|

|

市場調査レポート

商品コード

1784623

欧州のデータセンター向けプラガブルオプティクス市場の分析(2021~2031年):市場範囲・区分・動向・競合分析Europe Pluggable Optics for Data Center Market Report 2021-2031 by Scope, Segmentation, Dynamics, and Competitive Analysis |

||||||

|

|||||||

|

|||||||

| 欧州のデータセンター向けプラガブルオプティクス市場の分析(2021~2031年):市場範囲・区分・動向・競合分析 |

|

出版日: 2025年07月10日

発行: The Insight Partners

ページ情報: 英文 161 Pages

納期: 即納可能

|

全表示

- 概要

- 図表

- 目次

欧州のデータセンター向けプラガブルオプティクスの市場規模は、2023年の9億2,890万米ドルから2031年には21億1,333万米ドルに達すると予測されています。同市場は、2023~2031年にCAGR 10.8%を記録すると予測されています。

エグゼクティブサマリー - 欧州のデータセンター向けプラガブルオプティクス市場分析

ドイツ、フランス、英国、イタリアは、欧州のデータセンター向けプラガブルオプティクス市場成長に貢献している主要国です。データ量全体が指数関数的に増加しており、欧州のデータセンタ業界では強い需要が生じています。人工知能(AI)、機械学習(ML)、モノのインターネット(IoT)など急速に拡大する技術がプラガブルオプティクスの需要を押し上げており、今後3~5年は供給を上回り続けると見られています。例えば、2024年6月に発表されたTMT Consultants Ltdのデータによると、欧州のデータセンタではAI技術とデータストレージ容量の利用が拡大しています。これにより、より多くの処理能力に対する需要が高まり、AIベースのラックを数台追加することから、完全にAIに対応したセンターまで、さまざまな方法でデータセンターの設計がさらに変化します。この動向を受けて、ハイパースケーラはラック密度を2027年までに1ラックあたり50kWまで引き上げます。AI対応データセンタの開発は、ネットワークの可用性を高め、メンテナンス手順を簡素化するためにプラガブルオプティクスの採用を急増させています。さらに、欧州では主に電力供給の問題からAIの採用が大幅に増加しています。データセンターをAI対応にするには、AIの電力および冷却要件の増加に対応できる十分な容量を確保する必要があります。このため、HDR, Inc.もAI対応データセンターの開発に力を入れるようになりました。AI技術は、データセンターの自動化、監視、エネルギー効率の最適化を推進し、障害を迅速に特定する上でオペレーターをサポートします。このような新規建設やAIベースのデータセンターは、最適な作業環境を確保するためのプラガブルオプティクスの必要性を引き起こしています。

欧州のデータセンター向けプラガブルオプティクス市場 - セグメント別分析:

データセンター向けプラガブルオプティクス市場の分析に寄与した主要セグメントは、コンポーネントとデータレートです。

コンポーネントに基づいて、欧州はスイッチ、ルータ、サーバにセグメント化されます。スイッチは、2023年に市場で最大シェアを占めています。

データレート別では、欧州は100~400GB/S、400~800GB/S、800GB/S以上に区分されます。2023年には400-800GB/Sセグメントが最大シェアを占めています。

欧州のデータセンター向けプラガブルオプティクス市場 - 展望

プラガブルオプティクスにより、データセンタオペレータは、ケーブルシステムを完全に再構築することなく、トランシーバのアップグレードや交換を容易に行うことができます。データセンタにおけるプラガブルオプティクス需要の高まりは、顧客のダイナミックな要求に応えることができる新しい革新的製品の開発をメーカーに促しています。例えば、2024年3月、Infinera Corporationは、データセンター内の接続性を向上させるICE-Dの新しい製品ラインを発表しました。ICE-Dは、モノリシックリン化インジウム(InP)とフォトニック集積回路(PIC)技術に基づく高速データセンター内オプティクスの新ラインナップです。ICE-Dオプティクスは、1.6テラビット/秒(Tb/s)以上の速度でデータセンター内接続を提供しながら、ビットあたりのコストと電力を大幅に削減するように設計されています。この技術により、データセンター事業者はコスト効率に優れながら、増え続ける帯域幅需要に対応することができます。この新しいICE-Dデータセンター内オプティクスは、幅広いデータセンター内およびキャンパス内オプティカルソリューションに統合できるように設計されています。これらのソリューションには、デジタルシグナルプロセッサ(DSP)ベースのリタイミングオプティクス、リニアドライブプラガブルオプティクス(LPO)、シリアルおよびパラレルファイバーアプリケーション用のコパッケージオプティクス(CPO)が含まれます。以下に、データセンター向けプラガブルオプティクスの開発をいくつか紹介します:

2023年12月、コヒレント(Coherent Corp)は、光通信ネットワーク向けに超小型QSFP-DDとOSFPフォームファクタの800G ZR/ZR+トランシーバを発表しました。コヒレント社の800G ZR/ZR+トランシーバは、IPルータのQSFP-DDおよびOSFPトランシーバ・スロットに直接差し込むことができる世界初のデジタル・コヒーレント・オプティクス(DCO)です。0dBmの高出力を活用することで、これらのトランシーバは、中間インタフェースを追加することなく、ルータをアクセスメトロや地域DWDMトランスポートネットワークに直接接続することができ、光機器の全レイヤが不要になるため、設備投資と運用コストの両方を大幅に削減することができます。2023年3月、インフィネラコーポレーションは、コヒレント光サブシステムとコヒレントプラガブル光エンジンの新しいポートフォリオを発表しました。これらの製品は、ネットワーク事業者が二酸化炭素排出量を削減し、コスト効率に優れながら増え続ける帯域幅需要に対応できるように設計されています。新しいソリューションには、高性能送受信光サブアセンブリ(TROSA)、革新的なプログラマブル・デジタル・シグナル・プロセッサ(DSP)、高性能インテリジェント・プラガブル光トランシーバの製品ラインが含まれます。データセンターでは、スイッチやルーター一式を交換することなく、帯域幅需要の変化に迅速に対応できるプラガブル光トランシーバーの使用と需要が高まっており、動的な状況に理想的な選択肢となっています。さらに、プラガブルオプティクスはデータセンター事業者の高速伝送をサポートし、電力を最適化し、高速伝送を促進し、ネットワークアーキテクチャを簡素化します。このように、コスト効果の高いソリューションへの好みが高まっており、メーカーが製品開発活動に注力していることが、データセンター向けプラガブルオプティクス市場の成長に大きく寄与しています。

欧州のデータセンター向けプラガブルオプティクス市場 - 国別考察

国別に見ると、欧州のデータセンター向けプラガブルオプティクス市場は、ドイツ、英国、フランス、イタリア、ロシア、その他欧州で構成されます。2023年はドイツが最大シェア。

ドイツのデータセンター向けプラガブルオプティクス市場は、コロケーションデータセンタの投資拡大とITキャパシティの増加により、今後数年で大きく拡大すると予測されています。GERMAN DATACENTER ASSOCIATIONが発表した「Data Center Impact Report, Germany 2024」によると、ドイツのデータセンタは、2029年までにコロケーション容量拡大のために265億8,000万米ドル(240億ユーロ)以上の投資が見込まれています。前述の同じ情報源によると、ドイツのコロケーション・データセンターのIT容量は、2029年までに130万kWから33万kWに拡大すると予想されています。データセンターの新興国市場の拡大、データ処理需要の増加、データセンター開発投資の増加などが市場を牽引する要因となっています。

欧州のデータセンター向けプラガブルオプティクス市場 - 企業プロファイル

データセンター向けプラガブルオプティクス市場で事業を展開している主要企業には、Coherent Corp、Nokia Corp、Cisco Systems I、Infinera Corp、Telefonaktiebolaget LM Ericsson、Ciena Corp、Intel Corp、Lumentum Holdings Inc、Juniper Networks Inc、Marvell Technology Inc、Broadcom Incなどがあります。これらの企業は、消費者に革新的な製品を提供し、市場シェアを拡大するために、事業拡大、製品革新、M&Aなど様々な戦略を採用しています。

欧州のデータセンター向けプラガブルオプティクス市場 - 分析手法:

当レポートで紹介するデータの収集と分析には、以下の調査手法を採用しています:

二次調査の調査プロセスは、各市場の質的・量的データを収集するために、社内外の情報源を活用した包括的な二次調査から始まります。一般的に参照される二次調査情報源は以下の通りであるが、これらに限定されるものではありません:

企業のウェブサイト、年次報告書、財務諸表、ブローカーの分析、投資家のプレゼンテーション。業界専門誌、その他関連出版物政府文書、統計データベース、市場レポートニュース記事、プレスリリース、ウェブキャスト。ただし、企業プロファイルに含まれる財務データはすべて米ドルに統一されています。他の通貨で報告されている企業の数値は、該当年の関連為替レートを使用して米ドルに換算されています。

一次調査:インサイト・パートナーズでは、データ分析を検証し、貴重な知見を得るために、毎年、業界利害関係者や専門家に相当数の1次インタビューを実施しています。これらの調査は、以下を目的としています:

二次調査の結果を検証し、改良します。分析チームの専門知識と市場理解を深める。市場規模、動向、成長パターン、競合力学、将来の見通しに関する考察を得る。1次調査は、様々な市場、カテゴリー、セグメント、サブセグメントを対象とし、Eメールでのやり取りや電話インタビューで実施します。参加者は通常以下の通りです:

業界の利害関係者(副社長、事業開発マネージャー、マーケット・インテリジェンス・マネージャー、国内営業マネージャー)、業界固有の専門知識を持つ外部専門家(評価専門家、リサーチアナリスト、国内営業マネージャー、主要オピニオンリーダー)

目次

第1章 イントロダクション

第2章 エグゼクティブサマリー

- 主要洞察

- 市場の魅力

第3章 分析手法

- 二次調査

- 一次調査

- 仮説の策定

- マクロ経済要因分析

- 基礎数値の動向

- データの三角測量

- 国レベルのデータ

第4章 欧州のデータセンター向けプラガブルオプティクス市場の情勢

- エコシステム分析

- バリューチェーンのベンダー一覧

第5章 欧州のデータセンター向けプラガブルオプティクス市場:主な市場力学

- 市場促進要因

- 各メーカーの製品開発への注力

- 高性能コンピューティングへのニーズの高まり

- 市場抑制要因

- ネットワークの複雑化

- 市場機会

- 高性能AIインフラにおけるプラガブルオプティクスの需要

- エネルギー効率に対する需要

- 今後の動向

- 線形プラガブルオプティクス

- 促進要因と抑制要因の影響

第6章 データセンター向けプラガブルオプティクス市場:欧州市場の分析

- 欧州のデータセンター向けプラガブルオプティクス市場の収益 (2021~2031年)

- 欧州のデータセンター向けプラガブルオプティクス市場の予測・分析

第7章 欧州のデータセンター向けプラガブルオプティクス市場の分析:コンポーネント別

- スイッチ

- ルーター

- サーバ

第8章 欧州のデータセンター向けプラガブルオプティクス市場の分析:データレート別

- 100~400GB/S

- 400~800GB/S

- 800GB/S以上

第9章 欧州のデータセンター向けプラガブルオプティクス市場:国別分析

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- ロシア

- その他欧州

第12章 競合情勢

- ヒートマップ分析

- 企業のポジショニングと集中度

第13章 業界情勢

- 市場イニシアティブ

- 製品開発

- 企業合併・買収 (M&A)

第12章 企業プロファイル

- Coherent Corp

- Nokia Corp

- Cisco Systems Inc

- Infinera Corp

- Telefonaktiebolaget LM Ericsson

- Ciena Corp

- Intel Corp

- Lumentum Holdings Inc

- Juniper Networks Inc

- Marvell Technology Inc

- Yangtze Optical Fibre and Cable Joint Stock Ltd

- Broadcom Inc

第13章 付録

List Of Tables

- Table 1. Europe Pluggable Optics for Data Center Market Segmentation

- Table 2. List of Vendors

- Table 3. Europe Pluggable Optics for Data Center Market - Revenue and Forecast, 2021-2031 (US$ Million)

- Table 4. Europe Pluggable Optics for Data Center Market - Revenue and Forecast, 2021-2031 (US$ Million) - by Component

- Table 5. Europe Pluggable Optics for Data Center Market - Revenue and Forecast, 2021-2031 (US$ Million) - by Data Rate

- Table 6. Europe Pluggable Optics for Data Center Market - Revenue and Forecast, 2021-2031 (US$ Million) - by Country

- Table 7. Germany: Europe Pluggable Optics for Data Center Market - Revenue and Forecast, 2021 - 2031 (US$ Million) - by Component

- Table 8. Germany: Europe Pluggable Optics for Data Center Market - Revenue and Forecast, 2021 - 2031 (US$ Million) - by Data Rate

- Table 9. United Kingdom: Europe Pluggable Optics for Data Center Market - Revenue and Forecast, 2021 - 2031 (US$ Million) - by Component

- Table 10. United Kingdom: Europe Pluggable Optics for Data Center Market - Revenue and Forecast, 2021 - 2031 (US$ Million) - by Data Rate

- Table 11. France: Europe Pluggable Optics for Data Center Market - Revenue and Forecast, 2021 - 2031 (US$ Million) - by Component

- Table 12. France: Europe Pluggable Optics for Data Center Market - Revenue and Forecast, 2021 - 2031 (US$ Million) - by Data Rate

- Table 13. Italy: Europe Pluggable Optics for Data Center Market - Revenue and Forecast, 2021 - 2031 (US$ Million) - by Component

- Table 14. Italy: Europe Pluggable Optics for Data Center Market - Revenue and Forecast, 2021 - 2031 (US$ Million) - by Data Rate

- Table 15. Russia: Europe Pluggable Optics for Data Center Market - Revenue and Forecast, 2021 - 2031 (US$ Million) - by Component

- Table 16. Russia: Europe Pluggable Optics for Data Center Market - Revenue and Forecast, 2021 - 2031 (US$ Million) - by Data Rate

- Table 17. Rest of Europe: Europe Pluggable Optics for Data Center Market - Revenue and Forecast, 2021 - 2031 (US$ Million) - by Component

- Table 18. Rest of Europe: Europe Pluggable Optics for Data Center Market - Revenue and Forecast, 2021 - 2031 (US$ Million) - by Data Rate

- Table 19. List of Abbreviation

List Of Figures

- Figure 1. Europe Pluggable Optics for Data Center Market Segmentation - Country

- Figure 2. Europe Pluggable Optics for Data Center Market - Key Market Dynamics

- Figure 3. Impact Analysis of Drivers and Restraints

- Figure 4. Europe Pluggable Optics for Data Center Market Revenue (US$ Million), 2021-2031

- Figure 5. Europe Pluggable Optics for Data Center Market Share (%) - by Component (2023 and 2031)

- Figure 6. Switches: Europe Pluggable Optics for Data Center Market - Revenue and Forecast, 2021-2031 (US$ Million)

- Figure 7. Routers: Europe Pluggable Optics for Data Center Market - Revenue and Forecast, 2021-2031 (US$ Million)

- Figure 8. Servers: Europe Pluggable Optics for Data Center Market - Revenue and Forecast, 2021-2031 (US$ Million)

- Figure 9. Europe Pluggable Optics for Data Center Market Share (%) - by Data Rate (2023 and 2031)

- Figure 10.-400GB/S: Europe Pluggable Optics for Data Center Market - Revenue and Forecast, 2021-2031 (US$ Million)

- Figure 11.-800GB/S: Europe Pluggable Optics for Data Center Market - Revenue and Forecast, 2021-2031 (US$ Million)

- Figure 12.GB/S and Above: Europe Pluggable Optics for Data Center Market - Revenue and Forecast, 2021-2031 (US$ Million)

- Figure 13. Europe Pluggable Optics for Data Center Market Breakdown, by Key Countries, 2023 and 2031 (%)

- Figure 14. Germany: Europe Pluggable Optics for Data Center Market - Revenue and Forecast, 2021- 2031 (US$ Million)

- Figure 15. United Kingdom: Europe Pluggable Optics for Data Center Market - Revenue and Forecast, 2021- 2031 (US$ Million)

- Figure 16. France: Europe Pluggable Optics for Data Center Market - Revenue and Forecast, 2021- 2031 (US$ Million)

- Figure 17. Italy: Europe Pluggable Optics for Data Center Market - Revenue and Forecast, 2021- 2031 (US$ Million)

- Figure 18. Russia: Europe Pluggable Optics for Data Center Market - Revenue and Forecast, 2021- 2031 (US$ Million)

- Figure 19. Rest of Europe: Europe Pluggable Optics for Data Center Market - Revenue and Forecast, 2021- 2031 (US$ Million)

- Figure 20. Company Heat Map Analysis

- Figure 21. Company Positioning and Concentration

The Europe pluggable optics for data center market size is expected to reach US$ 2,113.33 million by 2031 from US$ 928.90 million in 2023. The market is estimated to record a CAGR of 10.8% from 2023 to 2031.

Executive Summary and Europe Pluggable Optics for Data Center Market Analysis:

Germany, France, the UK, and Italy are among the key countries contributing to the growth of the European pluggable optics for data center market. The overall volume of data is increasing exponentially, resulting in strong demand in the European data center industry. Rapidly expanding technologies such as artificial intelligence (AI), machine learning (ML), and the Internet of Things (IoT) are driving up demand for pluggable optics, which is expected to continue to surpass supply over the next three to five years. For instance, according to TMT Consultants Ltd data published in June 2024, the use of AI technology and data storage capacity is growing in European data centers. This increases the demand for more processing power, which further changes the data center design in a variety of ways, from adding a few AI-based racks to fully AI-enabled centers. In response to this trend, hyperscalers will raise rack density to 50kW per rack by 2027. The development of AI-enabled data centers surges the adoption of pluggable optics to enhance network availability and simplify maintenance procedures. Moreover, the adoption of AI in Europe is significantly increasing, primarily due to power supply difficulties. Making data centers AI-ready entails ensuring that they have sufficient capacity to meet AI's increased power and cooling requirements. This also increased HDR, Inc's focus on the development of AI-enabled data centers. AI technology supports operators in promoting automation, monitoring, and optimizing energy efficiencies in data centers, as well as quickly identifying faults. Such new construction and AI-based data centers trigger the need for pluggable optics to ensure optimal working environments.

Europe Pluggable Optics for Data Center Market Segmentation Analysis:

Key segments that contributed to the derivation of the Europe pluggable optics for data center market analysis are component and data rate.

Based on component, the Europe is segmented into switches, routers, and servers. The switches held the largest share of the market in 2023.

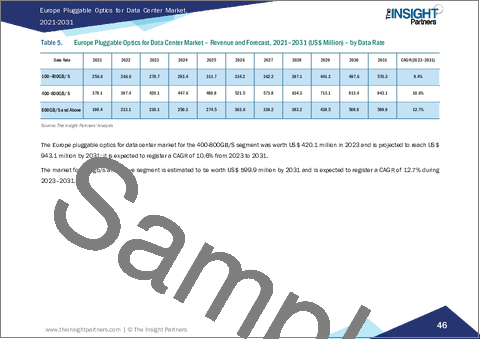

By data rate, the Europe is segmented into 100-400GB/S, 400-800GB/S, and 800GB/S and Above. The 400-800GB/S segment held the largest share of the market in 2023.

Europe Pluggable Optics for Data Center Market Outlook

Pluggable optics enable data center operators to easily upgrade or replace transceivers without having to completely rebuild the cable system. The rising demand for pluggable optics in data centers encourages manufacturers to develop new innovative products that are capable of meeting the dynamic requirements of customers. For instance, in March 2024, Infinera Corporation launched a new line of ICE-D to improve intra-data center connectivity. ICE-D, a new line of high-speed intra-data center optics based on monolithic indium phosphide (InP) and photonic integrated circuit (PIC) technology. ICE-D optics are designed to significantly reduce cost and power per bit while offering intra-data center connectivity at speeds of 1.6 terabits per second (Tb/s) or more. This technology allows data center operators to keep up with the ever-increasing demand for bandwidth while being cost-effective. This new ICE-D intra-data center optics are designed to be integrated into a wide range of intra- and campus data center optical solutions. These solutions include digital signal processor (DSP)-based retimed optics, linear-drive pluggable optics (LPO), and co-packaged optics (CPO) for both serial and parallel fiber applications. Below mentioned are a few developments in pluggable optics for data centers:

In December 2023, Coherent Corp introduced its 800G ZR/ZR+ transceiver in ultracompact QSFP-DD and OSFP form factors for optical communications networks. The 800G ZR/ZR+ transceivers from Coherent are the world's first digital coherent optics (DCO) that can plug directly into QSFP-DD and OSFP transceiver slots on IP routers. Leveraging their high output power of 0 dBm, these transceivers can connect routers directly to access metro and regional DWDM transport networks without additional intermediary interfaces, eliminating an entire layer of optical equipment and thereby significantly reducing both capital and operational expenditures. In March 2023, Infinera Corporation launched a new portfolio of coherent optical subsystems and coherent pluggable optical engines. These products are designed to help network operators reduce their carbon footprint and meet the ever-increasing demand for bandwidth while being cost-effective. The new solutions include a line of high-performance transmit-receive optical sub-assemblies (TROSAs), innovative programmable digital signal processors (DSPs), and a line of high-performance, intelligent pluggable optical transceivers. Data centers are increasingly using and demanding pluggable optics for swiftly adjusting to changing bandwidth demands without having to replace complete switches or routers, which makes them an ideal choice for dynamic situations. Moreover, pluggable optics support data center operators in high-speed transmission, optimize power, promote high-speed transmission, and simplify network architecture. Thus, the increasing preference for cost-effective solutions and manufacturers' focus on product development activities contribute significantly to the growth of pluggable optics for data center market.

Europe Pluggable Optics for Data Center Market Country Insights

Based on country, the Europe pluggable optics for data center market comprises Germany, the UK, France, Italy, Russia, and the Rest of Europe. Germany held the largest share in 2023.

The pluggable optics for data center market in Germany is projected to expand at a significant rate in the upcoming years due to the growing investment and increasing IT capacity of colocation data centers. According to a Data Center Impact Report, Germany 2024, published by the GERMAN DATACENTER ASSOCIATION, data center in Germany is expected to receive an investment of more than US$ 26.58 billion (24 billion euros) for the expansion of colocation capacity by 2029. According to the same source mentioned above, the IT capacity of colocation data centers in Germany is expected to expand from 1.3 GW to 3.3 GW by 2029. The growing capacity expansion of data centers, increase in data processing demand, and increasing investment to develop data centers are among the factors driving the market.

Europe Pluggable Optics for Data Center Market Company Profiles

Some of the key players operating in the pluggable optics for data center market include Coherent Corp, Nokia Corp, Cisco Systems I, Infinera Corp, Telefonaktiebolaget LM Ericsson, Ciena Corp, Intel Corp, Lumentum Holdings Inc, Juniper Networks Inc, Marvell Technology Inc, and Broadcom Inc among others. These players are adopting various strategies such as expansion, product innovation, and mergers and acquisitions to provide innovative products to their consumers and increase their market share.

Europe Pluggable Optics for Data Center Market Research Methodology :

The following methodology has been followed for the collection and analysis of data presented in this report:

Secondary Research The research process begins with comprehensive secondary research, utilizing both internal and external sources to gather qualitative and quantitative data for each market. Commonly referenced secondary research sources include, but are not limited to:

Company websites , annual reports, financial statements, broker analyses, and investor presentations. Industry trade journals and other relevant publications. Government documents , statistical databases, and market reports. News articles , press releases, and webcasts specific to companies operating in the market. Note: All financial data included in the Company Profiles section has been standardized to USD. For companies reporting in other currencies, figures have been converted to USD using the relevant exchange rates for the corresponding year.

Primary Research The Insight Partners' conducts a significant number of primary interviews each year with industry stakeholders and experts to validate its data analysis, and gain valuable insights. These research interviews are designed to:

Validate and refine findings from secondary research. Enhance the expertise and market understanding of the analysis team. Gain insights into market size, trends, growth patterns, competitive dynamics, and future prospects. Primary research is conducted via email interactions and telephone interviews, encompassing various markets, categories, segments, and sub-segments across different regions. Participants typically include:

Industry stakeholders : Vice Presidents, business development managers, market intelligence managers, and national sales managers External experts : Valuation specialists, research analysts, and key opinion leaders with industry-specific expertise

Table Of Contents

1. Introduction

- 1.1 Report Guidance

- 1.2 Market Segmentation

2. Executive Summary

- 2.1 Key Insights

- 2.2 Market Attractiveness

3. Research Methodology

- 3.1 Secondary Research

- 3.2 Primary Research

- 3.2.1 Hypothesis formulation:

- 3.2.2 Macroeconomic factor analysis:

- 3.2.3 Developing base number:

- 3.2.4 Data Triangulation:

- 3.2.5 Country-level data:

4. Europe Pluggable Optics for Data Center Market Landscape

- 4.1 Overview

- 4.2 Ecosystem Analysis

- 4.3 List of Vendors in the Value Chain

5. Europe Pluggable Optics for Data Center Market - Key Market Dynamics

- 5.1 Market Drivers

- 5.1.1 Manufacturers Focus on Product Development

- 5.1.2 Rising Need for High-Performance Computing

- 5.2 Market Restraints

- 5.2.1 Rising Network Complexity

- 5.3 Market Opportunities

- 5.3.1 Demand for Pluggable Optics in High-Performance AI Infrastructure

- 5.3.2 Demand for Energy Efficiency

- 5.4 Trends

- 5.4.1 Linear Pluggable Optics

- 5.5 Impact of Drivers and Restraints:

6. Pluggable Optics for Data Center Market - Europe Analysis

- 6.1 Europe Pluggable Optics for Data Center Market Revenue (US$ Million), 2021-2031

- 6.2 Europe Pluggable Optics for Data Center Market Forecast Analysis

7. Europe Pluggable Optics for Data Center Market Analysis - by Component

- 7.1 Switches

- 7.1.1 Overview

- 7.1.2 Switches: Europe Pluggable Optics for Data Center Market - Revenue and Forecast, 2021-2031 (US$ Million)

- 7.2 Routers

- 7.2.1 Overview

- 7.2.2 Routers: Europe Pluggable Optics for Data Center Market - Revenue and Forecast, 2021-2031 (US$ Million)

- 7.3 Servers

- 7.3.1 Overview

- 7.3.2 Servers: Europe Pluggable Optics for Data Center Market - Revenue and Forecast, 2021-2031 (US$ Million)

8. Europe Pluggable Optics for Data Center Market Analysis - by Data Rate

- 8.1-400GB/S

- 8.1.1 Overview

- 8.1.2-400GB/S: Europe Pluggable Optics for Data Center Market - Revenue and Forecast, 2021-2031 (US$ Million)

- 8.2-800GB/S

- 8.2.1 Overview

- 8.2.2-800GB/S: Europe Pluggable Optics for Data Center Market - Revenue and Forecast, 2021-2031 (US$ Million)

- 8.3GB/S and Above

- 8.3.1 Overview

- 8.3.2GB/S and Above: Europe Pluggable Optics for Data Center Market - Revenue and Forecast, 2021-2031 (US$ Million)

9. Europe Pluggable Optics for Data Center Market - Country Analysis

- 9.1 Europe

- 9.1.1 Europe Pluggable Optics for Data Center Market - Revenue and Forecast Analysis - by Country

- 9.1.1.1 Europe Pluggable Optics for Data Center Market - Revenue and Forecast Analysis - by Country

- 9.1.1.2 Germany: Europe Pluggable Optics for Data Center Market - Revenue and Forecast, 2021-2031 (US$ Million)

- 9.1.1.2.1 Germany: Europe Pluggable Optics for Data Center Market Share - by Component

- 9.1.1.2.2 Germany: Europe Pluggable Optics for Data Center Market Share - by Data Rate

- 9.1.1.3 United Kingdom: Europe Pluggable Optics for Data Center Market - Revenue and Forecast, 2021-2031 (US$ Million)

- 9.1.1.3.1 United Kingdom: Europe Pluggable Optics for Data Center Market Share - by Component

- 9.1.1.3.2 United Kingdom: Europe Pluggable Optics for Data Center Market Share - by Data Rate

- 9.1.1.4 France: Europe Pluggable Optics for Data Center Market - Revenue and Forecast, 2021-2031 (US$ Million)

- 9.1.1.4.1 France: Europe Pluggable Optics for Data Center Market Share - by Component

- 9.1.1.4.2 France: Europe Pluggable Optics for Data Center Market Share - by Data Rate

- 9.1.1.5 Italy: Europe Pluggable Optics for Data Center Market - Revenue and Forecast, 2021-2031 (US$ Million)

- 9.1.1.5.1 Italy: Europe Pluggable Optics for Data Center Market Share - by Component

- 9.1.1.5.2 Italy: Europe Pluggable Optics for Data Center Market Share - by Data Rate

- 9.1.1.6 Russia: Europe Pluggable Optics for Data Center Market - Revenue and Forecast, 2021-2031 (US$ Million)

- 9.1.1.6.1 Russia: Europe Pluggable Optics for Data Center Market Share - by Component

- 9.1.1.6.2 Russia: Europe Pluggable Optics for Data Center Market Share - by Data Rate

- 9.1.1.7 Rest of Europe: Europe Pluggable Optics for Data Center Market - Revenue and Forecast, 2021-2031 (US$ Million)

- 9.1.1.7.1 Rest of Europe: Europe Pluggable Optics for Data Center Market Share - by Component

- 9.1.1.7.2 Rest of Europe: Europe Pluggable Optics for Data Center Market Share - by Data Rate

- 9.1.1 Europe Pluggable Optics for Data Center Market - Revenue and Forecast Analysis - by Country

10. Competitive Landscape

- 10.1 Heat Map Analysis

- 10.2 Company Positioning Analysis

11. Industry Landscape

- 11.1 Overview

- 11.2 Market Initiative

- 11.3 Product Development

- 11.4 Mergers & Acquisitions

12. Company Profiles

- 12.1 Coherent Corp

- 12.1.1 Key Facts

- 12.1.2 Business Description

- 12.1.3 Products and Services

- 12.1.4 Financial Overview

- 12.1.5 SWOT Analysis

- 12.1.6 Key Developments

- 12.2 Nokia Corp

- 12.2.1 Key Facts

- 12.2.2 Business Description

- 12.2.3 Products and Services

- 12.2.4 Financial Overview

- 12.2.5 SWOT Analysis

- 12.2.6 Key Developments

- 12.3 Cisco Systems Inc

- 12.3.1 Key Facts

- 12.3.2 Business Description

- 12.3.3 Products and Services

- 12.3.4 Financial Overview

- 12.3.5 SWOT Analysis

- 12.3.6 Key Developments

- 12.4 Infinera Corp

- 12.4.1 Key Facts

- 12.4.2 Business Description

- 12.4.3 Products and Services

- 12.4.4 Financial Overview

- 12.4.5 SWOT Analysis

- 12.4.6 Key Developments

- 12.5 Telefonaktiebolaget LM Ericsson

- 12.5.1 Key Facts

- 12.5.2 Business Description

- 12.5.3 Products and Services

- 12.5.4 Financial Overview

- 12.5.5 SWOT Analysis

- 12.5.6 Key Developments

- 12.6 Ciena Corp

- 12.6.1 Key Facts

- 12.6.2 Business Description

- 12.6.3 Products and Services

- 12.6.4 Financial Overview

- 12.6.5 SWOT Analysis

- 12.6.6 Key Developments

- 12.7 Intel Corp

- 12.7.1 Key Facts

- 12.7.2 Business Description

- 12.7.3 Products and Services

- 12.7.4 Financial Overview

- 12.7.5 SWOT Analysis

- 12.7.6 Key Developments

- 12.8 Lumentum Holdings Inc

- 12.8.1 Key Facts

- 12.8.2 Business Description

- 12.8.3 Products and Services

- 12.8.4 Financial Overview

- 12.8.5 SWOT Analysis

- 12.8.6 Key Developments

- 12.9 Juniper Networks Inc

- 12.9.1 Key Facts

- 12.9.2 Business Description

- 12.9.3 Products and Services

- 12.9.4 Financial Overview

- 12.9.5 SWOT Analysis

- 12.9.6 Key Developments

- 12.10 Marvell Technology Inc

- 12.10.1 Key Facts

- 12.10.2 Business Description

- 12.10.3 Products and Services

- 12.10.4 Financial Overview

- 12.10.5 SWOT Analysis

- 12.10.6 Key Developments

- 12.11 Yangtze Optical Fibre and Cable Joint Stock Ltd

- 12.11.1 Key Facts

- 12.11.2 Business Description

- 12.11.3 Products and Services

- 12.11.4 Financial Overview

- 12.11.5 SWOT Analysis

- 12.11.6 Key Developments

- 12.12 Broadcom Inc

- 12.12.1 Key Facts

- 12.12.2 Business Description

- 12.12.3 Products and Services

- 12.12.4 Financial Overview

- 12.12.5 SWOT Analysis

- 12.12.6 Key Developments

13. Appendix

- 13.1 About The Insight Partners

- 13.2 Word Index