|

市場調査レポート

商品コード

1687398

クラウドゲーム-市場シェア分析、産業動向・統計、成長予測(2025年~2030年)Cloud Gaming - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| クラウドゲーム-市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 119 Pages

納期: 2~3営業日

|

- 全表示

- 概要

- 目次

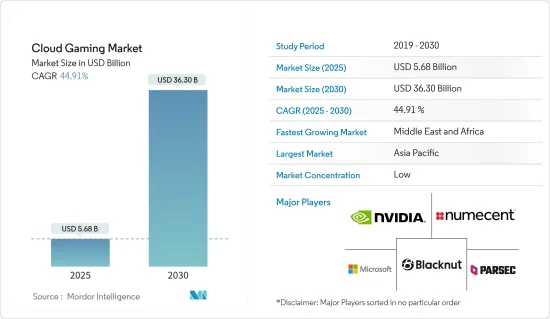

クラウドゲーム市場規模は2025年に56億8,000万米ドルと推計され、予測期間(2025年~2030年)のCAGRは44.91%で、2030年には363億米ドルに達すると予測されます。

市場成長の主な要因は、クラウドコンピューティング、高速インターネット接続、ストリーミング技術、クラウドインフラに関連する政府の取り組みなどの技術的進歩です。

主なハイライト

- 最近の高度なクラウド技術の進歩により、クラウドゲームのアイデアは現実のシナリオになりました。クラウド・ゲーミングは、インタラクティブなゲーム・アプリケーションをクラウド上で遠隔レンダリングし、そのシーンをビデオ・シーケンスとしてインターネット経由でプレイヤーにストリーミング再生します。これは、そうでなければ高品質のゲームを実行することができない、あまり強力でない計算デバイスのための利点です。

- インターネット・ユーザーの増加や、多くのデバイスでストレージの問題がある中、モバイル・デバイスでゲームをプレイする傾向が、市場促進要因として大きいです。クラウドベースのゲームの大きな利点は、スマートフォンやタブレットなど、ほとんどすべてのデバイスからいつでもゲームを利用できることです。また、モバイルクラウドゲームは、ユーザーがOSやデバイスを問わずにゲームをプレイできることから、ゲーム配信のパラダイムとして有望視されています。クラウドゲームでは、ゲームシーンのレンダリング、ゲームロジックの処理、ビデオエンコーディング、ビデオストリーミングなどの計算作業は、(すべてのゲームが保存されている)重要なサーバーが行う。

- さらに、予測期間中の市場成長率を高めるために、製品の発売やコラボレーションが増加していると分析されています。例えば、2023年12月、アップルはApp Storeでゲームをストリーミングするアプリを許可すると発表しました。これは、MicrosoftやNvidiaのようなブランドが、Xbox Cloud GamingやGeForce NowのようなクラウドゲームサービスのネイティブアプリをiPhoneやiPadのApp Storeで発売できることを意味します。新しい方針は世界のものです。

- クラウド・ゲーミング・サービスを採用するには、リアルタイムのゲーム体験が必要です。ゲーマーの期待に応えるスムーズなゲーム体験のためには、高い解像度とフレームレートが低遅延と組み合わされる必要があります。しかし、帯域幅の普及率が低い新興諸国は、クラウドゲームサービスの利用を避け、代わりにオフラインで利用できる従来のゲーミングサービスを利用する態勢をとっているため、クラウドゲームサービスは現在のインターネット技術に阻まれ、ゲーマーの期待に応えるのに苦労しています。

- COVID-19はクラウドゲーム市場に好影響を与えました。閉鎖期間中、クラウドベースのゲームはどのデバイスでも自由にプレイでき、ハードウェアを増やす必要がないため、需要が伸びた。マイクロソフト、Twitch、アクティビジョンといった企業はいずれも、プレイヤーへの投資において新たな高みに到達しました。スマートフォンの普及が進んでいることも、クラウドゲーム市場に貢献した大きな要因の一つです。

クラウドゲーム市場の動向

スマートフォン端末市場が大きな市場シェアを占める見込み

- 世界のインターネット普及率の上昇に支えられたクラウドゲームソリューションの成長が、スマートフォンにおけるクラウドゲーム需要を牽引し、今後の市場成長を後押ししています。例えば、2023年11月、StarHubは、クラウドゲームディストリビューターのCareGameおよびOnMobile Globalと提携し、モバイルゲーマー向けのポータブルゲームカテゴリであるGameHub+Mobile Playに100以上のモバイルゲームタイトルを提供することを発表しており、スマートフォンユーザーのクラウドゲームに対するニーズを示しています。

- さらに、スマートフォンベースのゲームソリューションにより、ゲーマーはクラウドを通じてモバイルゲームを楽しむことができ、パワフルなモバイルハードウェアやダウンロードに必要なストレージ容量が不要になります。さらに、ゲーマーは、超低遅延のスピードで、バタフライ・スムースなグラフィックスを持つAAAタイトルを含む幅広いモバイルゲームをプレイすることができます。

- 世界の5Gモバイルネットワークによる高速インターネットの普及は、スマートフォンの利用台数を増加させ、スマートフォンベースのクラウドゲームのインターネットデータ需要をサポートするネットワーク能力を高め、予測期間中の市場の成長を支えると思われます。例えば、2023年11月に発表されたEricsson Mobility Reportによると、北米の5G契約数は2023年に2億5,231万件に達し、2028年には4億540万件に拡大すると予測されており、より良いモバイル接続のために5Gの拡大傾向が強まっていることが示されており、予測期間中のクラウドベースのモバイルゲーム市場の成長をサポートすると考えられます。

- スマートフォン向けクラウドゲームサービス市場では、通信サービス事業者とクラウドゲームプロバイダーとの間で、クラウドゲームサービスを通信サービスの月額課金にバンドルするための重要な連携が見られ、市場の成長を後押ししています。

- そのため、スマートフォンの普及拡大、各国における5Gサービスへの投資、クラウドゲームプロバイダーと通信サービスプロバイダーとの協業によるスマートフォンベースのクラウドゲームポートフォリオのターゲット層の拡大が、予測期間中の市場成長を後押ししています。

中東・アフリカが大きな成長を牽引

- 中東・アフリカ地域には、サウジアラビア、アラブ首長国連邦、カタール、南アフリカなどの国々が含まれます。中東・アフリカのクラウドゲーム市場は、クラウドゲームにおける5Gの役割の進化、高速インターネットインフラ、新たなクラウド地域の開設によるクラウドインフラの拡大、主要ベンダーによる新たなクラウドゲーム製品の投入の増加などから、主に恩恵を受けています。

- さらに、多くのMENA諸国におけるクラウドコンピューティングインフラの拡大に対する政府の取り組みが、予測期間中のクラウドゲーム市場の成長を促進すると分析されています。例えば、サウジアラビアではクラウドコンピューティングが大幅に増加しています。同国政府は、2030年までに同国をクラウドコンピューティングの地域ハブにすることを目指しています。

- クラウドサービスプロバイダーはその必要性を認識し、この地域でクラウドインフラを拡大しています。例えば、2023年9月、Huawei CloudはHuawei Cloud Summit Saudi Arabia 2023でHuawei Cloud Riyadh Regionの立ち上げを発表しました。このクラウド・リージョンは、王国のデジタル主導の経済成長を促進するのに役立ちます。Huawei Cloud Riyadhの立ち上げは、Huawei Cloudが中東、中央アジア、アフリカへのサービス提供に注力し、安全で革新的、信頼性が高く持続可能なクラウドサービスを提供することになります。

- 世界市場のベンダーは、中東・北アフリカ地域のクラウドゲームエコシステムを開発し、中東・北アフリカ地域のゲーマーからのクラウドゲーム需要の高まりに対応するために、地域の通信プロバイダーと提携しています。

クラウドゲーム産業の概要

クラウドゲーム市場は非常に細分化されており、Nvidia Corporation、Numecent Holdings Ltd.、Blacknut、Microsoft Corporation、Parsec Cloud, Inc.(Unity Software INC.)などの主要企業が存在します。同市場のプレーヤーは、ソリューション提供を強化し、持続可能な競争優位性を獲得するために、提携や買収などの戦略を採用しています。

- 2023年12月-Radian ArcとBlacknutは、マレーシアのコンバージェンス・サービス・プロバイダーであるUnifi向けに新しいクラウドゲームオファーの提供を開始しました。ユニファイ社とのパートナーシップにより、ラジアン・アークはマレーシア国内外における数百万人のプレイヤーのゲーム体験を向上させ続ける。

- 2023年8月-GeForce NOWは、Ultimate KovvaKの課題開始を発表。この発売により、Nvidiaはゲーマーの狙い撃ち上達をサポートします。期間限定のSteam割引で完全発売。KovaaK'sは、GeForce NOWライブラリに加わる20以上の新しいゲームをリードします。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 産業バリューチェーン分析

- 業界の魅力度-ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

- COVID-19の市場への影響評価

第5章 市場力学

- 市場促進要因

- クラウドコンピューティング、高速インターネット接続、ストリーミング技術などの技術進歩

- クラウドインフラに関する政府の取り組みが市場拡大に寄与

- 市場抑制要因

- 低帯域幅の問題が新興国市場の成長を妨げる

- 規制と法的課題

第6章 市場セグメンテーション

- タイプ別

- ビデオストリーミング

- ファイルストリーミング

- デバイス別

- スマートフォン

- ゲーム機

- パソコン

- モバイル機器

- その他

- ゲーマータイプ別

- カジュアルゲーマー

- 熱心なゲーマー

- ライフスタイルゲーマー

- 地域別

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- その他の欧州

- アジア太平洋

- 中国

- 日本

- インド

- その他のアジア太平洋

- ラテンアメリカ

- 中東・アフリカ

- 北米

第7章 競合情勢

- 企業プロファイル

- Nvidia Corporation

- Numecent Holdings Ltd.

- Blacknut

- Microsoft Corporation

- Parsec Cloud Inc.(Unity Software Inc.)

- Tencent Holdings Limited

- Utomik BV

- Antplay.tech

- UBITUS KK

- Shadow SAS

第8章 投資分析

第9章 市場の将来

The Cloud Gaming Market size is estimated at USD 5.68 billion in 2025, and is expected to reach USD 36.30 billion by 2030, at a CAGR of 44.91% during the forecast period (2025-2030).

The market's growth is majorly attributed to technological advancements, such as cloud computing, high-speed internet connectivity, streaming technology, and government initiatives related to cloud infrastructure.

Key Highlights

- The recent advancement in advanced cloud technology has turned the idea of cloud gaming into a real scenario. Cloud gaming renders the interactive gaming application remotely in the cloud and then streams the scenes as a video sequence back to the player over the internet. This is the advantage for less-powerful computational devices that are otherwise incapable of running high-quality games.

- The growing number of internet users and the tendency to play games on mobile devices with storage issues in many devices are major drivers for the market. A significant advantage of cloud-based gaming is that games are available anytime from almost any device, such as smartphones and tablets. Also, mobile cloud gaming is a promising paradigm for gaming delivery, as users can play games on any OS or device. In cloud gaming, the vital server (where all the games are stored) does the computation work, including game scene rendering, game logic processing, video encoding, and video streaming.

- Further, the growing product launches and collaborations are analyzed to bolster the market growth rate during the forecast period. For instance, in December 2023, Apple announced it would now allow apps to stream games on its App Store. It means that brands like Microsoft and Nvidia can launch native apps for their cloud gaming services, such as Xbox Cloud Gaming and GeForce Now, on the App Store for iPhone and iPad. The new policy is global.

- A real-time gaming experience is required to adopt cloud gaming services. A high resolution and frame rate should be paired with low latency for a smooth gaming experience that meets gamers' expectations. However, cloud gaming services are held back by current internet technology and struggle to live up to gamers' expectations because developing countries with low bandwidth penetration are poised to avoid the usage of cloud gaming services and instead go with traditional gaming offers offline use.

- The COVID-19 had a positive impact on the cloud gaming market. During the lockdown, demand for cloud-based games grew as they were free to play on any device and did not need more hardware. Companies like Microsoft, Twitch, and Activision have all reached new heights in player investment. The growing smartphone penetration is one of the significant factors that have contributed to the cloud gaming market.

Cloud Gaming Market Trends

Smartphones Devices Market is Expected to Hold Significant Market Share

- The growth of cloud gaming solutions supported by the increasing Internet penetration rate worldwide is driving the demand for cloud games in Smartphones, fueling the market growth in the future. For instance, in November 2023, StarHub announced partnerships with cloud gaming distributors CareGame and OnMobile Global to bring over 100 mobile game titles to GameHub+ Mobile Play, a portable gaming category catered to mobile gamers, showing the need for cloud gaming for smartphone users.

- Additionally, smartphone-based gaming solutions enable gamers to enjoy mobile games by steaming them through the cloud, eliminating the need for powerful mobile hardware and storage space needed to download. Furthermore, gamers would be able to play a wide selection of mobile games, including AAA titles with buttery smooth graphics at ultra-low latency speeds, which shows the benefit of cloud gaming for smartphone users, which would fuel the market growth potential in the future.

- The growth of High-speed Internet through 5G mobile networks worldwide would raise the number of smartphone usage and their network capability to support the internet data demand for smartphone-based cloud gaming in the market, supporting the market's growth during the forecast period. For instance, in November 2023, the Ericsson Mobility Report stated that the 5G subscriptions in North America were expected to reach 252.31million in 2023 and are estimated to grow to 405.40 million by 2028, showing the increasing trend of 5G expansion for better mobile connectivity, which would support the growth of cloud-based mobile gaming market during the forecast period.

- The cloud gaming service market for smartphones is witnessing a significant collaboration among the telecom services providers and the cloud gaming providers to bundle their cloud gaming offerings in the telecom services' monthly billing, fueling the market's growth.

- Therefore, the growth of smartphone penetration, the investments in the 5G services in the countries., and the collaborations of cloud-based game providers with the telecom service providers to increase the target audiences of their smartphone-based cloud gaming portfolio are fueling the market growth during the forecast period.

Middle East and Africa to Witness Major Growth

- The Middle East and Africa region includes countries like Saudi Arabia, the United Arab Emirates, Qatar, and South Africa. The Middle East and Africa, cloud gaming market, is mainly benefitting from the evolving role of 5G in cloud gaming, high-speed internet infrastructure, expanding cloud infrastructure with the opening of new cloud regions, and growth in launches of new cloud gaming offerings by major market vendors.

- Further, government initiatives in many MENA countries to expand cloud computing infrastructure are analyzed to drive the growth of the cloud gaming market over the forecast period. For instance, Saudi Arabia is witnessing a significant increase in cloud computing. The country's government aims to make the Kingdom a regional hub for cloud computing by 2030.

- Cloud service providers are recognizing the need and expanding their cloud infrastructure in the region, thus positively elevating the growth of effective video streaming in the studied market. For instance, in September 2023, Huawei Cloud announced the launch of the Huawei Cloud Riyadh Region at the Huawei Cloud Summit Saudi Arabia 2023. This cloud Region will help promote digital-led economic growth in the Kingdom. The launch of the Huawei Cloud Riyadh will be Huawei Cloud's focus on serving the Middle East, Central Asia, and Africa, providing secure, innovative, reliable, and sustainable cloud services.

- Global market vendors are partnering with regional telecom providers to develop the MENA Cloud Gaming ecosystem and cater to the growing demand for cloud gaming from gamers across the region.

Cloud Gaming Industry Overview

The cloud gaming market is highly fragmented, with major players like Nvidia Corporation, Numecent Holdings Ltd., Blacknut, Microsoft Corporation, and Parsec Cloud, Inc. (Unity Software INC.). Players in the market are adopting strategies such as partnerships and acquisitions to enhance their solution offerings and gain sustainable competitive advantage.

- December 2023 - Radian Arc & Blacknut launched a new cloud gaming offer for Malaysian Convergence Services Provider Unifi. Through this partnership with Unifi, Radian Arc will continue to improve the gaming experiences of millions of players in Malaysia and beyond.

- August 2023 - GeForce NOW announced the launch of Ultimate KovvaK's challenge. With this launch, Nvidia helps gamers to improve their aim. It fully launches with a limited-time Steam discount. KovaaK's leads over 20 new games joining the GeForce NOW library.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Buyers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Assessment of Impact of COVID-19 on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Technological Advancements, Such as Cloud Computing, High-speed Internet Connectivity, and Streaming Technology

- 5.1.2 Government Initiatives Related to Cloud Infrastructure will Help in Market Expansion

- 5.2 Market Restraints

- 5.2.1 Low Bandwidth Issues is Hindering the Market Growth in Developing Countries

- 5.2.2 Regulatory and Legal Challenges

6 MARKET SEGMENTATION

- 6.1 By Type

- 6.1.1 Video Streaming

- 6.1.2 File Streaming

- 6.2 By Device

- 6.2.1 Smartphones

- 6.2.2 Gaming Consoles

- 6.2.3 PC

- 6.2.4 Mobile Devices

- 6.2.5 Others

- 6.3 By Gamer Type

- 6.3.1 Casual Gamers

- 6.3.2 Avid Gamers

- 6.3.3 Lifestyle Gamers

- 6.4 By Geography

- 6.4.1 North America

- 6.4.1.1 United States

- 6.4.1.2 Canada

- 6.4.2 Europe

- 6.4.2.1 Germany

- 6.4.2.2 United Kingdom

- 6.4.2.3 France

- 6.4.2.4 Italy

- 6.4.2.5 Rest of Europe

- 6.4.3 Asia-Pacific

- 6.4.3.1 China

- 6.4.3.2 Japan

- 6.4.3.3 India

- 6.4.3.4 Rest of Asia-Pacific

- 6.4.4 Latin America

- 6.4.5 Middle East and Africa

- 6.4.1 North America

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Nvidia Corporation

- 7.1.2 Numecent Holdings Ltd.

- 7.1.3 Blacknut

- 7.1.4 Microsoft Corporation

- 7.1.5 Parsec Cloud Inc. (Unity Software Inc.)

- 7.1.6 Tencent Holdings Limited

- 7.1.7 Utomik BV

- 7.1.8 Antplay.tech

- 7.1.9 UBITUS KK

- 7.1.10 Shadow SAS

8 INVESTMENT ANALYSIS

9 FUTURE OF THE MARKET