|

市場調査レポート

商品コード

1906976

ペクチン:市場シェア分析、業界動向と統計、成長予測(2026年~2031年)Pectin - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| ペクチン:市場シェア分析、業界動向と統計、成長予測(2026年~2031年) |

|

出版日: 2026年01月12日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

概要

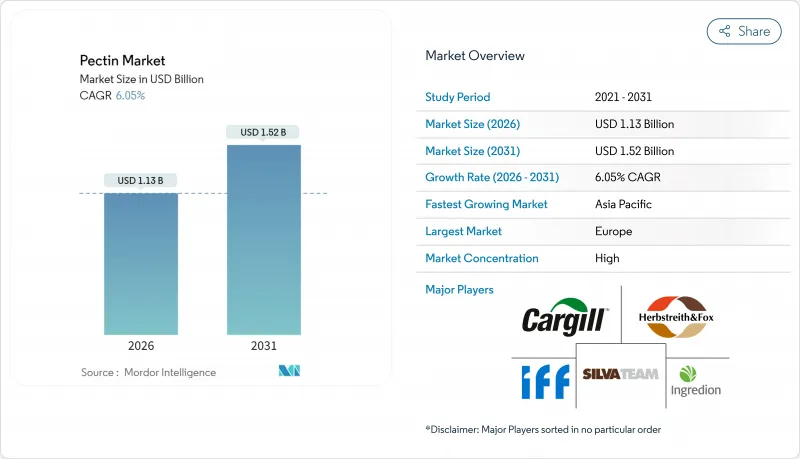

ペクチン市場は、2025年の10億7,000万米ドルから2026年には11億3,000万米ドルへ成長し、2026年から2031年にかけてCAGR6.05%で推移し、2031年までに15億2,000万米ドルに達すると予測されています。

合成水溶性多糖類に対する規制圧力が強まる一方、認知度の高い原料への需要が急増しております。さらに、これらの原料の機能性用途が医薬品や包装分野で拡大しており、市場の着実な成長を牽引しております。優れたゲル化特性で知られる柑橘由来ペクチンは、依然としてトップシェアを維持しております。しかしながら、ブラジルの柑橘類生産量が24%減少したことに加え、プランテーションの40%に影響を及ぼす緑化病(グレーニング病)により、この原料の供給が逼迫し、価格上昇を招いております。欧州では、リサイクル可能な包装材に関する厳格な規制が推進力となり、天然ポリマーへの投資を促進しております。これらの規制は、メーカーが持続可能な代替品を探求することを促し、欧州の市場における地位をさらに確固たるものとしております。一方、アジア太平洋地域では7.19%のCAGRを記録し、最も急速な需要拡大が見られます。この急増の一因は、中国が草案規制においてペクチンベースのキャンディー、飲料、チョコレートを承認したことにあり、これにより同地域のメーカーに新たな機会が開かれると予想されます。医薬品分野では、3Dバイオプリンティングと個別化医療が有望な分野として台頭しています。生体適合性で高く評価されるペクチンハイドロゲルは、薬物送達システムや組織工学システムにおいてニッチ市場を開拓し、先進的な医療用途に向けた革新的なソリューションを提供しています。

世界のペクチン市場動向と洞察

天然由来・クリーンラベル原料への需要

消費者が原材料表示を厳しくチェックする中、メーカーは人工増粘剤をペクチンに置き換えています。ペクチンはGRAS(一般に安全と認められる)ステータスを有し、食物繊維の利点も兼ね備えています。柑橘類やリンゴなどの天然由来のペクチンは、クリーンラベル製品への需要の高まりに合致し、食品配合における食感や安定性の向上といった機能的利点を提供します。米国FDAが天然着色添加物を環境アセスメント対象から除外した決定は、植物由来原料への明確な支持を示しており、天然原料の使用をさらに促進しています。欧州では小売業者が「フリーフロム」表示を棚に掲げ、ペクチンなどの認知度の高い水溶性食物繊維を優先しています。この動向を受け、加工業者は環境意識の高い消費者の共感を得るとともに規制要件にも合致する、トレーサビリティと持続可能な調達を特徴とするペクチンへの投資を拡大しています。さらに、包括的なサプライチェーン監査を実施・公表するブランドオーナーは、商品回転率の向上を実感しており、透明性、持続可能性、倫理的な調達慣行を優先するサプライヤーにとっての商業的優位性が浮き彫りとなっています。

包装食品の消費拡大

アジア太平洋地域における都市化の進展と共働き世帯の増加に伴い、利便性・手頃な価格・長期保存性を備えた常温保存食品への依存度が高まっています。植物細胞壁由来の天然多糖類であるペクチンは、粘度向上・口当たり改善・水分保持効果から食品用途で広く活用されています。ペクチンは、合成安定剤に頼ることなく、分量管理された包装が長期の物流サイクルに耐えられるよう保証することで、ソース、デザート、レトルト食品において極めて重要な役割を果たします。この機能性により、ペクチンは高品質で長期保存可能な食品の製造に不可欠な原料となっており、特に物流上の課題や多様な消費者嗜好が顕著な地域においてその重要性は高まっています。世界の品質基準を維持しつつ地域の嗜好に応えるため、クラフト・ハインツなどの多国籍大手企業はシンガポールに地域イノベーション拠点を設立しています。これらのセンターでは、地域の嗜好に合わせたレシピ開発に注力し、現地の知見を活用して消費者に支持される製品を創出しています。この戦略的アプローチにより、ペクチンの地域契約量が大幅に増加し、市場での需要をさらに促進するとともに、進化する食品業界の業界情勢におけるその役割を確固たるものにしています。

低コスト合成ハイドロコロイドの普及

価格に敏感な経済圏における大衆向け食品ブランドは、化学的に製造された増粘剤(加工澱粉やカルボキシメチルセルロースなど)への関心を高めています。これらは固形分ベースでペクチンより35%低価格であることが多く、製品機能性を損なわずに製造コスト削減を目指すメーカーにとって費用対効果の高い解決策を提供します。クリーンラベルの主張が後回しにされる場合、調達担当者は代替品の採用を優先する動向があり、特定のベーカリー製品や乳製品におけるペクチンの採用が制限される可能性があります。この動向は、特にコスト意識が天然素材への消費者需要を上回る地域において、ペクチンの普及にとって課題となっています。これに対応し、主要ペクチン供給業者は現在、配合量の最適化、製品性能の向上、コスト差の解消を目的とした技術サービスパッケージを提供しております。これらのサービスパッケージには、配合設計支援、応用試験、コスト削減戦略などが含まれることが多く、製造業者が望ましい製品品質を達成しつつ、費用を効果的に管理することを可能にしております。

セグメント分析

2025年現在、柑橘由来ペクチンは市場シェアの84.48%を占め、圧倒的な優位性を示しております。この強固な地位は、柑橘原料を支える充実した加工インフラと、多様な用途で求められる優れたゲル化特性に裏打ちされたものです。しかしながら、ブラジル産柑橘類の果皮供給には課題が迫っており、供給不足や病害の脅威に直面しているため、少なくとも2027年までは価格が高止まりする見込みです。こうした状況を受け、欧州の主要加工業者は転換を図り、原料基盤を拡大するため複数原料対応の加工ラインへの投資を進めています。供給業者も同様に、ヒマワリやテンサイパルプなどの代替原料に目を向けるなど、調達範囲を拡大しています。これらの動きは地域の廃棄物有効利用政策への対応を目的としていますが、柑橘ペクチンのゲル強度を再現するには技術的な課題が残されています。供給安定性が最優先課題となる中、ブランドオーナーは統合ジュース企業と複数年契約を締結し、皮原料の安定供給を確保しています。

一方、リンゴ由来ペクチンの需要は成長軌道にあり、CAGR6.38%が見込まれています。この急成長は主に、柑橘類不足の懸念から信頼性の高い代替原料を求める菓子類・乳製品業界の需要に支えられています。超音波抽出法をはじめとする抽出技術の革新が、リンゴペクチンの競争優位性を高めています。こうした進歩は主に中国とトルコで顕著であり、抽出収量を向上させるだけでなく、溶剤消費量を最大30%削減し、持続可能性と費用対効果の両方を強化しています。こうした進展により、リンゴ由来ペクチンはかつて柑橘系ペクチンが支配していた分野でより激しく競争できるようになりました。本質的に、リンゴ由来セグメントの急成長は、供給の安定性と機能性・環境配慮特性を両立させるという購買者の嗜好におけるパラダイムシフトを浮き彫りにしています。

2025年現在、総収益の58.35%を占める高メトキシルペクチンが市場を独占しており、これは主に高糖度保存食品や製菓用フィリングにおける不可欠な役割によるものです。このセグメントの優位性は、糖分環境下でのゲル化を必要とする製品における高メトキシルペクチンの普及に由来します。同ペクチンは強固で安定したゲルを形成する能力に優れており、伝統的なジャムやフィリングのレシピにおける長年の使用実績が、安定した需要と顕著な市場収益を保証しています。保存食品において望ましい食感と保存期間を実現する上で高メトキシルペクチンの果たす重要な役割は、特にこれらの特性を重視する市場において、その代替不可能性を強調しています。さらに、製造業者は、より複雑なペクチン品種と比較した場合、その比較的シンプルな加工要件に利点を見出しています。総合的に見て、高メトキシルペクチンの市場における重要な存在感は、伝統的な食品分野におけるその重要な役割を裏付けています。

一方、低メトキシルペクチンはペクチン市場で最も成長が著しいセグメントであり、2031年までに6.42%の予測CAGRを示し、市場全体の成長率を上回ると見込まれています。この急成長は、低糖質・低カロリー製品の需要増加に加え、医薬品や栄養補助食品分野での利用関心の高まりに起因しています。低メトキシルペクチンは、カルシウム誘導型架橋反応により低糖環境下でもゲル化できる特異的な能力を有しており、低糖ジャムなどの健康志向製品における最適な選択肢として位置づけられています。こうしたジャムの市場規模は2025年に2億6,400万米ドルに達し、年間成長率7.4%が見込まれています。しかしながら、低メトキシルペクチンの加工にはpH値とカルシウム濃度の厳密な管理が求められ、高度なイオンモニタリング装置を持たない小規模生産者にとっては課題となります。本セグメントはまた、スクロース不使用で理想的な食感を実現する栄養補助食品用グミや、タンパク質変性のリスクなく繊細な生物活性物質のカプセル化を可能とする医薬品分野でも優れた性能を発揮します。こうした先駆的な応用が、市場の急速な成長に大きく寄与しています。

地域別分析

2025年、欧州はジャムや乳製品における豊かな伝統、ならびに再生可能包装を推進する政策イニシアチブに支えられ、売上高の29.60%という大きなシェアを占めました。スペインの柑橘類の皮加工業者に近い立地を活かすドイツとフランスは、地域全体の生産量の3分の2を占めています。同地域の強力な柑橘類の皮加工インフラと持続可能性への注力が、市場における地位をさらに強化しています。一方、使い捨てプラスチック指令はペクチンフィルム複合材の研究開発助成を促進し、現地サプライヤーを天然包装分野の先駆者として位置づけています。この指令はイノベーションを奨励するだけでなく、欧州サプライヤーに世界市場での競争優位性をもたらしています。

アジア太平洋地域は2026年から2031年にかけてCAGR7.03%を記録する見込みです。健康食品の品揃えを拡大する中国が、この需要急増の主因となっています。同国における健康志向製品の重視と中産階級人口の増加が、この成長を支える主要因です。一方、インド食品安全基準局によるビタミンガミー規制の国際基準への整合化に伴い、グジャラート州およびマハラシュトラ州の受託製造業者では連続式ペクチン・ゼリー調理装置への投資が進んでいます。これらの投資により生産効率が向上し、ペクチン系製品への需要増に対応できる見込みです。インドネシアでは、カーギル社の2024年における混合プラント拡張により、現地ブランド向け増粘剤の供給が効率化され、地域メーカーは輸入依存度を低減しつつ、高品質増粘剤への需要増に対応可能となります。

北米では着実な成長が見られる一方、米国では特にボストンからサンディエゴに及ぶバイオテクノロジー回廊において、ペクチンを活用した3Dバイオプリンティング試験で独自の地位を確立しつつあります。この革新技術は医療・製薬分野に革命をもたらすと期待され、ペクチンの先端応用における同地域の主導的立場をさらに確固たるものにするでしょう。

ラテンアメリカの状況は対照的です。ブラジルは重要な果皮原料の供給源である一方、サプライチェーンの非効率性と生産量の変動により、国内の輸出不足に直面しています。一方、メキシコの菓子類業界は、ますます厳格化している米国のビーガン輸入基準を満たすためにペクチンを活用しています。中東およびアフリカでの採用は徐々に進んでいますが、湾岸協力会議(GCC)諸国における多国籍飲料メーカーからの投資によって後押しされています。これらの投資は、現地生産施設の開発を推進し、この地域におけるペクチンベースの製品の入手可能性を高めています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3か月間のアナリストサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- 天然およびクリーンラベル原料への需要

- 包装食品製品の消費増加

- 植物由来・ビーガン菓子類への移行拡大

- ペクチンを活用した3Dバイオプリンティングおよび個別化医療の拡大

- 生分解性食品包装フィルムにおけるペクチンの採用

- 農業廃棄物を活用する循環型経済規制

- 市場抑制要因

- 低コスト合成ヒドロコロイドの入手可能性

- 柑橘類の供給と価格変動の不安定さ

- 工業規模の「グリーン」抽出技術における高額な設備投資

- 酸ベース抽出法のカーボンフットプリントに対するESG監査

- サプライチェーン分析

- 規制情勢

- テクノロジーの展望

- ポーターのファイブフォース

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場規模と成長予測

- ソース別

- 柑橘類

- アップル

- その他の情報源

- タイプ別

- 高メトキシル(HM)ペクチン

- 低メトキシル(LM)ペクチン

- カテゴリー別

- 従来型

- オーガニック/ナチュラル

- 用途別

- 飲食品

- ジャム、ゼリー、および保存食品

- 焼き菓子

- 乳製品

- その他の飲食品

- 美容・パーソナルケア

- 医薬品

- その他の用途

- 飲食品

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- その他北米地域

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他欧州地域

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- その他アジア太平洋地域

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 中東・アフリカ

- 南アフリカ

- アラブ首長国連邦

- その他中東・アフリカ地域

- 北米

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場ランキング分析

- 企業プロファイル

- International Flavors & Fragrances

- Cargill Incorporated

- Herbstreith & Fox Corporate Group

- Silvateam S.p.A.

- DSM Firmenich

- Ingredion Incorporated

- Tate & Lyle PLC

- Lucid Colloids Ltd

- Pacific Pectin Inc.

- Naturex-Givaudan

- Yantai Andre Pectin Co.

- CEAMSA

- CP Kelco Denmark A/S

- Qingdao Reborn Materials

- Hainan YINmore Bio-Tech

- Shandong Jincheng Bio-Pharma

- Krishna Pectins Pvt. Ltd.

- Zhejiang Mingland Biotech