|

市場調査レポート

商品コード

1716464

ガス絶縁開閉装置市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測Gas Insulated Switchgear Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| ガス絶縁開閉装置市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測 |

|

出版日: 2025年03月03日

発行: Global Market Insights Inc.

ページ情報: 英文 135 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

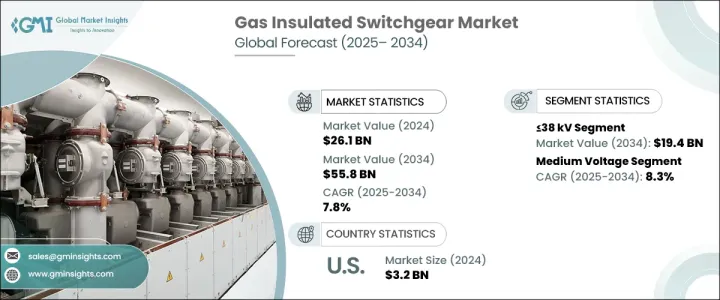

ガス絶縁開閉装置の世界市場は2024年に261億米ドルに達し、2025年から2034年にかけてCAGR 7.8%で成長すると予測されています。

世界の電力需要の増加、急速な都市化、送配電網の継続的な拡大が市場成長の原動力となっています。各国が電力インフラのアップグレードを進める中、GIS技術は産業、商業、公益セクターでますます採用されるようになっています。スペース効率、信頼性、低メンテナンスコストという点で優れた性能を持つGISは、従来の空気絶縁開閉装置(AIS)よりも優位に立っています。GISは高い耐久性と中断のない性能を提供するため、密集した都市環境、大規模な産業施設、極端な気象条件の地域の電力システムを管理するために不可欠になっています。

同市場では、電力網を近代化し、エネルギー効率を確保するために、政府と民間企業の両方からの投資が増加しています。エネルギー転換が勢いを増すにつれ、既存の送電網に再生可能エネルギー源を統合することが優先事項となっています。GISはこの移行を促進する上で極めて重要な役割を果たしており、持続可能性の目標に沿ったコンパクトで高性能なソリューションを提供しています。さらに、絶縁技術やデジタル監視機能の進歩により、GISの効率は向上しており、次世代電力インフラとして好ましい選択肢となっています。スマートグリッド・ソリューションとインテリジェント配電システムに対する需要は、特に送電ロスの削減と送電網の安定性向上に重点を置く地域でのGIS展開をさらに加速させています。環境の持続可能性に対する懸念が高まる中、多くの市場関係者はGISシステムの二酸化炭素排出量を最小限に抑えるため、環境に優しい代替ガスを模索しています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 261億米ドル |

| 予測金額 | 558億米ドル |

| CAGR | 7.8% |

高電圧部門は依然として市場を独占しており、定格150kV以上のGISシステムが大きなシェアを占めています。これらの大容量スイッチギア・ソリューションは、安定的かつ効率的な配電を確保するため、発電所、重工業、大規模ユーティリティ・プロジェクトに広く導入されています。コンパクトな設計で、リスクの高い環境でも確実に機能するため、スペースが限られ、運用効率が最優先される用途に最適です。石油・ガス、鉱業、運輸などの業界では、電力管理システムを最適化すると同時に、厳しい安全性と性能要件を満たすためにGIS技術を統合するケースが増えています。

中電圧GIS分野は、2034年までのCAGRが8.3%と予想され、大きな成長が見込まれています。スマートシティの台頭とともに都市インフラの急速な拡大が、効率的で信頼性の高い配電ソリューションの需要を促進しています。商業および住宅部門における近代化の取り組みは、再生可能エネルギー統合への関心の高まりと相まって、中電圧GISの採用に拍車をかけています。持続可能性と自動化を優先する産業は、業務効率を高め停電を最小限に抑えるためにGIS技術にシフトしています。

北米のガス絶縁開閉装置市場は2024年に32億米ドルを生み出し、米国が送電のアップグレード投資を主導しています。同国では電力需要の増加に対応するため、老朽化した送電網インフラを近代化しており、GISは次世代配電システムをサポートする上で重要な役割を果たしています。スマートグリッドや高度な電力管理ソリューションが重視されるようになり、GISの導入はさらに進んでいます。再生可能エネルギーとデジタル化された送電網への投資が増加する中、GISは北米の電力セクター変革の礎となると思われます。

目次

第1章 調査手法と調査範囲

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- 規制状況

- 業界への影響要因

- 促進要因

- 業界の潜在的リスク&課題

- 成長ポテンシャル分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- 戦略ダッシュボード

- イノベーションと持続可能性の展望

第5章 市場規模・予測:容量別、2021年~2034年

- 主要動向

- 38 kV以下

- 38 kV~72 kV未満

- 72 kV~150 kV未満

- 150 kV超

第6章 市場規模と予測:電圧レベル別、2021年~2034年

- 主要動向

- 中電圧

- 一次配電

- 二次配電

- 高電圧

第7章 市場規模・予測:用途別、2021年~2034年

- 主要動向

- 送電・配電

- 製造・加工

- インフラ・輸送

- 発電

- その他

第8章 市場規模・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- 英国

- フランス

- ドイツ

- イタリア

- ロシア

- スペイン

- アジア太平洋

- 中国

- オーストラリア

- インド

- 日本

- 韓国

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- トルコ

- 南アフリカ

- エジプト

- ラテンアメリカ

- ブラジル

- アルゼンチン

第9章 企業プロファイル

- ABB

- Bharat Heavy Electricals

- CHINT Group

- CG Power and Industrial Solutions

- Eaton

- Fuji Electric

- General Electric

- HD Hyundai Electric

- Hitachi

- Hyosung Heavy Industries

- Lucy Group

- Mitsubishi Electric

- Ormazabal

- Schneider Electric

- Siemens

- Skema

- Toshiba

The Global Gas Insulated Switchgear Market reached USD 26.1 billion in 2024 and is projected to grow at a CAGR of 7.8% between 2025 and 2034. The rising global demand for electricity, rapid urbanization, and the continuous expansion of power transmission and distribution networks are fueling market growth. As countries move toward upgrading their power infrastructure, GIS technology is increasingly being adopted across industrial, commercial, and utility sectors. Its superior performance in terms of space efficiency, reliability, and low maintenance costs gives it an edge over traditional air-insulated switchgear (AIS). GIS is becoming essential for managing power systems in dense urban environments, large-scale industrial setups, and regions with extreme weather conditions, as it offers high durability and uninterrupted performance.

The market is witnessing increased investments from both government and private players to modernize power grids and ensure energy efficiency. As the energy transition gains momentum, integrating renewable sources into existing grids is becoming a priority. GIS plays a pivotal role in facilitating this shift, providing compact and high-performance solutions that align with sustainability goals. Additionally, advancements in insulation technologies and digital monitoring capabilities are enhancing GIS efficiency, making it a preferred choice for next-generation power infrastructure. The demand for smart grid solutions and intelligent power distribution systems is further accelerating GIS deployment, particularly in regions focusing on reducing transmission losses and improving grid stability. With rising concerns over environmental sustainability, many market players are also exploring eco-friendly gas alternatives to minimize the carbon footprint of GIS systems.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $26.1 Billion |

| Forecast Value | $55.8 Billion |

| CAGR | 7.8% |

The high-voltage segment remains the dominant force in the market, with GIS systems rated above 150 kV holding a substantial share. These high-capacity switchgear solutions are widely deployed in power plants, heavy manufacturing industries, and large-scale utility projects to ensure stable and efficient electricity distribution. Their compact designs and ability to function reliably in high-risk environments make them ideal for applications where space is limited and operational efficiency is paramount. Industries such as oil and gas, mining, and transportation are increasingly integrating GIS technology to meet stringent safety and performance requirements while optimizing power management systems.

The medium-voltage GIS segment is projected to experience significant growth, with an expected CAGR of 8.3% through 2034. The rapid expansion of urban infrastructure, alongside the rise of smart cities, is driving the demand for efficient and reliable power distribution solutions. Modernization initiatives in commercial and residential sectors, coupled with the growing focus on renewable energy integration, are fueling the adoption of medium-voltage GIS. Industries prioritizing sustainability and automation are shifting toward GIS technology to enhance operational efficiency and minimize power outages.

North America Gas Insulated Switchgear Market generated USD 3.2 billion in 2024, with the United States leading investments in power transmission upgrades. As the country modernizes its aging grid infrastructure to meet increasing electricity demand, GIS is playing a crucial role in supporting next-generation power distribution systems. The growing emphasis on smart grids and advanced power management solutions is further strengthening GIS adoption. With investments in renewable energy and digitalized grid networks on the rise, GIS is set to become a cornerstone of North America's power sector transformation.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid

- 1.4.2.2 Public

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

Chapter 4 Competitive landscape, 2024

- 4.1 Strategic dashboard

- 4.2 Innovation & sustainability landscape

Chapter 5 Market Size and Forecast, By Capacity, 2021 – 2034 (USD Million, ‘000 Units)

- 5.1 Key trends

- 5.2 ≤ 38 kV

- 5.3 > 38 kV to ≤ 72 kV

- 5.4 > 72 kV to ≤ 150 kV

- 5.5 > 150 kV

Chapter 6 Market Size and Forecast, By Voltage Level 2021 – 2034 (USD Million, ‘000 Units)

- 6.1 Key trends

- 6.2 Medium voltage

- 6.2.1 Primary distribution

- 6.2.2 Secondary distribution

- 6.3 High voltage

Chapter 7 Market Size and Forecast, By Application 2021 – 2034 (USD Million, ‘000 Units)

- 7.1 Key trends

- 7.2 Transmission & distribution

- 7.3 Manufacturing & processing

- 7.4 Infrastructure & transportation

- 7.5 Power generation

- 7.6 Others

Chapter 8 Market Size and Forecast, By Region, 2021 – 2034 (USD Million, ‘000 Units)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.2.3 Mexico

- 8.3 Europe

- 8.3.1 UK

- 8.3.2 France

- 8.3.3 Germany

- 8.3.4 Italy

- 8.3.5 Russia

- 8.3.6 Spain

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Australia

- 8.4.3 India

- 8.4.4 Japan

- 8.4.5 South Korea

- 8.5 Middle East & Africa

- 8.5.1 Saudi Arabia

- 8.5.2 UAE

- 8.5.3 Turkey

- 8.5.4 South Africa

- 8.5.5 Egypt

- 8.6 Latin America

- 8.6.1 Brazil

- 8.6.2 Argentina

Chapter 9 Company Profiles

- 9.1 ABB

- 9.2 Bharat Heavy Electricals

- 9.3 CHINT Group

- 9.4 CG Power and Industrial Solutions

- 9.5 Eaton

- 9.6 Fuji Electric

- 9.7 General Electric

- 9.8 HD Hyundai Electric

- 9.9 Hitachi

- 9.10 Hyosung Heavy Industries

- 9.11 Lucy Group

- 9.12 Mitsubishi Electric

- 9.13 Ormazabal

- 9.14 Schneider Electric

- 9.15 Siemens

- 9.16 Skema

- 9.17 Toshiba