|

市場調査レポート

商品コード

1910637

食品包装:市場シェア分析、業界動向と統計、成長予測(2026年~2031年)Food Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 食品包装:市場シェア分析、業界動向と統計、成長予測(2026年~2031年) |

|

出版日: 2026年01月12日

発行: Mordor Intelligence

ページ情報: 英文 102 Pages

納期: 2~3営業日

|

概要

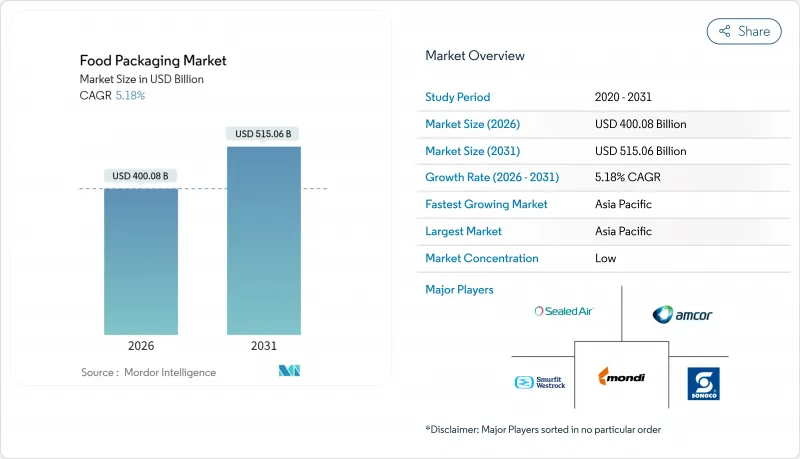

2026年の食品包装市場規模は4,000億8,000万米ドルと推定され、2025年の3,803億8,000万米ドルから成長し、2031年には5,150億6,000万米ドルに達すると予測されています。

2026年から2031年にかけての年間平均成長率(CAGR)は5.18%となる見込みです。

この拡大は、アジア太平洋地域における急速な都市化、北米および欧州全域での再生素材含有率に対する規制強化、そして世界のブランドオーナーによる材料効率の高い柔軟な包装形態への着実な移行に支えられています。また、冷蔵・冷凍食品の小売流通網を拡大するコールドチェーンインフラへの投資もメーカーにとって追い風となっています。一方、プレミアム化の流れはガラス需要を活性化させ、クリーンラベル表示を可能にする高バリア技術の導入を促進しています。供給面では、直接顧客関係が依然として主要な販路ですが、電子商取引物流専門企業は中小食品加工業者向け間接チャネルの拡大を加速させています。主要コンバーター間の合併活動は、研究開発、リサイクル資産、世界の流通網を統合することで競合環境を再構築しています。

世界の食品包装市場の動向と洞察

アジア全域における都市型コンビニエンスストアの急成長が、単品包装の需要を牽引

中国、インド、東南アジアにおける都市部への急速な人口移動により、買い物サイクルが短縮され、分量管理された食品包装への需要が高まっています。コンビニエンスストアは冷蔵スペースが限られる都心部の密集地域にまで進出しており、鮮度を保ち食品廃棄を抑制できる軽量な単品包装を提供するブランドが評価されています。若年層の働く消費者も携帯性を重視するため、加工メーカーは従来品目を再封可能なパウチやサーモフォームカップに再設計し、プレミアム価格帯での販売を図っています。移動中での消費形態への需要の高まりは、食品包装市場がバリア性を強化したフレキシブル包装や、保存期間目標を満たす薄肉硬質プラスチックへ移行する流れを後押ししています。2024年以降、コンパクトな充填ラインへの投資は1ユニットあたり最大18%減少しており、地域の共同包装業者にとって参入障壁が低下し、包装形態の多様化が加速しています。

北米食品包装における使用済み再生材含有率の法的推進

カリフォルニア州のSB54やメイン州のリサイクル素材使用義務化など州レベルの規制により、食品グレードのPCR供給が逼迫し、需要ピーク時にはバージンPET比15~20%の樹脂プレミアムが発生しています。このためブランドオーナーは、原料確保を確実にするため、リサイクル業者と複数年にわたる引き取り契約を締結し、選別能力への共同投資を進めています。機器サプライヤーによれば、透明性を損なわずに高比率のPCRを処理可能な押出・濾過システムの受注が26%増加しています。また、この法規制は再生材含有率を強調するラベルデザイン変更を促進しており、再生プラスチックの使用をブランドの社会的責任と結びつける消費者の意識の高まりに呼応しています。ガラス1トンあたり192米ドルからプラスチック1トンあたり423米ドルに及ぶEPR(拡大生産者責任)費用は、長期コストモデルに組み込まれつつあり、家庭ごみ回収に対応した単一素材のフレキシブルラミネートの採用を加速させています。

EU使い捨てプラスチック指令が複合柔軟構造のコンプライアンスコストを増加

欧州包装廃棄物規制により、2028年以降に販売される全消費者向け包装は実証可能なリサイクル性を達成することが義務付けられ、PET-PEやPA-PEラミネートに依存する加工業者には多額の設計変更費用が発生します。単一素材のポリプロピレンやポリエチレン構造への移行では、バリアコーティングの改良や既存シール装置との適合性試験により、原材料コストが最大14%上昇します。分別施設においても、新たなラミネートを識別可能な近赤外線センサーの導入が必須となりますが、小規模自治体ではこの投資の正当化が困難です。再設計コストを世界の生産量で償却できないメーカーは、より豊富な研究開発パイプラインを有する大手競合他社にEU市場での販売機会を奪われるリスクに直面しています。

セグメント分析

プラスチックは汎用性とコスト優位性により、2025年に食品包装市場シェアの58.55%を占め、最大の収益源となりました。価値ベースでは、バイオ循環型ポリプロピレンと化学的再生PETが商業規模で導入される2026年以降、プラスチック食品包装市場規模はCAGR4.92%で拡大すると予測されます。ガラスは基盤規模こそ小さいもの、無限にリサイクル可能という主張を活かす高級飲料やソースの需要に牽引され、年間7.12%の成長が見込まれます。

板紙の成長は電子商取引と段ボール輸送需要に連動し、金属は軽量化技術により缶詰食品分野でニッチな役割を維持します。全素材において、リサイクル性に関する規制優遇措置とデポジット返還制度の普及がブランド選択に影響を与えています。素材置換の決定ではコストに加えカーボンフットプリントが重視され、地域固有のリサイクルシステムに対応した単一素材構造への移行が加工業者に促されています。

フレキシブル包装ソリューションは2025年に市場全体の56.10%を占め、2031年までCAGR6.18%で拡大が見込まれます。スタンドアップパウチ、フローラップ、ピローバッグは、同等の硬質包装と比較して最大70%の輸送重量削減を実現し、小売業者の持続可能性目標達成を支援します。その結果、予測期間内にフレキシブル包装形式の食品包装市場規模は3,072億米ドルに達すると見込まれます。

製品の完全性や改ざん防止が最優先される分野では、硬質プラスチック、ガラス瓶、金属缶が依然として不可欠です。コンバーター各社は、後工程を必要としない360度グラフィックを実現するインモールドラベル技術を導入することで、硬質容器の有用性を拡大しています。今後の形態選択は、機械的リサイクル可能性、インフラ整備状況、ブランド固有のストーリーテリング目標を軸に進むでしょう。

食品包装市場レポートは、素材タイプ(プラスチック、紙、金属、ガラス)、形態(硬質、軟質)、製品タイプ(缶、ボトル等)、技術(MAP、真空、ホットフィル等)、流通経路(直接、間接)、用途(乳製品、肉類、農産物、ベーカリー製品、魚介類、レトルト食品、冷凍食品)、地域(北米、欧州、アジア太平洋、中東・アフリカ、南米)別に分析しております。市場予測は金額ベース(米ドル)で提示されます。

地域別分析

アジア太平洋地域は2025年に世界収益の40.85%を占め、所得の増加、コールドチェーンの拡大、組織化された小売業の急成長に後押しされ、2031年までCAGR8.22%で拡大すると予測されます。中国の規模はポリマー供給業者にとって大きな牽引力となっており、一方インド政府の食品パークに対する優遇措置は、カートン、パウチ、硬質PET容器の国内需要を促進しています。日本と韓国はプレミアム化と再生可能なガラス容器に注力する一方、東南アジア諸国では輸送コスト上昇に対抗するため軽量フレキシブル包装の採用が急速に進んでいます。地域全体では、輸出志向型の農産食品成長と国内消費のグレードアップを反映し、食品包装市場規模は2031年までに2,458億米ドルを超えると予測されています。

北米は成熟した包装食品カテゴリーとPCR規制における主導的立場により、価値ベースで第2位を維持しています。米国は植物由来素材の実証試験や化学的リサイクルのパイロット事業において最先端を走り、拡張可能な循環型経済の実現を約束しています。カナダはリサイクルインフラへの税額控除で業界発展を支援し、メキシコは米国小売業者への地理的近接性を活かし、国境沿いに合弁コンバーター企業を誘致しています。4州で実施中、複数州で導入準備中のEPR制度は、単一素材設計とリサイクル可能表示を促進します。これらの政策が相まって、高いベース消費量にもかかわらず、着実なCAGRを中単一桁台で支えています。

欧州市場はPPWR(包装廃棄物指令)に基づく厳格な環境規制によって形成されています。ドイツ、英国、フランスが生産量を主導し、イタリアは堆肥化可能なトレイの設計革新で先行しています。東欧の生産クラスターは、コスト効率を追求する西欧のコンバーター企業からの投資を集めています。規制負担があるにもかかわらず、欧州はデポジット返還制度の知識拠点としての地位を維持し、ラテンアメリカやアフリカの政策に影響を与えています。成長率はアジアに後れを取っていますが、プレミアムな持続可能な包装や廃棄物分別のためのデジタル透かし技術の普及率の高さにより、欧州は価値を確保しています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- アナリストによる3ヶ月間のサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- アジア全域における都市型コンビニエンスストアの急速な成長が、単品包装の需要を牽引しております

- 北米食品包装における使用済み再生材(PCR)含有率の法的推進

- 欧州における消費者向けミールキットサービスの急速な拡大に伴い、カスタマイズ可能な温度安定性包装が求められています

- 日本における即食シーフード需要の急増が、高バリア性レトルトパウチの採用を促進

- サブサハラアフリカにおけるコールドチェーンインフラ整備が非加熱処理カートンの成長を促進

- ラテンアメリカにおける小ロットSKU向けデジタル印刷の採用がブランド差別化を実現

- 市場抑制要因

- EUの使い捨てプラスチック指令により、多層フレキシブル構造のコンプライアンスコストが増加

- 再生樹脂価格の変動性が持続可能な包装形態のコスト競争力を損なう

- アジア太平洋地域における産業用堆肥化インフラの不足が堆肥化フィルムの普及を阻害

- 移行安全性への懸念が高脂肪食品用途における再生紙板の使用を制限

- サプライチェーン分析

- テクノロジーの展望

- 規制の見通し

- ポーターのファイブフォース分析

- 買い手・消費者の交渉力

- 供給企業の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

- 投資分析

第5章 市場規模と成長予測

- 素材タイプ別

- プラスチック

- PET

- PE(高密度ポリエチレンおよび低密度ポリエチレン)

- PP

- その他のプラスチック製品

- 紙・板紙

- 金属

- ガラス

- プラスチック

- 包装形態別

- 硬質

- 軟質

- 製品タイプ別

- 缶

- 瓶とジャー

- パウチ

- 段ボール箱

- その他の製品タイプ

- 技術別

- ガス置換包装(MAP)

- 真空包装

- ホットフィル

- 高圧処理(HPP)

- 滅菌

- レトルト

- 流通チャネル別

- 直販販売

- 間接販売

- 用途別

- 乳製品

- 鶏肉・肉製品

- 果物・野菜

- ベーカリー・菓子類

- シーフード

- レディミール・コンビニエンスフード

- 冷凍食品

- その他の用途

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- ロシア

- その他欧州

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- オーストラリアおよびニュージーランド

- その他アジア太平洋

- 中東・アフリカ

- 中東

- アラブ首長国連邦

- サウジアラビア

- トルコ

- その他中東

- アフリカ

- 南アフリカ

- ナイジェリア

- エジプト

- その他アフリカ

- 中東

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 北米

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア分析

- 企業プロファイル

- Amcor PLC

- Tetra Pak International S.A.

- Smurfit WestRock

- Ball Corporation

- Mondi Group

- Crown Holdings Inc.

- Sealed Air Corporation

- Sonoco Products Company

- International Paper Company

- Huhtamaki Oyj

- Graham Packaging Company Inc.

- Anchor Packaging Inc.

- Schur Flexibles Group

- ProAmpac LLC

- Constantia Flexibles

- Uflex Ltd.

- Stora Enso Oyj

- Clondalkin Group