|

市場調査レポート

商品コード

1640515

金属キャップ・クロージャー:市場シェア分析、産業動向と統計、成長予測(2025~2030年)Metal Caps & Closures - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 金属キャップ・クロージャー:市場シェア分析、産業動向と統計、成長予測(2025~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 127 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

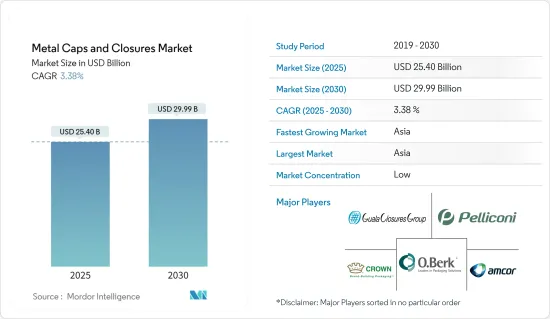

金属キャップ・クロージャー市場規模は2025年に254億米ドルと推定・予測され、予測期間中(2025~2030年)のCAGRは3.38%で、2030年には299億9,000万米ドルに達すると予測されます。

金属キャップ・クロージャー市場は、飲食品需要の増加により予測期間中に急拡大すると予測されます。アルコール飲料、ビール、パン、鶏肉・魚、調理済み食品、乳製品などの需要が高まっています。さらに、プラスチック規制のため、清涼飲料包装ベンダーは飲料包装に金属クラウンキャップを好んでおり、市場成長を牽引しています。

主要ハイライト

- 環境に優しい製品の使用に関する懸念の高まりが、金属キャップ・クロージャーの採用を後押ししています。プラスチックベースのキャップは金属キャップに高い脅威を与えるが、プラスチックキャップ市場は環境問題に関する高い脅威を目の当たりにしています。これが金属キャップ・クロージャーの機会を生み出しています。近年、いくつかの企業がプラスチックベースのキャップ・クロージャーを金属に置き換えています。

- さらに、金属キャップやクロージャーはロゴやその他のデザインでブランド化することができ、特徴的なブランドをアピールすることで需要を高めています。さらに、適応性のあるクラウンキャップは、ネジ式のボトルネックと組み合わせたときに最適なフィット感を与えるユニークな金属で構成されています。クラウン・キャップはリーズナブルな価格で、非常に機能的で、使い方が簡単で、高速で装着でき、本物の不正開封防止機能を備えています。

- 金属キャップ・クロージャーは、無菌で一般的に多層材料で作られているため、製薬産業でもよく利用されています。産業で最も一般的に使用されている金属キャップは、スチールとアルミニウムで構成されています。

- さらに、アルミニウムは、無地、エンボス加工、着色、天然など、さまざまなバリエーションで作られています。その結果、医薬品包装は消費者の需要に応じて提供される可能性があります。

- 小児用、付加価値用、高齢者用クロージャーの市場は、急速に拡大する製薬産業や、規制改革によってメーカーが優れた品質のキャップやクロージャーを製造するようになったことが原動力になると予想されます。

- しかし、プラスチックや木材などで作られた他のクロージャーシステムの存在が市場抑制要因として作用し、予測期間中の金属キャップ・クロージャー市場の成長を阻むと予想されます。

金属キャップ・クロージャー市場の動向

医薬品用途が成長の可能性を提供

- 金属キャップ・クロージャーは無菌であり、一般に層状材料で構成されているため、医薬品セグメントで主に使用されています。スチール製とアルミニウム製の金属キャップがこのセグメントで主に使用されています。また、アルミニウムは、天然、カラー、無地、エンボスなど、先進的カスタマイズが可能です。このように、医薬品包装は消費者のニーズに応じて供給することができます。

- 医薬品の販売と生産が急速に伸びていることと、規制の変更により、小児用、付加価値用、高齢者用のクロージャーがさらに好まれるようになっており、これが予測される期間の市場を牽引すると予想されます。世界保健機関(WHO)は、世界で販売される医薬品の3分の1が違法なものであると推定しています。偽造医薬品によるリスクの増大は、効率的な偽造防止ソリューションの必要性を生み出し、偽造防止用クロージャーの採用を後押ししています。

- 医薬品産業では、ゴム製クロージャーが医薬品を汚染する傾向があるため、アルミニウム製クロージャーの採用が増加しています。汚染はエラストマー容器のクロージャー部品に起因します。考えられる汚染物質には微生物、内毒素、化学品などがあります。2022年度には、166の製造拠点から912件の医薬品リコールが発生し、過去5年間で最多を記録しました。

- データによると、これらのリコールの最大の欠陥グループは、CDERが例年報告しているように、現行の適正製造規範(CGMP)逸脱であることに変わりはないです。リコールされた製品の大半は、倉庫における温度管理と保管に問題があったためです。報告書では、このような条件が製品の劣化を引き起こし、保存期間、安全性、有効性に悪影響を及ぼす可能性があることを強調しています。

- さらに、金属キャップ・クロージャーの需要は、シロップボトルセグメントでは、その使用において一般的な規制のため、いくつかの課題を確認する可能性があります。ハーブ医薬品(HMP)は最近重要性を増しており、様々な病気の予防や治療に広く使用されています。

アジア太平洋が最も速い成長を確認する

- アジア太平洋は、中国とインドという人口の多い2カ国の存在により、最も速い成長が見込まれています。この2カ国では、可処分所得の増加が金属キャップ・クロージャー市場の成長を補うと考えられます。

- アルコールから成るインドの飲料セクターは、最も多様なセクターのひとつです。この産業は、天候に関連した広大な地域の影響を強く受けています。それに伴い、飲料を封じ込め、輸送を可能にし、機械的ストレスや材料の損失から飲料を保護する包装機能が不可欠となっています。Banco do Nordesteの調査によると、2020年のインドのアルコール消費量は48億6,000万リットルでした。2024年には62億1,000万リットルに達すると予想されています。

- 中国の蒸留酒市場は継続的に拡大しており、包装ソリューションに対する高い需要につながっています。こうした売上高は、中国国内の飲料包装メーカーにとって大きな機会となります。外国人投資家は、このような市場セグメントの大きな可能性を認識しています。さらに、中国からのアルコール飲料の輸入額の増加が、飲料用キャップ・クロージャーの市場を押し上げています。2022年10月に発表された最近のデータによると、中国の税関データによると、中国は7月から9月にかけて北朝鮮に300万米ドル近いワインと酒類を輸出しました。

- サステイナブル飲料用包装の動向は東南アジアで加速しており、これは持続可能性に対する消費者の意識の高まりと様々な利害関係者による関心の高まりに後押しされたものです。一部のメーカーは、プラスチックをよりサステイナブル材料に置き換えることを選択しています。

- 包装食品と飲食品の需要の大幅な増加と、包装された消耗品を長期間新鮮に保つためにキャップ・クロージャーが果たす重要な役割は、これらの地域の市場を押し上げる可能性が高いです。

金属キャップ・クロージャー産業概要

世界の金属キャップ・クロージャー市場は、国際的なベンダーの存在により、非常に細分化され競合が激しいです。この市場の主要企業としては、Crown Holdings、O.Berk Company、Guala Closures S.P.A.、Amcor P.L.C.などが挙げられます。市場では、製品の差別化、ポートフォリオ、価格設定の面で激しい競争が繰り広げられています。付加価値の高いクロージャーや耐タンパー性に対する需要の高まりは、医薬品や飲料を中心とした様々なセグメントでのメタルキャップやクロージャーの使用を増大させると考えられます。

2022年7月、様々なタイプのボトル用クロージャーを製造するGuala Closuresは、ヴィチェンツァに本拠を置くハイエンドクロージャーの専門企業であるLabrentaを買収しました。この買収はGuala Closuresにとって非常に重要であり、高級品セグメントでのリーチを拡大し、産業の世界的リーダーとなることに貢献しました。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 産業バリューチェーン分析

- 産業の魅力-ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場力学

- 市場促進要因

- サステイナブル包装材料へのニーズの高まりに伴う飲料消費の増加

- その他のクロージャー材料に比べ優れた特性

- 市場抑制要因

- その他のタイプのクロージャー材料の高い採用率

第6章 市場セグメンテーション

- 材料タイプ別

- アルミニウム

- スチール

- 錫

- クロージャータイプ別

- クラウンキャップ

- スクリューキャップ

- ツイストメタルキャップ

- その他のキャップ(イージーオープンエンド、ROPPメタルキャップ)

- エンドユーザー産業別

- 食品

- 飲料

- アルコール飲料

- ノンアルコール

- 医薬品

- パーソナルケア

- その他

- 地域別

- 北米

- 欧州

- アジア

- オーストラリア・ニュージーランド

- ラテンアメリカ

- 中東・アフリカ

第7章 競合情勢

- 企業プロファイル

- Crown Holdings Inc.

- O.Berk Company

- Guala Closures S.P.A.

- Pelliconi & C. SpA

- Nippon Closures Co. Ltd

- Silgan White Cap LLC

- Sks Bottle & Packaging Inc.

- Amcor PLC

- Qorpak(Berlin Packaging)

- Alameda Packaging LLC

- Closure Systems International Inc(CSI)

第8章 投資分析

第9章 市場の将来

The Metal Caps & Closures Market size is estimated at USD 25.40 billion in 2025, and is expected to reach USD 29.99 billion by 2030, at a CAGR of 3.38% during the forecast period (2025-2030).

The market for metal caps and closures is predicted to expand rapidly during the forecast period due to the increased demand for food and beverages. There is a rising demand for alcoholic drinks, beer, bread, poultry and fish, ready-to-eat meals, dairy goods, etc. Moreover, due to plastic regulations, soft drink packaging vendors prefer metal crown caps for beverage packaging, driving the market growth.

Key Highlights

- The growing concerns regarding the usage of environment-friendly products have boosted the adoption of metal caps and closures. Though plastic-based caps pose a high threat to metal caps, the plastic caps market is witnessing high threats regarding environmental problems. This has been creating the opportunity for metal caps and closures. Several companies in recent years have been replacing their plastic-based caps and closures with metal.

- Further, metal caps and closures can be branded with logos or other designs, increasing demand for them by promoting the distinctive brand. Moreover, the adaptable crown caps are composed of a unique metal that gives the optimum fit when combined with a threaded bottleneck. Crown caps are reasonably priced, very functional, simple to use, allow for high-speed application, and provide genuine tamper protection.

- Metal caps and closures are also often utilized in the pharmaceutical industry since they are sterile and typically made of multilayer materials. The most common metal caps used in the industry are comprised of steel and aluminum.

- Additionally, aluminum is made in various variations, including plain or embossed, colored, or natural. As a result, pharmaceutical packaging may be provided in accordance with consumer demand.

- The market for child-resistant, value-added, and senior-friendly closures is expected to be driven by the rapidly expanding pharmaceutical industry as well as regulatory reforms, which have encouraged manufacturers to produce superior-quality caps and closures.

- However, the presence of other closure systems made of plastics, wood, etc., is expected to act as a restraint and challenge the growth of the metal closures market over the forecast period.

Metal Caps and Closures Market Trends

Pharmaceutical Application Offers Potential Growth

- Metal caps and closures are predominantly used in the pharmaceutical sector as they are sterile and are generally composed of layered material. Metals caps made of steel and aluminum are mostly used in the sector. Besides, aluminum can be highly customizable: natural or colored, plain or embossed. Thus, pharmaceutical packaging can be supplied according to the consumers' needs.

- The rapidly growing pharmaceutical sales and production and the regulatory changes further favor child-resistant, value-added, and senior-friendly closures, which are anticipated to drive the market in the foreseen period. The World Health Organization (WHO) estimated that one-third of all medicines sold worldwide are illegitimate. The increasing risks from falsified drugs are creating the need for efficient anti-counterfeiting solutions, boosting the adoption of anti-counterfeiting closures.

- The adaptation of aluminum closures in the pharmaceutical industry is on the rise, as its rubber counterparts tend to contaminate the drugs. The contamination is attributable to elastomeric container closure components. Possible contaminants include microorganisms, endotoxins, and chemicals. In the fiscal year 2022, 912 drug recalls were generated by 166 manufacturing sites, marking the highest number of recalls in the past five years.

- The data indicates that the largest defect group for these recalls remains current good manufacturing practice (CGMP) deviations, as reported in previous years by CDER. The majority of the products were recalled due to issues with temperature control and storage in warehouses. The report highlights the fact that these conditions can cause degradation of the product, leading to a negative impact on its shelf-life, safety, or effectiveness.

- Further, the demand for metal caps and closures may witness a few challenges in the syrup bottle sector owing to the regulations prevailing in their usage. Herbal medicinal products (HMP) have recently gained importance and are extensively used to prevent and treat various ailments.

Asia-Pacific to Witness the Fastest Growth

- Asia-Pacific is expected to witness the fastest growth because of the presence of two highly populated countries, i.e., China and India. In these two countries, the increase in disposable income will supplement the growth of the metal caps and closures market.

- The Indian beverage sector, consisting of alcohol, is one of the most diverse sectors. The industry is highly influenced by the country's vast geography associated with the weather. With it comes the imperative of packaging function to contain beverages, enabling transportation, and protecting beverages against mechanical stress and material loss. According to a study performed by Banco do Nordeste, alcohol consumption in India was 4.86 billion liters in 2020. The consumption is expected to reach 6.21 billion liters in 2024.

- China's spirits market is expanding continuously, leading to a high demand for packaging solutions. Such turnover represents an enormous opportunity for domestic producers in Chinese beverage packaging. Foreign investors have recognized the huge potential of such a market segment. Moreover, the growing import value of alcoholic drinks from China has boosted the market for caps and closures for beverages. Recent data published in October 2022 showed that China exported nearly USD 3 million of wine and liquor to North Korea from July to September, according to Chinese customs data.

- The trend for sustainable beverage packaging is accelerating in Southeast Asia, buoyed by greater consumer awareness of sustainability and increased focus by various stakeholders, with governments incentivizing a shift towards a circular economy and manufacturers focusing on recycling, packaging reduction, and the adoption of more sustainable packaging alternatives. Some manufacturers are opting to replace plastics with more sustainable materials.

- The vast rise in the demand for packaged foods and beverages and the critical role played by caps and closures in keeping packaged consumables fresh for extended periods are likely to boost the market in these regions.

Metal Caps and Closures Industry Overview

The global metal caps and closures market is highly fragmented and competitive due to the presence of international vendors. Some of the key players in this market are Crown Holdings, O.Berk Company, Guala Closures S.P.A., and Amcor P.L.C., amongst others. Intense competition prevails in the market in terms of product differentiation, portfolio, and pricing. The rising demand for value-added closures and tamper resistance properties will augment the usage of metal caps and closures in various segments, primarily pharmaceuticals and beverages.

In July 2022, Guala Closures, a company that produced closures for various types of bottles, acquired Labrenta, a high-end closure specialist based in Vicenza. This acquisition was crucial for Guala Closures as it helped the company expand its reach in the luxury segment, thus making it a world leader in the industry.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Consumers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitutes

- 4.3.5 Intensity of Competitive Rivalry

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing Consumption of Beverages with a Rising Need for Sustainable Packaging Materials

- 5.1.2 Superior Properties Compared to Other Closure Materials

- 5.2 Market Restraints

- 5.2.1 High Adoption Rate of Other Types of Closure Materials

6 MARKET SEGMENTATION

- 6.1 By Material Type

- 6.1.1 Aluminium

- 6.1.2 Steel

- 6.1.3 Tin

- 6.2 By Closures Type

- 6.2.1 Crown Caps

- 6.2.2 Screw Caps

- 6.2.3 Twist Metal Caps

- 6.2.4 Other Closures Types (Easy Open Ends, ROPP Metal Caps)

- 6.3 By End-User Industry

- 6.3.1 Food

- 6.3.2 Beverages

- 6.3.2.1 Alcoholic

- 6.3.2.2 Non-Alcoholic

- 6.3.3 Pharmaceuticals

- 6.3.4 Personal Care

- 6.3.5 Other End-User Industries

- 6.4 By Geography

- 6.4.1 North America

- 6.4.2 Europe

- 6.4.3 Asia

- 6.4.4 Australia and New Zealand

- 6.4.5 Latin America

- 6.4.6 Middle East and Africa

7 Competitive Landscape

- 7.1 Company Profiles

- 7.1.1 Crown Holdings Inc.

- 7.1.2 O.Berk Company

- 7.1.3 Guala Closures S.P.A.

- 7.1.4 Pelliconi & C. SpA

- 7.1.5 Nippon Closures Co. Ltd

- 7.1.6 Silgan White Cap LLC

- 7.1.7 Sks Bottle & Packaging Inc.

- 7.1.8 Amcor PLC

- 7.1.9 Qorpak (Berlin Packaging)

- 7.1.10 Alameda Packaging LLC

- 7.1.11 Closure Systems International Inc (CSI)