|

市場調査レポート

商品コード

1907000

RTD(Ready To Drink)飲料:市場シェア分析、業界動向と統計、成長予測(2026年~2031年)Ready To Drink Beverages - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| RTD(Ready To Drink)飲料:市場シェア分析、業界動向と統計、成長予測(2026年~2031年) |

|

出版日: 2026年01月12日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

概要

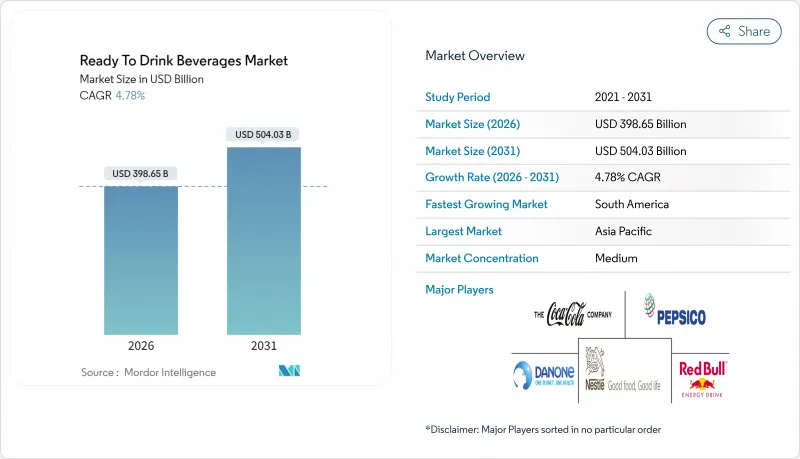

2026年のRTD(Ready To Drink)飲料市場規模は3,986億5,000万米ドルと推定され、2025年の3,804億6,000万米ドルから成長が見込まれます。

2031年の予測では5,040億3,000万米ドルに達し、2026年から2031年にかけてCAGR4.78%で拡大する見通しです。

先進国の家庭では長年これらの製品が受け入れられてきましたが、新興市場も急速に追いつきつつあります。都市化、忙しいライフスタイル、可処分所得の増加がこの動向を後押ししています。世界的に、より健康的な選択肢への移行はあらゆる層に広がっています。腸内環境の改善、認知機能の向上、免疫サポートを重視した製品の迅速な投入が進む一方、持続可能性の観点から包装形態が再構築されるなど、世界のRTD(Ready To Drink)飲料市場全体で変化が起きています。競合は中程度であり、世界の企業はニッチ市場を狙う機敏な新興企業と対峙しています。砂糖や包装廃棄物に関する規制の監視がイノベーションを制限し、方向性を示しています。メーカーはブランド価値を高め、利益率を維持するため、天然甘味料、再生素材、明確な表示を採用しています。

世界のRTD(Ready To Drink)飲料市場の動向と洞察

外出先での健康飲料に対する需要の増加

生活スタイルの多忙化と健康意識の高まりに伴い、消費者の期待は変化しています。世界保健機関(WHO)は、慢性疾患予防における栄養の役割を認識する世界の潮流を指摘し、健康効果と利便性を兼ね備えた機能性飲料の需要を牽引しています。この動向は全年齢層に広がり、高齢層では自身のニーズに合わせたRTD飲料を選択する傾向が強まっています。時間的制約に直面する専門職が集まる都市部は、RTD飲料の主要成長市場です。2024年、国際労働機関(ILO)の報告によれば、世界人口の57.92%が就労しており、利便性と健康志向を兼ね備えた選択肢への需要を反映しています。健康効果を強調しつつRTDの利便性を維持するブランドは、成功に向けて有利な立場にあります。さらに、糖分摂取削減や機能性栄養素を促進する政府施策が、RTD飲料市場全体における健康志向型RTD飲料の成長を支えています。

低糖質・無糖飲料への消費者の志向

世界の健康推進策により糖分摂取量の削減が進んでおり、WHOは自由糖分がエネルギー摂取量の10%未満となるよう推奨しています。これにより飲料メーカー、特に砂糖税を導入している地域では、味を損なわずに低カロリー代替品を開発する規制上の圧力が高まっています。欧州食品安全機関(EFSA)による天然甘味料の承認など、規制当局の認可がこうした取り組みを支えています。しかしながら、メーカーは味と低糖度のバランスを取る課題に直面しており、代替甘味料やフレーバー技術への投資を促しています。米国食品医薬品局(FDA)が改訂した栄養表示ラベルでは添加糖分が強調され、消費者の意識が高まり、低糖分オプションへの需要に影響を与えています。糖分の健康への影響に対する認識の高まりは、味と健康効果を両立させるブランドにとって機会をもたらしています。その結果、RTD(Ready To Drink)飲料市場におけるイノベーションと規制順守を原動力として、低糖飲料市場は予測期間中に大幅な成長が見込まれています。

化学成分に関する健康懸念

RTD飲料メーカーは、人工成分に対する世界の規制監視の強化という課題に直面しています。欧州食品安全機関(EFSA)は安全基準を厳格化し、FDAは合成添加物に対するより強力な安全性データの提出を求めています。これらの圧力は、合成成分に依存する傾向のあるエナジードリンクや機能性飲料にとって特に重大です。メーカーは規制と消費者の要求を満たす天然代替品に目を向けていますが、これによりコスト増加や効果の低下が懸念されます。カナダでは、保健省の新たな表示規則により人工成分の開示が明確化され、消費者の習慣が変化しています。これによりメーカーは、保存安定性とコストのバランスを取りつつ、クリーンラベル製品の優先度を高めています。企業は製品の再設計や天然成分製品の導入を進めていますが、こうした変更はサプライチェーン、収益性、効率性に影響を与えています。課題はあるもの、業界のイノベーションへの注力は、RTD(Ready To Drink)飲料業界における進化する期待に効果的に応える基盤を築いています。

セグメント分析

2025年、エナジードリンクは17.42%の市場シェアを占めております。これは機能性成分の革新と、エネルギー補給以上の効果を求める消費者層の拡大が牽引しております。国際エナジードリンク協会の調査では、特に18~34歳層における消費量の著しい伸びが明らかになっております。各ブランドは、天然カフェインやL-テアニンなどの機能性成分を用いた製品改良により、バランスの取れたエネルギー供給と急激な落ち込みの回避を図っています。FDAのカフェインガイドラインは、透明性の高い表示と責任あるマーケティングを促進しました。消費者がダイナミックなライフスタイルに即した安定した効果を重視する中、強いブランドロイヤルティとプレミアム価格設定がこのセグメントを支え、RTD(Ready To Drink)飲料市場の成長を後押ししています。

乳製品および代替乳製品セグメントは、タンパク質やプロバイオティクスの健康効果に対する認識の高まりを背景に、2026年から2031年にかけてCAGR5.11%で成長すると予測されています。米国農務省(USDA)の食事ガイドラインは、RTD乳飲料を便利な栄養源として推奨しています。メーカーは消費者の需要に応えるため、1食あたり15~30グラムの高タンパク製品を開発中です。FDAのプロバイオティクス承認とカナダ保健省のプロバイオティクス菌株認可がイノベーションを可能にし、メーカーは利便性と実証済みの健康効果を組み合わせることで、RTD飲料市場全体におけるセグメント成長を牽引しています。

2025年には、確立された供給網、明確な規制経路、コスト優位性により、従来型原料が67.92%のシェアで市場を独占します。FDAの安全性データベースは予測可能な規制プロセスと開発コストの低減を保証し、一貫した品質と世界の流通に不可欠な原料となっています。欧州食品安全機関(EFSA)などの規制機関による安全性検証に加え、消費者の認知度とコスト効率の高さが、特に価格に敏感な市場における地位を強化しています。製造効率とサプライチェーンの信頼性は、RTD飲料業界における大量生産をさらに支えています。

自然派・有機セグメントは、有機認証に対する規制支援と、馴染みのある原料を好む消費者の増加を背景に、2026年から2031年にかけてCAGR5.62%で成長すると予測されています。米国農務省(USDA)の国家有機プログラムが明確な基準を確立することで、消費者の信頼が高まり、プレミアム価格設定が可能となります。カナダ保健省による自然健康製品とその治療効果の主張への承認も、この成長をさらに後押しし、メーカーが特定の健康効果を強調することを可能にしております。国際有機農業運動連盟(IFOAM)などの団体が主導する国際的な有機基準は、世界の貿易を促進し、消費者の認知度を高めております。さらに、天然保存技術や原料加工技術の進歩により、メーカーは従来品に匹敵するクリーンラベル製品を開発することが可能となっております。

地域別分析

2025年、アジア太平洋地域は世界のRTD(Ready To Drink)飲料市場を33.05%のシェアでリードしています。この優位性は、都市化、拡大する中産階級、利便性と機能性への志向の変化に起因しています。食品安全と栄養を重視する政府の取り組みがさらなる成長を促進しています。例えば、中国国家衛生健康委員会は食事ガイドラインに機能性飲料を組み込み、インド食品安全基準局は機能性食品・飲料の規制を施行しています。地域の多様な嗜好が独自の製品展開を形成し、改善されたコールドチェーンインフラと近代的な小売業がこれを支えています。日本の厚生労働省は機能性飲料の利点を強調し、信頼性の高い健康強調表示を可能にすることで、RTD飲料市場全体の消費者に訴求しています。

南米地域は2026年から2031年にかけてCAGR6.55%と最も高い成長が見込まれており、所得の増加とRTD飲料を好むライフスタイルの変化が牽引役となります。ブラジルの国家衛生監視庁(ANVISA)は機能性飲料の規制を簡素化し、承認手続きを迅速化しました。同地域は農業資源を活用し、地元市場および輸出市場向けに固有の原料を用いた飲料を生産しています。アルゼンチンでは栄養表示の義務化により透明性が向上し、より健康的な選択肢への需要が高まっています。生鮮飲料が主流である一方、メーカーは品質と天然素材に注力することで課題を克服できます。バランスの取れた栄養摂取を促進する政府の健康キャンペーンも、RTD飲料業界における機能性飲料の成長をさらに後押ししています。

北米は革新性と厳格な安全・品質基準のバランスを保ち、強固な地位を維持しています。FDA(米国食品医薬品局)の原料・表示に関する監督はメーカーを導き、機能性RTD製品の革新を促進しています。カナダ保健省の自然健康製品規制は、承認済み機能性原料の効能を強調することを可能にし、プレミアムブランディングと消費者教育を実現しています。欧州では、欧州食品安全機関(EFSA)の厳格な承認プロセスが安全性を確保しつつイノベーションを促進しています。中東・アフリカ地域では、都市化と若年層人口がRTD飲料の普及を牽引していますが、多様な規制に対応するため、地域当局との連携による個別戦略が求められます。

その他の特典:

- エクセル形式の市場予測(ME)シート

- アナリストによる3ヶ月間のサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- 外出先での健康飲料に対する需要の増加

- 低糖質・無糖飲料への消費者志向

- 生産面における技術的進歩

- 風味・原材料・包装形態におけるイノベーション

- スポーツおよびフィットネス活動への参加増加

- エンドースメントとソーシャルメディアマーケティングの影響力拡大

- 市場抑制要因

- 化学成分に関する健康上の懸念

- 消費者の新鮮な調理済み飲料への嗜好

- 環境への影響と包装廃棄物に関する懸念

- 原材料価格の変動

- 消費者行動分析

- 規制の見通し

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の程度

第5章 市場規模と成長予測

- 製品タイプ別

- 紅茶

- コーヒー

- エナジードリンク

- ヨーグルト飲料

- 乳製品および乳製品代替品

- フレーバー付きおよび栄養強化水

- その他の製品タイプ

- 原材料別

- 従来型

- ナチュラル&オーガニック

- パッケージング別

- PET/ガラス瓶

- テトラパック

- 缶

- その他の包装形態

- 流通チャネル別

- オントレード

- オフトレード

- スーパーマーケット/ハイパーマーケット

- コンビニエンスストア/食料品店

- オンライン小売店

- その他流通チャネル

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- その他北米地域

- 欧州

- ドイツ

- 英国

- イタリア

- フランス

- スペイン

- オランダ

- ポーランド

- ベルギー

- スウェーデン

- その他欧州地域

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- インドネシア

- 韓国

- タイ

- シンガポール

- その他アジア太平洋地域

- 南米

- ブラジル

- アルゼンチン

- コロンビア

- チリ

- ペルー

- その他南米

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

- ナイジェリア

- エジプト

- モロッコ

- トルコ

- その他中東・アフリカ地域

- 北米

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア分析

- 企業プロファイル

- Red Bull GmbH

- PepsiCo, Inc.

- The Coca-Cola Company

- Nestle S.A

- Danone S.A

- Yakult Honsha Co. Ltd

- Suntory Holdings Limited

- JAB Holding Company

- Asahi Group Holdings Ltd

- Starbucks Corporation

- Unilever PLC

- Monster Energy Company

- Meiji Holdings Co. Ltd.

- Kirin Holdings Company, Limited.

- ITO EN, LTD.

- Danone S.A

- Red Bull GmbH

- The Coca Cola Company

- AriZona Beverages USA

- Milo's Tea Company, Inc.