航空機フェアリング:市場シェア分析、産業動向、統計、成長予測(2025年~2030年)

Aircraft Fairings - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 110 Pages

- 納期

- 2~3営業日

- 商品コード

- 1851122

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

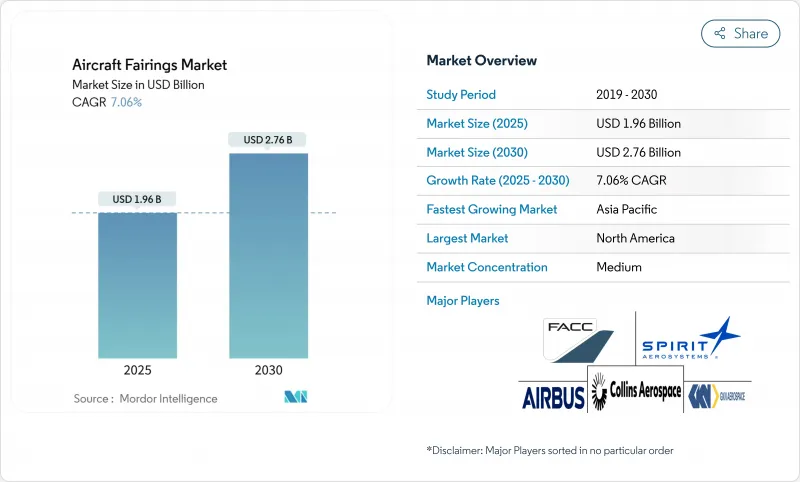

航空機フェアリング市場は、2025年に19億6,000万米ドル、2030年には27億6,000万米ドルの市場規模に達する見込みであり、予測期間中のCAGRは7.06%です。

1万5,000機を超える民間ジェット機の堅調な生産準備、燃費効率の義務化、老朽化した航空機の代替促進の加速が、長期的な需要見通しをもたらしています。複合材料の技術革新はこの成長パターンの中心です。炭素繊維強化ポリマー(CFRP)はすでに使用中のフェアリング材料の70%を占めており、このシフトは構造重量を削減し、耐腐食性を向上させる。2024年の販売量の48%を占めるナローボディ・プログラムへの依存度が高まっており、コストを抑制しながら生産規模を拡大できるサプライヤーが有利となっています。一方、UAVとeVTOLのコンセプトが急増しており、それぞれがラピッドプロトタイピングと少量生産を優先しているため、1機当たりのマージンが高いプレミアムニッチが形成されています。その結果、航空機フェアリング市場は、大量生産される商用プログラムと、急速に変化する先進的な航空モビリティの需要プールに二分され続け、サプライヤーは両分野のキャパシティをヘッジする必要に迫られています。

世界の航空機フェアリング市場の動向と洞察

燃費目標達成に向けた複合材の採用急増

燃料費削減のプレッシャーにさらされている航空会社は、アルミ製からCFRP製フェアリングへの切り替えを進めており、次世代航空機の複合材比率は、従来のA330の13%から、現在では50%以上に上昇しています。エアバスの多機能胴体実証機では、熱可塑性樹脂のスキンを使用することで、さらに10%の軽量化が可能であることを示しています。複合材フェアリングを取り付けた場合、生涯燃料の節約によって航空機の購入価格の15~20%を相殺することができます。しかし、この移行は、オートクレーブ、ロボットレイアップセル、専門的な労働力のために多額の資本支出を必要とするため、参入障壁が高くなり、OEMは成熟した複合材エコシステムを所有するパートナーを好むようになっています。

老朽化した航空機の迅速なフリート交換

年間700機以上のジェット機が退役し、後付け市場を拡大する部品の収穫と改修の需要を誘発します。ワイドボディのフェアリングは、長距離輸送のサイクルによって摩耗が激しくなり、納入が遅れる中、運航会社は新造機よりも空力アップグレードキットを求めるようになります。住友商事とWerner Aero社との提携に代表されるように、複合材フェアリングを二次市場向けに再生するサーキュラー・エコノミー・プログラムは支持を集めているが、CFRPのリサイクルには限りがあり、コストがかかるという厳しい現実に直面しています。

炭素繊維、エポキシ樹脂、高温樹脂の価格の高騰と変動がサプライヤーのマージンを圧迫

航空宇宙分野における炭素繊維の需要は毎年17%増加すると予測されているが、生産能力の増強には高価で長期的な投資が必要です。地政学的な緊張と関税へのエクスポージャーが価格予測を複雑にし、サプライヤーにコスト・プラス契約の採用を促すが、中小企業は運転資本を維持できない状況に追い込まれます。

セグメント分析

胴体フェアリングは、その複雑な翼と胴体の接合形状とOEM統合のハードルの高さにより、2024年の航空機フェアリング市場規模の33.24%を占めました。設計を変更すると空力特性の再試験が必要になるため、既存のサプライヤーはその座を明け渡すことが難しく、需要は低迷を続けています。ランディングギアフェアリングは、空港騒音規制の強化やeVTOLプログラムによる格納式ストラットの要件に後押しされ、CAGR7.15%で加速しています。翼胴フェアリングと制御面フェアリングは主流の製造率に沿ったままであるが、エンジンフェアリングは、冷却フェアリングシェルを義務付けるハイブリッド電気実証試験による増分の成長を拾い上げています。

新たなモビリティ・プラットフォームは、迅速な製造に設計ブリーフィングを歪める。ウィチタ州立大学の調査によると、UAVオペレータは、数週間ではなく数日で印刷可能なモジュール式フェアリングを好みます。ドイチェ・エアクラフト社のD328eco契約は、胴体と着陸装置のドアを1つの契約にまとめたもので、サプライヤーを統合したパッケージを目指すOEMの動きを示しています。このようなバンドルは、広範な設計ツールセットとテストアーティクル能力を持つベンダーに有利です。

CFRPのシェアが63.48%であることは、ワイドボディ、ナローボディ、さらには回転翼機プログラムに至るまで、CFRPの地位が確立していることを示しています。しかし、熱可塑性コンポジットと付加製造ポリマーは年間9.39%成長しており、オートクレーブのボトルネックを解消し、部品点数の統合を可能にして、組み立ての労力を削減しています。軽量UAVフェアリングでは、コストに敏感なグラスファイバーが採用されていますが、損傷に強い重要な部位(胴体下部のチャインパネルなど)では、依然としてアルミリチウム合金が採用されています。

ヘクセルのHexAM PEKKレーザー焼結プラットフォームは、従来の機械加工では不可能な複雑なフェアリング・ブラケットを印刷し、スクラップと重量を同時に削減しています。EUが資金提供するDOMMINIOの取り組みは、熱可塑性プラスチック製フェアリングに構造健全性センサーを埋め込むことで、このデジタルの糸を拡張し、予知的な完全性監視をライン・フィット設備に直接もたらします。やがて、ラミネートCFRPの表皮と印刷された熱可塑性プラスチックのリブとを嵌合させる混合材料スタックが、航空機フェアリング市場を独占する可能性があります。

地域分析

北米は2024年に航空機フェアリング市場シェアの36.54%を占め、ボーイングの生産回復と、米国の複数の州で複合材生産能力を増強するGEエアロスペースの10億米ドルの製造委託に支えられています。ワシントン州とサウスカロライナ州には長い歴史を持つクラスターがあり、サプライヤーに成熟したエコシステムを提供しています。RTXの20億米ドルを投じた設備拡張は、当面の事業環境がインフレ基調にあるとはいえ、OEMの持続的需要への信頼を浮き彫りにしています。

アジア太平洋は、2030年までのCAGRが8.83%と、最も急成長している地域です。中国のC919やインドのHTT-40のような国産化計画は、欧米のTier-1企業を合弁工場に引き込み、国産化の必要性を強めています。ストラタ・マニュファクチャリングは38%の生産増加を記録し、エアバスやボーイングのモデルから1万1,774機の構造体を輸出し、複合材大国になるという湾岸の野心を示しています。ハンファ・エアロスペースは、GEとロールス・ロイスの部品を生産する10万平方メートルのベトナムの新拠点で、このシフトをさらに実証しています。

欧州はエアバスの生産テンポの恩恵を受け、グリーン素材に注力しています。エアバスのヘリコプターのフェアリング用のバイオベースの炭素繊維の実現可能性試験は、カーボンニュートラルのサプライチェーンに向けた初期段階を示すものです。日本は、高品位炭素繊維サプライヤーとしてのニッチを維持し、三菱化学は将来のモビリティ・プログラムで12%の複合材成長を目標としています。一方、中東とアフリカ市場は、自由貿易地域と長距離路線への近接性を活用して、OEMからオフセットの仕事を獲得しています。しかし、欧米の同業他社と同等の認証を取得することは、現在も継続中の課題です。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- 燃費目標達成に向けた複合材採用の急増

- 老朽化した航空機のフリート全体での急速な更新

- UAV、高度な航空機動性、eVTOLプラットフォームの普及

- 交換用フェアリングに対するアフターマーケットMRO支出の成長

- ハイブリッド電気航空機計画が新たなフェアリング設計に拍車をかける

- 記録的な商業用単通路の受注残が生産の見通しを下支え

- 市場抑制要因

- 炭素繊維、エポキシ樹脂、高温樹脂の価格の高騰と変動

- 厳しい認証サイクルが新しいフェアリング技術を遅らせる

- サプライチェーンの統合による調達の選択肢の減少と利幅の縮小

- 地政学的貿易摩擦と関税が原材料コストを押し上げる

- バリューチェーン分析

- 規制とテクノロジーの展望

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場規模と成長予測

- 用途別

- 機体

- 着陸装置

- 翼

- 制御表面

- エンジン

- 材料別

- 炭素繊維強化ポリマー(CFRP)

- ガラス繊維複合材料

- 金属合金

- 熱可塑性複合材料

- 付加製造熱可塑性プラスチック

- 航空機タイプ別

- 商業用

- ナローボディ商用航空機

- ワイドボディ商用航空機

- ミリタリー

- コンバット

- 非コンバット

- 一般航空

- 無人システム

- 商業用

- 販売チャネル別

- OEM生産

- アフターマーケットMRO

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- 英国

- ドイツ

- フランス

- ロシア

- その他欧州地域

- アジア太平洋地域

- 中国

- 日本

- インド

- 韓国

- その他アジア太平洋地域

- 南米

- ブラジル

- その他南米

- 中東・アフリカ

- 中東

- サウジアラビア

- アラブ首長国連邦

- その他中東

- アフリカ

- 南アフリカ

- その他アフリカ

- 北米

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア分析

- 企業プロファイル

- Airbus Aerostructures(Airbus SE)

- Boeing Aerostructures Australia(The Boeing Company)

- Collins Aerospace(RTX Corporation)

- FACC AG

- GKN Aerospace

- Spirit AeroSystems, Inc.

- Saab AB

- Strata Manufacturing PJSC

- LATECOERE S.A

- Kaman Corporation

- CTRM Sdn. Bhd.

- ShinMaywa Industries, Ltd.

- Royal Engineered Composites

- FDC Composites Inc.

第7章 市場機会と将来の展望

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 110 Pages

- 納期

- 2~3営業日