|

市場調査レポート

商品コード

1687329

ガス絶縁開閉装置:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)Gas-insulated Switchgear - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| ガス絶縁開閉装置:市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 185 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

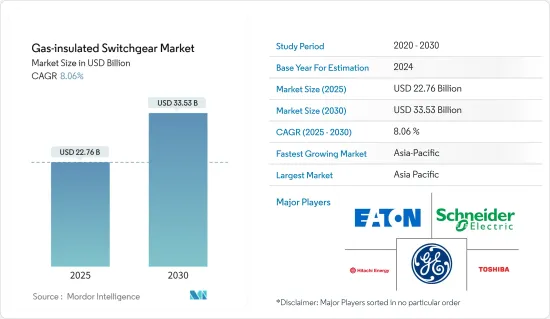

ガス絶縁開閉装置の市場規模は2025年に227億6,000万米ドルと推定され、予測期間(2025-2030年)のCAGRは8.06%で、2030年には335億3,000万米ドルに達すると予測されます。

COVID-19の発生は、世界経済の減速につながる一連のロックダウンを引き起こし、その結果、裁量支出の減少による産業・商業活動の鈍化を招き、ガス絶縁開閉装置(GIS)市場の足かせとなりました。市場の成長に関しては、トランスミッションや配電網の改善といった電力業界の変革、再生可能エネルギーベースの発電所の採用増加などの要因が、予測期間中に市場を牽引すると予想されます。しかし、GISに関連する厳しい環境・安全規制とともに、空気絶縁開閉装置と比較すると設備コストが高いことが、予測期間中の市場成長を抑制する可能性が高いです。

主なハイライト

- ユーティリティ分野での用途が多いことから、高電圧レベルセグメントが予測期間中市場を独占すると予想されます。

- スマートグリッドとエネルギーシステムへの市場開拓と、先進地域における変電所の古い開閉装置の拡張や交換は、GIS市場に豊富なビジネスチャンスをもたらすと予想されます。

- アジア太平洋地域が市場を独占すると予想され、需要の大部分はインドや中国などの国々からもたらされます。

ガス絶縁開閉装置の市場動向

高電圧レベルが市場を独占する見込み

- 36kV以上の電圧を扱う電力システムは高圧スイッチギアと呼ばれます。電圧レベルが高いため、スイッチング動作中に発生するアーク放電も非常に大きくなります。そのため、高圧開閉器の設計には特別な注意が必要です。高圧サーキットブレーカは高圧開閉装置の主要部品であるため、高圧サーキットブレーカ(CB)には安全で信頼性の高い動作のための特別な機能が必要です。

- これらの開閉装置は、風力タービン、電気モーター、発電機、太陽光発電、住宅配電、電力供給システム、環境に配慮した設置、地下駅、鉄鋼、製紙、鉱業、海洋アプリケーションの増加など、さまざまな産業で複数の用途があります。しかし、このセグメントの主な用途は、近代化されつつある大規模なトランスミッションと配電ネットワークであり、特にアジア太平洋地域の国々で高い割合で世界中に建設されています。

- しかし、この分野はダウンタイムやメンテナンスの問題に悩まされてきました。このため、2022年5月にACTOM High Voltage(HVE)などの企業が、技術パートナーと共同で、状態ベースのメンテナンス戦略で顧客を支援する資産パフォーマンス管理ソリューションを開発しています。業界におけるこうした試みは、特に同業他社と比較した場合、より実現可能な選択肢を市場に提供することで、市場の成長を助けると期待されています。

- また、アラブ首長国連邦で2021年12月に予定されている直流海底送電システムのような大型プロジェクトにより、アブダビ国営石油会社の海上生産活動に、よりクリーンで効率的なエネルギーを供給することが期待されており、同国の送配電会社が所有・運営するアブダビ陸上送電網を通じて供給されます。

- さらに、2021年の大きな開発として、シーメンス・エナジーと三菱電機は、地球温暖化係数(GWP)ゼロの高圧スイッチング・ソリューションの共同開発に関する実現可能性調査を実施する覚書に調印しました。この研究では、温室効果ガスをクリーンな空気で代替する絶縁に取り組む予定です。両社は、クリーンエア絶縁技術の高電圧への適用を拡大するための方法を研究する予定です。しかし、両パートナーは、スイッチギア・ソリューションの製造、販売、サービスを独自に継続し、技術移転のみが行われる見込みです。

- したがって、予測期間中は高圧スイッチギアが市場を独占すると予想されます。

アジア太平洋地域が市場を独占する

- アジア太平洋地域は人口が最も多い地域のひとつであり、工業化と都市化の急速な進展により、電力需要は過去数年間で大幅に急増しました。そのため、送配電(T&D)インフラへの投資も大幅に増加しました。さらに、長距離送配電プロジェクトは、ガス絶縁開閉装置がますます適している地下ネットワークと小型変電所の開発によって、より環境に優しくなっています。

- この地域はまた、中国とインドに牽引され、再生可能エネルギーの導入において最も急成長している市場でもあります。再生可能エネルギー発電の急速な増加に伴い、送電網に再生可能エネルギーが高水準で統合されている国々では、送電網の安定性が重要な問題となっており、旧式の送電・配電インフラの近代化も必要とされています。太陽光や風力などの再生可能エネルギー発電は出力が変動するため、従来の送配電システムは再生可能エネルギーの送配電に適していない可能性があり、アップグレードや改修が必要となります。

- さらに、太陽光発電所や風力発電所など、ほとんどのユーティリティ・スケールの再生可能エネルギー発電施設は、人口集中地区から離れた場所にあります。したがって、発電した電力を使用するためには、大規模な送電プロジェクトを通じて需要センターに接続する必要があります。こうしたプロジェクトは、予測期間中にガス絶縁開閉装置(GIS)に対する大規模な需要を生み出すと予想されます。

- 中国最大の国有電力会社である中国国家電網公司(SGCC)によると、2030年の同国のエネルギー需要は10ペタワット時(PWH)を超えると予想されています。その結果、既存の送電網の拡張が必要となり、同国におけるガス絶縁高圧開閉器の需要が高まると予想されます。

- 2022年1月、インド政府、西ベンガル州政府、世界銀行は、西ベンガル州の特定地域における電力供給の効率と信頼性を改善するため、1億3,500万米ドル相当のプロジェクトに署名しました。このプロジェクトでは、電力網の近代化において、他の機器とともにGISが採用されます。

- 電力需要の増加に伴い、新興国の大半は国内の電力需要を満たすことができなくなっています。そのため、この地域では新しい発電所の建設が進められています。

- また、この地域では再生可能エネルギー発電の導入が急速に進んでおり、このような発電所を統合するために独自のトランスミッションや配電ネットワーク、既存の送電網インフラの刷新が必要となっています。

- したがって、この動向は予測期間中も続くと予想され、ひいてはこの地域のガス絶縁開閉装置市場を牽引すると期待されます。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 イントロダクション

- 調査範囲

- 市場の定義

- 調査の前提

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場概要

- イントロダクション

- 2027年までの市場規模および需要予測

- 最近の動向と開発

- 政府の規制と政策

- 市場力学

- 促進要因

- 抑制要因

- サプライチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- 電圧レベル

- 低電圧

- 中電圧

- 高電圧

- エンドユーザー

- 電力会社

- 産業部門

- 商業および住宅

- 地域

- 北米

- アジア太平洋

- 欧州

- 南米

- 中東・アフリカ

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 主要企業の戦略

- 企業プロファイル

- Hitachi Energy Ltd

- Schneider Electric SE

- General Electric Company

- Powell Industries Inc.

- Eaton Corporation PLC

- Toshiba Corp.

- Mitsubishi Electric Corporation

- Siemens Energy AG

- Hyosung Heavy Industries Corp.

- Bharat Heavy Electricals Limited

第7章 市場機会と今後の動向

The Gas-insulated Switchgear Market size is estimated at USD 22.76 billion in 2025, and is expected to reach USD 33.53 billion by 2030, at a CAGR of 8.06% during the forecast period (2025-2030).

The outbreak of the COVID-19 led to a series of lockdowns leading to the global economic slowdown, which, in turn, led to a slowdown in industrial and commercial activities due to less discretionary spending, hampering the gas-insulated switchgear(GIS) market. In terms of the growth of the market, factors such as the transformation of the power industry in terms of upgrading transmission and distribution networks, rising adoption of renewable energy-based power plants, etc., are expected to drive the market during the forecast period. However, high equipment cost when compared to air-insulated switchgear, along with stringent environmental and safety regulations related to GIS, is likely to restrain the market growth during the forecast period.

Key Highlights

- The high voltage level segment due to most applications being in utility sectors, is anticipated to dominate the market during forecast period.

- Growing investments in smart grids and energy systems and the extension or replacement of old switchgear at substations in developed regions are expected to create ample opportunities in the GIS market soon.

- Asia-Pacific is expected to dominate the market, with the majority of the demand coming from the countries such as India and China.

Gas Insulated Switchgear Market Trends

High Voltage Level Segment Expected to Dominate the Market

- The power system that deals with voltage above 36kV is referred as high voltage switchgear. As the voltage level is high the arcing produced during switching operation is also very high. So, special care is to be taken during the designing of high voltage switchgear. High voltage circuit breaker, is the main component of HV switchgear, hence high voltage circuit breaker (CB) should have special features for safe and reliable operation.

- These switchgear have multiple usages across varied industries such as wind turbines, electrical motors, generators, solar power generation, residential power distribution, power supply systems, environmentally sensitive installation, underground stations, steel, paper, and mining industry, and growing number of marine applications. But the main application of the segment comes from large transmission and distribution networks being modernized and being built across the globe with especially high rates countries in the Asia-Pacific region.

- However, the segment has been plagued with downtime and maintenance issues. For this companies such as ACTOM High Voltage (HVE), in May 2022, in conjunction with its technology partners are developing asset performance management solutions to help customers with condition-based maintenance strategies. Such endeavors in the industry are expected to aid the growth of the market by providing a more feasible alternative to the market especially when compared to its peers.

- Also, the growing HVDC market is expected to aid the growth of the market with large projects, in December 2021, in the United Arab Emirates, such as the anticipated direct current subsea transmission system, which is expected to power Abu Dhabi National Oil Company's offshore production operations with cleaner and more efficient energy, delivered through the Abu Dhabi onshore power grid, owned and operated by the country's transmission and distribution companies.

- Further, in a major development in 2021, Siemens Energy and Mitsubishi Electric signed a Memorandum of Understanding to conduct a feasibility study on the joint development of high-voltage switching solutions with the prospect of zero global-warming potential (GWP). The study is expected to work on the substitution of greenhouse gases with clean air for insulation. Both companies are expected to research methods for scaling up the application of clean-air insulation technology to higher voltages. However, both partners are expected to continue to manufacture, sell, and service switchgear solutions independently and only the transfer of technology is expected to take.

- Hence, high-voltage switchgear are expected to dominate the market during the forecast period.

Asia-Pacific to Dominate the Market

- The Asia-Pacific region is one of the most populated regions, and due to rapid growth in industrialization and urbanization, power demand surged substantially over the past few years. Thus, investments in transmission and distribution (T&D) infrastructure also grew significantly. Additionally, long-distance T&D projects become more eco-friendly by developing underground networks and smaller substations, for which gas-insulated switch gears are increasingly suitable.

- The region is also the fastest-growing market in renewable energy deployment, led by China and India. With the rapid rise in renewable power generation, grid stability is a significant issue in countries with high levels of renewable integration in their grids, which also needs the modernization of older T&D infrastructure. As renewable power generated from sources, such as solar and wind, provide variable power output, traditional T&D systems may not be suitable for renewable energy transmission and distribution and would require upgradation or retrofitting.

- Additionally, most utility-scale renewable energy generation facilities, such as solar and wind farms, are situated far from population centers. Hence, they need to be connected to demand centers via large-scale transmission projects to use the power generated. Such projects are expected to create a massive demand for gas-insulated switchgear (GIS) over the forecast period.

- According to China's largest state-owned utility corporation, State Grid Corporation of China (SGCC), the country's energy demand in 2030, is expected to exceed 10 Petawatt hours (PWH). As a result, there is a need for the expansion of the existing power transmission network, which is expected to drive the demand for gas-insulated high voltage switchgear in the country.

- In January 2022, the Indian government, the West Bengal government along with the World Bank signed a project worth USD 135 million to improve the efficiency and reliability of electricity supply in selected areas of West Bengal. This project will see the adoption of GIS along with other equipment in the modernization of the electricity grid.

- As the demand for power increases, a majority of the emerging countries are unable to fulfill the domestic electricity demand. Therefore, new power plants are being built in this region.

- The region is also seeing rapid adoption of renewable energy-based power generation, which requires a transmission and distribution network of its own and revamping of existing grid infrastructure to integrate such power plants, which, in turn, is driving the demand for gas-insulated switchgear.

- Therefore, the trend is expected to continue during the forecast period as well, which, in turn, is expected to drive the gas-insulated switchgear market in the region.

Gas Insulated Switchgear Industry Overview

The gas-insulated switchgear market is moderately fragmented. Some of the key companies in the market include Hitachi Energy Ltd, Schneider Electric SE, General Electric Company, Eaton Corporation PLC, and Toshiba Corp.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD billion, till 2027

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.2 Restraints

- 4.6 Supply Chain Analysis

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes Products and Services

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Voltage Level

- 5.1.1 Low Voltage

- 5.1.2 Medium Voltage

- 5.1.3 High Voltage

- 5.2 End User

- 5.2.1 Power Utilities

- 5.2.2 Industrial Sector

- 5.2.3 Commercial and Residential

- 5.3 Geography

- 5.3.1 North America

- 5.3.2 Asia-Pacific

- 5.3.3 Europe

- 5.3.4 South America

- 5.3.5 Middle-East and Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 Hitachi Energy Ltd

- 6.3.2 Schneider Electric SE

- 6.3.3 General Electric Company

- 6.3.4 Powell Industries Inc.

- 6.3.5 Eaton Corporation PLC

- 6.3.6 Toshiba Corp.

- 6.3.7 Mitsubishi Electric Corporation

- 6.3.8 Siemens Energy AG

- 6.3.9 Hyosung Heavy Industries Corp.

- 6.3.10 Bharat Heavy Electricals Limited