|

市場調査レポート

商品コード

2038745

航空機フェアリング市場の機会、成長要因、業界動向分析、および2026年~2035年の予測Aircraft Fairings Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

カスタマイズ可能

|

|||||||

| 航空機フェアリング市場の機会、成長要因、業界動向分析、および2026年~2035年の予測 |

|

出版日: 2026年04月28日

発行: Global Market Insights Inc.

ページ情報: 英文 176 Pages

納期: 2~3営業日

|

概要

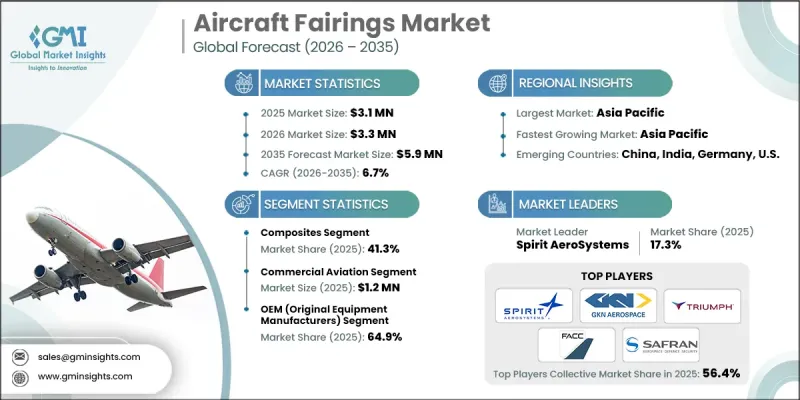

世界の航空機フェアリング市場は、2025年に310万米ドルと評価され、2035年までにCAGR 6.7%で成長し、590万米ドルに達すると推定されています。

市場の拡大は、民間航空機の生産増加、空力効率への重視の高まり、および航空機フリート全体における燃料効率最適化への需要拡大によって牽引されています。メーカーが軽量化と性能向上を優先するにつれ、軽量複合材構造の採用が加速しています。さらに、メンテナンス、修理、オーバーホール(MRO)活動の拡大が、航空機フェアリングに対する堅調なアフターマーケット需要を支えています。防衛航空分野の近代化プログラムも、先進的な外部構造部品の持続的な調達に寄与しています。航空会社や航空機OEM各社は、燃費と運用効率の向上にますます注力しており、これが先進的なフェアリング設計のさらなる統合を促進しています。継続的な機体数の拡大と高い航空機稼働率は、アフターマーケットにおける交換サイクルを後押ししています。材料工学および構造設計における技術の進歩により、耐久性と空力性能の向上が可能になっています。モジュール式およびプラットフォームベースのフェアリング設計アプローチへの移行は、製造戦略をさらに再構築し、生産効率を向上させ、民間および軍用航空の両セクターにおける長期的な市場成長を支えています。

| 市場の範囲 | |

|---|---|

| 開始年 | 2025年 |

| 予測期間 | 2026年~2035年 |

| 開始時の市場規模 | 310万米ドル |

| 予測額 | 590万米ドル |

| CAGR | 6.7% |

2025年、複合材料セグメントは41.3%のシェアを占めました。この優位性は、民間航空機および防衛用航空機の双方において、炭素繊維および強化複合材料が広く使用されていることに起因しています。これらの材料は、強度対重量比の効率性、耐食性、そして複雑な空力構造を支える能力が高く評価されており、OEM生産およびアフターマーケット用途において継続的な需要が確保されています。

2025年、民間航空機セグメントは120万米ドルを占めました。堅調な航空機生産台数と、胴体、主翼、エンジンアセンブリ全体へのフェアリングの広範な採用が、このセグメントを支える主な要因となっています。進行中の機体増強および更新プログラムにより、民間航空機の製造および整備業務におけるフェアリングへの需要は安定して維持されています。

2025年、北米の航空機フェアリング市場は31.4%のシェアを占めました。同地域の成長は、主要な航空機OEMメーカーやティア1航空機構造部品サプライヤーの強力な存在感、および商用・防衛用航空機からなる大規模な運用機群によって支えられています。活発な生産活動と、先進的な複合材料および空力技術の早期導入が、新規航空機プログラム全体での需要を引き続き牽引しています。また、同地域は確立されたMROエコシステムと安定した防衛支出の恩恵を受けており、これらが航空機フェアリングの更新およびアップグレード要件をさらに後押ししています。

よくあるご質問

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- 利益率

- コスト構造

- 各段階における付加価値

- バリューチェーンに影響を与える要因

- ディスラプション

- 業界への影響要因

- 促進要因

- 民間航空機の生産増加

- 燃費効率と抗力低減への注目が高まっています

- 先進複合材料の利用拡大

- 航空機MROおよびアフターマーケットセグメントの拡大

- 防衛用航空機の近代化および機体更新の進展

- 業界の潜在的リスク&課題

- 設計の高度な複雑性と認証要件

- 航空機生産の遅延およびプログラムの中断によるリスク

- 市場機会

- 先進的航空モビリティおよび電動垂直離着陸(eVTOL)航空機プラットフォームの開発拡大

- フェアリング製造における積層造形およびラピッドツーリングの採用

- 促進要因

- 成長可能性分析

- 規制情勢

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ

- ポーター分析

- PESTEL分析

- 技術およびイノベーションの動向

- 現在の技術動向

- 新興技術

- 価格動向

- 地域別

- 製品別

- 価格戦略

- 新興ビジネスモデル

- コンプライアンス要件

- 特許および知的財産分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 地域別

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ

- 市場集中度の分析

- 地域別

- 主要企業の競合ベンチマーキング

- 財務実績の比較

- 売上高

- 利益率

- 研究開発

- 製品ポートフォリオの比較

- 製品ラインの幅

- 技術

- イノベーション

- 地域展開の比較

- 世界展開の分析

- サービスネットワークのカバー範囲

- 地域別市場浸透率

- 競合ポジショニングマトリックス

- リーダー

- チャレンジャー

- フォロワー

- ニッチプレイヤー

- 戦略的展望マトリックス

- 財務実績の比較

- 主な発展

- 合併・買収

- パートナーシップおよび提携

- 技術的進歩

- 事業拡大および投資戦略

- デジタルトランスフォーメーションの取り組み

- 新興・スタートアップ競合企業の動向

第5章 市場推計・予測:素材タイプ別、2022-2035

- 複合材料

- 金属

- ハイブリッド

第6章 市場推計・予測:プラットフォーム別、2022-2035

- 商用航空

- ナローボディ機

- ワイドボディ機

- リージョナルジェット

- 軍事航空

- 戦闘機

- 輸送機

- 軍用UAV

- 一般航空

- ヘリコプター(回転翼機)

- 民間ヘリコプター

- 軍用ヘリコプター

第7章 市場推計・予測:用途別、2022-2035

- 胴体フェアリング

- 主翼フェアリング

- 着陸装置フェアリング

- 推進フェアリング

- 操縦面フェアリング

- レーダー・アンテナフェアリング

- その他

第8章 市場推計・予測:エンドユーザー別、2022-2035

- OEM(オリジナル・エクイップメント・メーカー)

- アフターマーケット(MROおよび交換用)

第9章 市場推計・予測:地域別、2022-2035

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- ロシア

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第10章 企業プロファイル

- 世界の主要企業

- Spirit AeroSystems

- GKN Aerospace

- Triumph Group

- FACC AG

- Safran

- 地域別主要企業

- 北米

- Kaman Corporation

- Nordam Group

- Meggitt

- アジア太平洋地域

- ShinMaywa Industries

- AVIC

- 欧州

- Leonardo S.p.A.

- Senior plc

- Aernnova Aerospace

- Stelia Aerospace

- MTorres

- 北米