|

|

市場調査レポート

商品コード

1270831

通信事業者による2022年の5Gへの代償 - 借入金の増加、マージンの低下:COVID以降、投資が急増し、一部の通信事業者は厳しい状況に- 金利上昇と新たな収益が見込めず、借入金増加を管理する必要があるTelcos Pay 5G Price - Higher Debt, Lower Margins in 2022: Investments Have Surged Since COVID, Putting Some Telcos in Tough Spot - Need to Manage Higher Debt as Interest Rates Rise and New Revenues Fail to Appear |

||||||

|

|

|||||||

|

|||||||

価格

| 通信事業者による2022年の5Gへの代償 - 借入金の増加、マージンの低下:COVID以降、投資が急増し、一部の通信事業者は厳しい状況に- 金利上昇と新たな収益が見込めず、借入金増加を管理する必要がある |

|

出版日: 2023年05月03日

発行: MTN Consulting, LLC

ページ情報: 英文 8 Pages

納期: 即納可能

|

- 全表示

- 概要

- 図表

- 目次

概要

2022年第4四半期の通信事業者の負債総額は1兆1,400億米ドルとなり、17%が来年に返済期限を迎えます。売上高に占めるソフトウェア設備投資の割合は、2022年には1.9%となり、2021年の1.8%から少し上昇しました。買収への支出は2022年に売上高の0.5%となり、2012年以降で最も低い数値となっています。

ビジュアル

当レポートは、通信事業者に焦点を当て、これまでの設備投資動向、2022年第4四半期の負債、今後の見通しなどについてまとめています。

目次

- サマリー

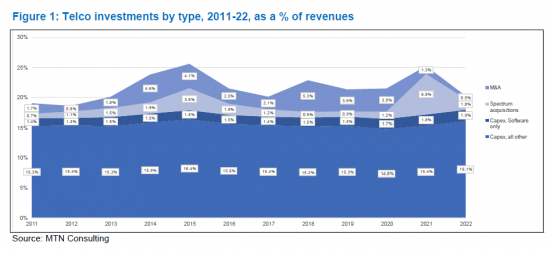

- 通信事業者は過去2年間、設備投資、周波数帯、M&Aに多額の費用を費やした

- 2022年第4四半期の通信会社負債総額は1兆1,400億米ドルで、17%は来年に返済期限となる

- 純負債は2022年に減少したが、EBITDAに対する比率は2015~19年と一致した

- 多くの個々の通信事業者は支出を制限する債務レベルを抱える

- 利益、負債、支出見通しへの影響

- 付録

図表

List of Figures

- Figure 1: Telco investments by type, 2011-22, as a % of revenues

- Figure 2: Telco sector total debt in US$B, and short-term debt as % total

- Figure 3: Components of telco sector total debt at year-end 2022 (US$B)*

- Figure 4: Telco industry net debt ($M) and net debt to EBITDA ratio, 2011-22

- Figure 5: Telcos with net debt to EBITDA ratios above 3 (YE2022)**

目次

Product Code: GNI-03052023-1

This brief report presents data aimed at shedding light on the following question: can telcos afford to pay for their future investment needs? The report considers debt, cash, and margin metrics, for the industry overall and for specific key players. It also speculates how 2022 trends may impact 2023 and beyond, in a rising interest rate climate. A number of large telcos have high debt, low margins, and/or weak top line growth, and may have to curtail spending in 2023-4 in order to cope with this reality.

VISUALS

Key findings include:

- Total telco debt in 4Q22 was $1.14 trillion, 17% due in next year

- Software capex as a % of revenues was 1.9% in 2022, up a bit from 1.8% in 2021.

- Spending on acquisitions amounted to 0.5% of revenues in 2022, the lowest figure since 2012.

- At the industry level, the ratio of net debt to EBITDA in 2022 was 1.9, a bit up from 2021 but down from 2020.

- A number of large telcos face short-term debt levels over 30% of total debt

- Average margins for the industry in 2022 disappointed: free cash flow margin for the telco industry in 2022 was 11.4%, down from 12.6% in 2021; EBITDA margin was 33.7% (2021: 34.0%), and EBIT margin was 14.4% (2021: 14.9%).

Companies mentioned:

|

|

Table of Contents

- Summary

- Telcos have spent big on capex, spectrum and M&A in last 2 years

- Total telco debt in 4Q22 was $1.14 trillion, 17% due in next year

- Net debt declined in 2022 but ratio to EBITDA in line with 2015-19

- Many individual telcos have debt levels which will constrain their spending

- Margins, debt, and implications for spending outlook

- Appendix

お電話でのお問い合わせ

044-952-0102

( 土日・祝日を除く )