|

市場調査レポート

商品コード

1685692

アルコール原料- 市場シェア分析、産業動向・統計、成長予測(2025年~2030年)Alcohol Ingredients - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| アルコール原料- 市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 156 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

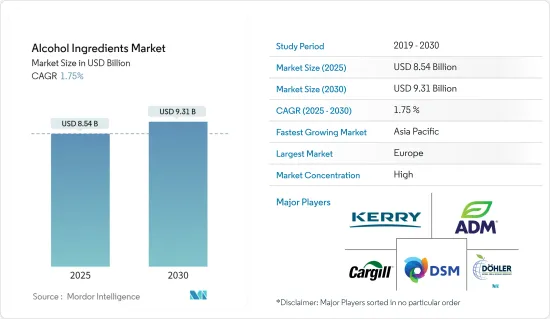

アルコール原料の市場規模は2025年に85億4,000万米ドルと推定され、予測期間中(2025年~2030年)のCAGRは1.75%で、2030年には93億1,000万米ドルに達すると予測されています。

ルーカス・ボルス社の年次報告書によると、近年、世界中でアルコール消費量が大幅に増加しています。アルコール飲料の生産、流通、販売、マーケティングを専門とするオランダの公開会社であるボルスは、西欧での収益が2016年の3,440万ユーロから2021年には4,211万ユーロに増加すると報告しています。しかし、COVID-19の影響で同社の収益は3,075万ユーロに減少しました。しかし、パンデミック後、市場は回復し、原料メーカーはアルコール飲料部門からの急増する需要に対応するために増産しています。さらに、消費者のクラフトビール志向が高まっており、その結果、世界中でクラフトビールの醸造所が増加しており、その店舗数は英国が最も多く、次いでドイツ、イタリアなどとなっています。

これもまた、世界のアルコール原料市場を牽引する要因となっています。さらに、需要の高まりを受けて、メーカーは生産能力を増強しています。例えば、2021年8月、Angel Yeastは買収と生産に多額の投資を行いました。中国本土の投資会社であるShandong Lufa Holding社とともに、同社はBio Sunkeen社を6,000万人民元(920万米ドル)で買収したと発表しました。さらに、メーカーはアルコール飲料の品質を高めるため、着色料、酵母、香料・塩、酵素など、さまざまな種類の原料を革新しています。

アルコール原料市場の動向

クラフトビール需要の増加

ここ数年、クラフトビールや蒸留酒の需要が大きく伸びています。世界中の消費者が個性的で風味豊かなビールを求めています。これがアルコール原料市場をビール市場へと押し上げています。醸造業界は、麦芽原料エキス補助/穀物、ホップ、ビール酵母、ビール添加物の5つの主要原料を利用します。澱粉源の混合物は、トウモロコシ(コーン)、米、砂糖などの二次糖類とともに使用されることがあり、これらは特に麦芽の低コスト代替品として使用される場合、しばしば補助添加物と呼ばれます。あまり広く使用されていないデンプン源としては、アフリカのキビ、ソルガム、キャッサバの根、ブラジルのジャガイモ、メキシコのリュウゼツランなどがあります。醸造用モルトエキスは最高品質の醸造用麦芽を使用し、特殊麦芽を使用することで色と風味を加えています。これにより、ビールに特定の醸造スタイルに求められる独特の個性と風味が生まれます。これらの麦芽は、多くの場合、窯の中でより長い時間、より高い温度で焙煎され、出来上がったビールに深みと複雑さを加えます。さらに、地ビールの開発とクラフトビールの生産量の増加が、クラフトビールの需要拡大につながりました。

アジア太平洋は引き続き急成長地域

特にアジア太平洋はクラフトビール市場にとって計り知れない潜在力を秘めており、現地の味覚や嗜好と融合した西洋化されたクラフトビールへの需要が旺盛です。伝統的なアルコールから輸入アルコールへと消費者の嗜好がシフトしていることが、この地域のアルコール飲料市場成長の原動力の一つとなっています。例えば、農林水産省によると、2021年には日本円で約1,880億円のワインが日本に輸入され、輸入量の大半を占めています。果実酒は日本の各都道府県で生産されていたにもかかわらず、輸入品が国内需要の大半をカバーしていました。中国のような国では、ボルドーのような有名なブドウ産地のワインが、伝統と名声のために消費者に好まれます。ウイスキー、コニャック、輸入ワインは、消費者の高級志向に伴い、この地域全体で人気が高まっています。

アルコール原料業界の概要

世界のアルコール原料市場は、複数の国内および世界企業が市場を独占しているため、非常に断片化されています。しかし、DSM、ADM、Cargill、Dohler Groupといった世界の主要企業が、国内メーカーとともに存在感を示しています。麦芽原料メーカーの間で最も採用されている戦略は拡大であり、製品革新、提携、M&Aがそれに続きます。大手メーカーは、市場の他のメーカーに差をつけるため、生産能力を拡大し、戦略的に輸出設備の補完を計画しています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場促進要因

- 市場抑制要因

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手・消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- 原料タイプ

- 酵母

- 酵素

- 着色料

- 香料と塩

- 飲料タイプ

- ビール

- スピリッツ

- ワイン

- ウィスキー

- ブランデー

- 地域

- 北米

- 米国

- カナダ

- メキシコ

- その他の北米

- 欧州

- スペイン

- 英国

- ドイツ

- フランス

- イタリア

- ロシア

- その他の欧州

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- その他のアジア太平洋

- 南米

- ブラジル

- アルゼンチン

- その他の南米

- 中東・アフリカ

- 南アフリカ

- アラブ首長国連邦

- その他の中東・アフリカ

- 北米

第6章 競合情勢

- 最も採用されている戦略

- 市場シェア分析

- 企業プロファイル

- Cargill, Incorporated

- Archer Daniels Midland Company

- Ashland Inc.

- D.D. Williamson & Co. Inc.

- Koninklijke Dsm NV

- Kerry Group PLC

- Treatt PLC

- Chr Hansen Holdings A/S

- Sensient Technologies Corporation

- Dohler Group

第7章 市場機会と今後の動向

The Alcohol Ingredients Market size is estimated at USD 8.54 billion in 2025, and is expected to reach USD 9.31 billion by 2030, at a CAGR of 1.75% during the forecast period (2025-2030).

According to Lucas Bols's annual reports, in recent years, alcohol consumption has increased significantly around the globe. Bols, a Dutch public company specializing in producing, distributing, selling, and marketing alcoholic beverages, reported a revenue increase in Western Europe from EUR 34.4 million in 2016 to EUR 42.11 million in 2021. But the company's revenue dropped to EUR 30.75 million as a result of COVID-19. However, post-pandemic, the market has recovered, and ingredient manufacturers are increasing their production to meet the burgeoning demand coming from the alcoholic beverage sector. Moreover, consumers are increasingly inclined toward craft beer, which has resulted in an increasing number of craft breweries around the globe, with the highest number of outlets in the United Kingdom, followed by Germany, Italy, and others.

This is yet another factor driving the alcohol ingredients market around the globe. Additionally, manufacturers are increasing their production capacity owing to the rising demand. For instance, in August 2021, Angel Yeast invested heavily in acquisitions and production. Together with Shandong Lufa Holding company, a local investment corporation within the Chinese mainland, the company announced the acquisition of Bio Sunkeen for RMB 60 million (USD 9.2 million). Additionally, manufacturers are innovating various types of ingredients colorants, yeast, flavors & salt, enzymes, and others to enhance the quality of alcoholic beverages.

Alcohol Ingredients Market Trends

Increasing Demand For Craft Beer

The demand for the craft brewing and distilling industries experienced significant growth during the past few years. Consumers across the world are seeking distinctive and flavored beers. This is pushing the alcohol ingredients market into the beer market space. The brewing industry utilizes five major ingredients, namely malt ingredient extract adjuncts/grains, hops, beer yeast, and beer additives. A mixture of starch sources may be used, with a secondary saccharide, such as maize (corn), rice, or sugar, as these are often termed adjuncts, especially when used as a lower-cost substitute for malted barley. Less widely used starch sources include millet, sorghum, and cassava root in Africa, potato in Brazil, and agave in Mexico, among others. Brewing-grade malt extracts are made with the highest-quality brewing malts and get additional colors and flavors from using specialty malts. This gives beer the unique character and flavor desired for the particular style of brew. These malts often have a longer time in the kiln, at higher temperatures, or get roasted to add depth and complexity to the resulting beer. Moreover, the increasing development of microbreweries and the growing production of craft beer led to a growing demand for craft beers.

Asia-Pacific Remains the Fastest Growing Region

Asia-Pacific, in particular, holds immense potential for the craft beer market, with robust demand for Westernized craft beer that is blended with local tastes and preferences. Shift in consumer preferences from traditional alcohol toward imported alcohol has been one of the driving factors for the growth of the alcoholic beverage market in the region. For instance, according to the Ministry of Agriculture, Forestry, and Fisheries, in 2021, approximately 188 billion Japanese Yen of wine was imported to Japan, making up most of the imports. Despite the fact that fruit wine was produced in various prefectures in Japan, imports covered the majority of domestic demand. In countries like China, consumers are inclined toward wines manufactured by famous vineyard regions, such as Bordeaux, owing to renowned heritage and prestige. Whiskies, Cognacs, and imported wines are becoming popular across the region as consumers are more inclined toward premium products.

Alcohol Ingredients Industry Overview

The global alcohol ingredient market is highly fragmented due to the dominance of several local and global players present in the market. Nonetheless, the market exhibits a strong presence of global key players, such as DSM, ADM, Cargill, and Dohler Group, alongside other domestic producers. Expansion remained the most adopted strategy among malt ingredient manufacturers, holding a major chunk of total strategies, followed by product innovation, partnership, and merger and acquisition. The major players are expanding their production capacities and strategically planning to supplement their export facilities in order to stand out among other manufacturers in the market.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Drivers

- 4.2 Market Restraints

- 4.3 Porter's Five Forces Analysis

- 4.3.1 Threat of New Entrants

- 4.3.2 Bargaining Power of Buyers/Consumers

- 4.3.3 Bargaining Power of Suppliers

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Ingredient Type

- 5.1.1 Yeast

- 5.1.2 Enzymes

- 5.1.3 Colorants

- 5.1.4 Flavors & Salts

- 5.2 Beverage Type

- 5.2.1 Beer

- 5.2.2 Spirits

- 5.2.3 Wine

- 5.2.4 Whisky

- 5.2.5 Brandy

- 5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.1.4 Rest of North America

- 5.3.2 Europe

- 5.3.2.1 Spain

- 5.3.2.2 United Kingdom

- 5.3.2.3 Germany

- 5.3.2.4 France

- 5.3.2.5 Italy

- 5.3.2.6 Russia

- 5.3.2.7 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 Japan

- 5.3.3.3 India

- 5.3.3.4 Australia

- 5.3.3.5 Rest of Asia-Pacific

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 South Africa

- 5.3.5.2 United Arab Emirates

- 5.3.5.3 Rest of Middle East and Africa

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Most Adopted Strategies

- 6.2 Market Share Analysis

- 6.3 Company Profiles

- 6.3.1 Cargill, Incorporated

- 6.3.2 Archer Daniels Midland Company

- 6.3.3 Ashland Inc.

- 6.3.4 D.D. Williamson & Co. Inc.

- 6.3.5 Koninklijke Dsm NV

- 6.3.6 Kerry Group PLC

- 6.3.7 Treatt PLC

- 6.3.8 Chr Hansen Holdings A/S

- 6.3.9 Sensient Technologies Corporation

- 6.3.10 Dohler Group