|

市場調査レポート

商品コード

1643149

ゲームにおけるバーチャルリアリティ(VR):市場シェア分析、産業動向と統計、成長予測(2025年~2030年)VR in Gaming - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| ゲームにおけるバーチャルリアリティ(VR):市場シェア分析、産業動向と統計、成長予測(2025年~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

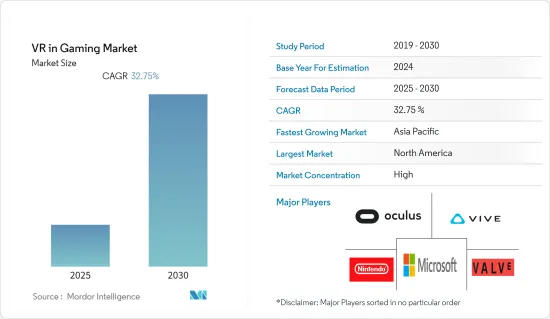

ゲームにおけるバーチャルリアリティ(VR)市場は、予測期間中にCAGR 32.75%を記録すると予想されます。

VRゲームでは、マウス、タッチスクリーン、その他のコンポーネントの助けを借りて、コンピューティングデバイス上のユーザーがゲーム設定の中で物理的な存在を感じることができる3D環境が含まれます。バーチャルリアリティヘッドセット、ラップアラウンドディスプレイスクリーン、ウェアラブルコンピュータを備えたバーチャルリアリティルーム、感覚コンポーネントなど、VR技術に関連するさまざまな付属品により、ゲーマーはゲーム設定内のオブジェクトと対話したり、見たり、移動したりすることができます。テクノロジー企業幹部、新興企業創業者、投資家、コンサルタントを対象とした世界規模の調査によると、回答者の59%が、VR技術開発への投資はゲームが主流になると考えています。

さらに、VRゲームはゲーム環境においてゲーマーにインタラクションやコミュニケーションを提供し、より多くの子供やゲーマーを惹きつけ、市場の成長を促進します。3Dinsiderによると、アクティブなVRユーザーの64%以上が、VR技術の進歩から恩恵を受ける可能性が最も高いのはゲームだと考えています。

同市場では、ゲームデザイナー、プロデューサー、プログラマー、アーティスト、ビジネス、営業、マーケティングなど、VRゲームに関連するさまざまな仕事が生まれています。

VRヘッドセットは、HTC ViveやPlayStation VRなど、ゲームに特化した用途のため、市場全体で人気を集めています。また、ソニー・インタラクティブエンタテインメントは昨年11月、プレイステーション5プラットフォーム向けの新しいバーチャルリアリティ(VR)システムであるプレイステーションVR2を発売すると発表しました。

COVID-19の発生により、ほとんどの国でロックダウンが実施され、人々はロックダウン中にVRゲームに時間を費やしていたため、VRゲームの市場は大幅な普及の増加を目の当たりにしました。

HTC Viveportのような多くのVRゲームプロバイダーは、複数の機能を備えたゲームを提供しています。例えば、Viveport Infinityの年間サブスクリプションは75%オフで、年間107.88米ドルから27米ドルになった。

昨年10月、メタ社は新しいVRヘッドセットの発売を発表しました。この製品は、アイトラッキングとフェイストラッキングによって実現される新機能を備えており、例えば「仮想現実でアイコンタクトを取る」ことができます。

ゲームにおけるバーチャルリアリティ(VR)の市場動向

プレミアムモバイルプラットフォームが市場成長に貢献

- モバイル・バーチャルリアリティ(VR)ゲームは、多額の費用をかけずにVRゲームを楽しみたい消費者にとって、最も手頃な体験です。また、携帯性と世界中のスマートフォンユーザーの膨大なインストールベースが、その普及につながっています。Plink社によると、世界には約22億人のモバイルゲーマーがいるといいます。

- モバイルゲーマーの増加に伴い、プレイヤーはモバイルベースのゲーマーにスムーズなVRゲーム体験を提供するために、ヘッドマウントディスプレイなどの様々なアクセサリーを提供しているため、モバイルVRゲーム市場は大きな牽引力を獲得すると予想されます。

- 携帯電話向けVRヘッドセットとして最も広く知られているのは、Samsung GearとGoogle Daydreamです。コンソールやPC用ヘッドセットと比べて低価格であること、モバイル用ヘッドセットは高級な携帯電話にバンドルされていることが多いことが、市場を牽引する重要な要因となっています。

- さらに、5G技術もモバイルベースのVRゲーム市場を牽引しています。例えば、HTCは昨年2月、同社の5G製品、Vive VRデバイス、関連取り組み、ENGAGEやVRChatなどのパートナーを含むメタバース環境であるViverseを発表しました。

- 現在、モバイルゲーム向けのVRは、コンソールやPCベースのVRに比べて没入感が劣るもの、モバイルVR環境における様々な技術的進歩により、予測期間中にその普及が進むと予想されます。また、スマートフォンの成長に伴い、予測期間中のVRゲーム市場には大きな可能性があります。

アジア太平洋地域が大きな成長を遂げる

- アジア太平洋地域は、インドや中国のような大規模かついくつかの新興経済国の存在と、同地域におけるバーチャルリアリティデバイスの受容の高まりにより、大きなシェアを占めると予想されます。このため、同地域の業界プレーヤーがVRゲームに投資することが期待されます。

- 同国におけるVR技術の採用が増加していることから、中国は同地域で突出したシェアを占めると予想されます。また、中国のVR市場は、政府の政策支援の増加や、同国における5Gなどの技術の展開により、拡大が見込まれています。業界規制当局によると、中国のバーチャルリアリティ(VR)市場は大幅に拡大すると予測されています。

- また、多くの地域プレーヤーが、よりリアルなゲーム内機能を備えた新しいゲームを開発し、市場を牽引しています。

- バーチュリープは、HTC Viveport Chinaチームとの提携により、Enhance VR脳トレアプリを中国で発売しました。Enhance VRは、記憶力、問題解決力、柔軟性、スピード、運動能力、空間的方向、空間的音声認識など、さまざまな認知能力を評価・訓練するために設計されたミニゲームを毎日トレーニングできます。

ゲームにおけるバーチャルリアリティ(VR)の概要

ゲームにおけるバーチャルリアリティ(VR)は、多くの大手プレイヤーの存在により、統合された市場となっています。市場は統合されており、主要企業は競合に打ち勝つために製品革新などの戦略を採用しています。同市場に参入しているプレーヤーには、Oculus VR(Facebook Technologies LLC)、HTC Vive、任天堂株式会社、マイクロソフト株式会社などがあります。

2022年1月、任天堂はSwitch OLEDモデルを中国本土で発売すると発表しました。Switch OLEDは2021年に国際的に発売され、今回は中国での発売を計画しています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の成果

- 調査の前提

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- VRフォーマットにおける魅力的でテーマ性の高いゲームの増加

- ミレニアル世代と高所得者層が中長期的な普及を牽引

- プレミアムモバイルプラットフォームが市場成長に貢献

- 市場抑制要因

- 視覚と聴覚に関する閾値|モバイルARゲームへの高い需要

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

- COVID-19がVRゲーム業界に与える影響

- VRゲームの人気テーマとトップパブリッシャーの分析(アーケード、アドベンチャー、ホラーなど)

- ARとVRベースのゲームの比較研究

第5章 市場セグメンテーション

- VRタイプ別

- PC

- スタンドアロン

- コンソール

- カートリッジ

- プレミアムモバイル

- ゲームでのVR別

- ハードウェア

- ソフトウェア

- 地域別

- 北米

- 欧州

- アジア太平洋

- 世界のその他の地域

第6章 競合情勢

- 企業プロファイル

- Oculus VR(Facebook Technologies LLC)

- HTC Vive

- Valve Corporation

- Intel Corporation

- Virtuix Omni

- Nintendo Co. Limited

- Microsoft Corporation

- Samsung Corporation

- Google LLC

- *List not exhaustive

第7章 投資分析

第8章 市場の将来

The VR in Gaming Market is expected to register a CAGR of 32.75% during the forecast period.

VR gaming involves a 3D environment that enables the user on a computing device, with the help of a mouse, touch screen, and other components, to feel the physical presence in the game settings. The various accessories associated with VR technology, such as virtual reality headsets, wrap-around display screens, virtual reality rooms equipped with wearable computers, and sensory components, enable gamers to interact, view and move around the objects in the game setting. According to a worldwide survey of technology company executives, startup founders, investors, and consultants, 59% of respondents believe gaming will dominate the investment in VR technology development.

Moreover, VR gaming provides interaction and communication to gamers in the game environment, attracting more children's and gamers, thus driving the market's growth. According to 3Dinsider, more than 64% of active VR users believe that gaming has the highest potential to benefit from advances in VR technology.

The market is creating various jobs related to VR gaming, such as game designers, producers, programmers, artists, business, sales, and marketing roles.

VR headset is gaining traction across the market due to their specific application for games, such as HTC Vive and PlayStation VR. Also, in November last year, Sony Interactive Entertainment announced that PlayStation VR2, a new virtual reality (VR) system for the PlayStation 5 platform, would be released.

With the outbreak of COVID-19, the market for VR gaming witnessed a significant increase in adoption as most countries enforced lockdowns, and people were spending their time on VR gaming during the lockdown.

Many VR gaming providers, such as HTC Viveport, provide games with multiple features. For instance, Viveport Infinity's annual subscription had a 75% off, taking it down from USD 107.88 per year to USD 27.

In October last year, Meta confirmed the launch of a new VR headset. This product would have new capabilities enabled by eye tracking and face tracking, like the capacity to make 'eye contact in virtual reality.'

Virtual Reality in Gaming Market Trends

Premium Mobile Platform Contributing to the Growth of Market

- Mobile virtual reality (VR) gaming is the most affordable experience for consumers who want to explore VR gaming without spending a substantial amount of money. Also, the portability and massive install base of smartphone users across the world are leading to its widespread adoption. According to Plink, there are about 2.2 billion mobile gamers worldwide.

- With the increasing number of mobile gamers, the mobile VR gaming market is expected to gain significant traction as players offer various accessories, such as a head-mounted display, for a smooth VR gaming experience for mobile-based gamers.

- The most widely known VR headsets for mobile phones are Samsung Gear and Google Daydream. The lower price compared to console and PC headsets and mobile headsets are often bundled with premium phones are vital factors driving the market.

- Moreover, 5G technologies are also driving the mobile-based VR gaming market. For instance, in February last year, HTC announced Viverse, a metaverse environment that includes its 5G products, Vive VR devices, associated efforts, and partners such as ENGAGE and VRChat.

- While VR for mobile gaming currently provides a less immersive experience than console and PC-based VR, its adoption is expected to increase during the forecast period due to a range of technological advancements in the mobile VR environment. Also, with the growth of smartphones, there is massive potential for the VR gaming market during the forecast period.

Asia-Pacific Region to Witness Significant Growth

- Asia-Pacific is expected to hold a significant share owing to the presence of large and several emerging economies, such as India and China, along with the rising acceptance of virtual reality devices in the region. This is, in turn, expected to encourage industry players to invest in VR gaming in the region.

- Due to the rising adoption of VR technology in the country, China is expected to account for a prominent share of the region. Also, the Chinese market for VR is expected to increase due to increased government policy support and the rolling out of technologies, such as 5G, in the country. According to the industry regulator, China's virtual reality (VR) market is forecast to expand significantly.

- Also, many regional players are building new games with more realistic in-game features that drive the market.

- Virtuleap launched the Enhance VR brain training app in China in partnership with the HTC Viveport China team. Enhance VR offers a daily workout of mini-games designed to assess and train different cognitive skills such as memory, problem-solving, flexibility, speed, motor skills, spatial orientation, and spatial audio awareness.

Virtual Reality in Gaming Industry Overview

Virtual reality in gaming is a consolidated market, owing to the presence of many large players. The market is consolidated with the key players adopting strategies, such as product innovation, to stay ahead of the competition. Some of the players in the market are Oculus VR (Facebook Technologies LLC), HTC Vive, Nintendo Co Limited, and Microsoft Corporation.

In January 2022, Nintendo announced that the company would release its Switch OLED model in mainland China. The Switch OLED launched internationally in 2021, and now the company plans to launch it in China.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Deliverables

- 1.2 Study Assumptions

- 1.3 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Availability of Compelling and Theme-based Games in the VR Format

- 4.2.2 Millennial and High-income Groups to Drive Adoption in the Near and Medium-term

- 4.2.3 Premium Mobile Platform Contributing to the Growth of Market

- 4.3 Market Restraints

- 4.3.1 Threshold Related to Visual and Auditory Aspects | High Demand for Mobile AR Gaming

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

- 4.5 Impact of COVID-19 on the VR Gaming industry

- 4.6 Analysis on the Popular Themes in VR Gaming and Top Publishers (Arcade, Adventure, Horror, etc.)

- 4.7 Comparative Study of AR and VR-based Gaming

5 MARKET SEGMENTATION

- 5.1 By VR Type

- 5.1.1 PC

- 5.1.2 Stand-alone

- 5.1.3 Console

- 5.1.4 Cartridges

- 5.1.5 Premium Mobile

- 5.2 By VR in Gaming

- 5.2.1 Hardware

- 5.2.2 Software

- 5.3 Geography

- 5.3.1 North America

- 5.3.2 Europe

- 5.3.3 Asia-Pacific

- 5.3.4 Rest of The World

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Oculus VR (Facebook Technologies LLC)

- 6.1.2 HTC Vive

- 6.1.3 Valve Corporation

- 6.1.4 Intel Corporation

- 6.1.5 Virtuix Omni

- 6.1.6 Nintendo Co. Limited

- 6.1.7 Microsoft Corporation

- 6.1.8 Samsung Corporation

- 6.1.9 Google LLC

- 6.1.10 *List not exhaustive