|

|

市場調査レポート

商品コード

1558312

生分解性材料の2030年までの市場予測: タイプ別、流通チャネル別、エンドユーザー別、地域別の世界分析Biodegradable Materials Market Forecasts to 2030 - Global Analysis By Type (Bioplastics, Natural Fibers, Compostable Materials and Other Types), Distribution Channel, End User and By Geography |

||||||

|

|||||||

カスタマイズ可能

|

|||||||

| 生分解性材料の2030年までの市場予測: タイプ別、流通チャネル別、エンドユーザー別、地域別の世界分析 |

|

出版日: 2024年09月06日

発行: Stratistics Market Research Consulting

ページ情報: 英文 200+ Pages

納期: 2~3営業日

|

全表示

- 概要

- 図表

- 目次

Stratistics MRCによると、世界の生分解性材料市場は2024年に82億6,000万米ドルを占め、2030年には225億7,000万米ドルに達すると予測され、予測期間中のCAGRは23.8%です。

生分解性材料は、微生物の活動などの自然プロセスによって、合理的な時間枠内で、より単純で無害な成分に分解できる物質です。生分解性材料は、水、二酸化炭素、バイオマスといった自然の要素に分解されます。生分解性素材は、環境への影響や廃棄物を削減する、環境に優しい代替品です。生分解性素材の技術革新は、その性能と価格の向上を目指しており、産業界全体でその採用を支援しています。

ナショナル・ジオグラフィックの調査によると、生産されるプラスチックの約40.0%は、一度使用されただけで廃棄される包装材です。さらに、世界中で年間約5億枚のレジ袋が使用されています。

企業の持続可能性への取り組みの高まり

企業の持続可能性への取り組みの高まりは、企業が環境に優しい慣行を採用することを奨励しています。企業が環境負荷の低減に取り組むにつれ、持続可能性の目標に沿うよう、生分解性素材など従来のプラスチックに代わるものを求める傾向が強まっています。このような取り組みには、廃棄物の削減、二酸化炭素排出量の削減、循環型経済の原則の推進などの目標設定が含まれることが多いです。生分解性素材に投資することで、企業はブランドの評判を高め、規制要件を満たし、環境意識の高い消費者にアピールすることができます。

標準化の欠如

生分解性材料の標準化の欠如は、「生分解性」を構成する定義や基準が地域によって異なることや、試験方法や規制が地域によって異なることから生じています。この一貫性のなさは、消費者やメーカーに混乱をもたらし、製品の比較や品質の確保を困難にすることで、市場の成長を妨げています。明確で統一された基準がなければ、広く普及させ、消費者の信頼を築き、規制遵守を徹底させることは困難であり、最終的には生分解性材料の市場拡大と技術革新の足かせとなります。

高まる廃棄物管理慣行

廃棄物管理システムが進化するにつれ、生分解性製品の効果的な収集、分別、堆肥化をサポートするようになってきています。このようなインフラは、生分解性材料が適切に処理され、汚染を減らし、リサイクルと堆肥化を促進することで、生分解性材料の実用化を促進します。また、廃棄物管理方法の改善は、生分解性材料の使用済み製品への影響に関する懸念の解消にも役立ち、持続可能な解決策を求める企業や消費者にとって、生分解性材料がより魅力的な選択肢となるため、市場の成長を促進します。

不十分な廃棄物管理と堆肥化インフラ

廃棄物管理と堆肥化のインフラが不十分なため、これらの製品の効果的な処理と廃棄が制限されています。生分解性材料の選別、堆肥化、リサイクルのための十分な設備がなければ、適切に分解されなかったり、埋立地行きになったりする可能性があり、環境面での利点が損なわれます。このようなインフラの欠如は、生分解性製品に対する消費者や企業の信頼を損ない、採用を阻害し、市場の成長とこれらの材料の潜在的な環境上の利点を阻害します。

COVID-19の影響

COVID-19の大流行は当初、サプライチェーンの中断と生産能力の低下を通じて生分解性素材市場を混乱させました。しかし、危機的状況の中で消費者や企業が環境への配慮を優先する傾向が強まったため、持続可能なソリューションへの需要も加速しました。パンデミックは、より持続可能なパッケージングと廃棄物管理の必要性を浮き彫りにし、生分解性素材への投資に拍車をかけた。この二重の影響により、市場成長の課題と機会の両方がもたらされ、より持続可能なものへと長期的にシフトしていった。

予測期間中、天然繊維分野が最大となる見込み

天然繊維セグメントは予測期間中最大になると予測されます。綿、麻、ジュート、竹などの天然繊維は、その持続可能性と環境上の利点から、生分解性素材に使用されることが多くなっています。これらの繊維は合成繊維の代替品よりも分解が早く、埋立廃棄物や汚染を減らすことができます。天然由来であるため生分解性と堆肥化が可能であり、環境に優しいパッケージング、テキスタイル、農産物に最適です。

消費財セグメントは予測期間中最も高いCAGRが見込まれる

消費財セグメントは予測期間中、最も高いCAGRが見込まれます。消費財における生分解性材料は、その環境上の利点から人気が高まっています。消費財では、包装、使い捨て食器、パーソナルケア製品に使用されています。従来のプラスチックを生分解性の代替品に置き換えることで、企業はエコロジカル・フットプリントを最小化し、持続可能な製品に対する消費者の需要に応えることで、循環型経済への貢献と環境負荷の低減を目指しています。

最大のシェアを占める地域:

アジア太平洋地域の生分解性材料市場は、環境意識の高まりと持続可能な慣行に対する政府の支援により、最大のシェアを占めると予想されます。急速な工業化と環境に優しい製品に対する消費者の需要の高まりが、包装、農業、その他の分野での生分解性材料の採用を促進しています。中国、日本、インドなどの国々は、技術の進歩とプラスチック廃棄物の削減に重点を置くようになっていることに支えられ、市場の拡大をリードしています。インフラと規制枠組みへの投資が市場開拓をさらに後押しし、技術革新と市場浸透を促進しています。

CAGRが最も高い地域:

北米では、環境意識の高まりとプラスチック廃棄物削減を目的とした厳しい規制政策により、生分解性材料市場のCAGRが最も高くなると予想されます。同地域では、包装、食品サービス、農業において、環境に優しい代替品への強い需要が見られます。技術と持続可能な実践の進歩に支えられた生分解性材料の革新が市場成長に寄与しています。

無料カスタマイズサービス:

本レポートをご購読のお客様には、以下の無料カスタマイズオプションのいずれかをご利用いただけます:

- 企業プロファイル

- 追加市場プレイヤーの包括的プロファイリング(3社まで)

- 主要企業のSWOT分析(3社まで)

- 地域セグメンテーション

- 顧客の関心に応じた主要国の市場推計・予測・CAGR(注:フィージビリティチェックによる)

- 競合ベンチマーキング

- 製品ポートフォリオ、地理的プレゼンス、戦略的提携に基づく主要企業のベンチマーキング

目次

第1章 エグゼクティブサマリー

第2章 序文

- 概要

- ステークホルダー

- 調査範囲

- 調査手法

- データマイニング

- データ分析

- データ検証

- 調査アプローチ

- 調査情報源

- 1次調査情報源

- 2次調査情報源

- 前提条件

第3章 市場動向分析

- 促進要因

- 抑制要因

- 機会

- 脅威

- エンドユーザー分析

- 新興市場

- COVID-19の影響

第4章 ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 代替品の脅威

- 新規参入業者の脅威

- 競争企業間の敵対関係

第5章 世界の生分解性材料市場:タイプ別

- バイオプラスチック

- デンプンベース

- PLA(ポリ乳酸)

- PHA(ポリヒドロキシアルカン酸)

- 天然繊維

- コットン

- ジュート

- 麻

- 竹

- 堆肥化可能な材料

- 紙・段ボール

- バガス

- 菌糸体由来材料

- その他のタイプ

第6章 世界の生分解性材料市場:流通チャネル別

- 直接販売

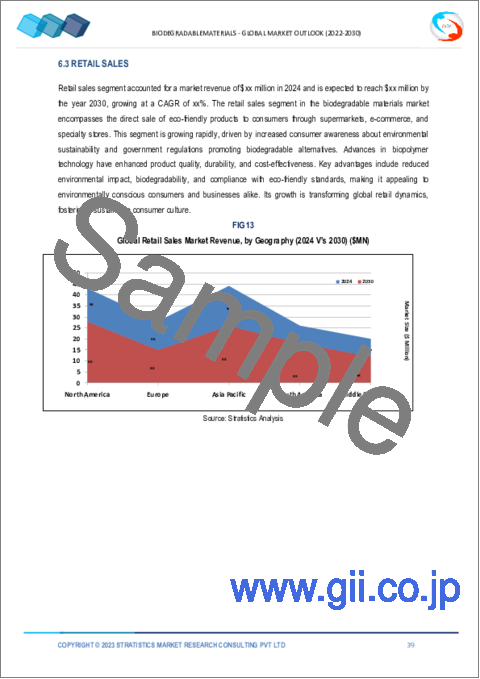

- 小売販売

- オンライン販売

- その他の流通チャネル

第7章 世界の生分解性材料市場:エンドユーザー別

- 飲食品

- テキスタイル・アパレル

- 消費財

- 農業

- ヘルスケア

- その他のエンドユーザー

第8章 世界の生分解性材料市場:地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- イタリア

- フランス

- スペイン

- その他欧州

- アジア太平洋

- 日本

- 中国

- インド

- オーストラリア

- ニュージーランド

- 韓国

- その他アジア太平洋地域

- 南米

- アルゼンチン

- ブラジル

- チリ

- その他南米

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- カタール

- 南アフリカ

- その他中東とアフリカ

第9章 主な発展

- 契約、パートナーシップ、コラボレーション、合弁事業

- 買収と合併

- 新製品発売

- 事業拡大

- その他の主要戦略

第10章 企業プロファイリング

- BASF SE

- Danimer Scientific

- NatureWorks LLC

- Novamont S.p.A.

- Corbion N.V.

- Total Corbion PLA

- Paptic Ltd.

- Green Dot Bioplastics

- Metabolix, Inc.

- Biome Bioplastics

- Cardia Bioplastics

- Ginkgo BioWorks

- BioBag International

- Tianan Biologic Materials Corporation

- Futerro

- ZymoChem

- Algenesis

List of Tables

- Table 1 Global Biodegradable Materials Market Outlook, By Region (2022-2030) ($MN)

- Table 2 Global Biodegradable Materials Market Outlook, By Type (2022-2030) ($MN)

- Table 3 Global Biodegradable Materials Market Outlook, By Bioplastics (2022-2030) ($MN)

- Table 4 Global Biodegradable Materials Market Outlook, By Starch-based (2022-2030) ($MN)

- Table 5 Global Biodegradable Materials Market Outlook, By PLA (Polylactic Acid) (2022-2030) ($MN)

- Table 6 Global Biodegradable Materials Market Outlook, By PHA (Polyhydroxyalkanoates) (2022-2030) ($MN)

- Table 7 Global Biodegradable Materials Market Outlook, By Natural Fibers (2022-2030) ($MN)

- Table 8 Global Biodegradable Materials Market Outlook, By Cotton (2022-2030) ($MN)

- Table 9 Global Biodegradable Materials Market Outlook, By Jute (2022-2030) ($MN)

- Table 10 Global Biodegradable Materials Market Outlook, By Hemp (2022-2030) ($MN)

- Table 11 Global Biodegradable Materials Market Outlook, By Bamboo (2022-2030) ($MN)

- Table 12 Global Biodegradable Materials Market Outlook, By Compostable Materials (2022-2030) ($MN)

- Table 13 Global Biodegradable Materials Market Outlook, By Paper & Cardboard (2022-2030) ($MN)

- Table 14 Global Biodegradable Materials Market Outlook, By Bagasse (2022-2030) ($MN)

- Table 15 Global Biodegradable Materials Market Outlook, By Mycelium-based Materials (2022-2030) ($MN)

- Table 16 Global Biodegradable Materials Market Outlook, By Other Types (2022-2030) ($MN)

- Table 17 Global Biodegradable Materials Market Outlook, By Distribution Channel (2022-2030) ($MN)

- Table 18 Global Biodegradable Materials Market Outlook, By Direct Sales (2022-2030) ($MN)

- Table 19 Global Biodegradable Materials Market Outlook, By Retail Sales (2022-2030) ($MN)

- Table 20 Global Biodegradable Materials Market Outlook, By Online Sales (2022-2030) ($MN)

- Table 21 Global Biodegradable Materials Market Outlook, By Other Distribution Channels (2022-2030) ($MN)

- Table 22 Global Biodegradable Materials Market Outlook, By End User (2022-2030) ($MN)

- Table 23 Global Biodegradable Materials Market Outlook, By Food & Beverage (2022-2030) ($MN)

- Table 24 Global Biodegradable Materials Market Outlook, By Textile & Apparel (2022-2030) ($MN)

- Table 25 Global Biodegradable Materials Market Outlook, By Consumer Goods (2022-2030) ($MN)

- Table 26 Global Biodegradable Materials Market Outlook, By Agriculture (2022-2030) ($MN)

- Table 27 Global Biodegradable Materials Market Outlook, By Healthcare (2022-2030) ($MN)

- Table 28 Global Biodegradable Materials Market Outlook, By Other End Users (2022-2030) ($MN)

Note: Tables for North America, Europe, APAC, South America, and Middle East & Africa Regions are also represented in the same manner as above.

According to Stratistics MRC, the Global Biodegradable Materials Market is accounted for $8.26 billion in 2024 and is expected to reach $22.57 billion by 2030 growing at a CAGR of 23.8% during the forecast period. Biodegradable materials are substances that can be broken down by natural processes, such as microbial activity, into simpler, non-toxic components within a reasonable timeframe. Biodegradable materials break down into natural elements like water, carbon dioxide, and biomass. They offer an eco-friendly alternative that reduces environmental impact and waste. Innovations in biodegradable materials aim to improve their performance and affordability, supporting their adoption across industries.

According to a National Geographic study, approximately 40.0% of plastic produced is packaging used just once and then discarded. Moreover, approximately 500 million plastic bags are used worldwide annually.

Market Dynamics:

Driver:

Rising corporate sustainability initiatives

Rising corporate sustainability initiatives encourages companies to adopt environmentally friendly practices. As businesses commit to reducing their environmental impact, they increasingly seek alternatives to traditional plastics, such as biodegradable materials, to align with their sustainability goals. These initiatives often involve setting targets for reducing waste, cutting carbon footprints, and promoting circular economy principles. By investing in biodegradable materials, companies can enhance their brand reputation, meet regulatory requirements, and appeal to environmentally conscious consumers, thereby accelerating market demand and innovation in the sector.

Restraint:

Lack of standardization

Lack of standardization in biodegradable materials arises from varying definitions and criteria for what constitutes "biodegradable," as well as differences in testing methods and regulations across regions. This inconsistency hampers market growth by creating confusion among consumers and manufacturers, leading to difficulties in comparing products and ensuring quality. Without clear, unified standards, it is challenging to achieve widespread adoption, build consumer trust, and enforce regulatory compliance, ultimately slowing the market's expansion and innovation in biodegradable materials.

Opportunity:

Mounting waste management practices

As waste management systems evolve, they increasingly support the effective collection, sorting, and composting of biodegradable products. This infrastructure facilitates the practical use of biodegradable materials by ensuring they are properly processed, reducing contamination, and promoting recycling and composting. Improved waste management practices also help address concerns about the end-of-life impact of biodegradable materials, making them a more attractive option for businesses and consumers seeking sustainable solutions, thus driving market growth.

Threat:

Inadequate waste management & composting infrastructure

Inadequate waste management and composting infrastructure limits the effective processing and disposal of these products. Without sufficient facilities for sorting, composting, and recycling biodegradable materials, they may not break down properly or could end up in landfills, negating their environmental benefits. This lack of infrastructure undermines consumer and business confidence in biodegradable products and discourages adoption, impeding market growth and the potential environmental advantages of these materials.

Covid-19 Impact

The covid-19 pandemic initially disrupted the biodegradable materials market through supply chain interruptions and reduced production capacity. However, it also accelerated demand for sustainable solutions as consumers and businesses increasingly prioritized environmental concerns amidst the crisis. The pandemic highlighted the need for more sustainable packaging and waste management practices, spurring investments in biodegradable materials. This dual impact led to both challenges and opportunities for market growth, with a long-term shift towards greater sustainability.

The natural fibers segment is expected to be the largest during the forecast period

The natural fibers segment is estimated to be the largest during the forecast period. Natural fibers, such as cotton, hemp, jute, and bamboo, are increasingly used in biodegradable materials due to their sustainability and environmental benefits. These fibers decompose more rapidly than synthetic alternatives, reducing landfill waste and pollution. Their natural origin ensures they are biodegradable and compostable, making them ideal for eco-friendly packaging, textiles, and agricultural products.

The consumer goods segment is expected to have the highest CAGR during the forecast period

The consumer goods segment is anticipated to witness the highest CAGR during the forecast period. Biodegradable materials in consumer goods are increasingly popular due to their environmental benefits. In consumer goods, they are used in packaging, disposable utensils, and personal care products. By replacing conventional plastics with biodegradable alternatives, companies aim to minimize their ecological footprint and meet consumer demand for sustainable products, contributing to a circular economy and reducing environmental impact.

Region with largest share:

The biodegradable materials market in the Asia-Pacific region is anticipated to witness the largest share due to increasing environmental awareness and government support for sustainable practices. Rapid industrialization and rising consumer demand for eco-friendly products are driving the adoption of biodegradable materials in packaging, agriculture, and other sectors. Countries like China, Japan, and India are leading in market expansion, supported by advancements in technology and a growing emphasis on reducing plastic waste. Investments in infrastructure and regulatory frameworks further support the market's development, fostering innovation and market penetration.

Region with highest CAGR:

In North America, the biodegradable materials market is expected to have highest CAGR, driven by heightened environmental awareness and stringent regulatory policies aimed at reducing plastic waste. The region sees strong demand for eco-friendly alternatives in packaging, food service, and agriculture. Innovations in biodegradable materials, supported by advancements in technology and sustainable practices, contribute to market growth.

Key players in the market

Some of the key players profiled in the Biodegradable Materials Market include BASF SE, Danimer Scientific, NatureWorks LLC, Novamont S.p.A., Corbion N.V., Total Corbion PLA, Paptic Ltd., Green Dot Bioplastics, Metabolix, Inc., Biome Bioplastics, Cardia Bioplastics, Ginkgo BioWorks, BioBag International, Tianan Biologic Materials Corporation, Futerro, ZymoChem and Algenesis.

Key Developments:

In July 2024, ZymoChem launched BAYSE(TM), the world's first bio-based and biodegradable super absorbent polymer. BAYSE(TM) represents a significant innovation in materials science, combining high absorbency with environmental sustainability. The polymer is designed to degrade into non-toxic components, addressing the environmental concerns associated with conventional SAPs that can contribute to plastic pollution.

In March 2024, Algenesis, a leader in sustainable materials, has created a TPU that is not only high-performing but also breaks down into non-toxic components, unlike conventional plastics that persist and fragment into microplastics. The TPU incorporates bio-based components, derived from renewable sources such as algae, which contributes to its environmental sustainability.

Types Covered:

- Bioplastics

- Natural Fibers

- Compostable Materials

- Other Types

Distribution Channels Covered:

- Direct Sales

- Retail Sales

- Online Sales

- Other Distribution Channels

End Users Covered:

- Food & Beverage

- Textile & Apparel

- Consumer Goods

- Agriculture

- Healthcare

- Other End Users

Regions Covered:

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- Italy

- France

- Spain

- Rest of Europe

- Asia Pacific

- Japan

- China

- India

- Australia

- New Zealand

- South Korea

- Rest of Asia Pacific

- South America

- Argentina

- Brazil

- Chile

- Rest of South America

- Middle East & Africa

- Saudi Arabia

- UAE

- Qatar

- South Africa

- Rest of Middle East & Africa

What our report offers:

- Market share assessments for the regional and country-level segments

- Strategic recommendations for the new entrants

- Covers Market data for the years 2022, 2023, 2024, 2026, and 2030

- Market Trends (Drivers, Constraints, Opportunities, Threats, Challenges, Investment Opportunities, and recommendations)

- Strategic recommendations in key business segments based on the market estimations

- Competitive landscaping mapping the key common trends

- Company profiling with detailed strategies, financials, and recent developments

- Supply chain trends mapping the latest technological advancements

Free Customization Offerings:

All the customers of this report will be entitled to receive one of the following free customization options:

- Company Profiling

- Comprehensive profiling of additional market players (up to 3)

- SWOT Analysis of key players (up to 3)

- Regional Segmentation

- Market estimations, Forecasts and CAGR of any prominent country as per the client's interest (Note: Depends on feasibility check)

- Competitive Benchmarking

- Benchmarking of key players based on product portfolio, geographical presence, and strategic alliances

Table of Contents

1 Executive Summary

2 Preface

- 2.1 Abstract

- 2.2 Stake Holders

- 2.3 Research Scope

- 2.4 Research Methodology

- 2.4.1 Data Mining

- 2.4.2 Data Analysis

- 2.4.3 Data Validation

- 2.4.4 Research Approach

- 2.5 Research Sources

- 2.5.1 Primary Research Sources

- 2.5.2 Secondary Research Sources

- 2.5.3 Assumptions

3 Market Trend Analysis

- 3.1 Introduction

- 3.2 Drivers

- 3.3 Restraints

- 3.4 Opportunities

- 3.5 Threats

- 3.6 End User Analysis

- 3.7 Emerging Markets

- 3.8 Impact of Covid-19

4 Porters Five Force Analysis

- 4.1 Bargaining power of suppliers

- 4.2 Bargaining power of buyers

- 4.3 Threat of substitutes

- 4.4 Threat of new entrants

- 4.5 Competitive rivalry

5 Global Biodegradable Materials Market, By Type

- 5.1 Introduction

- 5.2 Bioplastics

- 5.2.1 Starch-based

- 5.2.2 PLA (Polylactic Acid)

- 5.2.3 PHA (Polyhydroxyalkanoates)

- 5.3 Natural Fibers

- 5.3.1 Cotton

- 5.3.2 Jute

- 5.3.3 Hemp

- 5.3.4 Bamboo

- 5.4 Compostable Materials

- 5.4.1 Paper & Cardboard

- 5.4.2 Bagasse

- 5.4.3 Mycelium-based Materials

- 5.5 Other Types

6 Global Biodegradable Materials Market, By Distribution Channel

- 6.1 Introduction

- 6.2 Direct Sales

- 6.3 Retail Sales

- 6.4 Online Sales

- 6.5 Other Distribution Channels

7 Global Biodegradable Materials Market, By End User

- 7.1 Introduction

- 7.2 Food & Beverage

- 7.3 Textile & Apparel

- 7.4 Consumer Goods

- 7.5 Agriculture

- 7.6 Healthcare

- 7.7 Other End Users

8 Global Biodegradable Materials Market, By Geography

- 8.1 Introduction

- 8.2 North America

- 8.2.1 US

- 8.2.2 Canada

- 8.2.3 Mexico

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 Italy

- 8.3.4 France

- 8.3.5 Spain

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 Japan

- 8.4.2 China

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 New Zealand

- 8.4.6 South Korea

- 8.4.7 Rest of Asia Pacific

- 8.5 South America

- 8.5.1 Argentina

- 8.5.2 Brazil

- 8.5.3 Chile

- 8.5.4 Rest of South America

- 8.6 Middle East & Africa

- 8.6.1 Saudi Arabia

- 8.6.2 UAE

- 8.6.3 Qatar

- 8.6.4 South Africa

- 8.6.5 Rest of Middle East & Africa

9 Key Developments

- 9.1 Agreements, Partnerships, Collaborations and Joint Ventures

- 9.2 Acquisitions & Mergers

- 9.3 New Product Launch

- 9.4 Expansions

- 9.5 Other Key Strategies

10 Company Profiling

- 10.1 BASF SE

- 10.2 Danimer Scientific

- 10.3 NatureWorks LLC

- 10.4 Novamont S.p.A.

- 10.5 Corbion N.V.

- 10.6 Total Corbion PLA

- 10.7 Paptic Ltd.

- 10.8 Green Dot Bioplastics

- 10.9 Metabolix, Inc.

- 10.10 Biome Bioplastics

- 10.11 Cardia Bioplastics

- 10.12 Ginkgo BioWorks

- 10.13 BioBag International

- 10.14 Tianan Biologic Materials Corporation

- 10.15 Futerro

- 10.16 ZymoChem

- 10.17 Algenesis