|

|

市場調査レポート

商品コード

1284288

サーマルインターフェースマテリアル(TIM)の2028年までの市場予測- 製品タイプ、構成、用途、地域別の世界分析Thermal Interface Materials Market Forecasts to 2028 - Global Analysis By Product Type, Composition, Application and By Geography |

||||||

|

|

|||||||

カスタマイズ可能

|

|||||||

| サーマルインターフェースマテリアル(TIM)の2028年までの市場予測- 製品タイプ、構成、用途、地域別の世界分析 |

|

出版日: 2023年06月01日

発行: Stratistics Market Research Consulting

ページ情報: 英文 175+ Pages

納期: 2~3営業日

|

- 全表示

- 概要

- 図表

- 目次

Stratistics MRCによると、世界のサーマルインターフェースマテリアル(TIM)市場は2022年に21億4,000万米ドルを占め、予測期間中にCAGR 13.3%で成長し、2028年には45億2,000万米ドルに達すると予想されています。

熱界面充填材は、発熱部品とそれに対応するヒートシンクの間に自然に形成される空間や界面を塞ぐために使用されます。熱伝導を最大化するために、これらの界面材料は導電性媒体を提供し、空隙をなくします。小型化、小型化、高エネルギー密度のガジェットの生産に伴い、デバイスチップからヒートシンクへの熱伝達を改善し、熱の蓄積を防止してガジェットの寿命を延ばすことができる製品の需要が高まっています。

産業分析によると、自動車産業は2030年には世界全体で9兆米ドル以下に成長すると予測されています。このうち、新車販売台数は約38%を占めると予想されています。したがって、自動車産業の成長は、サーマルインターフェースマテリアル(TIM)市場の成長にとって有益な機会を創出することになります。

市場力学:

促進要因:

サーマルインターフェースマテリアル(TIM)は、LED市場の拡大により需要が高まっています。

必要以上にエネルギーを消費する蛍光灯は、現在LEDに置き換えられています。しかし、LED照明には、もともと物理的な矛盾があります。目的のルーメン出力を出すためには、LEDの電力は高くなければならないです。一方で、エネルギー損失や発熱を抑えるために、LEDの電流は小さくなければならないです。このような物理的な矛盾を解決するには、「時間的・空間的分離」「システム的分離」「条件的分離」の4つの分離原則を適用する必要があります。最適化が限界に達している多くの状況において、分離は最善の策です。しかし、LEDの寿命を延ばすためには、十分な熱交換媒体が必要です。TIMは、コスト、放熱能力、使用可能なスペースといった要素の間で理想的なバランスをとっています。TIMの需要は、LED照明の需要増に比例して増加すると予想されています。光学設計と熱設計を組み合わせて、電子駆動システムを含むシステム全体の効率と光質を向上させることが、高度なLED設計の課題となっています。その結果、LED設計の高度化に比例して、TIMの需要や効果も影響を受けることになります。

抑制要因:

サーマルインターフェースマテリアル(TIM)の性能は、物理的な特性によって制約を受けます。

電子機器、特にマイクロプロセッサチップの電力密度は、過去数十年にわたり増大しています。電子回路の熱問題は、デバイスの小型化という継続的な傾向の結果、著しく増加しています。このように、電子デバイスが意図したとおりに機能することを保証するために、熱管理に焦点を当てることはますます重要かつ基本的なことです。伝導性熱伝達は、通常、熱を発生点からヒートシンクの拡大された表面積に分散させるために使用されます。しかし、熱管理システムは、温度を適切な範囲に維持し、最大の性能と信頼性を確保するために、あらゆる種類の熱伝達を使用することができます。固体表面同士を接続して接触抵抗を最小化するアセンブリの重要な構成要素は、空隙を埋めるためにTIMを接合部に注入することです。TIMの導入により界面での熱伝達が促進されるにもかかわらず、TIMがシステムの熱抵抗の主因となることはよく知られています。

機会:

自動車産業におけるサーマルインターフェースマテリアル(TIM)の需要増加

自動車に使用されるサーマルインターフェースマテリアル(TIM)には、必須ジェル、隙間充填・絶縁パッド、粘着テープ、グリースなど、数多くの種類があります。産業分析によると、自動車産業は2030年までに世界で9兆米ドル弱に成長すると予想されています。このうち、新車販売台数は約38%を占めると予想されています。このことから、自動車産業の拡大は、サーマルインターフェースマテリアル(TIM)の市場拡大にとって好機となります。さらに、予測期間中は、技術の進歩、多様なエンドユーザー産業、新興国からの熱インターフェース材料に対する需要の高まりにより、市場拡大のための多くの新しい機会がもたらされるでしょう。

脅威:

ユーザーにとって最適な運用コストの見極め

TIMの熱伝導率は、その価格に直結しています。しかし、熱伝導率の向上は、取り扱い性の悪さや適合性の低下など、アセンブリ全体に悪影響を及ぼすことにもなります。TIMのコストと機器の所有コストは、熱伝導率、相変化、粘度、圧力、アウトガス、表面仕上げ、塗りやすさ、材料の機械的特性などの要素に影響されます。

COVID-19の影響:

COVID-19の流行はサーマルインターフェースマテリアル(TIM)の需要を大幅に減少させたが、それはわずかな期間しか続かなかっています。遠隔会議の普及とリモートワークの動向により、材料が必要とされるようになりました。在宅勤務戦略は市場の成長を刺激し、ノートパソコン、スマートフォン、パーソナルコンピューターなどの売上を増加させました。ヘルスケア機器では、医療機器の需要増加により、より多くのサーマルインターフェースマテリアル(TIM)が必要とされています。

予測期間中、シリコーン分野が最も大きくなると予想される

最も大きな市場シェアを占めるのはシリコーンセグメント。サーマルインターフェースマテリアル(TIM)では、2021年にシリコンがリードしています。シリコンは、さまざまな用途で効果的な性能を発揮するため、より広く使用されるようになりました。シリコンは、衝撃、振動、機械的ストレスに対して高い耐性を有しています。パッド、ギャップフィラー、グリース、接着剤など、多くの製品でシリコーンが頻繁に使用されています。

予測期間中、エラストマーパッド分野のCAGRが最も高くなると予想されています。

電気・電子部品に熱伝導性を持たせるための取り扱いや設置手順が簡単なことから、エラストマーパッドは予測期間中に大きなCAGRを記録すると予測されています。しかし、限られたアプリケーションスペースと高い製品単価が、予測期間中の成長を抑制すると予測されています。

最もシェアの高い地域:

この地域にはさまざまな産業の大規模な製造拠点が存在するため、アジア太平洋は2019年に37%以上の最高収益シェアを獲得して市場をリードしました。同地域の製造基盤を除けば、法人税の低下、世帯所得の増加、物品サービス税(GST)の低下、消費者の健康意識、政府の支援政策、ライフスタイルの変化といった要因が、同地域のサーマルインターフェースマテリアル(TIM)分野の発展に影響を及ぼしていると考えられます。

CAGRが最も高い地域:

予測期間中、アジア太平洋地域は大きく成長すると予想されています。この地域のサーマルインターフェースマテリアル(TIM)市場は、都市化、工業化、民生・通信機器需要の増加の結果、拡大しています。アジア太平洋地域におけるサーマルインターフェースマテリアル(TIM)の採用は、医療機器での使用拡大や電気自動車・ハイブリッド車の普及によって、さらに後押しされています。再生可能エネルギー源の使用を奨励するプログラムの導入、公的機関および民間機関による研究開発への投資、技術の進歩はすべて、この地域の市場成長を加速させるのに貢献しています。

主な発展:

2022年6月、Dow Corning Corporationは新しいTIMs、DOWSIL TC-4040を発売しました。このギャップフィラーは、吐出が容易で、高い熱伝導率を有し、スランプに抵抗します。この新製品の発売は、同社がTIMs市場で競争力を維持するのに役立つと思われます。

2022年1月、3Mはテネシー州クリントンの事業を拡大しました。3Mはテネシー州クリントンの工場に約4億7,000万米ドルを投資し、2025年までに約600人の新規雇用を追加します。

2020年9月、パーカー・ハネフィン・コーポレーションは、一液型の新しい熱伝導性ディスペンサブルマテリアル「THERM-A-GAP GEL 37」を発売しました。この新製品の発売により、同社はTIMs市場における製品ポートフォリオを強化することになります。

当レポートが提供するもの

- 地域別および国別セグメントの市場シェア評価

- 新規参入企業への戦略的提言

- 2020年、2021年、2022年、2025年、2028年の市場データを網羅

- 市場動向(促進要因、抑制要因、機会、脅威、課題、投資機会、推奨事項)

- 市場推定に基づく、主要ビジネスセグメントにおける戦略的提言

- 主要な共通トレンドをマッピングした競合情勢。

- 詳細な戦略、財務、最近の開発状況を含む企業プロファイル

- 最新の技術的進歩をマッピングしたサプライチェーン動向

無料のカスタマイズ提供:

本レポートをご購入いただいたお客様には、以下の無料カスタマイズオプションのいずれかを提供させていただきます:

- 企業プロファイル

- 追加市場プレイヤーの包括的なプロファイリング(最大3社まで)

- 主要プレイヤーのSWOT分析(3社まで)

- 地域別セグメンテーション

- お客様のご希望に応じて、主要国の市場推計・予測・CAGR(注:フィージビリティチェックによる。)

- 競合ベンチマーキング

- 製品ポートフォリオ、地域的プレゼンス、戦略的提携に基づく主要プレイヤーのベンチマーキング

目次

第1章 エグゼクティブサマリー

第2章 序文

- 概要

- ステークホルダー

- 調査範囲

- 調査手法

- データマイニング

- データ分析

- データ検証

- 調査アプローチ

- 調査ソース

- 1次調査ソース

- 2次調査ソース

- 仮定

第3章 市場動向分析

- 促進要因

- 抑制要因

- 機会

- 脅威

- 製品分析

- アプリケーション分析

- 新興市場

- 新型コロナウイルス感染症(COVID-19)の影響

第4章 ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 代替品の脅威

- 新規参入業者の脅威

- 競争企業間の敵対関係

第5章 世界のサーマルインターフェースマテリアル(TIM)市場:製品タイプ別

- テープとフィルム

- ギャップフィラー金属TIM

- エラストマーパッド

- グリースおよび接着剤

- 金属ベースのサーマル

- 界面材料

- 相変化材料

- その他の製品タイプ

第6章 世界のサーマルインターフェースマテリアル(TIM)市場:構成別

- エポキシ

- ポリイミド

- シリコーン

- その他の構成

第7章 世界のサーマルインターフェースマテリアル(TIM)市場:用途別

- コンピュータ

- 電気通信

- 医療機器

- 産業機械

- 耐久消費財

- カーエレクトロニクス

- その他の用途

第8章 世界のサーマルインターフェースマテリアル(TIM)市場:地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- イタリア

- フランス

- スペイン

- その他欧州

- アジア太平洋地域

- 日本

- 中国

- インド

- オーストラリア

- ニュージーランド

- 韓国

- その他アジア太平洋地域

- 南米

- アルゼンチン

- ブラジル

- チリ

- その他南米

- 中東とアフリカ

- サウジアラビア

- アラブ首長国連邦

- カタール

- 南アフリカ

- その他中東とアフリカ

第9章 主な発展

- 契約、パートナーシップ、コラボレーション、合弁事業

- 買収と合併

- 新製品の発売

- 事業拡大

- その他の主要戦略

第10章 会社概要

- AIM Specialty Materials

- AOS Thermal Compounds LLC

- CSL Smart Helmet Inc.

- CSW Industrials, Inc.

- Fuji Polymer Industries Co., Ltd.

- GrafTech International Ltd.

- Henkel AG and Co. KgaA

- Honeywell International, Inc.

- Hylomar LLC

- Indium Corporation

- Laird Technologies, Inc.

- Linseis GmbH

- llinois Tool Works Inc

- Mcgill Airseal LLC

- Momentive Performance Materials, Inc.

- Parker Hannifin Corp.

- Pidilite Industries Ltd.

- PPG Industries

- Shin-Etsu Chemical Co. Ltd.

- The 3M Company

- The Dow Chemical Company

- Wacker Chemie AG

- Wakefield Thermal, Inc.

List of Tables

- Table 1 Global Thermal Interface Materials Market Market Outlook, By Region (2020-2028) ($MN)

- Table 2 Global Thermal Interface Materials Market Market Outlook, By Product Type (2020-2028) ($MN)

- Table 3 Global Thermal Interface Materials Market Market Outlook, By Tapes and Films (2020-2028) ($MN)

- Table 4 Global Thermal Interface Materials Market Market Outlook, By Gap Fillers Metallic TIMs (2020-2028) ($MN)

- Table 5 Global Thermal Interface Materials Market Market Outlook, By Elastomeric Pads (2020-2028) ($MN)

- Table 6 Global Thermal Interface Materials Market Market Outlook, By Greases & Adhesives (2020-2028) ($MN)

- Table 7 Global Thermal Interface Materials Market Market Outlook, By Metal Based Thermal (2020-2028) ($MN)

- Table 8 Global Thermal Interface Materials Market Market Outlook, By Interface Materials (2020-2028) ($MN)

- Table 9 Global Thermal Interface Materials Market Market Outlook, By Phase Change Materials (2020-2028) ($MN)

- Table 10 Global Thermal Interface Materials Market Market Outlook, By Other Product Types (2020-2028) ($MN)

- Table 11 Global Thermal Interface Materials Market Market Outlook, By Composition (2020-2028) ($MN)

- Table 12 Global Thermal Interface Materials Market Market Outlook, By Epoxy (2020-2028) ($MN)

- Table 13 Global Thermal Interface Materials Market Market Outlook, By Polyimide (2020-2028) ($MN)

- Table 14 Global Thermal Interface Materials Market Market Outlook, By Silicone (2020-2028) ($MN)

- Table 15 Global Thermal Interface Materials Market Market Outlook, By Other Compositions (2020-2028) ($MN)

- Table 16 Global Thermal Interface Materials Market Market Outlook, By Applications (2020-2028) ($MN)

- Table 17 Global Thermal Interface Materials Market Market Outlook, By Computers (2020-2028) ($MN)

- Table 18 Global Thermal Interface Materials Market Market Outlook, By Telecommunications (2020-2028) ($MN)

- Table 19 Global Thermal Interface Materials Market Market Outlook, By Medical Devices (2020-2028) ($MN)

- Table 20 Global Thermal Interface Materials Market Market Outlook, By Industrial Machinery (2020-2028) ($MN)

- Table 21 Global Thermal Interface Materials Market Market Outlook, By Consumer Durables (2020-2028) ($MN)

- Table 22 Global Thermal Interface Materials Market Market Outlook, By Automotive Electronics (2020-2028) ($MN)

- Table 23 Global Thermal Interface Materials Market Market Outlook, By Other Applications (2020-2028) ($MN)

- Table 24 North America Thermal Interface Materials Market Market Outlook, By Country (2020-2028) ($MN)

- Table 25 North America Thermal Interface Materials Market Market Outlook, By Product Type (2020-2028) ($MN)

- Table 26 North America Thermal Interface Materials Market Market Outlook, By Tapes and Films (2020-2028) ($MN)

- Table 27 North America Thermal Interface Materials Market Market Outlook, By Gap Fillers Metallic TIMs (2020-2028) ($MN)

- Table 28 North America Thermal Interface Materials Market Market Outlook, By Elastomeric Pads (2020-2028) ($MN)

- Table 29 North America Thermal Interface Materials Market Market Outlook, By Greases & Adhesives (2020-2028) ($MN)

- Table 30 North America Thermal Interface Materials Market Market Outlook, By Metal Based Thermal (2020-2028) ($MN)

- Table 31 North America Thermal Interface Materials Market Market Outlook, By Interface Materials (2020-2028) ($MN)

- Table 32 North America Thermal Interface Materials Market Market Outlook, By Phase Change Materials (2020-2028) ($MN)

- Table 33 North America Thermal Interface Materials Market Market Outlook, By Other Product Types (2020-2028) ($MN)

- Table 34 North America Thermal Interface Materials Market Market Outlook, By Composition (2020-2028) ($MN)

- Table 35 North America Thermal Interface Materials Market Market Outlook, By Epoxy (2020-2028) ($MN)

- Table 36 North America Thermal Interface Materials Market Market Outlook, By Polyimide (2020-2028) ($MN)

- Table 37 North America Thermal Interface Materials Market Market Outlook, By Silicone (2020-2028) ($MN)

- Table 38 North America Thermal Interface Materials Market Market Outlook, By Other Compositions (2020-2028) ($MN)

- Table 39 North America Thermal Interface Materials Market Market Outlook, By Applications (2020-2028) ($MN)

- Table 40 North America Thermal Interface Materials Market Market Outlook, By Computers (2020-2028) ($MN)

- Table 41 North America Thermal Interface Materials Market Market Outlook, By Telecommunications (2020-2028) ($MN)

- Table 42 North America Thermal Interface Materials Market Market Outlook, By Medical Devices (2020-2028) ($MN)

- Table 43 North America Thermal Interface Materials Market Market Outlook, By Industrial Machinery (2020-2028) ($MN)

- Table 44 North America Thermal Interface Materials Market Market Outlook, By Consumer Durables (2020-2028) ($MN)

- Table 45 North America Thermal Interface Materials Market Market Outlook, By Automotive Electronics (2020-2028) ($MN)

- Table 46 North America Thermal Interface Materials Market Market Outlook, By Other Applications (2020-2028) ($MN)

- Table 47 Europe Thermal Interface Materials Market Market Outlook, By Country (2020-2028) ($MN)

- Table 48 Europe Thermal Interface Materials Market Market Outlook, By Product Type (2020-2028) ($MN)

- Table 49 Europe Thermal Interface Materials Market Market Outlook, By Tapes and Films (2020-2028) ($MN)

- Table 50 Europe Thermal Interface Materials Market Market Outlook, By Gap Fillers Metallic TIMs (2020-2028) ($MN)

- Table 51 Europe Thermal Interface Materials Market Market Outlook, By Elastomeric Pads (2020-2028) ($MN)

- Table 52 Europe Thermal Interface Materials Market Market Outlook, By Greases & Adhesives (2020-2028) ($MN)

- Table 53 Europe Thermal Interface Materials Market Market Outlook, By Metal Based Thermal (2020-2028) ($MN)

- Table 54 Europe Thermal Interface Materials Market Market Outlook, By Interface Materials (2020-2028) ($MN)

- Table 55 Europe Thermal Interface Materials Market Market Outlook, By Phase Change Materials (2020-2028) ($MN)

- Table 56 Europe Thermal Interface Materials Market Market Outlook, By Other Product Types (2020-2028) ($MN)

- Table 57 Europe Thermal Interface Materials Market Market Outlook, By Composition (2020-2028) ($MN)

- Table 58 Europe Thermal Interface Materials Market Market Outlook, By Epoxy (2020-2028) ($MN)

- Table 59 Europe Thermal Interface Materials Market Market Outlook, By Polyimide (2020-2028) ($MN)

- Table 60 Europe Thermal Interface Materials Market Market Outlook, By Silicone (2020-2028) ($MN)

- Table 61 Europe Thermal Interface Materials Market Market Outlook, By Other Compositions (2020-2028) ($MN)

- Table 62 Europe Thermal Interface Materials Market Market Outlook, By Applications (2020-2028) ($MN)

- Table 63 Europe Thermal Interface Materials Market Market Outlook, By Computers (2020-2028) ($MN)

- Table 64 Europe Thermal Interface Materials Market Market Outlook, By Telecommunications (2020-2028) ($MN)

- Table 65 Europe Thermal Interface Materials Market Market Outlook, By Medical Devices (2020-2028) ($MN)

- Table 66 Europe Thermal Interface Materials Market Market Outlook, By Industrial Machinery (2020-2028) ($MN)

- Table 67 Europe Thermal Interface Materials Market Market Outlook, By Consumer Durables (2020-2028) ($MN)

- Table 68 Europe Thermal Interface Materials Market Market Outlook, By Automotive Electronics (2020-2028) ($MN)

- Table 69 Europe Thermal Interface Materials Market Market Outlook, By Other Applications (2020-2028) ($MN)

- Table 70 Asia Pacific Thermal Interface Materials Market Market Outlook, By Country (2020-2028) ($MN)

- Table 71 Asia Pacific Thermal Interface Materials Market Market Outlook, By Product Type (2020-2028) ($MN)

- Table 72 Asia Pacific Thermal Interface Materials Market Market Outlook, By Tapes and Films (2020-2028) ($MN)

- Table 73 Asia Pacific Thermal Interface Materials Market Market Outlook, By Gap Fillers Metallic TIMs (2020-2028) ($MN)

- Table 74 Asia Pacific Thermal Interface Materials Market Market Outlook, By Elastomeric Pads (2020-2028) ($MN)

- Table 75 Asia Pacific Thermal Interface Materials Market Market Outlook, By Greases & Adhesives (2020-2028) ($MN)

- Table 76 Asia Pacific Thermal Interface Materials Market Market Outlook, By Metal Based Thermal (2020-2028) ($MN)

- Table 77 Asia Pacific Thermal Interface Materials Market Market Outlook, By Interface Materials (2020-2028) ($MN)

- Table 78 Asia Pacific Thermal Interface Materials Market Market Outlook, By Phase Change Materials (2020-2028) ($MN)

- Table 79 Asia Pacific Thermal Interface Materials Market Market Outlook, By Other Product Types (2020-2028) ($MN)

- Table 80 Asia Pacific Thermal Interface Materials Market Market Outlook, By Composition (2020-2028) ($MN)

- Table 81 Asia Pacific Thermal Interface Materials Market Market Outlook, By Epoxy (2020-2028) ($MN)

- Table 82 Asia Pacific Thermal Interface Materials Market Market Outlook, By Polyimide (2020-2028) ($MN)

- Table 83 Asia Pacific Thermal Interface Materials Market Market Outlook, By Silicone (2020-2028) ($MN)

- Table 84 Asia Pacific Thermal Interface Materials Market Market Outlook, By Other Compositions (2020-2028) ($MN)

- Table 85 Asia Pacific Thermal Interface Materials Market Market Outlook, By Applications (2020-2028) ($MN)

- Table 86 Asia Pacific Thermal Interface Materials Market Market Outlook, By Computers (2020-2028) ($MN)

- Table 87 Asia Pacific Thermal Interface Materials Market Market Outlook, By Telecommunications (2020-2028) ($MN)

- Table 88 Asia Pacific Thermal Interface Materials Market Market Outlook, By Medical Devices (2020-2028) ($MN)

- Table 89 Asia Pacific Thermal Interface Materials Market Market Outlook, By Industrial Machinery (2020-2028) ($MN)

- Table 90 Asia Pacific Thermal Interface Materials Market Market Outlook, By Consumer Durables (2020-2028) ($MN)

- Table 91 Asia Pacific Thermal Interface Materials Market Market Outlook, By Automotive Electronics (2020-2028) ($MN)

- Table 92 Asia Pacific Thermal Interface Materials Market Market Outlook, By Other Applications (2020-2028) ($MN)

- Table 93 South America Thermal Interface Materials Market Market Outlook, By Country (2020-2028) ($MN)

- Table 94 South America Thermal Interface Materials Market Market Outlook, By Product Type (2020-2028) ($MN)

- Table 95 South America Thermal Interface Materials Market Market Outlook, By Tapes and Films (2020-2028) ($MN)

- Table 96 South America Thermal Interface Materials Market Market Outlook, By Gap Fillers Metallic TIMs (2020-2028) ($MN)

- Table 97 South America Thermal Interface Materials Market Market Outlook, By Elastomeric Pads (2020-2028) ($MN)

- Table 98 South America Thermal Interface Materials Market Market Outlook, By Greases & Adhesives (2020-2028) ($MN)

- Table 99 South America Thermal Interface Materials Market Market Outlook, By Metal Based Thermal (2020-2028) ($MN)

- Table 100 South America Thermal Interface Materials Market Market Outlook, By Interface Materials (2020-2028) ($MN)

- Table 101 South America Thermal Interface Materials Market Market Outlook, By Phase Change Materials (2020-2028) ($MN)

- Table 102 South America Thermal Interface Materials Market Market Outlook, By Other Product Types (2020-2028) ($MN)

- Table 103 South America Thermal Interface Materials Market Market Outlook, By Composition (2020-2028) ($MN)

- Table 104 South America Thermal Interface Materials Market Market Outlook, By Epoxy (2020-2028) ($MN)

- Table 105 South America Thermal Interface Materials Market Market Outlook, By Polyimide (2020-2028) ($MN)

- Table 106 South America Thermal Interface Materials Market Market Outlook, By Silicone (2020-2028) ($MN)

- Table 107 South America Thermal Interface Materials Market Market Outlook, By Other Compositions (2020-2028) ($MN)

- Table 108 South America Thermal Interface Materials Market Market Outlook, By Applications (2020-2028) ($MN)

- Table 109 South America Thermal Interface Materials Market Market Outlook, By Computers (2020-2028) ($MN)

- Table 110 South America Thermal Interface Materials Market Market Outlook, By Telecommunications (2020-2028) ($MN)

- Table 111 South America Thermal Interface Materials Market Market Outlook, By Medical Devices (2020-2028) ($MN)

- Table 112 South America Thermal Interface Materials Market Market Outlook, By Industrial Machinery (2020-2028) ($MN)

- Table 113 South America Thermal Interface Materials Market Market Outlook, By Consumer Durables (2020-2028) ($MN)

- Table 114 South America Thermal Interface Materials Market Market Outlook, By Automotive Electronics (2020-2028) ($MN)

- Table 115 South America Thermal Interface Materials Market Market Outlook, By Other Applications (2020-2028) ($MN)

- Table 116 Middle East & Africa Thermal Interface Materials Market Market Outlook, By Country (2020-2028) ($MN)

- Table 117 Middle East & Africa Thermal Interface Materials Market Market Outlook, By Product Type (2020-2028) ($MN)

- Table 118 Middle East & Africa Thermal Interface Materials Market Market Outlook, By Tapes and Films (2020-2028) ($MN)

- Table 119 Middle East & Africa Thermal Interface Materials Market Market Outlook, By Gap Fillers Metallic TIMs (2020-2028) ($MN)

- Table 120 Middle East & Africa Thermal Interface Materials Market Market Outlook, By Elastomeric Pads (2020-2028) ($MN)

- Table 121 Middle East & Africa Thermal Interface Materials Market Market Outlook, By Greases & Adhesives (2020-2028) ($MN)

- Table 122 Middle East & Africa Thermal Interface Materials Market Market Outlook, By Metal Based Thermal (2020-2028) ($MN)

- Table 123 Middle East & Africa Thermal Interface Materials Market Market Outlook, By Interface Materials (2020-2028) ($MN)

- Table 124 Middle East & Africa Thermal Interface Materials Market Market Outlook, By Phase Change Materials (2020-2028) ($MN)

- Table 125 Middle East & Africa Thermal Interface Materials Market Market Outlook, By Other Product Types (2020-2028) ($MN)

- Table 126 Middle East & Africa Thermal Interface Materials Market Market Outlook, By Composition (2020-2028) ($MN)

- Table 127 Middle East & Africa Thermal Interface Materials Market Market Outlook, By Epoxy (2020-2028) ($MN)

- Table 128 Middle East & Africa Thermal Interface Materials Market Market Outlook, By Polyimide (2020-2028) ($MN)

- Table 129 Middle East & Africa Thermal Interface Materials Market Market Outlook, By Silicone (2020-2028) ($MN)

- Table 130 Middle East & Africa Thermal Interface Materials Market Market Outlook, By Other Compositions (2020-2028) ($MN)

- Table 131 Middle East & Africa Thermal Interface Materials Market Market Outlook, By Applications (2020-2028) ($MN)

- Table 132 Middle East & Africa Thermal Interface Materials Market Market Outlook, By Computers (2020-2028) ($MN)

- Table 133 Middle East & Africa Thermal Interface Materials Market Market Outlook, By Telecommunications (2020-2028) ($MN)

- Table 134 Middle East & Africa Thermal Interface Materials Market Market Outlook, By Medical Devices (2020-2028) ($MN)

- Table 135 Middle East & Africa Thermal Interface Materials Market Market Outlook, By Industrial Machinery (2020-2028) ($MN)

- Table 136 Middle East & Africa Thermal Interface Materials Market Market Outlook, By Consumer Durables (2020-2028) ($MN)

- Table 137 Middle East & Africa Thermal Interface Materials Market Market Outlook, By Automotive Electronics (2020-2028) ($MN)

- Table 138 Middle East & Africa Thermal Interface Materials Market Market Outlook, By Other Applications (2020-2028) ($MN)

According to Stratistics MRC, the Global Thermal Interface Materials Market is accounted for $2.14 billion in 2022 and is expected to reach $4.52 billion by 2028 growing at a CAGR of 13.3% during the forecast period. Thermal interface fillers are used to close up spaces and interfaces that naturally form between heat-generating parts and their corresponding heat sinks. In order to maximize heat transfer, these interface materials provide a conductive medium and eliminate air gaps. The demand for products that can improve heat transfer from device chips to the heat sink, preventing heat buildup and extending the life of the gadget, has increased with the production of compact, miniaturized, and high-energy-density gadgets.

According to the industrial analysis, it is expected that the automotive industry will grow to under nine trillion US dollars by 2030 globally. The new vehicle sales will account for approx. 38% of this value. Hence, the growing automotive sector will create beneficial opportunities for the growth of the thermal interface materials market.

Market Dynamics:

Driver:

Thermal interface materials are in demand due to the expanding led market.

Fluorescent lighting that uses more energy than necessary is currently being replaced by LED. However, there are some physical inconsistencies with LED lights by nature. To produce the desired lumen outputs, LED power must be high. At the same time, LED current must be low to minimize energy loss and heat generation. Applying the four separation principles separation in time and space, separation at the system level, and separation on condition can resolve these physical contradictions. Separation is the best course of action in many situations where optimizations have reached their limits. But a sufficient heat exchange medium is needed to lengthen the LED's operating life. They strike the ideal balance between factors like cost, heat dissipating capacity, and available space. The demand for TIMs is anticipated to increase proportionally to the growth in demand for LED lighting. Combining the optical and thermal design disciplines to improve the overall system efficiency and light quality, including the electronic driving system, is the challenge of a sophisticated LED design. As a result, the demand for and effectiveness of TIMs will be affected proportionately as LED designs become more advanced.

Restraint:

Performance of thermal interface materials is constrained by physical properties.

Power densities in electronic devices, particularly in microprocessor chips, have increased over the last few decades. Electronic circuit thermal problems have significantly increased as a result of the ongoing trend toward smaller device dimensions. Thus, it is increasingly important and fundamental to focus on thermal management in order to guarantee that electronic devices function as intended. Conductive heat transfer is typically used to disperse the heat from its point of generation into the extended surface area of a heat sink. However, a thermal management system may use all modes of heat transfer to maintain temperatures within their appropriate limits and ensure maximum performance and reliability. A crucial component of an assembly when solid surfaces are connected together to minimize contact resistance is the injection of TIMs into the joint to fill the air spaces. It is well known that TIMs are the primary cause of the system's thermal resistance, even though their introduction facilitates heat transfer across an interface.

Opportunity:

Increased demand for thermal interface materials in the automotive industry

There are numerous types of thermal interface materials found in automobiles, including essential gels, gap-filling and insulating pads, adhesive tapes, and greases. The automotive industry is anticipated to grow to less than nine trillion US dollars globally by 2030, according to the industrial analysis. This value will be accounted for by new car sales to the tune of about 38%. In light of this, the expanding automotive industry will present favorable opportunities for the market for thermal interface materials to expand. Additionally, the forecast period will bring about a number of new opportunities for the market to expand due to rising technological advancements, a variety of end-user industries, and rising demand for thermal interface materials from emerging economies.

Threat:

Determining the best operating costs for users

The thermal conductivity of TIMs directly relates to their price. However, an increase in thermal conductivity also has a detrimental effect on the assembly as a whole due to poor handling and decreased conformability. The cost of TIMs and the cost of ownership of equipment are influenced by factors like thermal conductivity, phase change, viscosity, pressure, outgassing, surface finish, ease of application, and mechanical properties of the material.

COVID-19 Impact:

The COVID-19 epidemic significantly reduced demand for thermal interface materials, but it only lasted a short while. The growing Acceptance of teleconferencing and trends toward remote working have necessitated the materials. The work-from-home strategy stimulated market growth and raised sales of laptops, smartphones, personal computers, and other technology. Healthcare devices require more thermal interface materials due to the rise in demand for medical equipment.

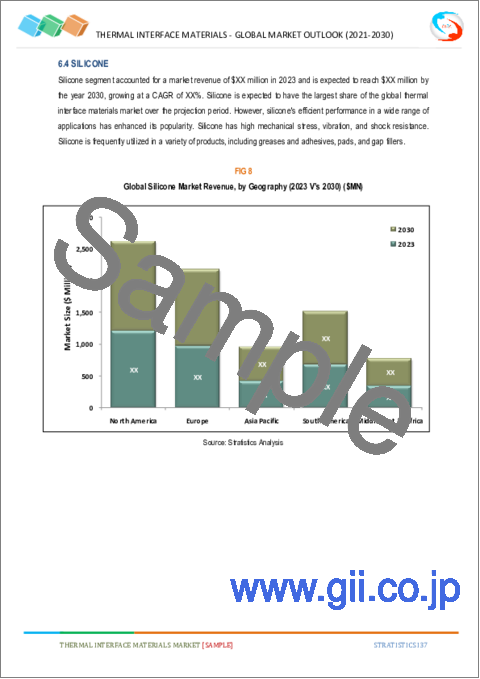

The silicone segment is expected to be the largest during the forecast period

The largest market share was held by the silicone segment. In terms of thermal interface materials, silicon led the way in 2021. Silicone has become more widely used as a result of its effective performance in a variety of applications. Silicone has a high level of resistance to shock, vibration, and mechanical stress. In numerous products, including pads, gap fillers, greases, and adhesives, silicone is frequently used.

The elastomeric pads segment is expected to have the highest CAGR during the forecast period

Due to their straightforward handling and installation procedures for thermal conductivity in electrical and electronic components, elastomeric pads are predicted to experience a significant CAGR during the forecasted period. However, it is anticipated that the limited application space and high product unit costs will stifle growth in the anticipated time frame.

Region with highest share:

Due to the presence of a sizable manufacturing base for a variety of industries in the region, Asia Pacific led the market with the highest revenue share of more than 37% in 2019. Aside from the region's manufacturing base, factors like lower corporate taxes, rising household incomes, a decline in the Goods and Services Tax (GST), consumer health consciousness, supportive governmental policies, and changing lifestyles may have had an impact on the development of the thermal interface materials sector in the area.

Region with highest CAGR:

During the forecast period, Asia-Pacific is anticipated to grow significantly. The region's market for thermal interface materials is expanding as a result of increased urbanization, industrialization, and consumer and telecommunications device demand. The adoption of thermal interface materials in Asia-Pacific is further boosted by their expanding use in medical devices and the rising popularity of electric and hybrid vehicles. The introduction of programs to encourage the use of renewable energy sources, investments in R&D by both public and private organizations, and technological advancements all help to speed up market growth in the area.

Key players in the market:

Some of the key players in Thermal Interface Materials market include AIM Specialty Materials, AOS Thermal Compounds LLC, CSL Silicones Inc. , CSW Industrials, Inc. , Fuji Polymer Industries Co., Ltd., GrafTech International Ltd., Henkel AG and Co. KgaA , Honeywell International, Inc., Hylomar LLC , Indium Corporation, Laird Technologies, Inc., Linseis GmbH, llinois Tool Works Inc , Mcgill Airseal LLC , Momentive Performance Materials, Inc., Parker Hannifin Corp., Pidilite Industries Ltd. , PPG Industries , Shin-Etsu Chemical Co. Ltd., The 3M Company, The Dow Chemical Company, Wacker Chemie AG and Wakefield Thermal, Inc.

Key Developments:

In June 2022, Dow Corning Corporation launched a new TIMs, DOWSIL TC-4040. This gap filler is easy to dispense, possess high thermal conductivity, and resist slumping. This new product launch will help the company stay competitive in the TIMs market.

In January 2022, 3M expanded its operations in Clinton, Tennessee. 3M invested approximately USD 470 million and adding around 600 new jobs by 2025 at its plant in Clinton, Tennessee.

In September 2020, Parker Hannifin Corporation launched THERM-A-GAP GEL 37, a new single component, thermally conductive dispensable material. This new product launch will help the company to strengthen its product portfolio in the TIMs market.

Product Types Covered:

- Tapes and Films

- Gap Fillers Metallic TIMs

- Elastomeric Pads

- Greases & Adhesives

- Metal Based Thermal

- Interface Materials

- Phase Change Materials

- Other Product Types

Compositions Covered:

- Epoxy

- Polyimide

- Silicone

- Other Compositions

Applications Covered:

- Computers

- Telecommunications

- Medical Devices

- Industrial Machinery

- Consumer Durables

- Automotive Electronics

- Other Applications

Regions Covered:

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- Italy

- France

- Spain

- Rest of Europe

- Asia Pacific

- Japan

- China

- India

- Australia

- New Zealand

- South Korea

- Rest of Asia Pacific

- South America

- Argentina

- Brazil

- Chile

- Rest of South America

- Middle East & Africa

- Saudi Arabia

- UAE

- Qatar

- South Africa

- Rest of Middle East & Africa

What our report offers:

- Market share assessments for the regional and country-level segments

- Strategic recommendations for the new entrants

- Covers Market data for the years 2020, 2021, 2022, 2025, and 2028

- Market Trends (Drivers, Constraints, Opportunities, Threats, Challenges, Investment Opportunities, and recommendations)

- Strategic recommendations in key business segments based on the market estimations

- Competitive landscaping mapping the key common trends

- Company profiling with detailed strategies, financials, and recent developments

- Supply chain trends mapping the latest technological advancements

Free Customization Offerings:

All the customers of this report will be entitled to receive one of the following free customization options:

- Company Profiling

- Comprehensive profiling of additional market players (up to 3)

- SWOT Analysis of key players (up to 3)

- Regional Segmentation

- Market estimations, Forecasts and CAGR of any prominent country as per the client's interest (Note: Depends on feasibility check)

- Competitive Benchmarking

- Benchmarking of key players based on product portfolio, geographical presence, and strategic alliances

Table of Contents

1 Executive Summary

2 Preface

- 2.1 Abstract

- 2.2 Stake Holders

- 2.3 Research Scope

- 2.4 Research Methodology

- 2.4.1 Data Mining

- 2.4.2 Data Analysis

- 2.4.3 Data Validation

- 2.4.4 Research Approach

- 2.5 Research Sources

- 2.5.1 Primary Research Sources

- 2.5.2 Secondary Research Sources

- 2.5.3 Assumptions

3 Market Trend Analysis

- 3.1 Introduction

- 3.2 Drivers

- 3.3 Restraints

- 3.4 Opportunities

- 3.5 Threats

- 3.6 Product Analysis

- 3.7 Application Analysis

- 3.8 Emerging Markets

- 3.9 Impact of Covid-19

4 Porters Five Force Analysis

- 4.1 Bargaining power of suppliers

- 4.2 Bargaining power of buyers

- 4.3 Threat of substitutes

- 4.4 Threat of new entrants

- 4.5 Competitive rivalry

5 Global Thermal Interface Materials Market Market, By Product Type

- 5.1 Introduction

- 5.2 Tapes and Films

- 5.3 Gap Fillers Metallic TIMs

- 5.4 Elastomeric Pads

- 5.5 Greases & Adhesives

- 5.6 Metal Based Thermal

- 5.7 Interface Materials

- 5.8 Phase Change Materials

- 5.9 Other Product Types

6 Global Thermal Interface Materials Market Market, By Composition

- 6.1 Introduction

- 6.2 Epoxy

- 6.3 Polyimide

- 6.4 Silicone

- 6.5 Other Compositions

7 Global Thermal Interface Materials Market Market, By Applications

- 7.1 Introduction

- 7.2 Computers

- 7.3 Telecommunications

- 7.4 Medical Devices

- 7.5 Industrial Machinery

- 7.6 Consumer Durables

- 7.7 Automotive Electronics

- 7.8 Other Applications

8 Global Thermal Interface Materials Market Market, By Geography

- 8.1 Introduction

- 8.2 North America

- 8.2.1 US

- 8.2.2 Canada

- 8.2.3 Mexico

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 Italy

- 8.3.4 France

- 8.3.5 Spain

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 Japan

- 8.4.2 China

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 New Zealand

- 8.4.6 South Korea

- 8.4.7 Rest of Asia Pacific

- 8.5 South America

- 8.5.1 Argentina

- 8.5.2 Brazil

- 8.5.3 Chile

- 8.5.4 Rest of South America

- 8.6 Middle East & Africa

- 8.6.1 Saudi Arabia

- 8.6.2 UAE

- 8.6.3 Qatar

- 8.6.4 South Africa

- 8.6.5 Rest of Middle East & Africa

9 Key Developments

- 9.1 Agreements, Partnerships, Collaborations and Joint Ventures

- 9.2 Acquisitions & Mergers

- 9.3 New Product Launch

- 9.4 Expansions

- 9.5 Other Key Strategies

10 Company Profiling

- 10.1 AIM Specialty Materials

- 10.2 AOS Thermal Compounds LLC

- 10.3 CSL Smart Helmet Inc.

- 10.4 CSW Industrials, Inc.

- 10.5 Fuji Polymer Industries Co., Ltd.

- 10.6 GrafTech International Ltd.

- 10.7 Henkel AG and Co. KgaA

- 10.8 Honeywell International, Inc.

- 10.9 Hylomar LLC

- 10.10 Indium Corporation

- 10.11 Laird Technologies, Inc.

- 10.12 Linseis GmbH

- 10.13 llinois Tool Works Inc

- 10.14 Mcgill Airseal LLC

- 10.15 Momentive Performance Materials, Inc.

- 10.16 Parker Hannifin Corp.

- 10.17 Pidilite Industries Ltd.

- 10.18 PPG Industries

- 10.19 Shin-Etsu Chemical Co. Ltd.

- 10.20 The 3M Company

- 10.21 The Dow Chemical Company

- 10.22 Wacker Chemie AG

- 10.23 Wakefield Thermal, Inc.