|

市場調査レポート

商品コード

1439796

生物分析検査サービス:市場シェア分析、業界動向と統計、成長予測(2024~2029年)Bioanalytical Testing Services - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 生物分析検査サービス:市場シェア分析、業界動向と統計、成長予測(2024~2029年) |

|

出版日: 2024年02月15日

発行: Mordor Intelligence

ページ情報: 英文 119 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

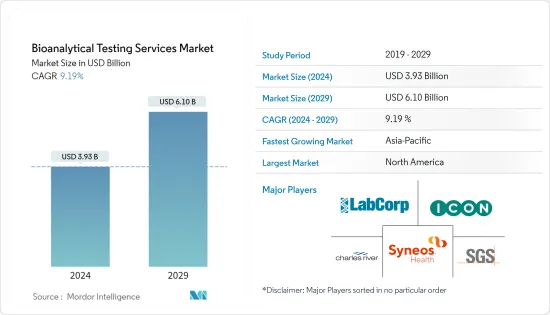

生物分析検査サービス市場規模は、2024年に39億3,000万米ドルと推定され、2029年までに61億米ドルに達すると予測されており、予測期間(2024年から2029年)中に9.19%のCAGRで成長します。

生物分析技術は、COVID-19ウイルス感染症のパンデミックを緩和する上で重要な役割を果たしており、今後もこのパンデミックの次の波や将来の感染症の流行を防ぐ上での基礎であり続けるでしょう。 SGSなどの企業は、質量分析、イムノアッセイ、細胞ベースのアッセイなど、小分子と生物製剤の両方に対するあらゆる生物分析サービスを提供しています。 2020年 11月、世界有数の検査、検証、試験、認証会社であるSGSは、グラスゴーにあるバイオセーフティセンターオブエクセレンスに投資し、効果的なワクチン、細胞および遺伝子治療の開発において科学者やメーカーをサポートする能力を強化しました。他の生物学的医薬品。

調査対象の市場の成長に貢献する主な要因は、研究開発活動における特定の種類のテストの必要性の増加と、臨床検査サービスのアウトソーシングの傾向が増加していることです。臨床検査サービスのアウトソーシングの増加傾向により、企業はさまざまな種類のサービスやソリューションを提供することで市場シェアを拡大しています。さらに、大手企業は合併、買収、その他の開発など、さまざまな戦略に注力しています。たとえば、2021年8月、ユーロフィンズ・サイエンティフィックは、日本におけるユーロフィンズの検査ポートフォリオを拡大するために、遺伝子解析における日本の大手企業であるジーンテック社を買収する契約をノーリツ鋼機と締結しました。生物分析検査サービスは重要な役割を果たします。したがって、市場は大幅に成長すると予想されます。

生物分析検査サービスの需要の増加は、感染症やHIVなどの蔓延の増加によるものである可能性もあります。さらに、新型コロナウイルス感染症(COVID-19)などの感染症の流行を制御するための政府の取り組みの高まりにより、より多くの機会が提供されると予想されます。調査対象の市場の成長に貢献すると期待されています。

生物分析検査サービス市場動向

低分子サブセグメントは生物分析検査サービス市場でさらなる成長を示すと予想される

小分子検査サービスのサブセグメントは、ブランド医薬品のジェネリック医薬品の開発において極めて重要な役割を果たしているため、成長が見込まれています。生物分析試験は、ジェネリック医薬品の放出プロファイルとブランド医薬品の放出プロファイルをシミュレートする効率を証明する上で重要な役割を果たし、その結果、このセグメントの成長につながります。

一方、大分子セグメントは、予測期間中に有利な成長を遂げると予想されます。大きな分子の生物分析試験は、バイオ医薬品分野にとって最も困難なタスクの1つです。そのため、Maldi-TOF-MS、リガンド結合アッセイ、サイズ排除アフィニティークロマトグラフィーなどのさまざまな技術が使用されます。大きな分子の生物分析試験は、一般にバイオ医薬品分野の確立された研究開発ラボで実施され、その後に他の第II相試験が行われます。一方、長期的な毒性研究はほとんどが外部委託されています。したがって、これらの分子の生物分析検査のアウトソーシングは、予測期間を通じて一般的な傾向となる可能性があります。

新型コロナウイルス感染症(COVID-19)のパンデミックにより、多くのバイオテクノロジー企業や製薬企業は、新型コロナウイルス感染症(COVID-19)の迅速な診断と、ヘルスケア全体にわたるケアの適切性を確保することで感染拡大の緩和に役立つワクチンや治療薬の開発のための効果的かつ迅速な技術に焦点を当てています。これにより、世界中で生物分析検査サービスの需要がさらに高まっています。たとえば、2020年7月、米国に本拠を置くGLP認定の受託調査機関であるCIRION BioPharma調査Inc.は、同社がCOVID-19に関連する医薬品およびワクチンの開発を支援するために既存の研究所施設を増強し、生物分析サービスを拡大すると発表しました。したがって、上記の要因により、小分子サブセグメントは予測期間中に大きく貢献すると予想されます。

北米が市場を独占しており、その優位性は予測期間中も継続すると予想される

北米は生物分析検査サービス市場を独占すると予想されており、この傾向は予測期間中続くと予想されます。これは主に、大量の進行中の調査活動や臨床試験を伴う生物分析サービスの需要の高まりに起因しており、これがこの地域の市場成長を促進すると予想されています。

北米では、さまざまな慢性疾患の患者数が増加し、副作用の多い小分子の代替としてペプチドやその他の大分子治療薬の採用が増加しているため、米国が最大の市場シェアを占めています。米国では慢性疾患に約3兆5,000億米ドルが費やされています。したがって、企業は、調査対象の市場を刺激すると予想される高い需要に対応するための取り組みを行っています。

さらに、国際糖尿病連盟によると、2020年には北米で約4,800万人の成人が糖尿病を抱えており、この傾向は今後も続くと予想されており、その結果、糖尿病患者の増加を阻止するための新規治療薬の生物分析に対する需要が高まっているといいます。したがって、生物分析サービスに対する需要の高まり、多数の進行中の臨床試験、および多くの大手製薬会社による巨額投資が、この国で研究されている市場の成長を推進する重要な要因となっています。

生物分析検査サービス業界の概要

生物分析検査サービス市場は適度な競争があり、いくつかの主要企業で構成されています。さまざまな種類のサービスを提供し、アッセイ検証のための新しい方法を開始することで市場での地位を拡大している企業もあれば、研究室向けソリューションを提供している企業もあります。現在市場を独占している企業には、SGS SA、ICON PLC、Laboratory Corporation of America Holdings、Syneos Health Inc.、Charles River Laboratories Inc.などがあります。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3か月のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 研究開発活動における特定の種類の試験の必要性の増加

- 臨床検査サービスのアウトソーシングの増加傾向

- 市場抑制要因

- 研究所を維持するための複雑な規制枠組み

- 適切な分析技術の開発における課題

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手の交渉力

- 供給企業の交渉力

- 代替製品の脅威

- 競争企業間の敵対関係の激しさ

第5章 市場セグメンテーション

- 分子タイプ別

- 低分子

- 高分子

- 検査タイプ別

- 生物学的利用能と生物学的同等性の研究

- 薬物動態

- 薬力学

- その他の検査タイプ

- 地域

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他欧州

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- その他アジア太平洋地域

- 中東とアフリカ

- GCC

- 南アフリカ

- その他中東およびアフリカ

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 北米

第6章 競合情勢

- 企業プロファイル

- Pharmaceutical Product Development LLC

- ICON PLC

- Laboratory Corporation of America Holdings

- Charles River Laboratories International Inc.

- Syneos Health

- SGS SA

- Toxikon Corporation

- Intertek Group PLC

- Wuxi Apptec Co. Ltd

第7章 市場機会と将来の動向

The Bioanalytical Testing Services Market size is estimated at USD 3.93 billion in 2024, and is expected to reach USD 6.10 billion by 2029, growing at a CAGR of 9.19% during the forecast period (2024-2029).

Bioanalytical technologies have played a critical role in mitigating the COVID-19 pandemic and will continue to be foundational in the prevention of the subsequent waves of this pandemic, along with future infectious disease outbreaks. Companies, such as SGS, offer a full range of bioanalytical services for both small molecules and biologics, including mass spectrometry, immunoassays, and cell-based assays. In November 2020, SGS, the world's leading inspection, verification, testing, and certification company, invested in its Biosafety Center of Excellence in Glasgow, boosting its capacity to support scientists and manufacturers in the development of effective vaccines, cell and gene therapies, and other biological medicines.

The major factor contributing to the growth of the market studied is the increased necessity for specific types of tests in R&D activities and the increasing trend of outsourcing laboratory testing services. Due to the increasing trend of outsourcing laboratory testing services, companies are expanding their market share by offering various types of services and solutions. Additionally, major players are focusing on different strategies, such as mergers, acquisitions, and other developments. For instance, in August 2021, Eurofins Scientific signed an agreement with Noritsu Koki Co. Ltd to acquire GeneTech Inc., a leading Japanese player in genetic analysis, to expand Eurofins' testing portfolio in Japan. The bioanalytical testing service plays an important role; hence, the market is anticipated to grow significantly.

The rise in demand for bioanalytical testing services can also be due to the growing prevalence of infectious diseases, HIV, etc. Additionally, rising government initiatives to control the outbreaks of infectious diseases such as COVID-19 is expected to provide more opportunities, which is expected to contribute to the growth of the market studied.

Bioanalytical Testing Services Market Trends

Small Molecule Sub-segment Expected to Show Better Growth in the Bioanalytical Testing Services Market

The small molecule testing services sub-segment is anticipated to witness growth due to its pivotal role in developing generic versions of branded drugs. Bioanalytical testing plays a significant role in proving the efficiency to simulate generic drug release profiles with that of branded drugs, resulting in the growth of the segment.

On the other hand, the large molecule segment is expected to witness lucrative growth during the forecast period. Bioanalytical testing of large molecules is one of the most challenging tasks for the biopharmaceutical sector. Hence, various techniques are used, such as Maldi-TOF-MS, Ligand Binding Assays, size exclusion affinity chromatography, etc. Bioanalytical testing of large molecules is generally conducted in well-established R&D labs by the biopharmaceutical sector, followed by other Phase II studies, while long-term toxicity studies are mostly outsourced. Hence, outsourcing bioanalytical testing of these molecules is likely to be the prevailing trend over the forecast period.

Owing to the COVID-19 pandemic, many biotech and pharmaceutical firms have been focusing on effective and rapid technologies for the fast diagnosis of COVID-19 and to develop vaccines/therapeutics that can help mitigate the spread by ensuring the appropriateness of care across all healthcare settings and achieving high-quality outcomes, which are further driving demand for the bioanalytical testing services globally. For instance, in July 2020, CIRION BioPharma Research Inc., a US-based GLP-certified contract research laboratory, announced that the company is expanding its bioanalytical services by increasing its existing laboratory facilities to support drug and vaccine developments related to COVID-19. Thus, the small molecule sub-segment is expected to contribute significantly over the forecast period due to the abovementioned factors.

North America Dominates the Market and its Dominance Expected to Continue in the Forecast Period

North America is expected to dominate the bioanalytical testing services market, and this trend is expected to continue over the forecast period. This can be majorly attributed to the growing demand for bioanalytical services with a high volume of ongoing research activities and clinical trials, which is expected to fuel the market growth in the region.

In North America, the US holds the largest market share due to the increased patient pool of various chronic diseases and increased adoption of peptides and other large molecule therapeutics as an alternative to small molecules that have more side effects. According to the Centers for Disease Control and Prevention, around USD 3.5 trillion is spent on chronic diseases in the US. Therefore, companies have been taking initiatives to meet the high demand, which is expected to fuel the market studied.

Moreover, according to the International Diabetes Federation, in 2020, about 48 million adults in North America were living with diabetes, and the trend is expected to continue, resulting in higher demand for bioanalysis of novel therapeutics to stop the growing diabetes patient pool. Thus, the rising demand for bioanalytical services, the large number of ongoing clinical trials, and huge investments by many major pharmaceutical companies are the key factors driving the growth of the market studied in the country.

Bioanalytical Testing Services Industry Overview

The bioanalytical testing services market is moderately competitive and consists of several major players. Some of the companies are expanding their market position by offering various types of services, launching new methods for assay validation, while others are offering laboratory solutions. Some companies currently dominating the market are SGS SA, ICON PLC, Laboratory Corporation of America Holdings, Syneos Health Inc., Charles River Laboratories Inc., etc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increased Necessity of Specific Types of Tests in R&D Activities

- 4.2.2 Increased Trend of Outsourcing Laboratory Testing Services

- 4.3 Market Restraints

- 4.3.1 Complex Regulatory Framework for Maintaining Laboratories

- 4.3.2 Challenges in the Development of Proper Analytical Techniques

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 By Molecule Type

- 5.1.1 Small Molecules

- 5.1.2 Large Molecules

- 5.2 By Test Type

- 5.2.1 Bioavailability and Bioequivalence Studies

- 5.2.2 Pharmacokinetics

- 5.2.3 Pharmacodynamics

- 5.2.4 Other Test Types

- 5.3 Geography

- 5.3.1 North America

- 5.3.1.1 US

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 UK

- 5.3.2.3 France

- 5.3.2.4 Italy

- 5.3.2.5 Spain

- 5.3.2.6 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 Japan

- 5.3.3.3 India

- 5.3.3.4 Australia

- 5.3.3.5 South Korea

- 5.3.3.6 Rest of Asia-Pacific

- 5.3.4 Middle-East and Africa

- 5.3.4.1 GCC

- 5.3.4.2 South Africa

- 5.3.4.3 Rest of Middle-East and Africa

- 5.3.5 South America

- 5.3.5.1 Brazil

- 5.3.5.2 Argentina

- 5.3.5.3 Rest of South America

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Pharmaceutical Product Development LLC

- 6.1.2 ICON PLC

- 6.1.3 Laboratory Corporation of America Holdings

- 6.1.4 Charles River Laboratories International Inc.

- 6.1.5 Syneos Health

- 6.1.6 SGS SA

- 6.1.7 Toxikon Corporation

- 6.1.8 Intertek Group PLC

- 6.1.9 Wuxi Apptec Co. Ltd