi Ganfeng Lithium Co., Ltd. and the municipal government of Yichun City in order to establish a manufacturing facility for lithium-ion batteries and other related manufacturing network initiatives. According to the release, the company intends to set up a lithium metal project with a planned production capacity of 7,000 tons in the Yichun Economic & Technological Development Zone, as well as a new-type lithium-ion production facility with a yearly output capacity of 30 GWh.

Demand - Drivers, Challenges, and Opportunities

Market Drivers: Increasing Need for Fast Charging and High-Density Batteries

The evolution of lithium-ion batteries has ushered in a digital electronic revolution by serving as a powerhouse for a variety of devices such as laptops, mobile phones, and numerous other electronic gadgets. The increased demand for EVs as a result of escalating environmental concerns places a premium on battery energy storage capacity. The growing demand for EVs has a direct impact on the lithium-ion battery and next-generation anode materials markets. Major impediments to the growth of EVs and consumer appliances are charging difficulties, as recharging EV batteries takes much longer than fueling conventional petroleum vehicles. Graphite, a commonly used anode material, has a considerably low discharge potential. This inhibits the lithium-ion battery's ability to charge quickly. Furthermore, researchers are Sdeveloping various combinations of battery anode elements such as silicon, tin, and germanium to enable the batteries' quick charging capability without compromising their durability. Thus, it can be said that the growing demand for higher-density and fast-charging batteries is driving the growth of the global next-generation anode materials market.

Market Challenges: Lack of Large-Scale Production of High-Quality Graphene

The electrochemical performance of numerous end-use applications has improved as a result of the evolution of nanostructured graphene. A potential additive for self-healing materials is graphene. According to scientists at the Samsung Advanced Institute of Technology, batteries with graphene coatings have a five-fold increase in charging capacity. Through its use in batteries, graphene's electronic properties have the potential to usher in a revolutionary development in energy storage applications. The difficulty in scaling up mass graphene production, however, limits the wide adaptability of graphene despite its advantageous properties. Large-scale production has a significant impact on graphene's characteristics, including its thermal conductivity, mechanical flexibility, transparency, and electrical conductivity. As a result, maintaining the quality of graphene becomes challenging.

Market Opportunities: Increasing Investment in Renewable Energy Sources

Global acceptance and investment in renewable energy are increasing. Lithium-ion batteries are anticipated to play a significant role in the transition that both governments and businesses are attempting to navigate away from fossil fuels and toward renewable energy sources in order to minimize carbon emissions and meet the targets of the Paris Agreement. The firms are additionally researching the potential for adopting lithium-ion batteries as the primary energy storage system for renewable energy accomplished off-grid. Furthermore, lithium-ion batteries outperform other commercially available batteries in terms of energy density, specific energy, and power density. Furthermore, lithium-ion batteries' rising use as energy storage devices for renewable energy sources is fueled by their high-power discharge capability, improved round-trip efficiency, low self-discharge rate, and substantially longer work life.

How can this report add value to an organization?

Product/Innovation Strategy: The product segment helps the reader to understand the different types involved in the next-generation anode materials market. Moreover, the study provides the reader with a detailed understanding of the global next-generation anode materials market based on the end user (transportation, electrical and electronics, energy storage, and others). Next-generation anode materials market is gaining traction in end-user industries on the back of sustainability concerns and their higher efficiency properties. Next-generation anode materials are also being used for controlling green house gas (GHG) emissions. Moreover, partnerships and collaborations are expected to play a crucial role in strengthening market position over the coming years, with the companies focusing on bolstering their technological capabilities and gaining a dominant market share in the next-generation anode materials industry.

Growth/Marketing Strategy: The global next-generation anode materials market has been growing at a rapid pace. The market offers enormous opportunities for existing and emerging market players. Some of the strategies covered in this segment are mergers and acquisitions, product launches, partnerships and collaborations, business expansions, and investments. The strategies preferred by companies to maintain and strengthen their market position primarily include partnerships, agreements, and collaborations.

Competitive Strategy: The key players in the global next-generation anode materials market analyzed and profiled in the study include next-generation anode materials providers that develop, maintain, and market next-generation anode materials. Moreover, a detailed competitive benchmarking of the players operating in the global next-generation anode materials market has been done to help the reader understand the ways in which players stack against each other, presenting a clear market landscape. Additionally, comprehensive competitive strategies such as partnerships, agreements, and collaborations will aid the reader in understanding the untapped revenue pockets in the market.

Research Methodology

Factors for Data Prediction and Modeling

- The scope of this report has been focused on next-generation anode materials.

- The market volume has been calculated based on the anode materials production and share of the next-generation anode materials market in overall anode material production.

- Based on the classification, the average selling price (ASP) has been calculated by the weighted average method. ASP calculations are completely based on the number of data points considered while conducting the research.

- The base currency considered for the market analysis is the US$. Currencies other than the US$ have been converted to the US$ for all statistical calculations, considering the average conversion rate for that particular year.

- The currency conversion rate has been taken from the historical exchange rate of the Oanda website.

- Nearly all the recent developments from January 2020 to March 2023 have been considered in this research study.

- The study of the market is limited to next-generation anode materials type and does not include other types.

- The information rendered in the report is a result of in-depth primary interviews, surveys, and secondary analysis.

- Where relevant information was not available, proxy indicators and extrapolation were employed.

- Any economic downturn in the future has not been taken into consideration for the market estimation and forecast.

- Technologies currently used are expected to persist through the forecast with no major technological breakthroughs.

Market Estimation and Forecast

The market size for the global next-generation anode materials market has been calculated through a mix of secondary research and primary inputs. A combination of top-down and bottom-up approaches has been followed to derive the quantitative information. The steps involved in the bottom-up approach are as follows:

- Overall battery, battery cell, and anode materials production for each country have been calculated separately.

- Further, based on past data and future scenarios, each country's next-generation anode materials have been estimated till the forecast timeframe.

- For each country, the next-generation anode materials penetration is calculated based on different secondary sources, and the same information has been validated from primary sources across the ecosystem of the next-generation anode materials market.

- Once the next-generation anode materials penetration has been estimated in the anode materials production, the penetration for each level is estimated based on the parameters such as:

- Major end-users, such as electric vehicle developments in the country

- A regulatory scenario of each country

- The presence of next-generation anode materials manufacturers in the country

- The economic condition of the country

- The estimated numbers of next-generation anode materials have been derived based on the demand for different types of anode materials.

- From different secondary sources and primary respondents, the penetration of next-generation anode materials is estimated for each product and application.

- Further, based on past end-user trends, primary interviews, and future scenarios, region shares have been estimated till the forecast timeframe.

- For each country, the next-generation anode materials penetration was calculated based on different secondary sources, and the same information has been validated from primary sources across the ecosystem of the next-generation anode materials market.

- Based on the penetration of next-generation anode materials under each product and application, the total estimated number of next-generation anode materials was derived for each country. After calculating the same data for each country, the numbers are summed up to get regional-level demand, and regional-level demand is summed up to get global demand from 2022 to 2032.

- All the factors, such as penetration levels in each country, are validated from different primaries throughout the duration of the study.

Primary Research

The primary sources involve industry experts from the next-generation anode materials ecosystem, including the raw material supplier, next-generation anode materials manufacturers, and battery manufacturers, among others. Respondents such as CEOs, vice presidents, marketing directors, and technology and innovation directors have been interviewed to obtain and verify both qualitative and quantitative aspects of this research study.

The key data points taken from primary sources include:

- validation and triangulation of all the numbers and graphs

- validation of reports segmentation and key qualitative findings

- understanding the competitive landscape

- current and proposed production values of a particular product by market players

- validation of the numbers of various markets for market type

- percentage split of individual markets for regional analysis

Some of the key primary sources include:

- Godi India Pvt. Ltd.

- Morgan Advanced Materials

- Faraday Battery Challenge

- GODI energy

- Battery Mineral & Materials

- Cygni Energy Pvt. Ltd.

- Centre for Materials for Electronics Technology

- Batx Energies

- Norley Carbon & Graphite Consultants, LLC

- e-TRNL Energy

- Ola electric

- Fastmarkets

- Ango Zara Comercio E Industria Lda.

Secondary Research

This research study involves the usage of extensive secondary research, directories, company websites, and annual reports. It also makes use of databases, such as Hoovers, Bloomberg, Businessweek, Factiva, and One-Source, to collect useful and effective information for an extensive, technical, market-oriented, and commercial study of the global market. In addition to the data sources, the study has been undertaken with the help of other data sources and websites, such as www.weforum.org and www.trademap.org.

Secondary research was done to obtain crucial information about the industry's value chain, revenue models, the market's monetary chain, the total pool of key players, and current and potential use cases and applications.

The key data points taken from secondary research include:

- Segmentation breakups, split-ups, and percentage shares

- Data for market value

- Key industry trends of the top players of the market

- Qualitative insights into various aspects of the market, key trends, and emerging areas of innovation

- Quantitative data for mathematical and statistical calculations

Some of the key secondary sources include:

- International Energy Agency (IEA)

- International Renewable Energy Agency (IRENA)

- Energy Storage Association (ESA)

- German Association of Energy and Water Industries (BDEW)

- United States Energy Association (USEA)

- The Energy and Resources Institute (TERI)

- RenewableUK

- National Solar Energy Federation of India (NSEFI)

- International Solar Energy Society (ISES)

- Clean Energy Regulator (CER)

- Association of European Automotive and Industrial Battery Manufacturers (EUROBAT)

- OurEnergyPolicy Foundation

- China Association of Automobile Manufacturers (CAAM)

- International Battery Materials Association (IBA)

- Battery Association of Japan (BAJ)

Key Market Players and Competition Synopsis

The companies that are profiled have been selected based on inputs gathered from primary experts and analyzing company coverage, product portfolio, and market penetration.

Among the top players profiled in the report, the private companies operating in the global next-generation anode materials market accounted for around 73% of the market share in 2022, while the public companies operating in the market captured around 27% of the market share.

Some of the prominent names in this market are:

Private Companies:

|

Public Companies:

|

Table of Contents

1 Markets

- 1.1 Industry Outlook

- 1.1.1 Trends: Current and Future

- 1.1.1.1 Expanding Market of Next-Generation Anode Materials for Electric Vehicles

- 1.1.1.2 Focus on Silicon Recycling Promotes Applications in Lithium-Ion Batteries

- 1.1.1.3 Growing Demand for Solid-State Lithium-Metal Batteries in Various End-Use Applications

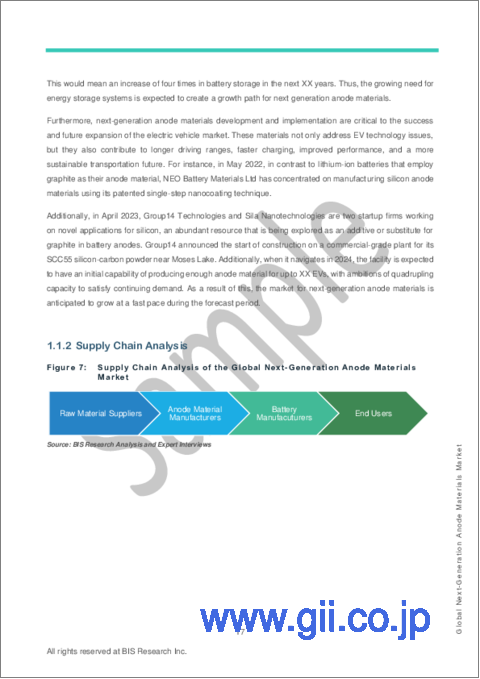

- 1.1.2 Supply Chain Analysis

- 1.1.3 Ecosystem of Global Next-Generation Anode Materials Market

- 1.1.3.1 Consortiums and Associations

- 1.1.3.2 Regulatory/Certification Bodies

- 1.1.3.3 Government Programs

- 1.1.3.4 Programs by Research Institutions and Universities

- 1.1.4 Comparison Analysis between Anode and Cathode Materials

- 1.1.5 Investment Scenario

- 1.1.1 Trends: Current and Future

- 1.2 Business Dynamics

- 1.2.1 Business Drivers

- 1.2.1.1 Increasing Need for Fast Charging and High-Density Batteries

- 1.2.1.2 Growing Demand of Silicon Material Due to Low Cost, Sustainable, and Abundant Nature

- 1.2.1.3 Increased Frequency of R&D Projects to Enhance Battery Composition

- 1.2.1.4 Increasing Investment in Advanced Energy Storage Technologies

- 1.2.2 Business Restraints

- 1.2.2.1 High Cost of Next-Generation Anode Materials

- 1.2.2.2 Lack of Large-Scale Production of High-Quality Graphene

- 1.2.2.3 Increased Volume and Degradation of Silicon Anodes

- 1.2.3 Business Strategies

- 1.2.3.1 Product and Market Development

- 1.2.4 Corporate Strategies

- 1.2.4.1 Mergers and Acquisitions, Partnerships, Collaborations, and Joint Ventures

- 1.2.5 Business Opportunities

- 1.2.5.1 Increasing Investment in Renewable Energy Sources

- 1.2.5.2 Growing Concern for the Environment and Carbon Neutrality Targets

- 1.2.5.3 Creating Resilient Binders for Assuring the Stability of Silicon Anodes

- 1.2.5.4 Designing New Electrolytes for Lithium Metal Batteries

- 1.2.1 Business Drivers

- 1.3 Start-Up Landscape

- 1.3.1 Key Start-Ups in the Ecosystem

2 Application

- 2.1 Global Next-Generation Anode Materials Market (Applications and Specifications)

- 2.1.1 Global Next-Generation Anode Materials Market (by End User)

- 2.1.1.1 Transportation

- 2.1.1.1.1 Passenger Electric Vehicles

- 2.1.1.1.2 Commercial Electric Vehicles

- 2.1.1.1.3 Others

- 2.1.1.2 Energy Storage

- 2.1.1.3 Electrical and Electronics

- 2.1.1.4 Others

- 2.1.1.1 Transportation

- 2.1.1 Global Next-Generation Anode Materials Market (by End User)

- 2.2 Demand Analysis of Global Next-Generation Anode Materials Market (by End User), Volume and Value Data

3 Products

- 3.1 Global Next-Generation Anode Materials Market (Products and Specifications)

- 3.1.1 Global Next-Generation Anode Materials Market (by Type)

- 3.1.1.1 Silicon/Silicon Oxide (Si/SiOx) Blend

- 3.1.1.2 Lithium Titanium Oxide

- 3.1.1.3 Silicon-Carbon Composite

- 3.1.1.4 Siliocn-Graphene Composite

- 3.1.1.5 Lithium Metal

- 3.1.1.6 Others

- 3.1.1 Global Next-Generation Anode Materials Market (by Type)

- 3.2 Comparative Analysis Between Types of Next-Generation Anode Materials

- 3.3 Demand Analysis of Global Next-Generation Anode Materials Market (by Type), Volume and Value Data

- 3.4 Product Benchmarking: Growth Rate - Market Share Matrix (by Type), 2022

- 3.5 Patent Analysis

- 3.5.1 Patent Analysis (by Status)

- 3.5.2 Patent Analysis (by Organization)

- 3.6 Pricing Analysis

- 3.6.1 Average Pricing Analysis, Next-Generation Anode Materials Market

4 Regions

- 4.1 North America

- 4.1.1 Market

- 4.1.1.1 Key Producers/Suppliers in North America

- 4.1.1.2 Business Drivers

- 4.1.1.3 Business Challenges

- 4.1.2 Application

- 4.1.2.1 North America Next-Generation Anode Materials Market (by End User), Volume and Value Data

- 4.1.3 Product

- 4.1.3.1 North America Next-Generation Anode Materials Market (by Type), Volume and Value Data

- 4.1.4 North America (by Country)

- 4.1.4.1 U.S.

- 4.1.4.1.1 Market

- 4.1.4.1.1.1 Buyer Attributes

- 4.1.4.1.1.2 Key Producers/Suppliers in the U.S.

- 4.1.4.1.1.3 Regulatory Landscape

- 4.1.4.1.1.4 Business Drivers

- 4.1.4.1.1.5 Business Challenges

- 4.1.4.1.2 Application

- 4.1.4.1.2.1 U.S. Next-Generation Anode Materials Market (by End User), Volume and Value Data

- 4.1.4.1.3 Product

- 4.1.4.1.3.1 U.S. Next-Generation Anode Materials Market (by Type), Volume and Value Data

- 4.1.4.1.1 Market

- 4.1.4.2 Canada

- 4.1.4.2.1 Market

- 4.1.4.2.1.1 Buyer Attributes

- 4.1.4.2.1.2 Key Producers/Suppliers in Canada

- 4.1.4.2.1.3 Regulatory Landscape

- 4.1.4.2.1.4 Business Drivers

- 4.1.4.2.1.5 Business Challenges

- 4.1.4.2.2 Application

- 4.1.4.2.2.1 Canada Next-Generation Anode Materials Market (by End User), Volume and Value Data

- 4.1.4.2.3 Product

- 4.1.4.2.3.1 Canada Next-Generation Anode Materials Market (by Type), Volume and Value Data

- 4.1.4.2.1 Market

- 4.1.4.3 Mexico

- 4.1.4.3.1 Market

- 4.1.4.3.1.1 Buyer Attributes

- 4.1.4.3.1.2 Key Producers/Suppliers in Mexico

- 4.1.4.3.1.3 Regulatory Landscape

- 4.1.4.3.1.4 Business Drivers

- 4.1.4.3.1.5 Business Challenges

- 4.1.4.3.2 Application

- 4.1.4.3.2.1 Mexico Next-Generation Anode Materials Market (by End User), Volume and Value Data

- 4.1.4.3.3 Product

- 4.1.4.3.3.1 Mexico Next-Generation Anode Materials Market (by Type), Volume and Value Data

- 4.1.4.3.1 Market

- 4.1.4.1 U.S.

- 4.1.1 Market

- 4.2 Europe

- 4.2.1 Market

- 4.2.1.1 Key Manufacturers/Suppliers in Europe

- 4.2.1.2 Business Drivers

- 4.2.1.3 Business Challenges

- 4.2.2 Application

- 4.2.2.1 Europe Next-Generation Anode Materials Market (by End User), Volume and Value Data

- 4.2.3 Product

- 4.2.3.1 Europe Next-Generation Anode Materials Market (by Type), Volume and Value Data

- 4.2.4 Europe (by Country)

- 4.2.4.1 Germany

- 4.2.4.1.1 Market

- 4.2.4.1.1.1 Buyer Attributes

- 4.2.4.1.1.2 Key Manufacturers/Suppliers in Germany

- 4.2.4.1.1.3 Regulatory Landscape

- 4.2.4.1.1.4 Business Drivers

- 4.2.4.1.1.5 Business Challenges

- 4.2.4.1.2 Application

- 4.2.4.1.2.1 Germany Next-Generation Anode Materials Market (by End User), Volume and Value Data

- 4.2.4.1.3 Product

- 4.2.4.1.3.1 Germany Next-Generation Anode Materials Market (by Type), Volume and Value Data

- 4.2.4.1.1 Market

- 4.2.4.2 Spain

- 4.2.4.2.1 Market

- 4.2.4.2.1.1 Buyer Attributes

- 4.2.4.2.1.2 Key Manufacturers/Suppliers in Spain

- 4.2.4.2.1.3 Regulatory Landscape

- 4.2.4.2.1.4 Business Drivers

- 4.2.4.2.1.5 Business Challenges

- 4.2.4.2.2 Application

- 4.2.4.2.2.1 Spain Next-Generation Anode Materials Market (by End User), Volume and Value Data

- 4.2.4.2.3 Product

- 4.2.4.2.3.1 Spain Next-Generation Anode Materials Market (by Type), Volume and Value Data

- 4.2.4.2.1 Market

- 4.2.4.3 Poland

- 4.2.4.3.1 Market

- 4.2.4.3.1.1 Buyer Attributes

- 4.2.4.3.1.2 Key Manufacturers/Suppliers in Poland:

- 4.2.4.3.1.3 Regulatory Landscape

- 4.2.4.3.1.4 Business Drivers

- 4.2.4.3.1.5 Business Challenges

- 4.2.4.3.2 Application

- 4.2.4.3.2.1 Poland Next-Generation Anode Materials Market (by End User), Volume and Value Data

- 4.2.4.3.3 Product

- 4.2.4.3.3.1 Poland Next-Generation Anode Materials Market (by Type), Volume and Value Data

- 4.2.4.3.1 Market

- 4.2.4.4 Hungary

- 4.2.4.4.1 Market

- 4.2.4.4.1.1 Buyer Attributes

- 4.2.4.4.1.2 Key Manufacturers/Suppliers in Hungary:

- 4.2.4.4.1.3 Regulatory Landscape

- 4.2.4.4.1.4 Business Drivers

- 4.2.4.4.1.5 Business Challenges

- 4.2.4.4.2 Application

- 4.2.4.4.2.1 Hungary Next-Generation Anode Materials Market (by End User), Volume and Value Data

- 4.2.4.4.3 Product

- 4.2.4.4.3.1 Hungary Next-Generation Anode Materials Market (by Type), Volume and Value Data

- 4.2.4.4.1 Market

- 4.2.4.5 Rest-of-Europe (RoE)

- 4.2.4.5.1 Market

- 4.2.4.5.1.1 Buyer Attributes

- 4.2.4.5.1.2 Key Manufacturers/Suppliers in Rest-of-Europe:

- 4.2.4.5.1.3 Business Drivers

- 4.2.4.5.1.4 Business Challenges

- 4.2.4.5.2 Application

- 4.2.4.5.2.1 Rest-of-Europe Next-Generation Anode Materials Market (by End User), Volume and Value Data

- 4.2.4.5.3 Product

- 4.2.4.5.3.1 Rest-of-Europe Next-Generation Anode Materials Market (by Type), Volume and Value Data

- 4.2.4.5.1 Market

- 4.2.4.1 Germany

- 4.2.1 Market

- 4.3 U.K.

- 4.3.1 Market

- 4.3.1.1 Buyer Attributes

- 4.3.1.2 Key Manufacturers/Suppliers in the U.K.

- 4.3.1.3 Regulatory Landscape

- 4.3.1.4 Business Drivers

- 4.3.1.5 Business Challenges

- 4.3.2 Application

- 4.3.2.1 U.K. Next-Generation Anode Materials Market (by End User), Volume and Value Data

- 4.3.3 Product

- 4.3.3.1 U.K. Next-Generation Anode Materials Market (by Type), Volume and Value Data

- 4.3.1 Market

- 4.4 China

- 4.4.1 Market

- 4.4.1.1 Buyer Attributes

- 4.4.1.2 Key Manufacturers/Suppliers in China

- 4.4.1.3 Regulatory Landscape

- 4.4.1.4 Business Drivers

- 4.4.1.5 Business Challenges

- 4.4.2 Application

- 4.4.2.1 China Next-Generation Anode Materials Market (by End User), Volume and Value Data

- 4.4.3 Product

- 4.4.3.1 China Next-Generation Anode Materials Market (by Type), Volume and Value Data

- 4.4.1 Market

- 4.5 Asia-Pacific and Japan

- 4.5.1 Market

- 4.5.1.1 Key Manufacturers/Suppliers in Asia-Pacific and Japan

- 4.5.1.2 Business Drivers

- 4.5.1.3 Business Challenges

- 4.5.2 Application

- 4.5.2.1 Asia-Pacific and Japan Next-Generation Anode Materials Market (by End User), Volume and Value Data

- 4.5.3 Product

- 4.5.3.1 Asia-Pacific and Japan Next-Generation Anode Materials Market (by Type), Volume and Value Data

- 4.5.4 Asia-Pacific and Japan (by Country)

- 4.5.4.1 Japan

- 4.5.4.1.1 Market

- 4.5.4.1.1.1 Buyer Attributes

- 4.5.4.1.1.2 Key Manufacturers/ Suppliers in Japan

- 4.5.4.1.1.3 Regulatory Landscape

- 4.5.4.1.1.4 Business Drivers

- 4.5.4.1.1.5 Business Challenges

- 4.5.4.1.2 Application

- 4.5.4.1.2.1 Japan Next-Generation Anode Materials Market (by End User), Volume and Value Data

- 4.5.4.1.3 Product

- 4.5.4.1.3.1 Japan Next-Generation Anode Materials Market (by Type), Volume and Value Data

- 4.5.4.1.1 Market

- 4.5.4.2 South Korea

- 4.5.4.2.1 Market

- 4.5.4.2.1.1 Buyer Attributes

- 4.5.4.2.1.2 Key Manufacturers/ Suppliers in South Korea

- 4.5.4.2.1.3 Regulatory Landscape

- 4.5.4.2.1.4 Business Drivers

- 4.5.4.2.1.5 Business Challenges

- 4.5.4.2.2 Application

- 4.5.4.2.2.1 South Korea Next-Generation Anode Materials Market (by End User), Volume and Value Data

- 4.5.4.2.3 Product

- 4.5.4.2.3.1 South Korea Next-Generation Anode Materials Market (by Type), Volume and Value Data

- 4.5.4.2.1 Market

- 4.5.4.3 India

- 4.5.4.3.1 Market

- 4.5.4.3.1.1 Buyer Attributes

- 4.5.4.3.1.2 Key Manufacturers/ Suppliers in India

- 4.5.4.3.1.3 Regulatory Landscape

- 4.5.4.3.1.4 Business Drivers

- 4.5.4.3.1.5 Business Challenges

- 4.5.4.3.2 Application

- 4.5.4.3.2.1 India Next-Generation Anode Materials Market (by End User), Volume and Value Data

- 4.5.4.3.3 Product

- 4.5.4.3.3.1 India Next-Generation Anode Materials Market (by Type), Volume and Value Data

- 4.5.4.3.1 Market

- 4.5.4.4 Rest-of-Asia-Pacific and Japan

- 4.5.4.4.1 Market

- 4.5.4.4.1.1 Buyer Attributes

- 4.5.4.4.1.2 Key Manufacturers/ Suppliers in the Rest-of-Asia-Pacific and Japan

- 4.5.4.4.1.3 Business Drivers

- 4.5.4.4.1.4 Business Challenges

- 4.5.4.4.2 Application

- 4.5.4.4.2.1 Rest-of-Asia-Pacific and Japan Next-Generation Anode Materials Market (by End User), Volume and Value Data

- 4.5.4.4.3 Product

- 4.5.4.4.3.1 Rest-of-Asia Pacific and Japan Next-Generation Anode Materials Market (by Type), Volume and Value Data

- 4.5.4.4.1 Market

- 4.5.4.1 Japan

- 4.5.1 Market

- 4.6 Rest-of-the-World

- 4.6.1 Market

- 4.6.1.1 Key Manufacturers/ Suppliers in the Rest-of-the-World

- 4.6.1.2 Business Drivers

- 4.6.1.3 Business Challenges

- 4.6.2 Application

- 4.6.2.1 Rest-of-the-World Next-Generation Anode Materials Market (by End User), Volume and Value Data

- 4.6.3 Product

- 4.6.3.1 Rest-of-the-World Next-Generation Anode Materials Market (by Type), Volume and Value Data

- 4.6.4 Rest-of-the-World (by Region)

- 4.6.4.1 South America

- 4.6.4.1.1 Market

- 4.6.4.1.1.1 Buyer Attributes

- 4.6.4.1.1.2 Key Manufacturers/ Suppliers in South America

- 4.6.4.1.1.3 Regulatory Landscape

- 4.6.4.1.1.4 Business Drivers

- 4.6.4.1.1.5 Business Challenges

- 4.6.4.1.2 Application

- 4.6.4.1.2.1 South America Next-Generation Anode Materials Market (by End User), Volume and Value Data

- 4.6.4.1.3 Product

- 4.6.4.1.3.1 South America Next-Generation Anode Materials Market (by Type), Volume and Value Data

- 4.6.4.1.1 Market

- 4.6.4.2 Middle East and Africa

- 4.6.4.2.1 Market

- 4.6.4.2.1.1 Buyer Attributes

- 4.6.4.2.1.2 Key Manufacturers/ Suppliers in the Middle East and Africa

- 4.6.4.2.1.3 Regulatory Landscape

- 4.6.4.2.1.4 Business Drivers

- 4.6.4.2.1.5 Business Challenges

- 4.6.4.2.2 Application

- 4.6.4.2.2.1 Middle East and Africa Next-Generation Anode Materials Market (by End User), Volume and Value Data

- 4.6.4.2.3 Product

- 4.6.4.2.3.1 Middle East and Africa Next-Generation Anode Materials Market (by Type), Volume and Value Data

- 4.6.4.2.1 Market

- 4.6.4.1 South America

- 4.6.1 Market

5 Markets - Competitive Benchmarking & Company Profiles

- 5.1 Competitive Benchmarking

- 5.1.1 Competitive Position Matrix

- 5.1.2 Product Matrix of Key Companies (by Type)

- 5.1.3 Market Share Analysis of Key Companies, 2022

- 5.2 Company Profiles

- 5.2.1 Altairnano

- 5.2.1.1 Company Overview

- 5.2.1.1.1 Role of Altairnano in the Global Next-Generation Anode Materials Market

- 5.2.1.1.2 Product Portfolio

- 5.2.1.2 Analyst View

- 5.2.1.1 Company Overview

- 5.2.2 LeydnJar Technologies BV

- 5.2.2.1 Company Overview

- 5.2.2.1.1 Role of LeydnJar Technologies BV in the Global Next-Generation Anode Materials Market

- 5.2.2.1.2 Product Portfolio

- 5.2.2.2 Business Strategies

- 5.2.2.2.1 Product Development

- 5.2.2.2.2 Market Development

- 5.2.2.3 Corporate Strategies

- 5.2.2.3.1 Partnerships, Collaborations, and Joint Ventures

- 5.2.2.4 Analyst View

- 5.2.2.1 Company Overview

- 5.2.3 Nexeon Ltd.

- 5.2.3.1 Company Overview

- 5.2.3.1.1 Role of Nexeon Ltd. in the Global Next-Generation Anode Materials Market

- 5.2.3.1.2 Product Portfolio

- 5.2.3.2 Business Strategies

- 5.2.3.2.1 Market Development

- 5.2.3.3 Corporate Strategies

- 5.2.3.3.1 Partnerships, Collaborations, and Joint Ventures

- 5.2.3.4 Analyst View

- 5.2.3.1 Company Overview

- 5.2.4 pH Matter LLC

- 5.2.4.1 Company Overview

- 5.2.4.1.1 Role of pH Matter LLC in the Global Next-Generation Anode Materials Market

- 5.2.4.1.2 Product Portfolio

- 5.2.4.2 Business Strategies

- 5.2.4.2.1 Product Development

- 5.2.4.3 Corporate Strategies

- 5.2.4.3.1 Partnerships, Collaborations, and Joint Ventures

- 5.2.4.4 Analyst View

- 5.2.4.1 Company Overview

- 5.2.5 Sila Nanotechnologies Inc.

- 5.2.5.1 Company Overview

- 5.2.5.1.1 Role of Sila Nanotechnologies Inc. in the Global Next-Generation Anode Materials Market

- 5.2.5.1.2 Product Portfolio

- 5.2.5.2 Business Strategies

- 5.2.5.2.1 Market Development

- 5.2.5.3 Corporate Strategies

- 5.2.5.3.1 Partnerships, Collaborations, and Joint Ventures

- 5.2.5.4 Analyst View

- 5.2.5.1 Company Overview

- 5.2.6 Cuberg

- 5.2.6.1 Company Overview

- 5.2.6.1.1 Role of Cuberg in the Global Next-Generation Anode Materials Market

- 5.2.6.1.2 Product Portfolio

- 5.2.6.2 Business Strategies

- 5.2.6.2.1 Market Development

- 5.2.6.3 Analyst View

- 5.2.6.1 Company Overview

- 5.2.7 Shanghai Shanshan Technology Co., Ltd.

- 5.2.7.1 Company Overview

- 5.2.7.1.1 Role of Shanghai Shanshan Technology Co., Ltd. in the Global Next-Generation Anode Materials Market

- 5.2.7.1.2 Product Portfolio

- 5.2.7.2 Business Strategies

- 5.2.7.2.1 Market Development

- 5.2.7.3 Analyst View

- 5.2.7.1 Company Overview

- 5.2.8 AMPIRUS TECHNOLOGIES

- 5.2.8.1 Company Overview

- 5.2.8.1.1 Role of AMPIRUS TECHNOLOGIES in the Global Next-Generation Anode Materials Market

- 5.2.8.1.2 Product Portfolio

- 5.2.8.1.3 Production Sites

- 5.2.8.2 Business Strategies

- 5.2.8.2.1 Market Development

- 5.2.8.3 Corporate Strategies

- 5.2.8.3.1 Partnerships, Collaborations, and Joint Ventures

- 5.2.8.4 R&D Analysis

- 5.2.8.5 Analyst View

- 5.2.8.1 Company Overview

- 5.2.9 California Lithium Battery

- 5.2.9.1 Company Overview

- 5.2.9.1.1 Role of California Lithium Battery in the Global Next-Generation Anode Materials Market

- 5.2.9.1.2 Product Portfolio

- 5.2.9.1.3 Production Sites

- 5.2.9.2 Analyst View

- 5.2.9.1 Company Overview

- 5.2.10 Enovix

- 5.2.10.1 Company Overview

- 5.2.10.1.1 Role of Enovix in the Global Next-Generation Anode Materials Market

- 5.2.10.1.2 Product Portfolio

- 5.2.10.2 Business Strategies

- 5.2.10.2.1 Market Development

- 5.2.10.3 Analyst View

- 5.2.10.1 Company Overview

- 5.2.11 Albemarle Corporation

- 5.2.11.1 Company Overview

- 5.2.11.1.1 Role of Albemarle Corporation in the Global Next-Generation Anode Materials Market

- 5.2.11.1.2 Product Portfolio

- 5.2.11.2 Business Strategies

- 5.2.11.2.1 Market Development

- 5.2.11.3 Corporate Strategies

- 5.2.11.3.1 Partnerships, Collaborations, and Joint Ventures

- 5.2.11.4 R&D Analysis

- 5.2.11.5 Analyst View

- 5.2.11.1 Company Overview

- 5.2.12 Talga Group.

- 5.2.12.1 Company Overview

- 5.2.12.1.1 Role of Talga Group. in the Global Next-Generation Anode Materials Market

- 5.2.12.1.2 Product Portfolio

- 5.2.12.2 Business Strategies

- 5.2.12.2.1 Market Development

- 5.2.12.3 Corporate Strategies

- 5.2.12.3.1 Partnerships, Collaborations, and Joint Ventures

- 5.2.12.4 Analyst View

- 5.2.12.1 Company Overview

- 5.2.13 Tianqi Lithium Corporation

- 5.2.13.1 Company Overview

- 5.2.13.1.1 Role of Tianqi Lithium Corporation in the Global Next-Generation Anode Materials Market

- 5.2.13.1.2 Product Portfolio

- 5.2.13.1.3 Production Sites

- 5.2.13.2 Analyst View

- 5.2.13.1 Company Overview

- 5.2.14 Jiangxi Ganfeng Lithium Co., Ltd.

- 5.2.14.1 Company Overview

- 5.2.14.1.1 Role of Jiangxi Ganfeng Lithium Co., Ltd. in the Global Next-Generation Anode Materials Market

- 5.2.14.1.2 Product Portfolio

- 5.2.14.1.3 Production Sites

- 5.2.14.2 Business Strategies

- 5.2.14.2.1 Market Development

- 5.2.14.3 Corporate Strategies

- 5.2.14.3.1 Partnerships, Collaborations, and Joint Ventures

- 5.2.14.4 R&D Analysis

- 5.2.14.5 Analyst View

- 5.2.14.1 Company Overview

- 5.2.15 POSCO CHEMICAL

- 5.2.15.1 Company Overview

- 5.2.15.1.1 Role of POSCO CHEMICAL in the Global Next-Generation Anode Materials Market

- 5.2.15.1.2 Product Portfolio

- 5.2.15.1.3 Production Sites

- 5.2.15.2 Business Strategies

- 5.2.15.2.1 Market Development

- 5.2.15.3 Corporate Strategies

- 5.2.15.3.1 Partnerships, Collaborations, and Joint Ventures

- 5.2.15.4 Analyst View

- 5.2.15.1 Company Overview

- 5.2.1 Altairnano

6 Research Methodology

- 6.1 Primary Data Sources

- 6.2 BIS Data Sources

- 6.3 Assumptions and Limitations