|

市場調査レポート

商品コード

1851483

生分解性プラスチック包装:市場シェア分析、産業動向、統計、成長予測(2025年~2030年)Biodegradable Plastic Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 生分解性プラスチック包装:市場シェア分析、産業動向、統計、成長予測(2025年~2030年) |

|

出版日: 2025年07月03日

発行: Mordor Intelligence

ページ情報: 英文 183 Pages

納期: 2~3営業日

|

概要

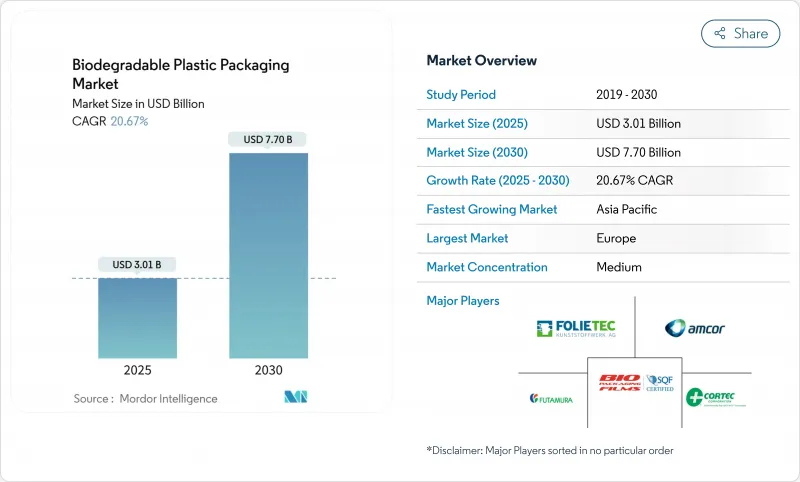

生分解性プラスチック包装の市場規模は2025年に30億1,000万米ドル、2030年には77億米ドルに達し、CAGR 20.67%で拡大すると予測されています。

この力強い軌道は、規制の義務化、企業の炭素価格政策、バイオ樹脂加工の急速な進歩が、コンポスタブル・フォーマットの経済的実現可能性を共に向上させていることを反映しています。ブランドオーナーは現在、地域的な包装仕様よりもグローバルな包装仕様を好み、単位当たりのコストを下げる大量契約を可能にしています。海洋分解性PHAや耐熱性PBATは、今や厳しいバリア要件や温度要件を満たしています。これと並行して、自治体の廃棄物削減目標が、食品配送や小売部門に堆肥化可能な認証済みソリューションの採用を促し、樹脂サプライヤーにとって予測可能なオフテイクを生み出しています。そのため、生分解性プラスチック包装市場は、依然として不安定な農業原料価格を補う明確なライン・オブ・サイト需要を享受しています。

世界の生分解性プラスチック包装市場の動向と洞察

EUとインドで加速する使い捨て石油プラスチック包装の禁止

欧州連合(EU)の2024年単一使用プラスチック指令は、カトラリーやクラムシェルなどのリサイクル困難な品目に取って代わり、認証された堆肥化可能な食品接触パックの需要を直ちに高めました。インドの州全体にわたる禁止措置は、18億人以上の消費者を同じ転換にさらし、多国籍企業に世界的な仕様の調和を迫り、樹脂工場のスケールメリットを引き出します。バイオ材料のプレミアムを上回る罰則は、さらに採用を加速させる。オーストラリアの2024年の禁止措置は、生産者の数量可視性を維持する連鎖的政策効果を強化します。

北米における堆肥化対応フォーマットを必要とする食品宅配アプリの普及

主要なアグリゲーターは、2024年に記録された自治体の転用目標および消費者の嗜好の追跡調査に合わせて、大都市圏の一流レストランに対して堆肥化可能なボウル、カップ、カトラリーの使用を義務付ける。宅配料金の仕組みは、素材の割高感を隠しているため、事業者はブランド認知と埋立料金の節約に重点を置いています。チェーン店のパイロット試験では、廃棄コストが15~20%削減され、市条例へのコンプライアンスもスムーズになったと報告されています。この要件はクラウドキッチンネットワークに波及し、ソースやサイドメニューのフレキシブルパック需要を増幅させています。

西欧以外では産業用堆肥化インフラが厳しい

アジア太平洋とラテンアメリカでは、バイオ樹脂を完全に分解できる高温堆肥化プラントの建設が急ピッチで進んでいます。自治体による資金調達の制限や許認可のハードルが施設の稼働を遅らせている一方で、民間の事業者は、食品廃棄物と包装廃棄物の混合廃棄物の受け入れルールがより明確になるのを待っています。生産能力が拡大するまでは、適切な使用済み廃棄物の選択肢がない地域への販売は制限され、生分解性プラスチック包装市場の急速な拡大が抑制されます。

セグメント分析

生分解性プラスチック包装の素材タイプ別市場規模は、2024年に66.45%のシェアを占めるポリ乳酸に偏っているが、ポリヒドロキシアルカノエートが25.34%のCAGRで最も強い見通しを示しています。PHAは海洋環境で生分解する能力を持ち、沿岸廃棄物に関する法規制が強化されているため、島や港湾都市をターゲットにしたストロー、カトラリー、バリア性の高いポーチに適しています。メーカーは、その幅広いメルトフローウィンドウを利用して、PLAでは扱いにくい厚みのある医薬品バイアルやパーソナルケアジャーを成形しています。また、米国とタイで、食品用の砂糖の代わりに農業残渣を利用した新たな生産能力が発表され、原料の変動からPLAを守ることができるようになりました。

PLAは、工業的堆肥化が行われている地域ではコスト競争力を維持しており、西欧ではベーカリーフィルムや熱成形サラダ用チューブを支えています。継続的な研究開発により、充填温度105℃に耐える高熱インジオグレードが開発され、以前の性能格差が縮小しました。PBATとPBSはニッチな耐熱用途や化学薬品に接触する用途に使用され、デンプンブレンドは超価格重視の食料品袋プログラムを支配しています。全体的な材料状況は、第一世代のコストリーダーシップから第二世代のパフォーマンスリーダーシップへの移行を示し、市場情勢の長期的多様化を補強しています。

フレキシブル・フォーマットは2024年の生分解性プラスチック包装市場シェアの58.77%を占め、eコマースやミールキット配送の運賃を最小限に抑える軽量パウチ、ラップ、メーラーに支えられています。後付けラインで加工されたフィルムは、生鮮食品に適した酸素透過率を達成し、二次包装なしで賞味期限を延長します。プレミアム・スナック・ブランドは、製品の完全性をアピールするために透明化PLA製の透明ウィンドウを重視し、PBATを組み込んだラミネートは耐パンク性を向上させています。

リジッドフォーマットは、コーヒーポッド、ホットカップライニング、電子レンジ対応トレイを背景にCAGR23.1%で加速しています。ネイチャーワークス社と機械サプライヤーのIMA社は、KeurigとNespressoの仕様に適合し、90日で堆肥化できるターンキーポッドシステムを発表し、大量の飲料チャネルを開拓しました。外食チェーンは、ポリスチレンのクラムシェルから、工業用コンポスターと互換性のあるPHAライニングのファイバーボウルにシフトし、パフォーマンスとブランド・エクイティの目標を達成しています。急成長しているリジッド分野は、機能性の向上が従来の優位性を侵食し、市場セグメンテーションの総収益を拡大することを示しています。

生分解性プラスチック包装市場レポートは、材料タイプ(デンプンブレンド、ポリ乳酸(PLA)、その他)、包装タイプ(軟包装、硬包装)、最終用途産業(食品、飲食品、フードサービス、その他)、堆肥化可能性(家庭用堆肥化可能性、工業用堆肥化可能性)、地域(北米、欧州、アジア太平洋、MEA、南米)で区分されています。市場予測は金額(米ドル)で提供されます。

地域分析

欧州の成熟した堆肥化インフラと包括的な規制背景が2024年に35.57%の生分解性プラスチック包装市場シェアを確保地域の樹脂生産者は、結束したEN規格と拡大生産者責任料金によって生み出される予測可能な需要から利益を得ており、変換業者は、パリ、ベルリン、マドリードに遍在する高成長食品配送プラットフォームに近接していることから利益を得ています。有機廃棄物の分別収集に対する政府の補助金がパックの採用をさらに後押しし、欧州の短期的リーダーシップが確固たるものになります。

アジア太平洋は、インド、中国、タイがリサイクル困難な包装形態を段階的に禁止しているため、CAGRが24.65%と最も高いです。第一級都市における「非分解性」プラスチックを対象とする中国の指令は、2027年までにキャリーバッグから持ち帰り用容器へと拡大し、キャッサバや米の籾殻を原料とする地域密着型の工場が生まれます。インドの各州の規制は断片的なままだが、人口カバー率が累積しているため、多国籍のクイックサービス・レストランが堆肥化可能なコーティング技術の標準化を進めています。オーストラリアとニュージーランドも包括的な使い捨てプラスチック禁止法を採用し、オセアニア全域で即時の代替需要を牽引しています。

北米では、フォーチュン500企業の食品配送義務化と社内炭素価格設定を活用して採用を推進しているが、産業用堆肥化の地域的な普及率にはまだばらつきがあります。サンパウロやメキシコ・シティのような中南米の巨大都市は、試験的な堆肥化ハブを展開し、より広範な成長の舞台を整えています。中東とアフリカでは、埋立地の不足と観光業主導のプラスチック禁止が、特に湾岸協力会議のホスピタリティ部門にニッチな機会を生み出しています。全体として、管轄地域の政策動向とインフラ投資パターンが、生分解性プラスチック包装市場の地域別成長を説明しています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- EUとインドで使い捨て石油プラスチック包装の禁止が加速

- 北米で堆肥化可能なフォーマットを必要とするフードデリバリーアプリの普及

- 小売企業の「プラスチックニュートラル」宣言(例:ウォルマート、カルフール)が需要を押し上げる

- 既存のフィルムブローラインをバイオ樹脂用に改造(CAPEX15%)

- パックの透明カーボンラベルへのブランドシフト

- 企業レベルでの炭素価格導入(70米ドル超/トン)により、バイオ・オプションが有利になります。

- 市場抑制要因

- 西欧以外の逼迫した産業堆肥インフラ

- PLAの原料価格変動(トウモロコシ、サトウキビ)

- 堆肥化可能」と「生分解性」の主張をめぐる消費者の混乱

- 米国と日本における機械的リサイクルによる汚染の罰則

- サプライチェーン分析

- 規制とテクノロジーの展望

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 供給企業の交渉力

- 買い手の交渉力

- 代替品の脅威

- 競争企業間の敵対関係

- エコシステム分析

- 生分解性とバイオベースのプラスチック包装におけるイノベーション

- 比較分析- 石油プラスチックと生分解性包装の比較

- バイオプラスチックの生産情勢

- バイオプラスチックの生産統計

- 樹脂タイプ別生産量

- 地域別生産量

- フードサービス/HoReCaセクターの進化する動向

- 新興産業動向

第5章 市場規模と成長予測

- 材料タイプ別

- でんぷんブレンド

- ポリ乳酸(PLA)

- ポリブチレンアジペートーコ-テレフタレート(PBAT)

- ポリブチレンサクシネート(PBS)

- ポリヒドロキシアルカノエート(PHA)

- その他の材料

- パッケージングタイプ別

- 軟包装

- バッグとパウチ

- フィルムおよびラップ

- ラベルとスリーブ

- 硬包装

- 食器

- トレイとボウル

- 食品容器

- コーヒーカップとポッド

- その他の硬包装

- 軟包装

- 最終用途産業別

- 食品

- 飲料

- フードサービス

- パーソナルケアとホームケア

- 医薬品

- その他の最終用途産業

- 堆肥化別

- ホームコンポスタブル

- 産業用コンポスタブル

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- ロシア

- その他欧州地域

- アジア太平洋地域

- 中国

- インド

- 日本

- 韓国

- オーストラリアおよびニュージーランド

- その他アジア太平洋地域

- 中東・アフリカ

- 中東

- アラブ首長国連邦

- サウジアラビア

- トルコ

- その他中東

- アフリカ

- 南アフリカ

- ナイジェリア

- エジプト

- その他アフリカ

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 北米

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア分析

- 企業プロファイル

- Amcor plc

- BASF SE

- NatureWorks LLC

- Tetra Pak International S.A.

- Sealed Air Corporation

- Kuraray Co., Ltd.

- Taghleef Industries

- FKuR Kunststoff GmbH

- good natured Products Inc.

- Pactiv Evergreen Inc.

- ALPLA Werke Alwin Lehner GmbH

- Transcontinental Inc.

- Plascon Industries

- Futamura Group

- Cortec Corporation

- BioBag International AS

- Biome Bioplastics

- Bio Packaging Films

- Bio Futura

- Groupe Barbier

- VektoPack

- Singular Solutions Inc.

- Biogreen Biotech

- Plabottles.eu(Global Solutions BV)