米国のOTT:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)

US OTT - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 100 Pages

- 納期

- 2~3営業日

- 商品コード

- 1644431

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

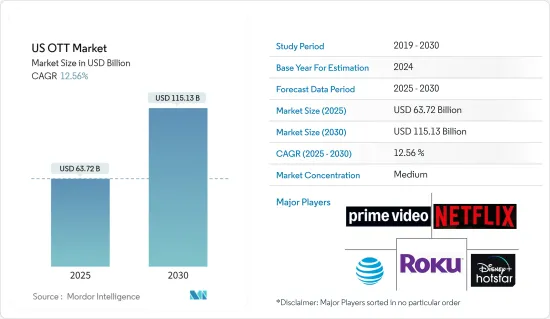

米国のOTT市場規模は2025年に637億2,000万米ドルと推定され、予測期間(2025-2030年)のCAGRは12.56%で、2030年には1,151億3,000万米ドルに達すると予測されています。

米国は世界最大級のOTT市場です。スマートTVやスマートフォンなどのスマートデバイスの普及率の高さ、VODコンテンツへの需要の高まり、ユーザーごとの決済率の高さなどが、同国のOTT市場を牽引する主な要因となっています。NetflixやAmazonのような世界のトップOTTベンダーのほとんどは米国に拠点を置いており、この地域市場に優位性をもたらしています。

主なハイライト

- OTTコンテンツへの注目が高まるにつれ、米国市民はケーブル、地理的制限、放送スケジュールから解放され、ビデオの販売、制作、消費方法を根本的に変えることができます。そのため、ジャンルのカスタマイズ、パッケージの柔軟性、幅広いデバイスの利用可能性、インターネットの普及、低コストに起因する採用が増加しています。NetflixとAmazonは、国内で最も多く加入しているOTTプラットフォームです。

- 収益数の増加に伴い、OTTビデオコンテンツへの視聴時間の割合が急増していることは、ストリーミングの成長を反映しており、国内のエンターテインメントの状況を変えつつあります。Uscreenによると、視聴者は米国で週に平均21時間コンテンツを消費しており、これは2024年にデジタルメディアをストリーミングするアルバイトに相当します。注目すべきは、コンテンツの65%がウェブブラウザではなく、モバイルやTVアプリ経由で消費されていることです。

- しかし、OTTプロバイダーにとっては、消費量の増加に伴ってコストも上昇し、採用するコンテンツ配信ネットワーク・モデルによってサービスの影響度は異なります。通常、CDNサービスは配信されたコンテンツに対して課金されるため、OTTの視聴量が増えれば、OTTプロバイダーの配信コストも増えます。

- さらに、テレビの視聴時間が増加し、人々はテレビコンテンツをオンラインで視聴することに慣れてきています。このため、短期的にはプラス成長の見通しです。ベンダー面では、米国の無料ストリーミング・サービス会社Pluto TVを背景に、D2C(Direct to Consumer)サービスを提供するViacomが重要なベンダーです。

米国のOTT市場動向

スマートTVの高普及で大幅成長

- この地域では、ディズニーのようなコンテンツ所有者が消費者、通信事業者(AT&T)、アマゾンのようなOTT専業事業者などに直接ストリーミング・コンテンツを提供する動きが活発化しています。同時に、ストリーミングのための4Kの出現は、スマートテレビのフォーマット全体で利用できるようにするためにOTTコンテンツの成長を推進しています。

- ストリーミングデバイスの一貫した利用成長、インターネット普及率の増加、スマートTVの需要は、メディア企業がオーバー・ザ・トップ(OTT)業界に参入する有利な機会を提供しています。複数のテレビメーカーが革新的なスマートテレビを発表しています。

- 例えば、ソニー・エレクトロニクスは2023年3月、コグニティブ・プロセッサーXRを搭載し、ホームエンタテインメント体験を提供する2023年BRAVIA XR TVラインアップを発表しました。同社は、いくつかの新しいブラビアXRラインアップを発表した:X95L、X93L Mini LED、X90L Full Array LED、A95L QD-OLED、A80L OLEDです。すべてのモデルは、映画、ゲーム、ストリーミングアプリなどの視聴において没入感を生み出す技術が統合されています。

- コンテンツ消費の観点から、消費者の視聴形態は変化しています。従来のテレビ視聴よりもオンライン消費の方が伸びています。市場を牽引する主な要因は、手頃な価格で利用できる加入プランの柔軟性です。消費者は、地下室でスマートTVを使ってホームシアター体験を演出することで、ホームエンターテインメントへの関心を高めています。さらに、コンテンツジャンルの多様性、快適さ、自由度、時間の柔軟性が市場の成長を後押ししています。

- コンテンツ制作者は、Netflixと提携し、このプラットフォームで独占的にコンテンツを提供しています。例えば、2023年、ペリーとネットフリックスはクリエイティブ・パートナーシップを締結し、ペリーは複数年契約の下、長編映画の脚本、監督、制作に貢献しました。ネットフリックスによると、米国とカナダにおけるストリーミング・プラットフォームの有料加入者数は、2024年第1四半期に8,266万人を占め、同プラットフォームの人気を示しています。多くのプロデューサーがNetflixと協力し、統合された機能を使ってより多くの収益を上げています。

SVoDセグメントが大きな市場シェアを握る

- サブスクリプション・ビデオ・オン・デマンド(SVoD)は、従来のTVパッケージと似ており、ユーザーは月額定額料金で好きなだけコンテンツを視聴できます。主なサービスには、Sky(傘下のNow TVも)、Amazon Prime Video、Netflix、Huluなどがあります。

- 米国を拠点とする6大プラットフォーム、すなわちNetflix、Amazon、Disney+、Paramount+、Apple TV+、HBOがSVoDを支配しています。SVoDプラットフォームの出現は、より多くの消費者を惹きつけることにも貢献しています。米国のSVoD契約数は、今後5年間で大きく伸びると予測されています。

- 米国のOTT市場におけるSVoDセグメントは、重要なセグメントの一つです。2025年までに、500万人以上の有料加入者を持つプラットフォームが12社になると予想されており、米国市場が世界のその他の地域と比較していかに先行しているかがわかる。Amazon、Netflix、Huluのような既存のプレーヤーは、Disney+、Peacock、CBS All Accessのような若いライバルとの激しい競争により、成長に影響を受けると思われます。

- Media Playのデータによると、SVoDは2023年に525億米ドルの貢献をしており、2029年には546億米ドルに達すると予想されています。市場の主要企業は、より多くの顧客を獲得するために、より安価な加入プランを提供しています。コンテンツの多様性、柔軟性、没入型体験、提供される地域コンテンツなどを特徴とするOTTプラットフォームは、市場の成長を促進する主な要因です。

米国のOTT産業の概要

米国のOTT市場は、参入企業の増加により競争企業間の敵対関係が激化しており、徐々に市場の統合が進んでいます。主要な市場プレーヤーは、M&Aを含む市場シェア拡大のための様々な戦略に取り組んでいます。さらに、テレビ放送局はアプリを発表するか、別のOTTプラットフォームに投資することで市場に参入しています。最終的には、今後数年間で、ほとんどのテレビケーブル事業者は、業界におけるプレゼンスを確立するために、これらのビジネスモデルに投資すると予想されます。

- 2024年4月:ロクはトレードデスク、アイスポット、NBCユニバーサルとの提携を発表。この提携は、プログラマティック・バイイングや計測の容易さなど、コネクテッド・テレビが直面する問題を解決することを目的としています。さらに、NBCUniversalとの提携により、2024年パリ・オリンピックのハイライトをRokuプラットフォームで提供します。トレードデスクとの提携により、独立したデマンド・サイド・プラットフォーム(DSP)がRokuの在庫データにアクセスできるようになり、メディアバイヤーはより精度の高い視聴者ターゲティングができるようになります。

- 2024年3月ウォルト・ディズニーは、米国でディズニー・バンドル加入者向けにHulu on Disney+を開始すると発表。これにより、加入者は何千もの一般的なエンタテインメントタイトルを探索することができ、HuluとDisney+のコンテンツがパーソナライズされた体験とともに提供されます。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 現在の市場シナリオ

- 業界の魅力度-ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 競争企業間の敵対関係

- 代替品の脅威

- COVID-19が業界に与える影響

第5章 市場力学

- 市場促進要因

- スマートTVの高い普及率と大手OTTプロバイダーの存在が、この地域におけるOTT普及の拡大に貢献

- 市場統合によるコラボレーションとパートナーシップの重視

- 市場抑制要因

- データプライバシーとセキュリティへの懸念

第6章 市場セグメンテーション

- タイプ別

- SVoD

- TVoD

- AVoD

第7章 OTT再生市場- ジャンル別

第8章 競合情勢

- 企業プロファイル

- Netflix

- Disney+

- Amazon Prime Video

- Roku

- HBO Max(AT&T Inc.)

- CBS All Acess(Viacomcbs Inc.)

- Sling TV LLC

- Apple Inc.

- YouTube(Google LLC)

第9章 投資分析

第10章 市場の将来

目次

The US OTT Market size is estimated at USD 63.72 billion in 2025, and is expected to reach USD 115.13 billion by 2030, at a CAGR of 12.56% during the forecast period (2025-2030).

The United States is one of the largest OTT markets in the world. The high penetration of smart devices, like smart TVs and smartphones, growing demand for VOD content, and a high rate of per-user payment are some of the major factors driving the country's OTT market. Most of the top global OTT vendors, like Netflix and Amazon, are US-based, providing an advantage to the regional market.

Key Highlights

- The increasing gravitation toward OTT content allows US citizens to get rid of cables, geographic restrictions, and broadcast schedules and fundamentally changes how video is sold, produced, and consumed. Thus, increasing adoption has been attributable to customized genre choices, package flexibility, wider device availability, internet penetration, and lower costs. Netflix and Amazon are the most commonly subscribed OTT platforms in the country.

- With increasing revenue numbers, the surging percentage of viewing time going to OTT video content reflects the streaming growth and is changing the country's entertainment landscape. According to the Uscreen, viewers spend an average of 21 hours per week consuming content in the United States, equivalent to a part-time job streaming digital media in 2024. Notably, 65% of content is consumed via mobile or TV apps rather than web browsers.

- However, some costs for OTT providers also rise along with increased consumption, with services impacted by varying degrees depending on the content delivery network model employed. As the OTT viewing amount increases, so does the OTT provider's delivery cost since CDN services are usually charged for the content delivered.

- Moreover, the hours spent on TV have risen, and people are getting used to watching TV content online. This entails a positive growth outlook on a near-term basis. On the vendor front, Viacom is a significant vendor offering a direct-to-consumer (D2C) service on the back of Pluto TV, the free streaming service company in the United States.

US OTT Market Trends

High Penetration of Smart TV Witnesses Significant Growth

- Streaming content in the region has intensified as content owners like Disney go directly to consumers, telcos (AT&T), and OTT-only operators like Amazon, to name a few. Simultaneously, the emergence of 4K for streaming has propelled OTT content growth to be made available across smart TV formats.

- Consistent growth in streaming device usage, increasing internet penetration, and demand for smart TVs have provided lucrative opportunities for media companies to enter the over-the-top (OTT) industry. Several TV makers are introducing innovative smart TVs.

- For instance, in March 2023, Sony Electronics announced the 2023 BRAVIA XR TV Lineup, equipped with Cognitive Processor XR, for a home entertainment experience. The company launched a few new BRAVIA XR lines: X95L and X93L Mini LED, X90L Full Array LED, A95L QD-OLED, and A80L OLED. All models are integrated with technology to create an immersive experience for watching movies, gaming, streaming apps, and others.

- Consumer viewership is transforming in terms of content consumption. There is more growth in online consumption than traditional TV viewership. Major factors driving the market are the flexibility of subscription plans that are available at affordable prices. Consumers have grown their interest in home entertainment by using Smart TVs in their basement areas to create home theater experiences. Additionally, it allows a diversity of content genres, comfort, freedom, and time flexibility, propelling the market's growth.

- Content producers are partnering with Netflix to feature their content exclusively on the platform. For instance, in 2023, Perry and Netflix signed a creative partnership in which Perry contributed to writing, directing, and producing feature films under a multi-year deal. According to Netflix, the number of subscribers paying for streaming platforms in the United States and Canada accounted for 82.66 million in Q1 2024, which shows the popularity of the platform. Many producers are collaborating with Netflix to generate more revenue using integrated capabilities.

SVoD Segment to Hold Significant Market Share

- Subscription video-on-demand (SVoD) is similar to traditional TV packages, allowing users to consume as much content as they desire at a flat monthly rate. Major services include Sky (also its subsidiary Now TV), Amazon Prime Video, Netflix, and Hulu.

- Six major US-based platforms, namely Netflix, Amazon, Disney+, Paramount+, Apple TV+, and HBO, dominate the SVoD landscape. The emergence of SVoD platforms is also helping to attract more consumers. The number of SVoD subscriptions in the United States is projected to grow significantly in the next five years.

- The SVoD segment in the US OTT market is one of the significant segments. By 2025, the country is expected to witness a dozen platforms with more than 5 million paying subscribers, revealing just how ahead the US market is compared with the rest of the world. Growth for established players such as Amazon, Netflix, and Hulu will be affected due to intense competition from younger rivals such as Disney+, Peacock, and the augmented CBS All Access.

- As per the data by Media Play, SVoD contributed USD 52.5 billion in 2023, which is expected to reach USD 54.6 billion by 2029. Major market players are offering cheaper subscription plans to attract more customers. OTT platforms featuring content diversity, flexibility, immersive experiences, and regional content offered are the major drivers that foster the market's growth.

US OTT Industry Overview

The US OTT market is witnessing increasing competitive rivalry as more companies enter, leading to the gradual consolidation of the market. The major market players are involved in various strategies to expand their market share, including mergers and acquisitions. Moreover, TV broadcasters are entering the market either by launching their app or investing in another OTT platform. Eventually, in the coming years, most TV cable operators are expected to invest in these business models to establish their presence in the industry.

- April 2024: Roku announced a partnership with Trade Desk, iSpot, and NBCUniversal. This alliance aims to solve the problem faced during connected television space, which includes ease of programmatic buying and measurement. Moreover, in collaboration with NBCUniversal, it will provide 2024 Paris Olympics highlights, featuring all available sports for Olympics coverage on the Roku platform. In partnership with the Trade Desk, it facilitates independent Demand Side Platform (DSP) to gain access to Roku data on Roku inventory, which will allow media buyers to target viewers with more precision.

- March 2024: Walt Disney announced the launch of Hulu on Disney+ in the United States for Disney Bundle subscribers, which brought a variety of genres with integrated content libraries. This allowed subscribers to explore thousands of general entertainment titles, bringing Hulu and Disney+ content together with a personalized experience.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Report

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Current Market Scenario

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Intensity of Competitive Rivalry

- 4.2.5 Threat of Substitutes

- 4.3 COVID-19 Impact on the Industry

5 MARKET DYNAMICS

- 5.1 Market drivers

- 5.1.1 High Penetration of Smart TV and the Presence of Major OTT Providers have Contributed to the Growth of OTT Adoption in the Region

- 5.1.2 Market Consolidation to Result in Emphasis on Collaboration and Partnerships

- 5.2 Market Restraints

- 5.2.1 Data Privacy and Security Concerns

6 MARKET SEGMENTATION

- 6.1 By Type

- 6.1.1 SVoD

- 6.1.2 TVoD

- 6.1.3 AVoD

7 OTT PLAYBACK MARKET - BY GENRE

8 COMPETITIVE LANDSCAPE

- 8.1 Company Profiles

- 8.1.1 Netflix

- 8.1.2 Disney+

- 8.1.3 Amazon Prime Video

- 8.1.4 Roku

- 8.1.5 HBO Max (AT&T Inc.)

- 8.1.6 CBS All Acess (Viacomcbs Inc.)

- 8.1.7 Sling TV LLC

- 8.1.8 Apple Inc.

- 8.1.9 YouTube (Google LLC)

9 INVESTMENT ANALYSIS

10 FUTURE OF THE MARKET

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 100 Pages

- 納期

- 2~3営業日