|

市場調査レポート

商品コード

1690829

世界の製剤開発アウトソーシング-市場シェア分析、業界動向・統計、成長予測(2025年~2030年)Global Formulation Development Outsourcing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 世界の製剤開発アウトソーシング-市場シェア分析、業界動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 164 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

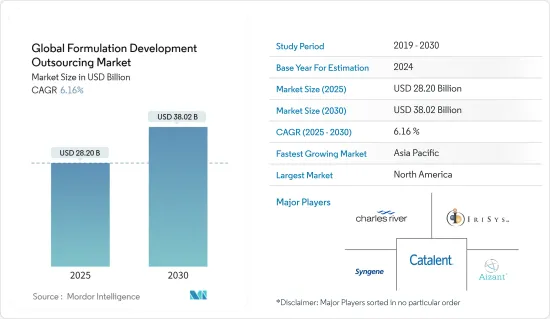

世界の製剤開発アウトソーシング市場規模は2025年に282億米ドルと推定され、予測期間(2025~2030年)のCAGRは6.16%で、2030年には380億2,000万米ドルに達すると予測されます。

COVID-19が大流行する中、各国の医療制度はウイルスと闘うための研究開発に急速に投資しており、製剤開発アウトソーシング市場に大きな影響を与えています。例えば、2020年10月、AiPharmaはCOVID-19に対する経口抗ウイルス剤Avigan/Reeqomusの開発を進めるため、製薬、製造、流通のリーダーによる世界のコンソーシアムに参加しました。このコンソーシアムの一員として、アイファーマは、COVID-19と他の11の感染症を標的とする広範な経口抗ウイルス薬であるファビピラビルのすべての製剤を商業化しています。このように、パンデミックの発生は製剤開発アウトソーシング市場に大きな利益をもたらしています。さらに、2021年8月に発表された「Pharmaceutical Technology, 2021 Outsourcing Resources Supplement(製薬技術、2021年アウトソーシングリソース補足)」と題する記事によると、製薬アウトソーシング市場では、特にCOVID-19パンデミックへの産業の対応により、過去1年間にワクチン開発と製造活動が増加しました。その結果、製剤開発のアウトソーシング活動が増加し、市場拡大に寄与しています。

さらに、主要医薬品の特許切れ動向や製薬・バイオ製薬企業のアウトソーシング増加も、市場成長を後押しする主要因となっています。主要医薬品の特許切れ動向の増加が市場成長の原動力となっています。例えば、ジェネリック医薬品・バイオシミラー・イニシアチブによる2021年の更新によると、ジェネリック医薬品の品質を向上させ、効率的で競合ジェネリック医薬品市場を確保するための継続的な活動の一環として、韓国食品医薬品安全部(MFDS)は、2021年に158件の医薬品の特許が失効すると予想されると発表しました。同ソースによると、MFDSのグリーンリスト(米国食品医薬品局(FDA)のオレンジブックに類似したリスト)によると、44件の特許は、関連する製品に関する他の特許がないため、すぐにジェネリック医薬品に参入できる状態になっています。このため、新規候補品の製剤開発アウトソーシングのニーズが高まり、市場拡大に寄与しています。

しかし、製薬産業の構造変化や、製剤開発を通じて医薬品開発プロセスを実施するための資金不足が、市場開拓を阻害する主要因となっています。

製剤開発アウトソーシング市場動向

予測期間中、がん領域が大幅な成長を遂げる見込み

用途別では、がん領域が市場の主要シェアを占めると予測されます。この背景には、世界のがん罹患率の上昇があります。世界保健機関(WHO)によると、2020年のがんによる死亡者数は約1,000万人です。さらに、米国がん協会による2021年の統計によると、2040年までに、がんの世界の負担は2,750万人の新規罹患者と1,630万人のがん死亡者にまで拡大すると予想されています。

安定性、溶解性、バイオアベイラビリティを含む製剤の問題は、医薬品開発プロセスにとって重要な考慮事項であるため、製剤開発は抗がん剤において重要な役割を果たしています。したがって、ほとんどの製薬サービス会社は、がん治療開発のためのエンドツーエンドのソリューションを提供するために、がん治療の製剤開発に注力しています。例えば、2021年11月、Oncology Pharma Inc.は、NanoSmart Pharmaceuticals Inc.との共同開発プロジェクトにおけるリード医薬品候補の開発計画を明らかにしました。同様に、2021年10月、米国を拠点とするMayne Pharmaの医薬品開発・製造受託部門であるメトリックスコントラクトサービスは、ESSA Pharmaceuticalsと開発・製造契約を締結しました。Metricsは、本契約の一環として、経口投与がん治療の進行中の臨床開発をサポートするため、製剤開発、分析サービス、製造を記載しています。

このように、がん罹患率の高さとバイオ医薬品企業によるがん治療への注目の高まりが、予測期間中の同セグメントの成長を後押しするとみられます。

予測期間中、北米が大きな市場シェアを占める見込み

北米では米国が大きなシェアを占めると予想されます。これは、慢性疾患の負担が増加していることと、同地域、特に米国に主要企業が存在することに起因しています。主要医薬品のほとんどが特許切れの段階にあるため、主要企業は新薬開発に取り組んでいます。こうした中、製薬企業は製剤開発における一連の臨床検査や評価検査への時間と投資を節約するため、製剤開発サービスをCROにアウトソーシングしており、これが同地域の市場開拓を促進する可能性があります。

さらに、COVID-19パンデミックの中、いくつかの共同研究プログラムは、Biomedical Advanced Research and Development Authority(BARDA)やCoalition for Epidemic Preparedness Innovations(CEPI)などの機関と協力することで、治療やワクチンの開発プロセスを迅速に進めようとしています。例えば、2020年5月、米国商務省の国立標準技術ラボ(NIST)は、発生したアウトブレイクに対応して、影響の大きいバイオ医薬品製造プロジェクトに約890万米ドルの資金を提供しました。そのため、こうした取り組みが製剤開発のアウトソーシング増加に寄与し、市場開拓に貢献しています。

さらに、複数の市場参入企業が戦略的イニシアチブの実施に取り組んでおり、市場成長に寄与しています。例えば、2022年1月、主に低分子治療開発における複雑な製剤・製造課題の解決に特化した開発・製造受託機関(CDMO)であるRecro Pharma Inc.は、米国政府の主要部門から新たな製剤開発とcGMP製造契約を受注したことを報告しました。

このように、上記の要因により、市場は予測期間中に大幅な成長が見込まれます。

製剤開発アウトソーシング産業概要

製剤開発アウトソーシング市場の競争は中程度です。市場シェアでは、Charles River Laboratories、Aizant Drug Research Solutions Private Limited、Catalent Inc.社、Laboratory Corporation of America Holdings、Syngene International Ltdなど数社が最大シェアを占めています。主要な市場参入企業は、買収、提携、新製品の発売など、さまざまな戦略的提携を通じて進化を遂げ、世界の製品ポートフォリオを拡大し、世界市場での地位を確保しています。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場の促進要因

- 主要医薬品の特許切れ動向の増加

- アウトソーシングする製薬・バイオ医薬品企業の増加

- 市場抑制要因

- 製薬産業の構造変化

- 製剤開発を通じた医薬品開発プロセスを実施するための資金不足

- 産業の魅力-ポーターのファイブフォース分析

- 買い手・消費者の交渉力

- 供給企業の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- サービス別

- プレフォーミュレーションサービス

- 創薬と前臨床検査サービス

- 分析サービス

- 製剤最適化

- フェーズI

- フェーズII

- フェーズIII

- フェーズIV

- プレフォーミュレーションサービス

- 剤形別

- 注射剤

- 経口剤

- 外用剤

- その他

- 用途別

- 腫瘍学

- 遺伝子疾患

- 神経学

- 感染症

- 呼吸器

- 循環器

- その他

- エンドユーザー別

- 製薬会社とバイオ製薬会社

- 政府機関と学術機関

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他の欧州

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- その他のアジア太平洋

- 中東・アフリカ

- GCC諸国

- 南アフリカ

- その他の中東・アフリカ

- 南米

- ブラジル

- アルゼンチン

- その他の南米

- 北米

第6章 競合情勢

- 企業プロファイル

- Charles River Laboratories

- Aizant Drug Research Solutions Private Limited

- Catalent Inc.

- Laboratory Corporation of America Holdings

- Syngene International Ltd

- Irisys LLC

- Intertek Group PLC

- Piramal Pharma Solutions

- QIoTient Sciences

- Patheon(Thermo Fisher Scientific Inc.)

- Emergent BioSolutions Inc.

- Lonza Group AG

- Dr. Reddy's Laboratories Ltd

第7章 市場機会と今後の動向

The Global Formulation Development Outsourcing Market size is estimated at USD 28.20 billion in 2025, and is expected to reach USD 38.02 billion by 2030, at a CAGR of 6.16% during the forecast period (2025-2030).

Amid the COVID-19 pandemic, countries' health systems are rapidly investing in research and development to combat the virus, having a significant impact on the formulation development outsourcing market. For instance, in October 2020, AiPharma joined a global consortium of pharmaceutical, manufacturing, and distribution leaders to advance oral antiviral Avigan/Reeqomus for COVID-19. As a part of the consortium, AiPharma commercializes all formulations of favipiravir, a broad spectrum oral antiviral drug that targets COVID-19 and 11 other infectious diseases. Thus, the onset of the pandemic has significantly benefitted the formulation development outsourcing market. Moreover, as per an article titled 'Pharmaceutical Technology, 2021 Outsourcing Resources Supplement', published in August 2021, the pharmaceutical outsourcing market has seen a growth in vaccine development and manufacturing activity in the past year, particularly due to the industry's response to the COVID-19 pandemic. As a result of which, there has been an increase in the formulation development outsourcing activities, thereby contributing to the market growth.

Furthermore, the major factors fueling the market growth are the increasing trend of patent protection expiration of major drugs and the rising number of pharmaceutical and biopharmaceutical companies outsourcing their services. The increasing trend of patent protection expiration of major drugs is driving the market growth. For instance, as per a 2021 update by the Generics and Biosimilar Initiative, as part of ongoing action to improve the quality of generics and ensure an efficient and competitive generics market, the Korean Ministry of Food and Drug Safety (MFDS) announced that 158 patents for pharmaceutical products were anticipated to expire in 2021. As per the same source, the MFDS's Green List (a list similar to the US Food and Drug Administration's (FDA) Orange Book) shows that 44 of the patents will be ready for immediate generics entry, having no other patents on the products involved. Thus, this increases the need for formulation development outsourcing for newer candidates, thereby contributing to the market growth.

However, structural changes in the pharmaceutical industry and insufficient funding to perform the drug development process through formulation development are the major factors hindering the market growth.

Formulation Development Outsourcing Market Trends

The Oncology Segment is Expected to Witness Significant Growth over the Forecast Period

By application, the oncology segment is anticipated to hold a major share of the market. This can be attributed to the rising incidence rates of cancer cases globally. According to the World Health Organization (WHO), cancer accounted for approximately 10 million deaths in 2020. Additionally, as per the 2021 statistics by the American Cancer Society, by 2040, the global burden of cancer is expected to grow to 27.5 million new cases and 16.3 million cancer deaths.

Formulation development plays a vital role in anti-cancer drugs, as formulation issues, including stability, solubility, and bioavailability, are important considerations for the drug development process. Hence, most pharma service companies are focused on oncology formulation development to provide end-to-end solutions for oncology drug development. For instance, in November 2021, Oncology Pharma Inc. revealed plans for the development of a lead drug candidate in a co-development project with NanoSmart Pharmaceuticals Inc. Likewise, in October 2021, Metrics Contract Services, the US-based contract pharmaceutical development and manufacturing division of Mayne Pharma entered a development and manufacturing agreement with ESSA Pharmaceuticals. Metrics will provide formulation development, analytical services, and manufacturing to support the ongoing clinical development of an orally administered oncology drug as a part of the agreement.

Thus, the high incidence rates of cancer cases and the increasing focus on cancer therapeutics by biopharmaceutical companies are expected to aid in the growth of the segment over the forecast period.

North America is Expected to Hold Significant Market Share over the Forecast Period

Within North America, the United States is expected to hold a major share of the market. This can be attributed to the growing burden of chronic diseases and the presence of key players in the region, especially in the United States. As most of the major drugs are in the stage of patent expiration, key players are involved in novel drug development. In this context, to save time and investment on a series of clinical trials and evaluation studies in formulation development, pharmaceutical companies are outsourcing formulation development services to CROs, which may drive market growth in the region.

Additionally, amid the COVID-19 pandemic, several collaborative research programs are looking to fast-track their process in terms of advancing therapeutics and vaccines by collaborating with institutions, such as the Biomedical Advanced Research and Development Authority (BARDA) and Coalition for Epidemic Preparedness Innovations (CEPI). For instance, in May 2020, the United States Department of Commerce's National Institute of Standards and Technology (NIST) funded around USD 8.9 million to the highly impacted biopharmaceutical manufacturing projects in response to the emerged outbreak. Therefore, such initiatives are contributing to the increasing outsourcing for formulation development, thereby contributing to the market growth.

Moreover, several market players are engaged in the implementation of strategic initiatives, thereby contributing to market growth. For instance, in January 2022, Recro Pharma Inc., a contract development and manufacturing organization (CDMO) dedicated to solving complex formulation and manufacturing challenges primarily in small molecule therapeutic development, reported being awarded a new formulation development and cGMP manufacturing contract from a key department of the United States government.

Thus, due to the above-mentioned factors, the market is expected to witness significant growth over the forecast period.

Formulation Development Outsourcing Industry Overview

The formulation development outsourcing market is moderately competitive. In terms of market share, a few companies, such as Charles River Laboratories, Aizant Drug Research Solutions Private Limited, Catalent Inc., Laboratory Corporation of America Holdings, and Syngene International Ltd, among others, hold the largest market shares. Key market players are evolving through various strategic alliances, such as acquisitions, collaborations, and new product launches, to expand their global product portfolios and secure their positions in the global market.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Trend of Patent Protection Expiration of Major Drugs

- 4.2.2 Rising Number of Pharmaceutical and Biopharmaceutical Companies Outsourcing Their Services

- 4.3 Market Restraints

- 4.3.1 Structural Changes in the Pharmaceutical Industry

- 4.3.2 Insufficient Funding to Perform the Drug Development Process Through Formulation Development

- 4.4 Industry Attractiveness - Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Buyers/Consumers

- 4.4.2 Bargaining Power of Suppliers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size by Value - USD million)

- 5.1 By Service

- 5.1.1 Pre-formulation Services

- 5.1.1.1 Discovery and Preclinical Services

- 5.1.1.2 Analytical Services

- 5.1.2 Formulation Optimization

- 5.1.2.1 Phase I

- 5.1.2.2 Phase II

- 5.1.2.3 Phase III

- 5.1.2.4 Phase IV

- 5.1.1 Pre-formulation Services

- 5.2 By Dosage Form

- 5.2.1 Injectable

- 5.2.2 Oral

- 5.2.3 Topical

- 5.2.4 Other Dosage Forms

- 5.3 By Application

- 5.3.1 Oncology

- 5.3.2 Genetic Disorders

- 5.3.3 Neurology

- 5.3.4 Infectious Diseases

- 5.3.5 Respiratory

- 5.3.6 Cardiovascular

- 5.3.7 Other Applications

- 5.4 By End User

- 5.4.1 Pharmaceutical and Biopharmaceutical Companies

- 5.4.2 Government and Academic Institutes

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle-East and Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle-East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Charles River Laboratories

- 6.1.2 Aizant Drug Research Solutions Private Limited

- 6.1.3 Catalent Inc.

- 6.1.4 Laboratory Corporation of America Holdings

- 6.1.5 Syngene International Ltd

- 6.1.6 Irisys LLC

- 6.1.7 Intertek Group PLC

- 6.1.8 Piramal Pharma Solutions

- 6.1.9 Qiotient Sciences

- 6.1.10 Patheon (Thermo Fisher Scientific Inc.)

- 6.1.11 Emergent BioSolutions Inc.

- 6.1.12 Lonza Group AG

- 6.1.13 Dr. Reddy's Laboratories Ltd