|

|

市場調査レポート

商品コード

1510721

アジア太平洋地域の風力タービンローターブレード市場:2030年市場予測と地域別分析- タイプ別、展開タイプ別Asia Pacific Wind Turbine Rotor Blade Market Forecast to 2030 - Regional Analysis - by Type (Below 40m, 41-60m, 61-70m, and Above 70m) and Deployment Type (Onshore and Offshore) |

||||||

|

|||||||

|

|||||||

| アジア太平洋地域の風力タービンローターブレード市場:2030年市場予測と地域別分析- タイプ別、展開タイプ別 |

|

出版日: 2024年05月07日

発行: The Insight Partners

ページ情報: 英文 71 Pages

納期: 即納可能

|

全表示

- 概要

- 図表

- 目次

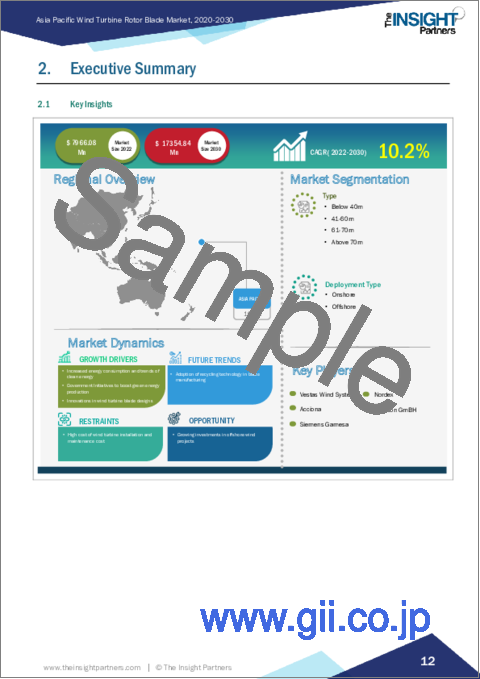

アジア太平洋地域の風力タービンローターブレード市場は、2022年には79億6,608万米ドルとなり、2030年には173億5,484万米ドルに達すると予測され、2022年から2030年までのCAGRは10.2%で成長すると予測されています。

洋上風力プロジェクトへの投資拡大アジア太平洋地域の風力タービンローターブレード市場。

洋上風力発電所は、風速が速く、一貫性が高く、陸地や人工物による物理的干渉がないため、陸上風力発電所よりも効率が高いと考えられています。洋上の風速は一般的に陸上よりも速いです。風速がわずかに変化するだけで、エネルギー生産量は大幅に増加します。風速15マイルで稼働するタービンは、風速12マイルで稼働するタービンの2倍のエネルギーを生産することができます。洋上の風速が速ければ、より多くのエネルギーを生み出すことができます。洋上の風速は陸上よりも安定しています。より安定した風の供給は、より信頼できるエネルギー源となります。そのため、陸上風力発電所よりも効率が高く、洋上風力発電所への投資が増加しています。

アジア太平洋地域では、政府が再生可能エネルギーの促進に力を入れていることが、風力発電プロジェクトの増加に拍車をかけています。Pinnapuram Integrated Renewable Energy Project、Yudean Yangjiang Qingzhou I Offshore Wind Farm、MacIntyre Wind Farm、Yuedean Yangjiang Qingzhou II Offshore Wind Farm、Abukuma Onshore Wind Farmは、2022年のアジア太平洋における主要な風力発電プロジェクトです。さらにインドは、2030年までに30ギガトン(GW)の洋上風力発電容量を建設するという野心的な目標を掲げています。さらに2022年には、アジア開発銀行がBIM Wind Power Joint Stock Companyとの間で、ベトナムのニントゥアン省における88MWの風力発電所の操業を支援する1億700万米ドルの融資プロジェクトに調印しました。また日本では、政府が2030年までに10GWの洋上風力発電を設置するという目標を掲げています。

このような投資は、将来的に洋上風力発電所の需要を促進し、最終的に風力タービンブレード業界に有利な機会を生み出すと期待されています。

アジア太平洋地域の風力タービンローターブレード市場概要

アジア太平洋地域の風力タービンローターブレード市場は、中国、インド、日本、オーストラリア、韓国、その他アジア太平洋地域に分類されます。アジア太平洋地域は、風力エネルギーコストの最小化、有利な政府イニシアティブ、風力エネルギープロジェクトへの投資の増加により、風力タービンローターブレード市場の主要地域の一つとなっています。アジア太平洋地域における風力タービンローターブレード市場の拡大は、再生可能エネルギー産業への投資の増加、産業化と都市化の急激な増加、風力エネルギー発電能力、新しい電化プロジェクト、送電網強化の取り組みが主な要因です。

Global Wind Energy Councilによると、2022年にアジア太平洋地域で新たに追加される風力発電容量は、世界全体の風力発電容量追加分の56%を占め、中国がアジア太平洋地域の風力発電容量追加分の87%を占めています。アジア太平洋地域の風力エネルギー部門は急速に拡大します。新しい研究によれば、2030年までに中国本土が世界最大の市場になるにつれ、洋上風力発電に対する高い国内需要が高まるため、この10年間で風力発電は同地域の電力容量の4分の1近くを占めるようになるといいます。このように、この地域における風力エネルギー設備の急速な拡大は、2022年から2030年にかけて風力タービンローターブレードの需要を促進すると予想されています。

アジア太平洋地域の風力タービンローターブレード市場の収益と2030年までの予測(金額)

アジア太平洋地域の風力タービンローターブレード市場のセグメンテーション

アジア太平洋地域の風力タービンローターブレード市場は、タイプ、展開タイプ、国によって区分されます。タイプ別では、アジア太平洋地域の風力タービンローターブレード市場は、40m未満、41~60m、61~70m、70m以上に区分されます。2022年には70m以上セグメントが最大の市場シェアを占めています。

展開タイプ別では、アジア太平洋地域の風力タービンローターブレード市場は陸上と海洋に二分されます。2022年の市場シェアは陸上の方が大きいです。

国別では、アジア太平洋地域の風力タービンローターブレード市場は、オーストラリア、中国、インド、日本、韓国、その他アジア太平洋地域に区分されます。2022年のアジア太平洋地域の風力タービンローターブレード市場シェアは中国が独占。

TPI Composites Inc、Vestas Wind Systems AS、ENERCON GmbH、LM Wind Power AS、Siemens Gamesa Renewable Energy SA、Acciona SA、Suzlon Energy Ltd、Nordex SE、Envision Energy USA Ltd、Lianyungang Zhongfu Lianzhong Composites Group Co Ltdは、アジア太平洋地域の風力タービンローターブレード市場で事業を展開している大手企業です。

目次

第1章 イントロダクション

第2章 エグゼクティブサマリー

- 主要洞察

- 市場の魅力

第3章 調査手法

- 調査範囲

- 2次調査

- 1次調査

第4章 アジア太平洋地域の風力タービンローターブレード市場情勢

- エコシステム分析

第5章 アジア太平洋地域の風力タービンローターブレード市場:主要産業力学

- 風力タービンローターブレード市場:主要産業力学

- 市場促進要因

- エネルギー消費の増加とクリーンエネルギーの動向

- グリーンエネルギー生産を促進する政府の取り組み

- 風力タービンブレード設計の革新

- 市場抑制要因

- 風力タービンの設置とメンテナンスの高コスト

- 市場機会

- 洋上風力プロジェクトへの投資の増加

- 今後の動向

- リサイクル技術の採用増加

- 促進要因と抑制要因の影響

第6章 風力タービンローターブレード市場:アジア太平洋地域市場分析

- 風力タービンローターブレード市場の売上高、2022年~2030年

- 風力タービンローターブレード市場の予測・分析

第7章 アジア太平洋地域の風力タービンローターブレード市場分析:タイプ別

- 40m未満

- 40m未満市場、収益と2030年までの予測

- 41-60m

- 41-60m市場、収益と2030年までの予測

- 61-70m

- 61-70m市場、収益と2030年までの予測

- 70m以上

- 70m以上市場、収益と2030年までの予測

第8章 アジア太平洋地域の風力タービンローターブレード市場分析:展開タイプ

- 陸上

- 陸上市場、収益と2030年までの予測

- オフショア

- オフショア市場、収益と2030年までの予測

第9章 アジア太平洋地域の風力タービンローターブレード市場:国別分析

- アジア太平洋地域

- オーストラリア

- 中国

- インド

- 日本

- 韓国

- その他アジア太平洋地域

第10章 競合情勢

- 主要企業によるヒートマップ分析

第11章 業界情勢

- 市場イニシアティブ

- 製品開発

- 合併と買収

第12章 企業プロファイル

- TPI Composites Inc

- Vestas Wind Systems AS

- ENERCON GmbH

- LM Wind Power AS

- Siemens Gamesa Renewable Energy SA

- Acciona SA

- Suzlon Energy Ltd

- Nordex SE

- Envision Energy USA Ltd

- Lianyungang Zhongfu Lianzhong Composites Group Co Ltd

第13章 付録

List Of Tables

- Table 1. Wind Turbine Rotor Blade Market Segmentation

- Table 2. Wind Turbine Rotor Blade Market Revenue and Forecasts to 2030 (US$ Million)

- Table 3. Wind Turbine Rotor Blade Market Revenue and Forecasts to 2030 (US$ Million) - Type

- Table 4. Wind Turbine Rotor Blade Market Revenue and Forecasts to 2030 (US$ Million) - Deployment Type

- Table 5. Australia Wind Turbine Rotor Blade Market Revenue and Forecasts to 2030 (US$ Mn) - By Type

- Table 6. Australia Wind Turbine Rotor Blade Market Revenue and Forecasts to 2030 (US$ Mn) - By Deployment Type

- Table 7. China Wind Turbine Rotor Blade Market Revenue and Forecasts to 2030 (US$ Mn) - By Type

- Table 8. China Wind Turbine Rotor Blade Market Revenue and Forecasts to 2030 (US$ Mn) - By Deployment Type

- Table 9. India Wind Turbine Rotor Blade Market Revenue and Forecasts to 2030 (US$ Mn) - By Type

- Table 10. India Wind Turbine Rotor Blade Market Revenue and Forecasts to 2030 (US$ Mn) - By Deployment Type

- Table 11. Japan Wind Turbine Rotor Blade Market Revenue and Forecasts to 2030 (US$ Mn) - By Type

- Table 12. Japan Wind Turbine Rotor Blade Market Revenue and Forecasts to 2030 (US$ Mn) - By Deployment Type

- Table 13. South Korea Wind Turbine Rotor Blade Market Revenue and Forecasts to 2030 (US$ Mn) - By Type

- Table 14. South Korea Wind Turbine Rotor Blade Market Revenue and Forecasts to 2030 (US$ Mn) - By Deployment Type

- Table 15. Rest of Asia Pacific Wind Turbine Rotor Blade Market Revenue and Forecasts to 2030 (US$ Mn) - By Type

- Table 16. Rest of Asia Pacific Wind Turbine Rotor Blade Market Revenue and Forecasts to 2030 (US$ Mn) - By Deployment Type

- Table 17. Heat Map Analysis by Key Players

List Of Figures

- Figure 1. Wind Turbine Rotor Blade Market Segmentation, By Country

- Figure 2. Ecosystem: Wind Turbine Rotor Blade Market

- Figure 3. Impact Analysis of Drivers and Restraints

- Figure 4. Wind Turbine Rotor Blade Market Revenue (US$ Million), 2022 - 2030

- Figure 5. Wind Turbine Rotor Blade Market Share (%) - Type, 2022 and 2030

- Figure 6. Below 40m Market Revenue and Forecasts to 2030 (US$ Million)

- Figure 7. 41-60m Market Revenue and Forecasts to 2030 (US$ Million)

- Figure 8. 61-70m Market Revenue and Forecasts to 2030 (US$ Million)

- Figure 9. Above 70m Market Revenue and Forecasts to 2030 (US$ Million)

- Figure 10. Wind Turbine Rotor Blade Market Share (%) - Deployment Type, 2022 and 2030

- Figure 11. Onshore Market Revenue and Forecasts to 2030 (US$ Million)

- Figure 12. Offshore Market Revenue and Forecasts to 2030 (US$ Million)

- Figure 13. Wind Turbine Rotor Blade Market, by Key Countries - Revenue (2022) (US$ Million)

- Figure 14. Asia Pacific Wind Turbine Rotor Blade Market Breakdown by Country (2022 and 2030)

- Figure 15. Australia Wind Turbine Rotor Blade Market Revenue and Forecasts to 2030 (US$ Mn)

- Figure 16. China Wind Turbine Rotor Blade Market Revenue and Forecasts to 2030 (US$ Mn)

- Figure 17. India Wind Turbine Rotor Blade Market Revenue and Forecasts to 2030 (US$ Mn)

- Figure 18. Japan Wind Turbine Rotor Blade Market Revenue and Forecasts to 2030 (US$ Mn)

- Figure 19. South Korea Wind Turbine Rotor Blade Market Revenue and Forecasts to 2030 (US$ Mn)

- Figure 20. Rest of Asia Pacific Wind Turbine Rotor Blade Market Revenue and Forecasts to 2030 (US$ Mn)

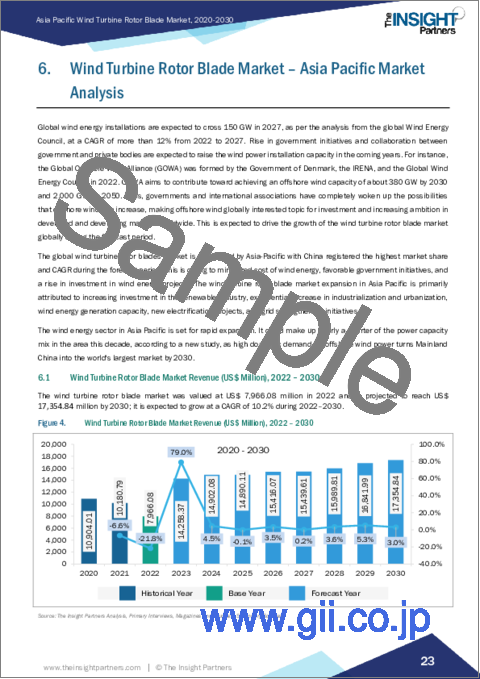

The Asia Pacific wind turbine rotor blade market was valued at US$ 7,966.08 million in 2022 and is expected to reach US$ 17,354.84 million by 2030; it is estimated to grow at a CAGR of 10.2% from 2022 to 20 30.

Growing Investments in Offshore Wind Projects Asia Pacific Wind Turbine Rotor Blade Market.

Offshore wind farms are thought to be more efficient than onshore wind farms due to higher wind speeds, greater consistency, and a lack of physical interference from land or man-made things. Offshore wind speeds are typically higher than on land. Small changes in wind speed result in substantial gains in energy production: a turbine operating in a 15-mph wind can produce twice as much energy as a turbine operating in a 12-mph wind. Faster offshore wind speeds mean that significantly more energy can be generated. Offshore wind speeds are more consistent than on land. A more consistent supply of wind means a more dependable source of energy. Thus, owing to higher efficiency compared to onshore wind farms, the investments in offshore farms are increasing.

In Asia Pacific, the growing governmental focus on promoting renewable energy is fueling the number of wind projects. Pinnapuram Integrated Renewable Energy Project, Yudean Yangjiang Qingzhou I Offshore Wind Farm, MacIntyre Wind Farm, Yuedean Yangjiang Qingzhou II Offshore Wind Farm, and Abukuma Onshore Wind Farm were a few major wind projects in Asia Pacific in 2022. Further, India has also set an ambitious goal of constructing 30 gigatons (GW) of offshore wind capacity by 2030. Additionally, in 2022, the Asian Development Bank sealed a US$ 107 million financing project with BIM Wind Power Joint Stock Company to help the operation of an 88 MW wind farm in Ninh Thuan province, Vietnam. Also, in Japan, the government has set the target of 10 GW of offshore wind installation by 2030.

Such investments are expected to fuel the demand for offshore wind farms in the future, ultimately generating lucrative opportunities for the wind turbine blades industry.

Asia Pacific Wind Turbine Rotor Blade Market Overview

The Asia-Pacific wind turbine rotor blade market is classified into China, India, Japan, Australia, South Korea, and the Rest of Asia Pacific. Asia Pacific is one of the leading regions in the wind turbine rotor blade market due to minimized cost of wind energy, favorable government initiatives, and a rise in investment in wind energy projects. The wind turbine rotor blade market expansion in Asia Pacific is primarily attributed to increasing investment in the renewable industry, exponential increase in industrialization and urbanization, wind energy generation capacity, new electrification projects, and grid strengthening initiatives.

According to the Global Wind Energy Council, newly added wind capacity in Asia Pacific in 2022 accounted for 56% of total wind capacity additions globally, with China contributing 87% of total additions in Asia Pacific. The wind energy sector in Asia Pacific is set for rapid expansion. It could make up nearly a quarter of the power capacity mix in the area this decade, according to a new study, as high domestic demand for offshore wind power turns Mainland China into the world's largest market by 2030. Thus, the rapid expansion of wind energy installations in the region is anticipated to propel the demand for wind turbine rotor blades from 2022 to 2030.

Asia Pacific wind turbine rotor blade market Revenue and Forecast to 2030 (US$ Million)

Asia Pacific Wind Turbine Rotor Blade Market Segmentation

The Asia Pacific wind turbine rotor blade market is segmented based on type, deployment type, and country. Based on type, the Asia Pacific wind turbine rotor blade market is segmented into Below 40m, 41-60m, 61-70m, and Above 70m . The Above 70m segment held the largest market share in 2022.

In terms of deployment type, the Asia Pacific wind turbine rotor blade market is bifurcated into onshore and offshore . The onshore held a larger market share in 2022.

Based on country, the Asia Pacific wind turbine rotor blade market is segmented into Australia, China, India, Japan, South Korea, and the Rest of Asia Pacific. China dominated the Asia Pacific wind turbine rotor blade market share in 2022.

TPI Composites Inc, Vestas Wind Systems AS, ENERCON GmbH, LM Wind Power AS, Siemens Gamesa Renewable Energy SA, Acciona SA, Suzlon Energy Ltd, Nordex SE, Envision Energy USA Ltd, and Lianyungang Zhongfu Lianzhong Composites Group Co Ltd are some of the leading companies operating in the Asia Pacific wind turbine rotor blade market.

Table Of Contents

Table of Content

1. Introduction

- 1.1 The Insight Partners Research Report Guidance

- 1.2 Market Segmentation

2. Executive Summary

- 2.1 Key Insights

- 2.2 Market Attractiveness

3. Research Methodology

- 3.1 Coverage

- 3.2 Secondary Research

- 3.3 Primary Research

4. Asia Pacific Wind Turbine Rotor Blade Market Landscape

- 4.1 Overview

- 4.2 Ecosystem Analysis

5. Asia Pacific Wind Turbine Rotor Blade Market - Key Industry Dynamics

- 5.1 Wind Turbine Rotor Blade Market - Key Industry Dynamics

- 5.2 Market Drivers

- 5.2.1 Increased Energy Consumption and Trends of Clean Energy

- 5.2.2 Government Initiatives to Boost Green Energy Production

- 5.2.3 Innovations in Wind Turbine Blade Designs

- 5.3 Market Restraints

- 5.3.1 High Cost of Wind Turbine Installation and Maintenance

- 5.4 Market Opportunities

- 5.4.1 Growing Investments in Offshore Wind Projects

- 5.5 Future Trends

- 5.5.1 Increasing Adoption of Recycling Technology

- 5.6 Impact of Drivers and Restraints:

6. Wind Turbine Rotor Blade Market - Asia Pacific Market Analysis

- 6.1 Wind Turbine Rotor Blade Market Revenue (US$ Million), 2022 - 2030

- 6.2 Wind Turbine Rotor Blade Market Forecast and Analysis

7. Asia Pacific Wind Turbine Rotor Blade Market Analysis -Type

- 7.1 Wind Turbine Rotor Blade Market, By Type (2022 and 2030)

- 7.2 Below 40m

- 7.2.1 Overview

- 7.2.2 Below 40m Market, Revenue and Forecast to 2030 (US$ Million)

- 7.3 41-60m

- 7.3.1 Overview

- 7.3.2 41-60m Market, Revenue and Forecast to 2030 (US$ Million)

- 7.4 61-70m

- 7.4.1 Overview

- 7.4.2 61-70m Market, Revenue and Forecast to 2030 (US$ Million)

- 7.5 Above 70m

- 7.5.1 Overview

- 7.5.2 Above 70m Market, Revenue and Forecast to 2030 (US$ Million)

8. Asia Pacific Wind Turbine Rotor Blade Market Analysis - Deployment Type

- 8.1 Wind Turbine Rotor Blade Market, By Deployment Type (2022 and 2030)

- 8.2 Onshore

- 8.2.1 Overview

- 8.2.2 Onshore Market, Revenue and Forecast to 2030 (US$ Million)

- 8.3 Offshore

- 8.3.1 Overview

- 8.3.2 Offshore Market, Revenue and Forecast to 2030 (US$ Million)

9. Asia Pacific Wind Turbine Rotor Blade Market - Country Analysis

- 9.1 Asia Pacific

- 9.1.1 Asia Pacific Wind Turbine Rotor Blade Market Overview

- 9.1.2 Asia Pacific Wind Turbine Rotor Blade Market Revenue and Forecasts and Analysis - By Country

- 9.1.2.1 Australia Wind Turbine Rotor Blade Market Revenue and Forecasts to 2030 (US$ Mn)

- 9.1.2.1.1 Australia Wind Turbine Rotor Blade Market Breakdown by Type

- 9.1.2.1.2 Australia Wind Turbine Rotor Blade Market Breakdown by Deployment Type

- 9.1.2.2 China Wind Turbine Rotor Blade Market Revenue and Forecasts to 2030 (US$ Mn)

- 9.1.2.2.1 China Wind Turbine Rotor Blade Market Breakdown by Type

- 9.1.2.2.2 China Wind Turbine Rotor Blade Market Breakdown by Deployment Type

- 9.1.2.3 India Wind Turbine Rotor Blade Market Revenue and Forecasts to 2030 (US$ Mn)

- 9.1.2.3.1 India Wind Turbine Rotor Blade Market Breakdown by Type

- 9.1.2.3.2 India Wind Turbine Rotor Blade Market Breakdown by Deployment Type

- 9.1.2.4 Japan Wind Turbine Rotor Blade Market Revenue and Forecasts to 2030 (US$ Mn)

- 9.1.2.4.1 Japan Wind Turbine Rotor Blade Market Breakdown by Type

- 9.1.2.4.2 Japan Wind Turbine Rotor Blade Market Breakdown by Deployment Type

- 9.1.2.5 South Korea Wind Turbine Rotor Blade Market Revenue and Forecasts to 2030 (US$ Mn)

- 9.1.2.5.1 South Korea Wind Turbine Rotor Blade Market Breakdown by Type

- 9.1.2.5.2 South Korea Wind Turbine Rotor Blade Market Breakdown by Deployment Type

- 9.1.2.6 Rest of Asia Pacific Wind Turbine Rotor Blade Market Revenue and Forecasts to 2030 (US$ Mn)

- 9.1.2.6.1 Rest of Asia Pacific Wind Turbine Rotor Blade Market Breakdown by Type

- 9.1.2.6.2 Rest of Asia Pacific Wind Turbine Rotor Blade Market Breakdown by Deployment Type

- 9.1.2.1 Australia Wind Turbine Rotor Blade Market Revenue and Forecasts to 2030 (US$ Mn)

10. Competitive Landscape

- 10.1 Heat Map Analysis by Key Players

11. Industry Landscape

- 11.1 Overview

- 11.2 Market Initiative

- 11.3 Product Development

- 11.4 Mergers & Acquisitions

12. Company Profiles

- 12.1 TPI Composites Inc

- 12.1.1 Key Facts

- 12.1.2 Business Description

- 12.1.3 Products and Services

- 12.1.4 Financial Overview

- 12.1.5 SWOT Analysis

- 12.1.6 Key Developments

- 12.2 Vestas Wind Systems AS

- 12.2.1 Key Facts

- 12.2.2 Business Description

- 12.2.3 Products and Services

- 12.2.4 Financial Overview

- 12.2.5 SWOT Analysis

- 12.2.6 Key Developments

- 12.3 ENERCON GmbH

- 12.3.1 Key Facts

- 12.3.2 Business Description

- 12.3.3 Products and Services

- 12.3.4 Financial Overview

- 12.3.5 SWOT Analysis

- 12.3.6 Key Developments

- 12.4 LM Wind Power AS

- 12.4.1 Key Facts

- 12.4.2 Business Description

- 12.4.3 Products and Services

- 12.4.4 Financial Overview

- 12.4.5 SWOT Analysis

- 12.4.6 Key Developments

- 12.5 Siemens Gamesa Renewable Energy SA

- 12.5.1 Key Facts

- 12.5.2 Business Description

- 12.5.3 Products and Services

- 12.5.4 Financial Overview

- 12.5.5 SWOT Analysis

- 12.5.6 Key Developments

- 12.6 Acciona SA

- 12.6.1 Key Facts

- 12.6.2 Business Description

- 12.6.3 Products and Services

- 12.6.4 Financial Overview

- 12.6.5 SWOT Analysis

- 12.6.6 Key Developments

- 12.7 Suzlon Energy Ltd

- 12.7.1 Key Facts

- 12.7.2 Business Description

- 12.7.3 Products and Services

- 12.7.4 Financial Overview

- 12.7.5 SWOT Analysis

- 12.7.6 Key Developments

- 12.8 Nordex SE

- 12.8.1 Key Facts

- 12.8.2 Business Description

- 12.8.3 Products and Services

- 12.8.4 Financial Overview

- 12.8.5 SWOT Analysis

- 12.8.6 Key Developments

- 12.9 Envision Energy USA Ltd

- 12.9.1 Key Facts

- 12.9.2 Business Description

- 12.9.3 Products and Services

- 12.9.4 Financial Overview

- 12.9.5 SWOT Analysis

- 12.9.6 Key Developments

- 12.10 Lianyungang Zhongfu Lianzhong Composites Group Co Ltd

- 12.10.1 Key Facts

- 12.10.2 Business Description

- 12.10.3 Products and Services

- 12.10.4 Financial Overview

- 12.10.5 SWOT Analysis

- 12.10.6 Key Developments

13. Appendix

- 13.1 About The Insight Partners