|

市場調査レポート

商品コード

1910460

液体塗膜:市場シェア分析、業界動向と統計、成長予測(2026年~2031年)Liquid Applied Membrane - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 液体塗膜:市場シェア分析、業界動向と統計、成長予測(2026年~2031年) |

|

出版日: 2026年01月12日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

概要

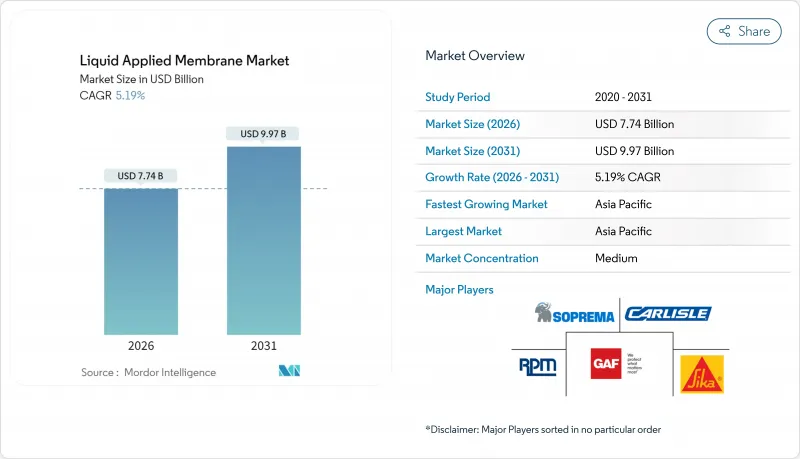

液体塗膜市場は、2025年に73億6,000万米ドルと評価され、2026年の77億4,000万米ドルから2031年までに99億7,000万米ドルに達すると予測されています。

予測期間(2026-2031年)におけるCAGRは5.19%と見込まれています。

エンドユーザーは、ロール状製品からシームレスコーティングへの移行を継続しております。後者はひび割れを補修し、動きに耐え、より長い耐用年数を実現するため、ライフサイクルコストの削減につながります。中国、インド、米国におけるインフラ更新プログラムが需要を支える一方、カリフォルニア州、カナダ、欧州連合(EU)における厳格な低揮発性有機化合物(VOC)規制が、水性化学製品への仕様変更を促進しております。クールルーフ、太陽光発電統合、グリーンルーフ組立を奨励する建築基準が、さらなる普及を加速させています。メーカーは、混雑した現場でのダウンタイムを削減する自己修復型、太陽光発電対応型、急速硬化型システムを投入することで、利益率の低下に対抗しています。

世界の液体塗膜市場の動向と洞察

建物の長寿命化に向けた防水膜の活用拡大

所有者は現在、先進的なコーティングを予期せぬ修理を抑制する資本資産として扱っています。オークリッジ国立研究所の試算によれば、商業用屋根の寿命をわずか5年延長するだけで、米国の廃棄物処理コストを年間25億米ドル削減し、埋立地の容量も削減できるとされています。MAPEI社のMapelastic AquaDefenseのような液体システムは、最大3.2mmのひび割れを橋渡しし、熱サイクル下でも柔軟性を維持するため、地震多発地域において魅力的な選択肢となっています。保険会社は、所有者が長寿命防水シートを指定した場合に保険料割引を提供し始めており、導入を促進する経済的インセンティブが追加されています。

成熟経済圏における老朽化屋根の費用対効果の高い改修

カナダでは、SOPREMA社がCFシャンプレーンショッピングセンターの屋根を再舗装し、全面撤去と比較して資材費を45%削減、工期を35%短縮しながら、耐用年数をさらに25年延長しました。コーティングは不規則な下地に密着するため、施工業者はデッキの撤去という混乱を避けられ、ショッピングモール、病院、学校は営業を継続できます。また、再舗装は廃棄物処理量と埋蔵炭素量を削減し、施設管理チームが巨額の設備投資予算なしでESG目標を達成する一助となります。

シート状およびプレハブ型塗膜の供給状況

TPOなどの熱可塑性ロール材は、広大な物流施設において施工速度の優位性を維持し、施工業者は1シフトあたり900m2以上の施工が可能です。メーカーはコーティングの成長に対応し、トーチ使用リスクを低減する自己接着シートを発売し、液体防水材の差別化要因の一つを削りました。しかしながら、複雑な貫通部、垂直面への接続部、居住空間での改修工事など、火気使用が禁止される現場では、液体防水材が依然として強い支持を得ています。

セグメント分析

アスファルト系コーティングは、数十年にわたる現場実績と低単価を背景に、2025年の液体塗膜市場で30.10%のシェアを占めました。ポリウレタン系は、太陽光パネル・クールルーフ顔料・伸縮目地への耐性を有するエラストマー性能に支えられ、CAGR6.24%で価値成長を牽引しました。

アクリル系分散液は、ローラー施工が可能で水洗浄による清掃が容易なため、改修工事で採用が増加しています。PMMA(ポリメチルメタクリレート)は、30分という短時間で硬化するため、高交通量のバルコニーやスタジアムコンコースなど、工期確実性が求められる現場で活用されています。ポリウレタンとアスファルトの混合物やポリウレア変性エラストマーなどのハイブリッド化学製品は、超短時間での使用再開や寒冷地施工といったニッチな需要に対応し、設計者の設計自由度を拡大しています。

液体塗膜市場レポートは、タイプ別(セメント系、アスファルト系、ポリウレタン系、ポリウレア系、アクリル系など)、用途別(屋根、壁、地下・トンネル、その他用途)、エンドユーザーセクター別(住宅、商業、工業、公共施設・インフラ)、地域別(アジア太平洋、北米、欧州など)に分類されています。市場予測は金額(米ドル)ベースで提供されます。

地域別分析

アジア太平洋地域は2025年の世界収益の52.70%を占め、2031年までCAGR6.65%で拡大が見込まれます。中国の地下鉄延伸、インドのスマートシティ回廊、ASEANの洪水対策トンネルは、合わせて数億平方メートルの防水材を必要とします。現地開発業者はEN 14891およびGB 50108への準拠をますます要求しており、試験証明書の更新を目的とした輸入を促進しています。

北米市場は成熟しつつも機会豊富な領域であり、屋根改修が主流です。米国自治体ではクールルーフ補助金制度を拡充、カナダでは2025年施行の連邦VOC規制が水性技術普及を加速させています。メキシコ・コアツァコアルコス浸水式トンネルではGCP社のIntegritankシステムがシームレスな防食対策として採用され、複雑なプロジェクトにおける地域の技術力を裏付けています。

欧州の改修ブームは脱炭素化が中心であり、ドイツのBEG補助金制度では気密性向上が求められ、流動性気密材の採用が一般的です。ジョージア州がEUのVOC規制上限を採用したことは、規制の東側への調和を示しています。中東・アフリカ地域は高い成長性を示す一方、気候の極端さが課題です。ドバイのエキスポシティ公園では、45℃の夏季をチョーキング(白化現象)なく耐えるため、脂肪族ポリウレアが採用されました。

その他の特典:

- エクセル形式の市場予測(ME)シート

- アナリストによる3ヶ月間のサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- 建物の長寿命化に向けた防水膜の普及拡大

- 成熟経済圏における老朽化屋根の費用対効果の高い改修

- アジア太平洋地域およびアフリカにおけるインフラ整備の急拡大

- VOCフリーソリューションを義務付ける規制

- 太陽光発電対応型液体屋根材の急速な普及

- 市場抑制要因

- シートおよびプレハブ膜の入手可能性

- 石油化学原料価格の変動性

- 新興市場における施工技術者の不足

- バリューチェーン分析

- ポーターのファイブフォース

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の程度

第5章 市場規模と成長予測

- タイプ別

- セメント系

- アスファルト

- ポリウレタン

- ポリウレア

- アクリル(分散)

- PMMA

- ハイブリッド(ポリウレタン/ポリウレア(PU/PUA)、改質ポリウレタン・アスファルト系など)

- 用途別

- 屋根材

- 壁

- 地下およびトンネル

- その他の用途(床、バルコニー、歩道、ポディウム、タンク、飲料水タンク、プランターボックスなど)

- 最終用途分野別

- 住宅用

- 商業用

- 産業

- 公共施設・インフラ

- 地域

- アジア太平洋地域

- 中国

- インド

- 日本

- 韓国

- ASEAN

- その他アジア太平洋地域

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- ロシア

- その他欧州地域

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- その他の中東・アフリカ

- アジア太平洋地域

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア(%)/順位分析

- 企業プロファイル

- Alchimica

- ARDEX Group

- Bostik

- Carlisle Companies Incorporated

- Fosroc Inc.

- GAF Materials LLC

- HB Fuller

- Holcim

- Johns Manville

- MAPEI SpA

- RPM INTERNATIONAL INC.

- Saint-Gobain

- Sika AG

- SOPREMA Group