|

市場調査レポート

商品コード

1642072

オーバーザトップ(OTT):市場シェア分析、業界動向・統計、成長予測(2025年~2030年)Over The Top (OTT) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| オーバーザトップ(OTT):市場シェア分析、業界動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

- 全表示

- 概要

- 目次

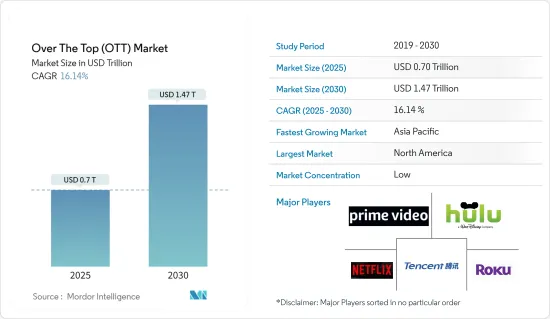

オーバーザトップ(OTT)市場規模は2025年に7,000億米ドルと推定され、2030年には1兆4,700億米ドルに達すると予測され、予測期間(2025-2030年)のCAGRは16.14%です。

オーバーザトップ(OTT)市場とは、ケーブルテレビや衛星テレビのような伝統的な配信チャンネルをバイパスして、ビデオ、オーディオ、その他のメディア・コンテンツをインターネット経由でユーザーに直接配信することを指します。OTTプラットフォームは、映画、テレビ番組、ライブイベント、オリジナル番組など、幅広いコンテンツへのオンデマンドアクセスを提供します。

主なハイライト

- オーバーザトップ(OTT)とは、ケーブルや衛星プロバイダーベースのプラットフォームではなく、高速インターネット接続を介して提供される映画やテレビのコンテンツ・プラットフォームです。OTTの採用は、ビデオ、音楽、ポッドキャスト、オーディオ・ストリーミングのカテゴリーに大きく貢献しています。採用が増加している背景には、ジャンルの選択肢の狭さ、パッケージングの柔軟性、利用可能なデバイスの広さ、インターネットの普及、コストの低さなどがあります。カスタマイズされたコンテンツに対する需要の高まりは、OTTデバイスの大幅な普及率につながった。

- スポーツやエンターテインメント・サービスのコモディティ化が進み、OTTプロバイダー間の競争が激化していることが、オーバーザトップ(OTT)市場を牽引すると予想されます。近年、スポーツ・イベントやエンターテインメント・コンテンツの消費方法に大きな変化が起きています。従来、これらのサービスは主にケーブルテレビや衛星放送の契約を通じて提供されており、カスタマイズやオンデマンド視聴のオプションは限られていました。しかし、OTTプラットフォームの台頭は、幅広いスポーツイベント、ライブ放送、エンターテインメントコンテンツを消費者に直接提供することで、このモデルを破壊しました。

- 新興市場でSVOD(Subscription Video on Demand)サービスの採用が増加していることが、OTT(Over-the-Top)市場を牽引すると予想されます。いくつかの要因により、SVODサービスは新興市場を含む世界中で大きな人気を博しています。多くの新興国における中間層の拡大と可処分所得の増加が、SVODサービスの成長に寄与しています。加入する経済的余裕を持つ個人が増えるにつれ、OTTプラットフォームを通じて多種多様なコンテンツにアクセスしたいという需要が高まっています。

- ビデオコンテンツの違法コピーは、OTT市場に影響を与える重要な問題です。著作権侵害には、著作権で保護されたコンテンツの無許可の配信と消費が含まれ、コンテンツ制作者と合法的なストリーミングプラットフォームの収益損失につながります。著作権侵害は、加入料や広告収入に依存して事業を維持し、コンテンツ制作に資金を供給しているOTTプロバイダーのビジネスモデルを損ないます。

- COVID-19の流行は、オーバーザトップ(OTT)市場に大きな影響を与えました。世界の健康危機とそれに伴う封鎖措置は、ストリーミング・サービスに対する需要の急増につながり、いくつかの点でOTT産業の成長を加速させました。規制のために家に閉じこもり、エンターテインメントの選択肢を求める人々によって、ストリーミングサービスの需要は急増しました。多くの個人が、映画、テレビ番組、ドキュメンタリー、その他の形態のコンテンツを求めてOTTプラットフォームを利用しました。この需要の急増により、既存のストリーミング・サービスの契約数は大幅に増加し、新たなプラットフォームも登場しました。

オーバーザトップ(OTT)市場の動向

スマートデバイスの普及とインターネットの高速化がOTT市場を牽引する見込み

- スマートデバイスの普及と高速インターネットへのアクセスの拡大が、オーバーザトップ(OTT)市場の成長を促進する主な要因となっています。スマートフォン、タブレット、スマートテレビ、その他の接続機器の普及が進み、ユーザーはOTTサービスにアクセスする手段が増えました。これらの機器にはインターネット接続機能が搭載され、ストリーミング・アプリケーションをサポートしているため、消費者はお気に入りの番組や映画、その他のコンテンツをオンデマンドで簡単に視聴できます。

- ブロードバンドや4G/5Gモバイルネットワークなどの高速インターネット接続の利用可能性は、シームレスなストリーミング体験を可能にする上で重要な役割を果たしています。インターネット・ユーザーの増加は世界の傾向だが、地域差も存在します。

- シスコシステムズによると、予測期間中、インターネットの普及率が最も高いのは北米である(次いで西欧)。それでも、中東とアフリカは増加すると予想されている(2018年から2023年までのCAGRは10%)。インターネットの高速化により、よりスムーズな再生、バッファリング時間の短縮、高精細(HD)および超高精細(UHD)コンテンツのストリーミングが可能になります。これにより、全体的なユーザー体験が大幅に改善され、OTTサービスの人気が高まる一因となっています。

- スマート・デバイスと高速インターネットの組み合わせは、パーソナライゼーションと利便性の向上にもつながっています。OTTプラットフォームは、データ分析と推薦アルゴリズムを活用してユーザーの嗜好を理解し、パーソナライズされたコンテンツ推薦を提供します。ユーザーはインターネット接続さえあれば、いつでもどこでもコンテンツにアクセスできます。

- こうした要因がOTTプラットフォームの成長に拍車をかけ、多くの加入者を惹きつけ、加入料や広告による収益を押し上げています。その結果、従来のメディア企業や放送局はOTTの重要性を認識し、ストリーミング・サービスを開始したり、既存のOTTプラットフォームと提携したりして、この拡大する市場に参入しています。

北米が大きな市場シェアを占める見込み

- 北米のOTT市場は近年著しい成長を遂げています。北米には、Netflix、Amazon Prime Video、Hulu、Disney+など、最も著名で確立されたOTTプラットフォームがあります。これらのプラットフォームは多くの加入者を獲得しており、映画、テレビ番組、ドキュメンタリー、オリジナル作品などの膨大なコンテンツライブラリを提供しています。

- 北米では、Roku、Apple TV、Amazon Fire TV、Google Chromecastなどのストリーミングデバイスが広く普及しています。これらのデバイスは様々なOTTプラットフォームへのアクセスを提供し、ユーザーはテレビで直接コンテンツをストリーミングできます。

- 北米では消費者の視聴習慣が大きく変化しており、従来のケーブルテレビや衛星テレビサービスに加入せず、OTTサービスを選ぶ人が増えています。OTTプラットフォームの柔軟性、費用対効果、パーソナライズされたコンテンツ提供がこの動向に寄与しています。

- 北米ではスポーツ・ストリーミングの人気が高まっており、主要なスポーツリーグや団体がOTTプラットフォームを立ち上げたり、既存のサービスと提携したりしています。これらのプラットフォームは、スポーツのライブイベントや独占コンテンツ、舞台裏の中継などを提供し、スポーツコンテンツに対する需要の高まりに対応しています。

- コンテンツのローカライゼーションは、北米OTT市場の重要な動向です。プロバイダーは、地域の嗜好や人口統計をターゲットに、その地域に特化したオリジナルコンテンツの制作に投資しています。このアプローチは、加入者の獲得と維持に役立ち、競争の激しい市場でプラットフォームを差別化します。

オーバーザトップ(OTT)業界の概要

オーバーザトップ(OTT)市場は細分化されています。多くのメディア企業やコンテンツ企業がストリーミングTVの流行に乗り、マーケットプレースの競争は激化しており、視聴者を飽きさせない質の高いコンテンツを求める競争はさらに激化しています。各社は消費者の注目を集めるため、製品のイノベーションに注力しています。市場の主要企業は、Netflix Inc.、Amazon.com Inc.(プライム・ビデオ)、The Walt Disney Company(Hulu)、Tencent Holdings Ltd.、Roku Inc.です。同市場のプレーヤーは、製品ラインナップを強化し、持続可能な競争優位性を獲得するために、提携や買収などの戦略を採用しています。

- 2024年2月- メディアとエンターテインメントの複合企業であるShemaroo Entertainmentは、OTTプラットフォームであるShemarooMeを拡大するため、国際的な通信事業者4社と提携しました。Zain、STC、サウジアラビアのMobily、カタールのVodafoneとの提携は、DCB(Direct Carrier Billing)パートナーである3A netとone97 communicationsによって促進され、多様なエンターテインメント体験を提供するという同社の世界なコミットメントを示すものです。

- 2024年2月- ベリマトリックスは、クラウドベースのOTTコンテンツ・セキュリティ・プラットフォーム「Streamkeeper Multi-DRM」の拡張性、可用性、使いやすさをさらに高めるため、アマゾンウェブサービス(AWS)と提携。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- エコシステム分析

- 業界の魅力度-ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場力学

- 市場促進要因

- スマートデバイスの普及と高速インターネットへのアクセスの拡大

- OTTプロバイダー間の競争激化と相まって、スポーツ・娯楽サービスの競合化が進行中

- 新興市場におけるSVOD(定額制サービス)の普及拡大

- 市場抑制要因

- ビデオ・コンテンツの違法コピーの脅威とスパイウェアによるユーザー・データベースのセキュリティ脅威の増大

- マクロ経済要因がOTTおよびTV業界に与える影響

第6章 市場セグメンテーション

- サービスタイプ別

- SVOD

- TVOD

- AVOD

- 地域別

- 北米

- 欧州

- アジア

- オーストラリア・ニュージーランド

- ラテンアメリカ

- 中東・アフリカ

第7章 競合情勢

- 企業プロファイル

- Netflix Inc.

- Amazon.com Inc.(Prime Video)

- The Walt Disney Company(Hulu)

- Tencent Holdings Ltd

- Roku Inc.

- Google LLC(YouTube)

- DAZN Group Limited

- NBC Universal(Hayu)

- PCCW Media Group(Viu)

第8章 投資分析

第9章 市場の将来

The Over The Top Market size is estimated at USD 0.70 trillion in 2025, and is expected to reach USD 1.47 trillion by 2030, at a CAGR of 16.14% during the forecast period (2025-2030).

The over-the-top (OTT) market refers to delivering video, audio, and other media content over the internet directly to users, bypassing traditional distribution channels like cable or satellite television. OTT platforms provide on-demand access to a wide range of content, including movies, TV shows, live events, and original programming.

Key Highlights

- Over-the-top (OTT) is a film and television content platform provided via a high-speed internet connection instead of a cable or satellite provider-based platform. OTT adoption has significantly aided the video, music, podcast, and audio streaming category. Increasing adoption may be attributed to narrow genre choices, packaging flexibility, wider device availability, internet penetration, and lower costs. The rising demand for customized content led to significant adoption rates of OTT devices.

- The ongoing shift toward commoditizing sporting and entertainment services and growing competition among OTT providers are expected to drive the over-the-top (OTT) market. In recent years, there has been a significant shift in how sporting events and entertainment content are consumed. Traditionally, these services were primarily delivered through cable and satellite TV subscriptions, with limited options for customization and on-demand viewing. However, the rise of OTT platforms has disrupted this model by offering a wide range of sporting events, live broadcasts, and entertainment content directly to consumers.

- The increasing adoption of Subscription Video on Demand (SVOD) services in emerging markets is expected to drive the over-the-top (OTT) market. Due to several factors, SVOD services have gained significant popularity worldwide, including in emerging markets. The expanding middle class and rising disposable incomes in many emerging economies have contributed to the growth of SVOD services. As more individuals have the financial means to afford subscriptions, there is an increased demand for access to a wide variety of content through OTT platforms.

- Video content piracy is a significant issue affecting the OTT market. Piracy involves the unauthorized distribution and consumption of copyrighted content, leading to revenue losses for content creators and legitimate streaming platforms. It undermines the business models of OTT providers, who rely on subscription fees or advertising revenue to sustain their operations and fund content creation.

- The COVID-19 pandemic significantly impacted the over-the-top (OTT) market. The global health crisis and associated lockdown measures led to a surge in demand for streaming services and accelerated the growth of the OTT industry in several ways. With people staying at home due to restrictions and seeking entertainment options, the demand for streaming services skyrocketed. Many individuals turned to OTT platforms for movies, TV shows, documentaries, and other forms of content. This surge in demand resulted in a significant increase in subscriptions for established streaming services and the launch of new platforms.

Over the Top (OTT) Market Trends

Adoption of Smart Devices and higher Internet Speeds is Expected to Drive Over the Top (OTT) Market

- The growth in the adoption of smart devices and greater access to higher internet speeds are key factors driving the growth of the over-the-top (OTT) market. The increasing penetration of smartphones, tablets, smart TVs, and other connected devices has provided users with more avenues to access OTT services. These devices come equipped with internet connectivity and support streaming applications, making it easier for consumers to watch their favorite shows, movies, and other content on demand.

- The availability of high-speed internet connections, such as broadband and 4G/5G mobile networks, has played a crucial role in enabling seamless streaming experiences. While the increase in Internet users is a worldwide trend, regional variances exist.

- According to Cisco Systems, North America is likely to have the greatest internet adoption rate during the projection period (followed by Western Europe). Still, the Middle East and Africa are expected to increase (10% CAGR from 2018 to 2023). Faster internet speeds allow for smoother playback, reduced buffering times, and the ability to stream high-definition (HD) and ultra-high-definition (UHD) content. This has greatly improved the overall user experience and contributed to the growing popularity of OTT services.

- The combination of smart devices and high-speed internet has also led to increased personalization and convenience. OTT platforms leverage data analytics and recommendation algorithms to understand users' preferences and provide personalized content recommendations. Users may access content whenever and wherever they want, as long as they have an internet connection.

- These factors have fueled the growth of OTT platforms, attracting many subscribers and driving the revenue generated by subscription fees and advertisements. As a result, traditional media companies and broadcasters have recognized the importance of OTT and have launched their streaming services or partnered with existing OTT platforms to tap into this expanding market.

North America is Expected to Hold the Significant Market Share

- The North American OTT market has witnessed significant growth in recent years. North America is home to some of the most prominent and established OTT platforms, including Netflix, Amazon Prime Video, Hulu, and Disney+. These platforms have gained a large subscriber base and offer a vast content library, including movies, TV shows, documentaries, and original productions.

- Streaming devices, such as Roku, Apple TV, Amazon Fire TV, and Google Chromecast, have seen widespread adoption in North America. These devices provide access to various OTT platforms and allow users to stream content directly on their TVs.

- North America has experienced a significant shift in consumer viewing habits, with an increasing number of individuals opting for OTT services and not subscribing to traditional cable or satellite TV services. OTT platforms' flexibility, cost-effectiveness, and personalized content offerings have contributed to this trend.

- Sports streaming has gained traction in North America, with major sports leagues and organizations launching their OTT platforms or partnering with existing services. These platforms offer live sports events, exclusive content, and behind-the-scenes coverage to cater to the growing demand for sports content.

- Localization of content is a significant trend in the North American OTT market. Providers invest in original content production specific to the region, targeting local preferences and demographics. This approach helps attract and retain subscribers and differentiate platforms in a competitive market.

Over the Top (OTT) Industry Overview

The over-the-top (OTT) market is fragmented. With many media and content companies jumping on the streaming TV bandwagon, the marketplace is becoming increasingly competitive, creating even more competition for high-quality content to keep viewers hooked. The companies are focusing on product innovation to gain consumer attention. Major players in the market are Netflix Inc., Amazon.com Inc.(Prime Video), The Walt Disney Company (Hulu), Tencent Holdings Ltd, and Roku Inc. Players in the market are adopting strategies such as partnerships and acquisitions to enhance their product offerings and gain sustainable competitive advantage.

- February 2024 - Shemaroo Entertainment, a media and entertainment conglomerate, collaborated with four international telecom operators to expand its OTT platform, ShemarooMe. This partnership with Zain, STC, Mobily in Saudi Arabia, and Vodafone in Qatar, facilitated by DCB (Direct Carrier Billing) partners, 3A net, and one97 communications, showcases the company's global commitment to offering diverse entertainment experiences.

- February 2024 - Verimatrix collaborated with Amazon Web Services (AWS) to further increase scalability, availability, and ease of use for its Streamkeeper Multi-DRM cloud-based OTT content security platform.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Ecosystem Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Threat of New Entrants

- 4.3.2 Bargaining Power of Buyers

- 4.3.3 Bargaining Power of Suppliers

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Adoption of Smart Devices and Greater Access to Higher Internet Speeds

- 5.1.2 Ongoing Shift Towards Commoditization of Sporting and Entertainment Services Coupled with Growing Competition Among OTT Providers

- 5.1.3 Increasing Adoption of SVOD (Subscription - Based Services) in Emerging Markets

- 5.2 Market Restraints

- 5.2.1 Growing Threat of Video Content Piracy and Security Threat of User Database Due to Spyware

- 5.3 Impact of Macro Economic Factors on the OTT and TV industry

6 MARKET SEGMENTATION

- 6.1 By Type of Service

- 6.1.1 SVOD

- 6.1.2 TVOD

- 6.1.3 AVOD

- 6.2 By Geography

- 6.2.1 North America

- 6.2.2 Europe

- 6.2.3 Asia

- 6.2.4 Australia and New Zealand

- 6.2.5 Latin America

- 6.2.6 Middle East & Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Netflix Inc.

- 7.1.2 Amazon.com Inc. (Prime Video)

- 7.1.3 The Walt Disney Company (Hulu)

- 7.1.4 Tencent Holdings Ltd

- 7.1.5 Roku Inc.

- 7.1.6 Google LLC (YouTube)

- 7.1.7 DAZN Group Limited

- 7.1.8 NBC Universal (Hayu)

- 7.1.9 PCCW Media Group (Viu)

8 INVESTMENT ANALYSIS

9 FUTURE OF THE MARKET